Netflix Update: Losing Its Grip or Pulling Away?

Get smarter on investing, business, and personal finance in 5 minutes.

Business Update

Netflix shares are down 42% over the past year, and the shares currently trade at almost the same price as they did during their 2021 high.

The shares have come down a lot in price, especially given that the business has improved a lot over the past 5 years.

So this week’s Five Minute Money is going to be an update on Netflix, providing some news, some updates, some updated valuation, as well as just emphasizing some of the strategic advantages Netflix has versus competition.

The Warner Brothers and Paramount Merger.

The first thing we're going to kick off with is on the acquisition front, mostly a section of non-news, that is things that didn't happen.

Most front and center news is the Warner Brothers acquisition that Netflix did not close.

They gave Paramount the opportunity to come up with a better offer, and once they did, Netflix walked away from the deal, taking a $2.8bn dollar breakup fee.

Warner Brothers was ultimately acquired by Paramount Sky Studios for a $110bn, with the combined company now carrying $80bn of debt.

You don't need any fancy math to know that is a lot of debt, especially on a traditional media conglomerate trying to transition from a legacy linear TV business to more of a streamer.

It's worth emphasizing that this deal has not closed yet.

The Justice Department gave its blessings, but every state is also allowed to potentially challenge the merger.

California, led by Attorney General Rob Bonta, has been vocal in being suspicious that this transaction is going to be a net good for consumers.

And there's also some politics at play, because Paramount is controlled by the Ellison family, who have been seen as cozying up to Trump, raising suspicions among more Democratic states.

States will eventually probably band together and attempt to file an injunction, which could stop the merger in the meantime while it goes through litigation.

Even if it does ultimately close, it could lead to concessions and asset divestitures.

The UK and the EU also haven't said anything about whether or not this merger will be approved, and the FCC needs to approve any move in broadcast licenses.

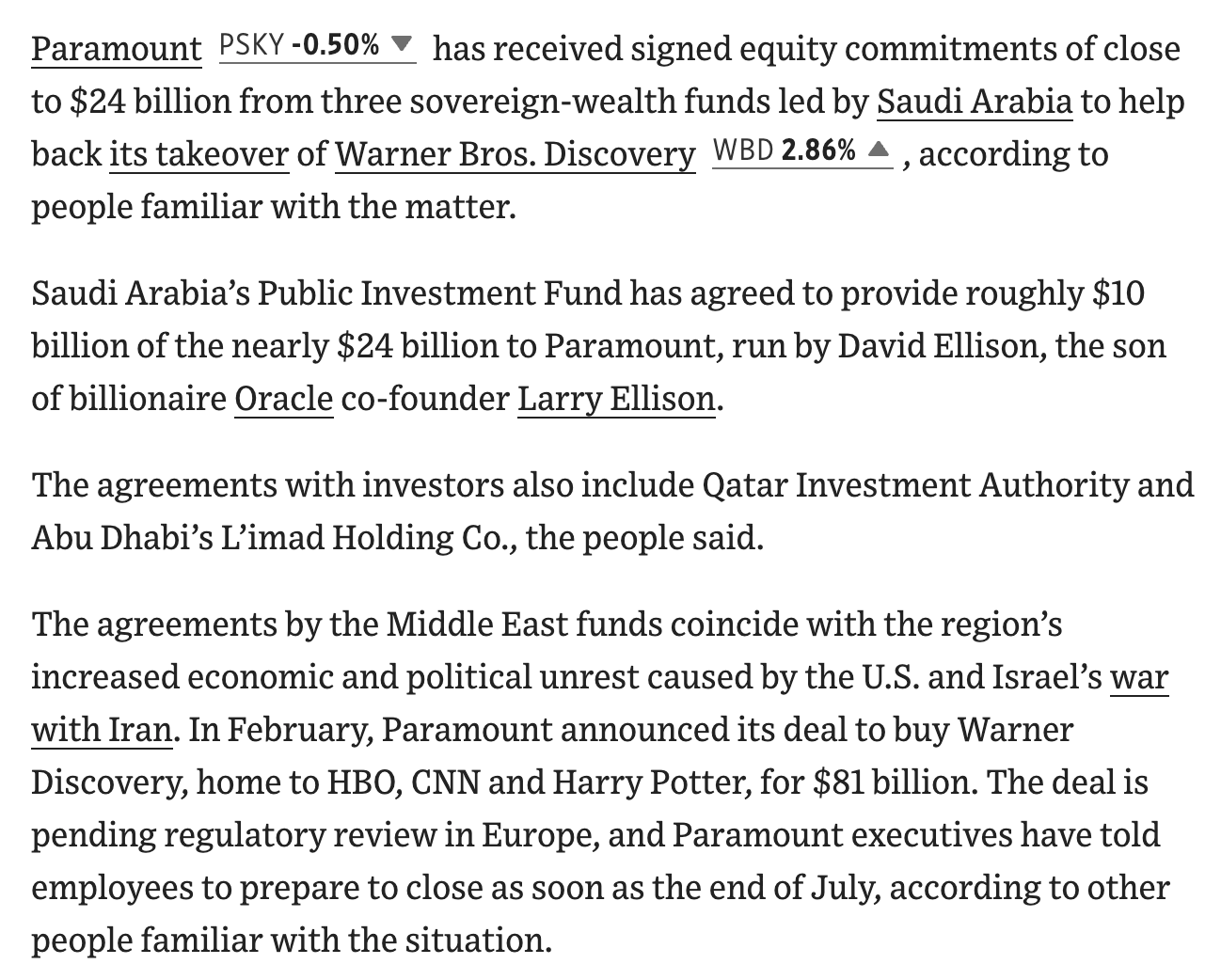

Their concern is mostly the $24bn in funding coming from Saudi Arabia, Qatar, and the UAE, and the risk that they could pressure the company to censor content.

And by the way, if the deal doesn't close by September 13th, they will start to pay that ticking fee, about $650 million dollars a quarter, basically just making the deal more expensive for Paramount.

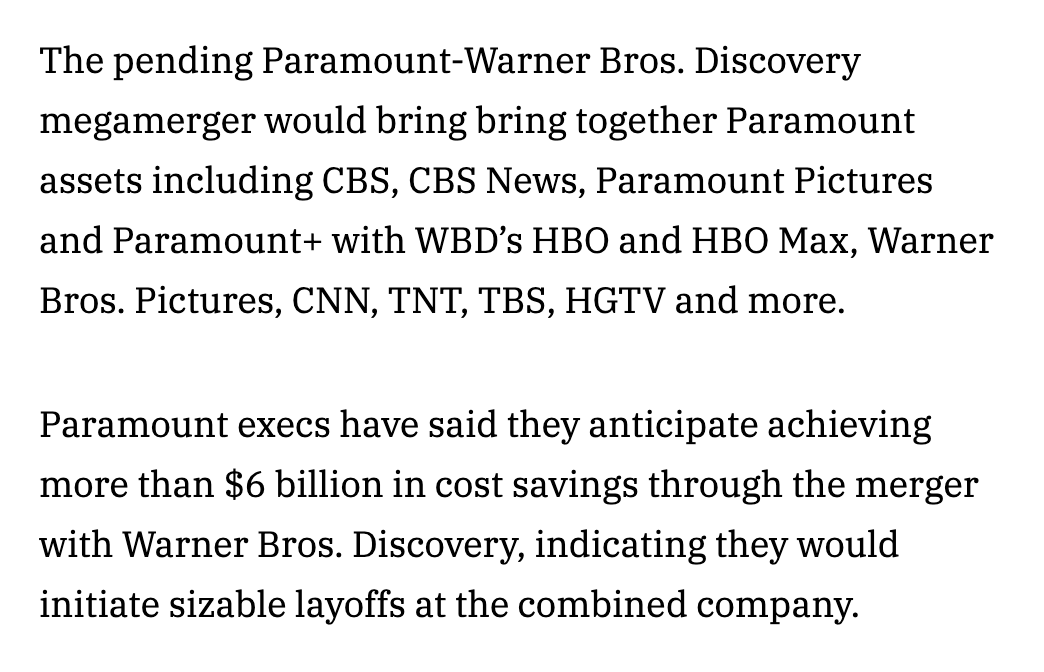

The big thing from Netflix's perspective is that's a distracted competitor with a lot of debt, unable to make all of the moves they were hoping to make in terms of rationalizing their cost synergies.

When Paramount did this deal, they were hoping for $6bn in cost synergies, which would bring their EBITDA to about $18bn and a net debt to EBITDA ratio of 4.2.

And we know from history that hoped-for synergies don't always become realized.

As a combined company, they'll have about 200 million direct-to-consumer subscribers and ~$30bn dollars in content spend.

During the merger, they said they weren't going to cut content costs, but needing to look for areas to save money if synergies don't come into play, I think their content spend could potentially come down.

However, it's not easy to decrease because that content is going all over the place, not a single unified platform like Netflix.

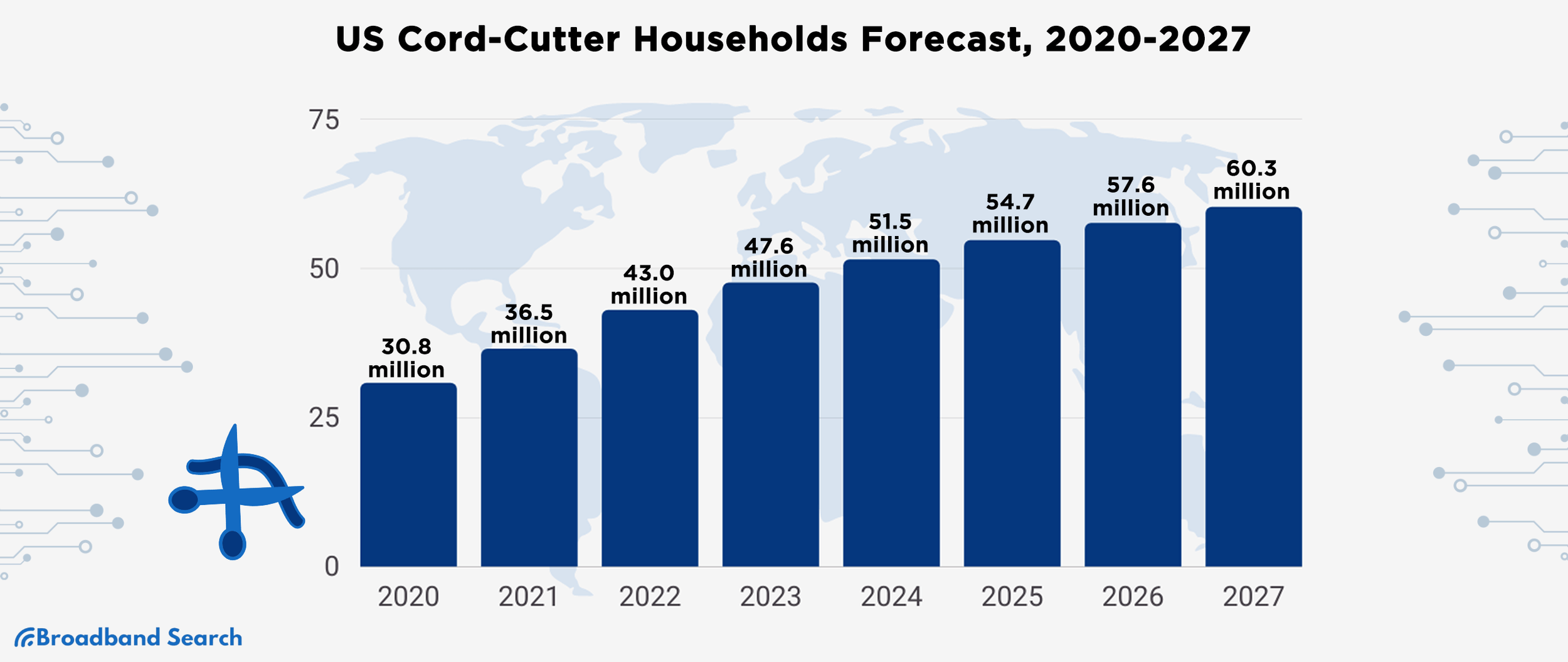

They don't just have Paramount Plus and HBO Max; they also have all these different TV stations and an entire movies business, all currently being pressured by cord-cutting.

Even though cord-cutting has been an ongoing trend for a long time, a lot of their revenues and financial viability is still predicated on these older legacy TV businesses.

The big takeaway for Netflix shareholders is that it's actually a good thing that Netflix didn't just try to outbid and win an auction.

As Warren Buffett says, you don't really want to be the one winning an auction, because that means you overpaid.

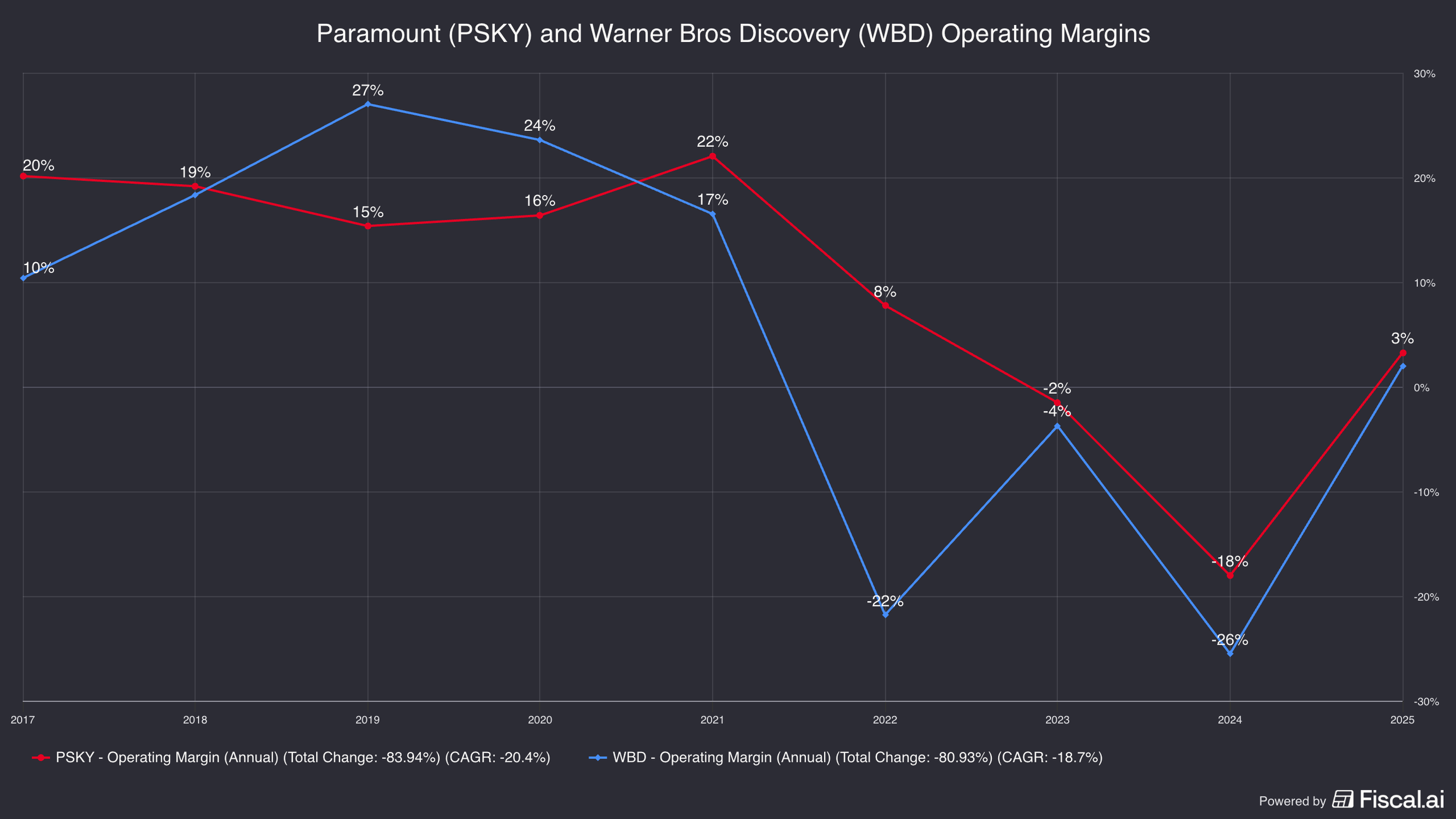

They paid $110bn with a lot of debt on top, and both Paramount and Warner Brothers on their own had negative operating margins over the last 12 months.

Acquisition Activity: What Netflix Did and Didn't Do.

The other news that's been happening, and this in my opinion is basically because Netflix stock has been down a lot, is investors looking for a reason to understand why the price is down and trying to attribute different news to it.

Lionsgate Acquisition Rumor.

One thing that popped up was that Netflix was trying to acquire Lionsgate.

Investors interpreted that to mean they feel like they need more content since losing the Warner Brothers deal.

That's not true on two levels.

One, they put out a statement saying they weren't trying to bid on Lionsgate.

But on top of that, I don't think it's true they need more content.

Netflix's churn is the lowest of all the video streaming players.

I think that was the market grasping for straws to figure out why the stock price was down.

Roku Bid.

Then there was acquisition news about a bid for Roku.

Most people don't know this, but Roku was actually incubated inside of Netflix originally.

Why would they want to acquire it many years later?

It mostly has to do with their push into advertising.

When you own that device, you're getting more proprietary data and controlling that platform, giving you more ability to show ads and sell advertising.

But they stepped out of that.

I think it's a good thing that management is interested in acquisitions and exploring them, but shows they're very price-disciplined.

They're not trying to be empire builders acquiring Warner Brothers and Lionsgate and Roku at any cost.

Instead, they're thinking about: what is the ROI to our shareholders?

Does it allow us to increase ARPU?

Is it cheaper if we just build this ourselves?

These are the exact questions you would want to see a management team asking.

The Interpositive Acquisition.

The one acquisition they did do, back in March, was Interpositive, an AI company co-founded by Ben Affleck.

It's about using AI in post-production of filming a video, taking content that's already been made and using AI models to help improve how the content looks, basically special effects.

That acquisition was rumored to be around $600 million, with earn-outs involved.

It shows how AI could be a potential beneficiary for Netflix if it helps lower production costs.

If they're continuing to spend around $20bn in content, it's just going to go farther, as money can go to actually paying actors to film things rather than on the back end of making everything look better.

Netflix has also been really good historically about being flexible when their model was wrong.

The best example was the introduction of ads.

For decades they said, "We'll never do ads, it's going to be just subscription pricing."

And then they realized that was wrong, and if they wanted to expand the service to more people and make it more affordable, they needed to get into advertising.

SmartTV Secular Tailwind.

There's only 45% penetration of smart TVs out of the 850 million households, so more TVs becoming smart TVs is a secular tailwind that's still going on, though maybe not as impactful as the past since the most valuable markets already have high smart TV penetration.

They also note they're only 5% of total TV time currently and 7% of the total TAM, which they said was $670bn on a revenue basis.

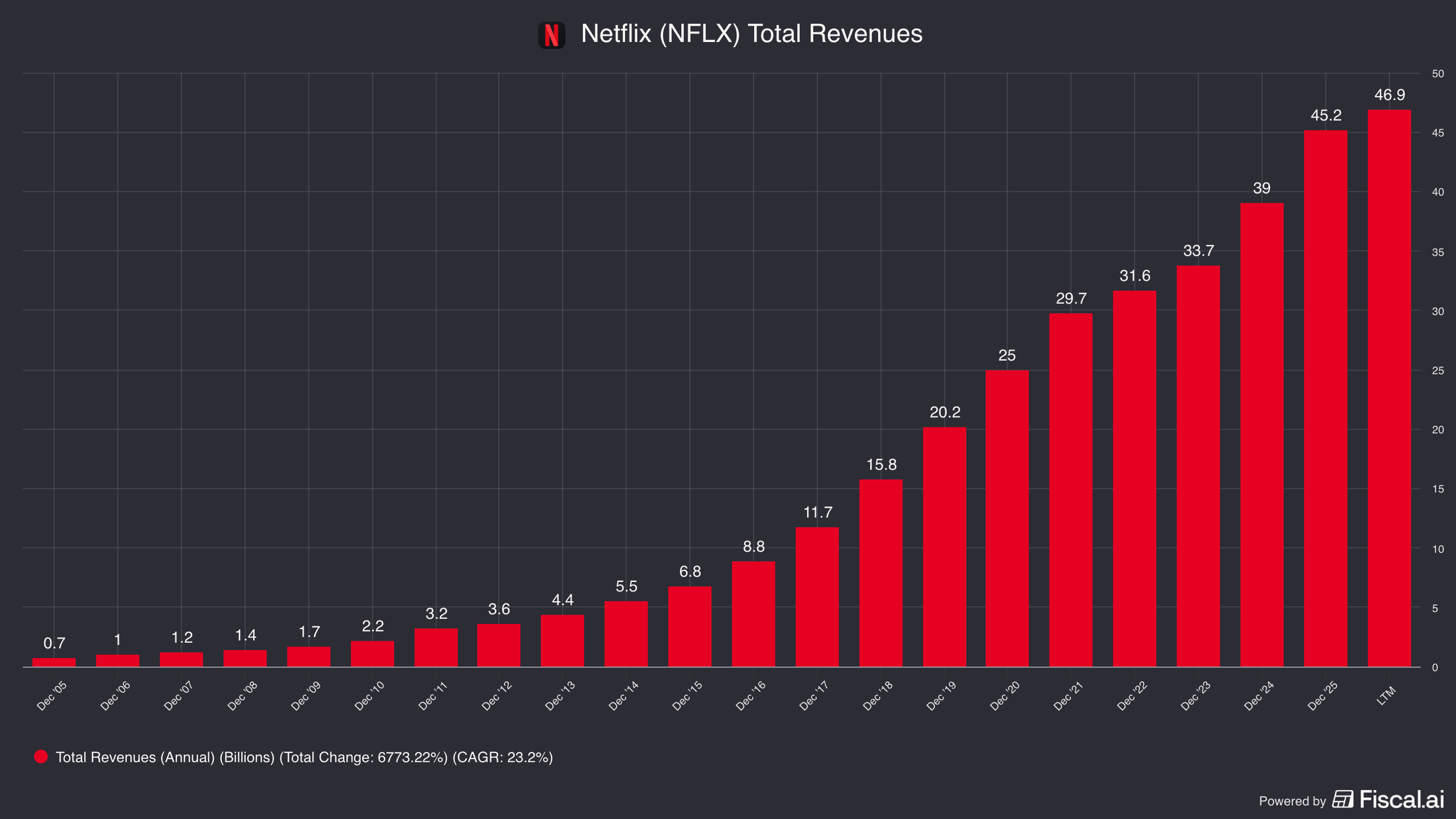

If you're looking at the last 12 months, they had about $47bn in revenue.

Three Strategic Priorities.

On the last earnings call, they put their opportunities into three focuses: 1) improving the core offering, 2) technology, and 3) improving monetization.

Improving the Core Offering.

Within improving the core offering, one of the newer initiatives is podcasts.

They have a partnership with Spotify as well.

The idea is pretty simple: this is just a new category of content that should allow them to be particularly stronger during daytime TV, which is where they've kind of sagged.

And it could improve mobile usage, because people tend to listen to podcasts very often on their phone.

This is just another reason to get a user into the Netflix app, getting them a little bit more attachment and engagement with the service.

And it's not a terribly expensive form of content.

The next thing they're working on is gaming.

What right to win does Netflix really have in gaming?

The brutal answer is none, as of right now.

They don't have a crazy amount of IP to draw someone to a video game, no great gaming hits, and they've been at this for a few years without much traction.

But the bigger thing is about engagement and churn reduction.

If you're able to get someone to play a game on Netflix, they're much less likely to cancel.

And if they create a Squid Game game, for instance, playing that makes you more likely to engage with the TV series, and the game becoming popular is another advertising event for their series.

They've rolled out a separate gaming app called Playground just for kids.

In theory, I don't see anything wrong with gaming, and their margins haven't been impacted by this effort at all.

Whether it ends up being successful remains to be seen, but people doubted they would ever be successful creating content too, and they've clearly proven otherwise.

Technology: Recommendations and Ad Tech.

The second priority is technology, which breaks into two things: 1) recommendations and 2) ad tech.

Recommendations is straightforward but extremely powerful, because a lot of times you're not sure what TV show you want to watch, and very often you'll go to one TV streamer, then the next, then the next until you find something.

By Netflix improving their algorithm, it makes it much more likely that when you hit the Netflix app, which a lot of people do tend to hit first, they'll actually be able to show you content you end up watching, which means you're a more engaged subscriber, with better pricing power and less likely to churn.

Recommendations is a lesser-mentioned thing, but it's incredibly powerful given Netflix's long tail of niche content.

Even today, they're just a lot farther ahead of all the other platforms in recommendations.

If you pull up HBO, there's really very little going on in terms of recommendations.

The second area of technology is their ad tech stack.

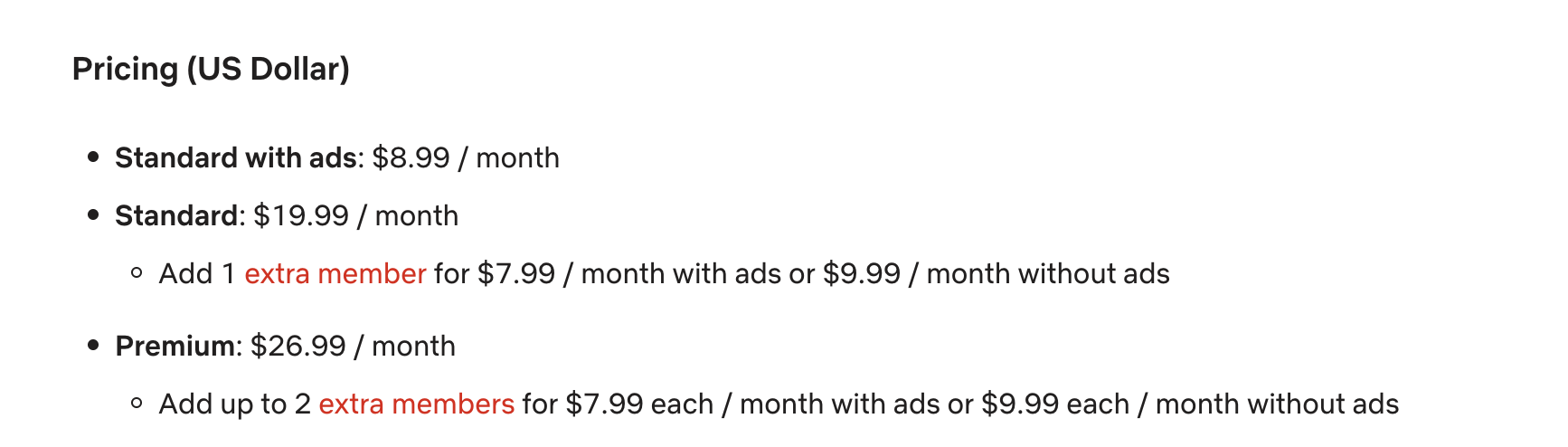

The price for their ad-plan is $8.99 compared to their standard ad-free plan of $19.99.

That's an $11 difference in pricing they need to make up in advertising revenue.

My guess is they're not there yet, but they picked that pricing differential because that's where they thought they could get to relatively quickly.

One of the problems right now is they have about 4,000 advertisers, but a lot of the ad slots have no ad inventory behind them.

No one is paying for that ad, so it's basically being under-monetized.

As fill rates go up and more advertisers come onto the platform, you'll have the opportunity to increase this differential.

As advertising gets better, they could adjust pricing from either end.

They could lower the price of the ad-plan, making up that difference through better ad monetization, which means more people can subscribe at a lower price point.

At the other end, they could raise the price of the ad-free version.

And eventually, I think they might have a totally free tier, entirely ad-supported, the same way YouTube works today.

They talked about doing like $3bn in ad revenue for this year, against $47bn in revenue, so a very small portion of their overall revenue base.

I think eventually advertising could be the majority of revenues.

YouTube does $40bn in ad revenue and maybe $20bn in subscription revenue from YouTube Premium, which shows how much bigger the advertising business can be versus subscriptions.

Netflix right now charges around $30-$40 CPM, the ad price per thousand impressions, with about 4-5 minutes of ads per hour versus around 15 minutes in traditional TV.

They sell premium, brand-safe ads, a very different model from YouTube's direct-response platform.

Netflix is the highest quality advertising venue you could really get for TV.

The last thing on advertising is AI.

Generative AI could help advertisers make more commercials and personalize them to individuals.

The problem for Netflix versus Meta is they don't have a feedback loop since no one is doing direct purchasing activity on Netflix.

But their $30 to $40 CPMs are already plenty high that they don't need to dramatically improve targeting in order to get a higher price.

Improving Monetization.

The third focus is improving monetization through advertising and subscription price increases.

They noted that their retention is up year over year, their internal metric of premium quality engagement is at an all-time high, and Netflix's cost per hour of content consumed is the cheapest among all streaming video-on-demand players.

If we provide more value than price we're taking and churn is stabilized, there's a good chance we could take more price in the future.

They did just take pricing recently, and noted they didn't notice a bunch of churn.

These are all positive signs suggesting more pricing power to come.

Netflix's Content Cost Per Subscriber Advantage.

Netflix's structural advantage versus all the other competitors comes down to a simple thing: content cost per subscriber.

Right now, Netflix with their 325 million paid subscribers comes out to spending an average of $5 in content cost per subscriber per month.

That is the lowest in the industry by far, because all of these other players are split between linear TV subscribers and streaming subscribers.

If you took Paramount's content spend and attributed it just to their video streaming subscribers, that number would be about $18.

Including Paramount plus Warner Brothers together, you're still looking at content cost per sub of around $12-13, more than twice what Netflix is.

This goes to show how much more margin Netflix has to play with versus legacy competitors who need all of the linear TV revenues to help subsidize their video streaming platform.

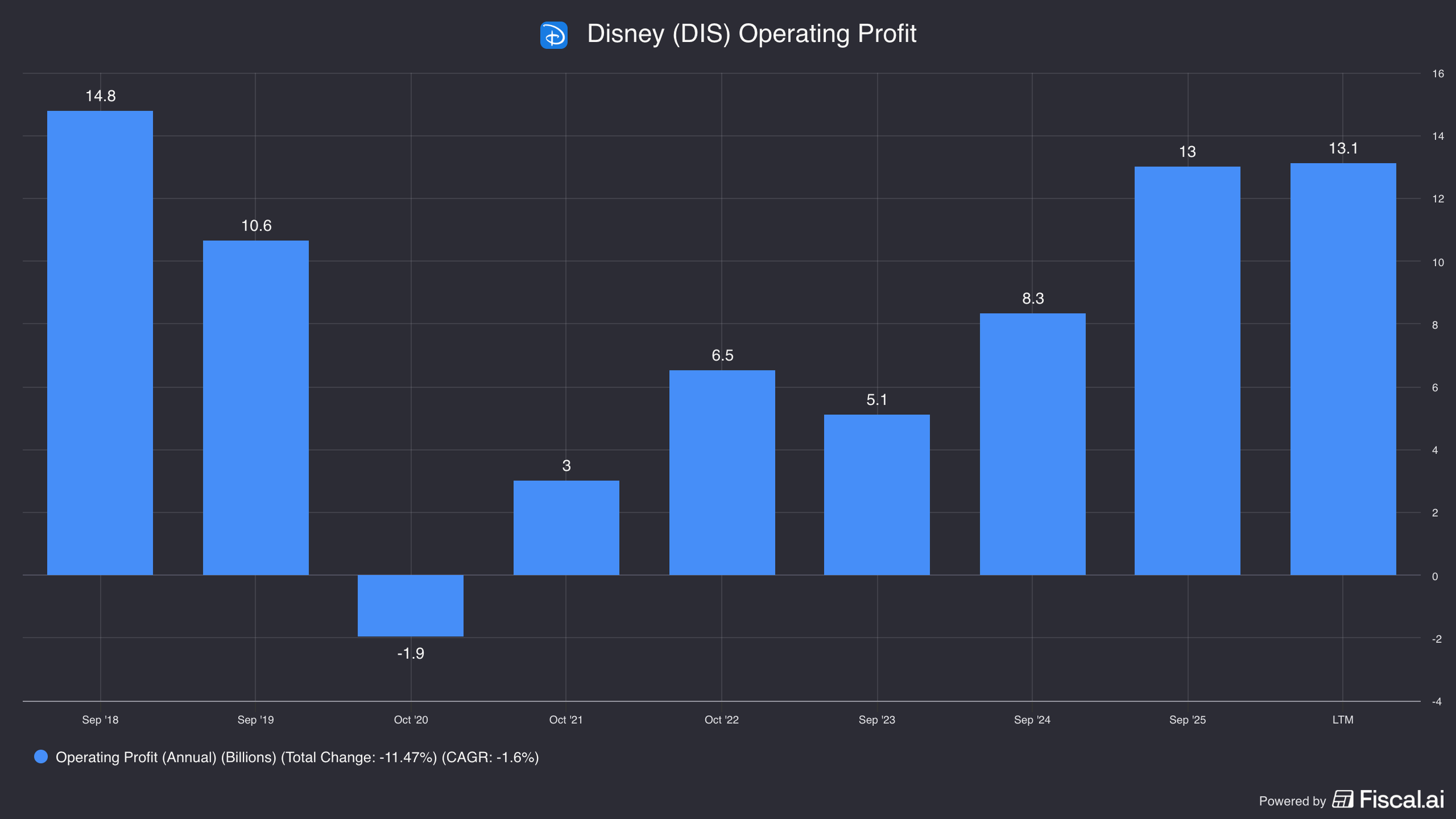

Disney, who has by far the best IP of any player, has seen flat operating income since 2018.

The reason is they keep transitioning from the legacy business into a streaming business where the economics are just worse: going from collecting maybe $13 in carriage fees for a linear TV subscriber to getting $9 on video on demand, plus higher churn and higher customer acquisition costs.

Now, this hasn't been a problem for Netflix because this is the business they grew up in.

It's the same sort of idea as Clay Christensen's innovator's dilemma, where when you're starting from the bottom with a very low-margin business, every dollar you make more in that business is better than the worst business you were in before.

Because they never had a legacy TV business to escape from, they never had to worry about overearning in a different business, which is what is really hurting these other players.

Just looking at some of the biggest players: Paramount has negative margins, Time Warner has negative margins, Disney has a low double-digit margin despite a really profitable parks business.

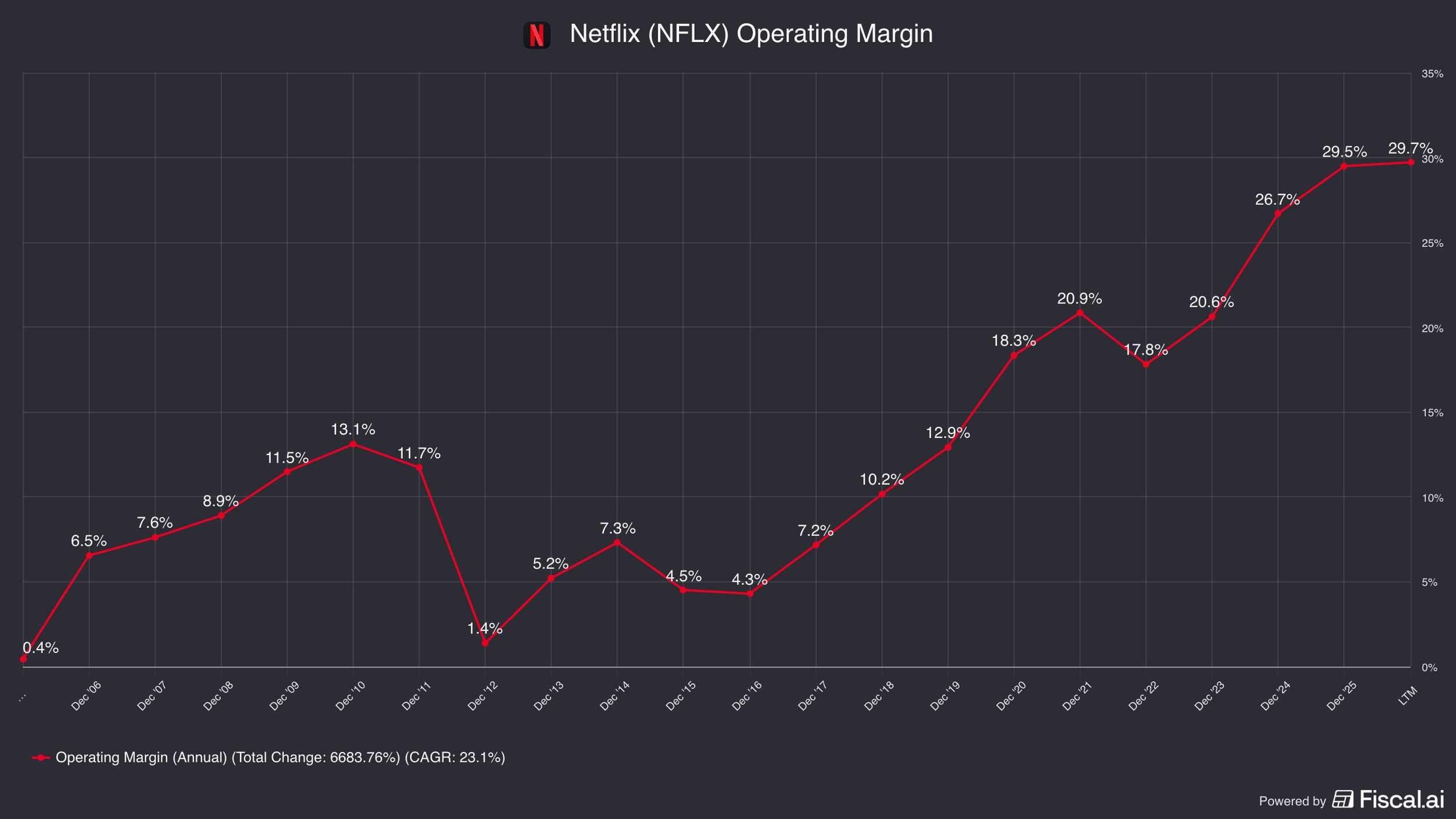

And then you have Netflix, going to do a 31.5% operating margin this year.

When you have a unified platform and a coherent strategy, the economics of the business can just look so much better than your competition.

It also goes to show how hard it is to disrupt your own business.

These legacy companies are still generating billions of dollars in cash flow and can't just not accept it today, even knowing they're over-earning in a declining business.

They still need to collect it while trying to transition to a video streaming platform.

Netflix's Weaknesses and Experiments.

Not everything is perfect at Netflix.

They certainly have a lot of trouble creating the highest end of content, the Academy Award, Oscar-winning level content.

They haven't really been able to do that, and a big part of that is because they haven't done theatrical releases.

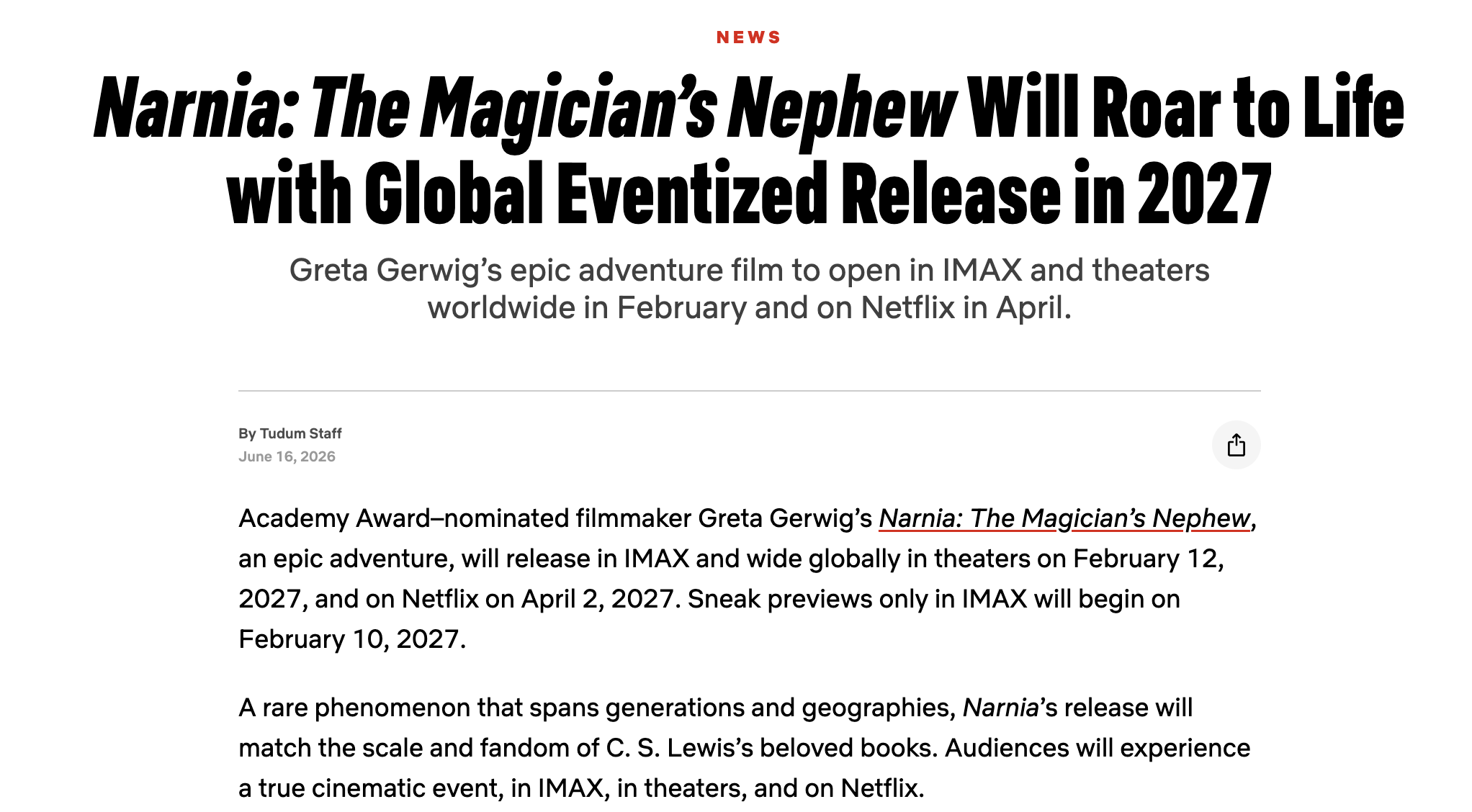

However, more recently with Narnia, they're showing willingness to experiment.

This is going to be the first movie they ever release getting a full standard theatrical release, global worldwide opening, with a 49-day lock before it can come to streaming.

They're experimenting to see if that works, and it's content they probably wouldn't have been able to get otherwise.

You could critique them and say that a lot of their content is not as high end as some of the stuff coming out on Paramount or HBO or Disney, and that's okay.

Ultimately, the goal is creating content that people enjoy watching and are willing to pay for.

They may not need the most Academy Awards in order to keep subscribers engaged.

And if you're looking at third party statistics of churn and all that, they've seemed pretty successful so far.

Valuation.

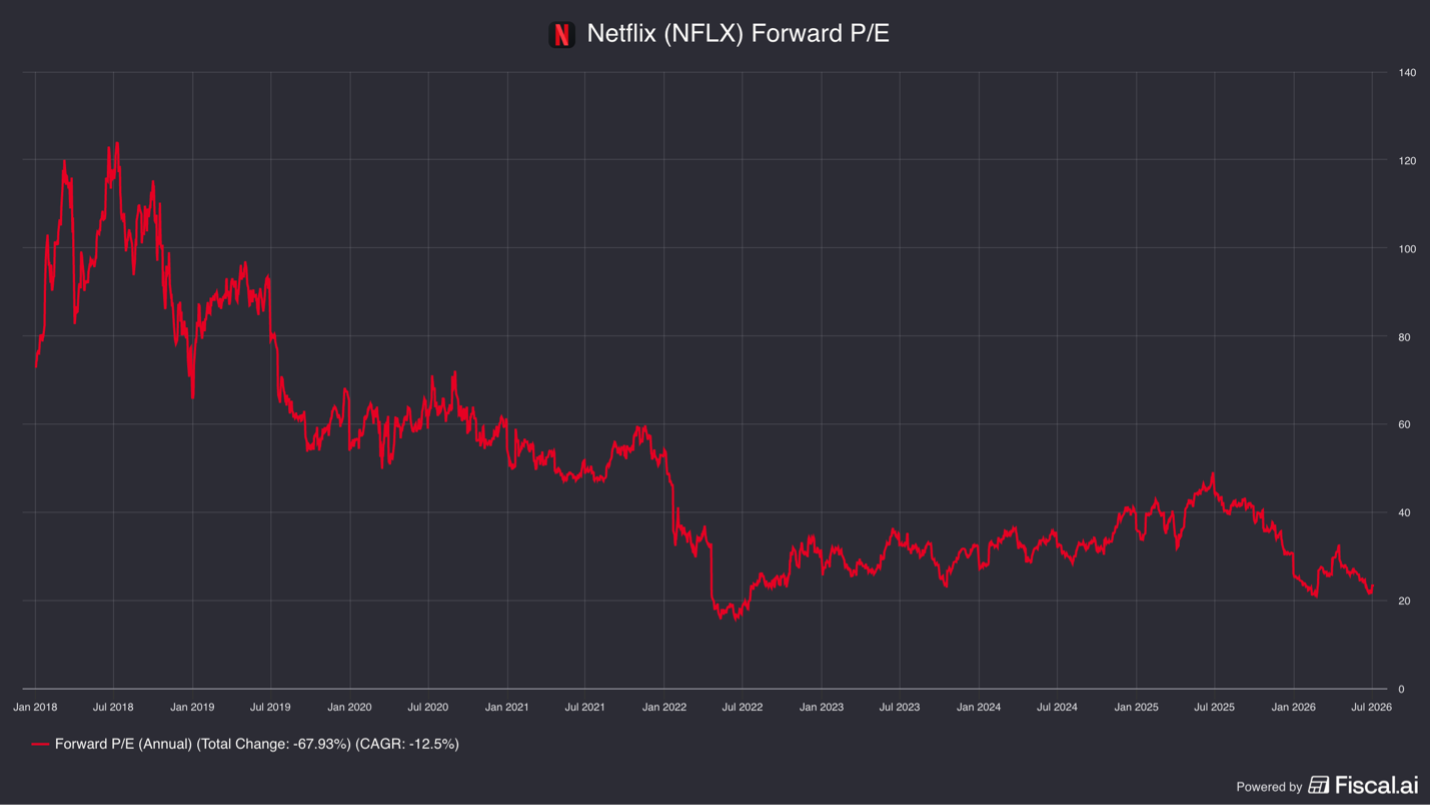

Right now, Netflix trades at a $77 stock price, putting them at 24x 2026 earnings.

This year, they're expected to grow top line 12 to 14%, but they said they're expecting growth of multiple years to be beyond that.

This is a model with incredible operating leverage.

In just the past five years, operating margins went from 18% to 31.5%.

If they can increase ARPUs by $1, operating income will increase about 20%.

If you think this model can work for a long period of time, continuing to invest in more content, providing a better experience, and then taking just a little bit of pricing and enjoying operating leverage off of that, you could see this business have 40% operating margins one day.

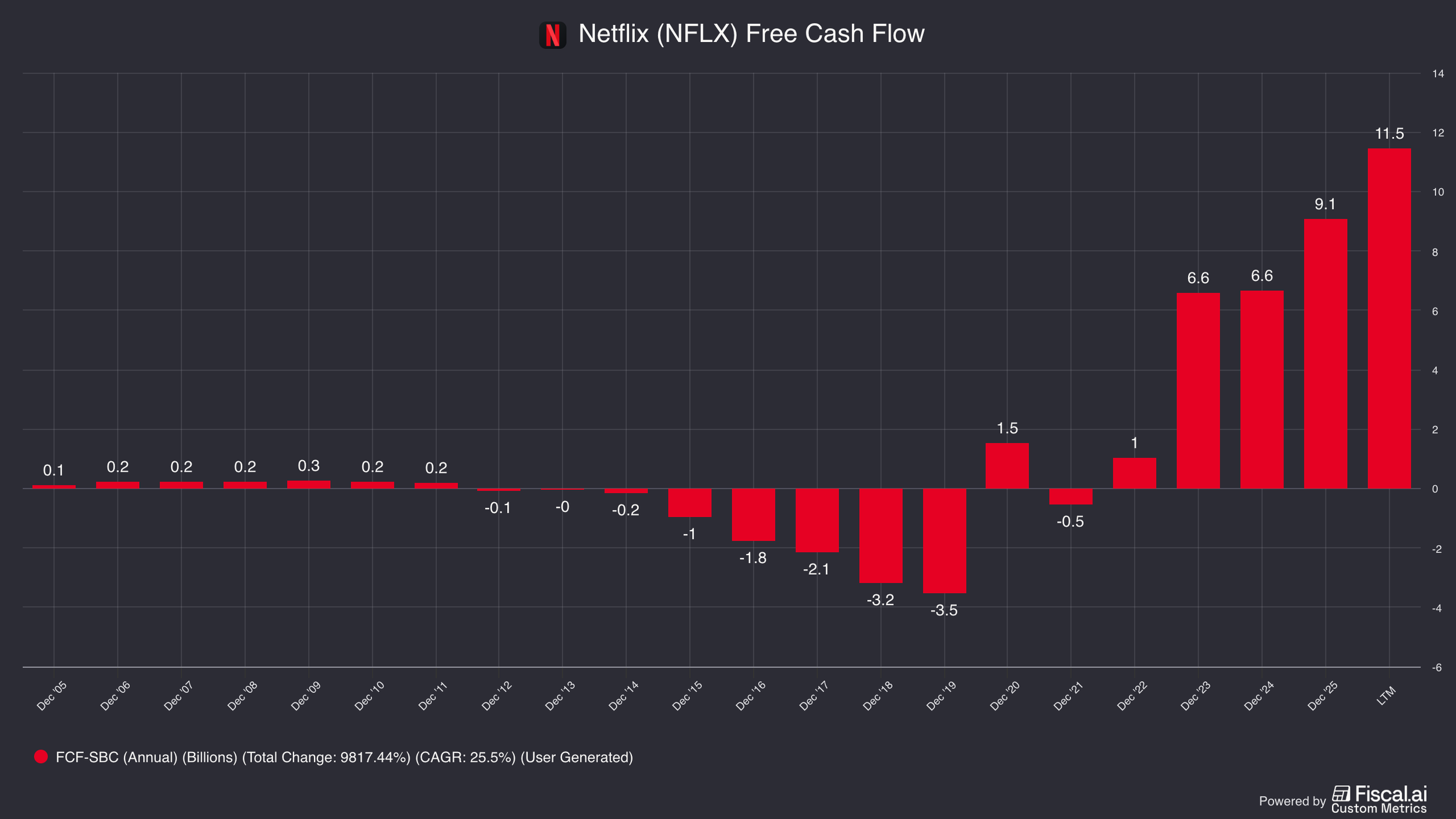

While criticized for so long for burning up so much money, right now they're generating around $12bn in cash flow.

They just did a $25bn stock buyback authorization, in addition to another $6bn left on the prior one, for $31bn in repurchase authorization in total.

At today's cash flow levels, they could take that out in just under three years.

Which is kind of the true irony here, where you have all of these other legacy media companies that had wildly cash flow positive businesses, and none of them are really that cash generative anymore.

And instead, it is Netflix, the one criticized for being reckless in their spending for so many years, that is now returning the most cash to investors.

However, you still have to decide, as an investor, if 24x forward earnings is the right multiple to pay for this business.

And that will be for you to decide.

For more on Netflix, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.