Dying Business or Easy Money? Adobe Update

Get smarter on investing, business, and personal finance in 5 minutes.

Business Update

Adobe is a very contentious business because in the minds of investors, this is either a no-brainer, a stock trading at 12x earnings, or it's a business that is dying, a sort of classic value trap.

That is why this has been such a contentious sort of battleground stock for a lot of different investors.

It also, though, is at the juncture of whether or not humans are going to be involved in creative work at all.

And so, it is a stock that really takes on almost every single facet of the AI debate.

As you may have noticed, Adobe stock has been down a lot, so in this week’s Five Minute Money, I wanted to revisit Adobe and provide a little bit of an update to see if the Adobe thesis has changed over the past couple of quarters to support an investor’s confidence in an investment in Adobe, or whether or not it suggests things are not going as planned.

ARR Slowdown.

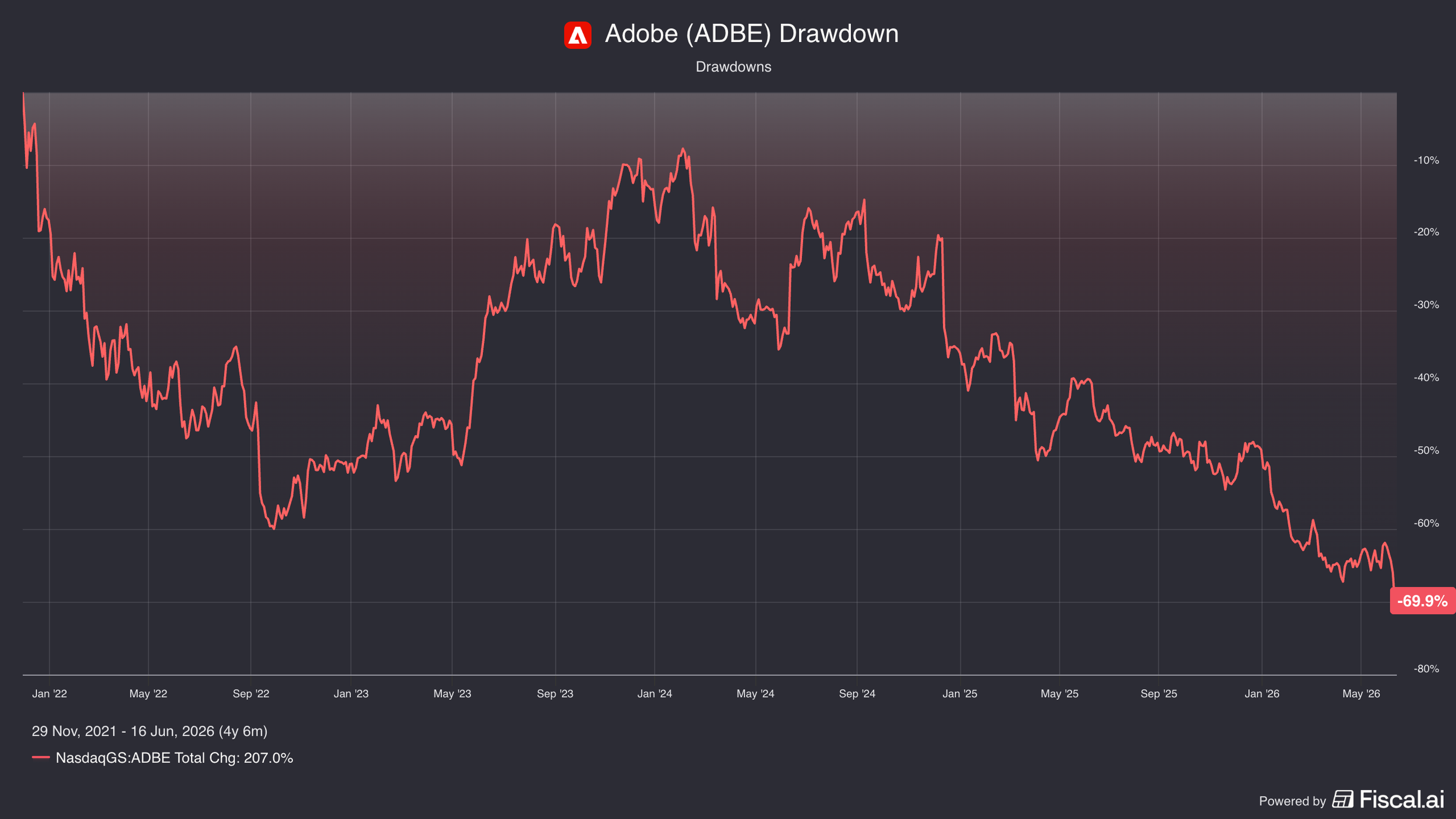

From its all-time high in 2021, the stock is down -70%.

Year to date, it's down about -40%, and just in the past month, since the beginning of June, it's down about -24%, and it sold off even more in after-hours, after earnings.

There are a lot of investors who are just looking at the P&L of Adobe, the fundamentals, and saying, "Well, they're still growing revenues double digits, still have a very strong operating margin, still very cash generative, and they're putting all this money into buybacks. If AI was going to disrupt them, it doesn't seem like there's any sort of evidence of that in the fundamentals, right?"

And that is not entirely correct.

The way I would phrase this, being precise, is the same way a scientist would phrase a hypothesis for an experiment, which is that, so far, there is no evidence to support the hypothesis that Adobe is not being disrupted by AI.

In layman English, what that means is that if you own Adobe and your thesis is that they're not getting disrupted by AI, you don't have great evidence for that yet.

What that means, though, is not that you're wrong, it's just you don't know whether or not you're right yet.

The past couple quarters of performance for Adobe has not given you any sort of confidence that Adobe is not disrupting them, or that there's not some disruption in the business.

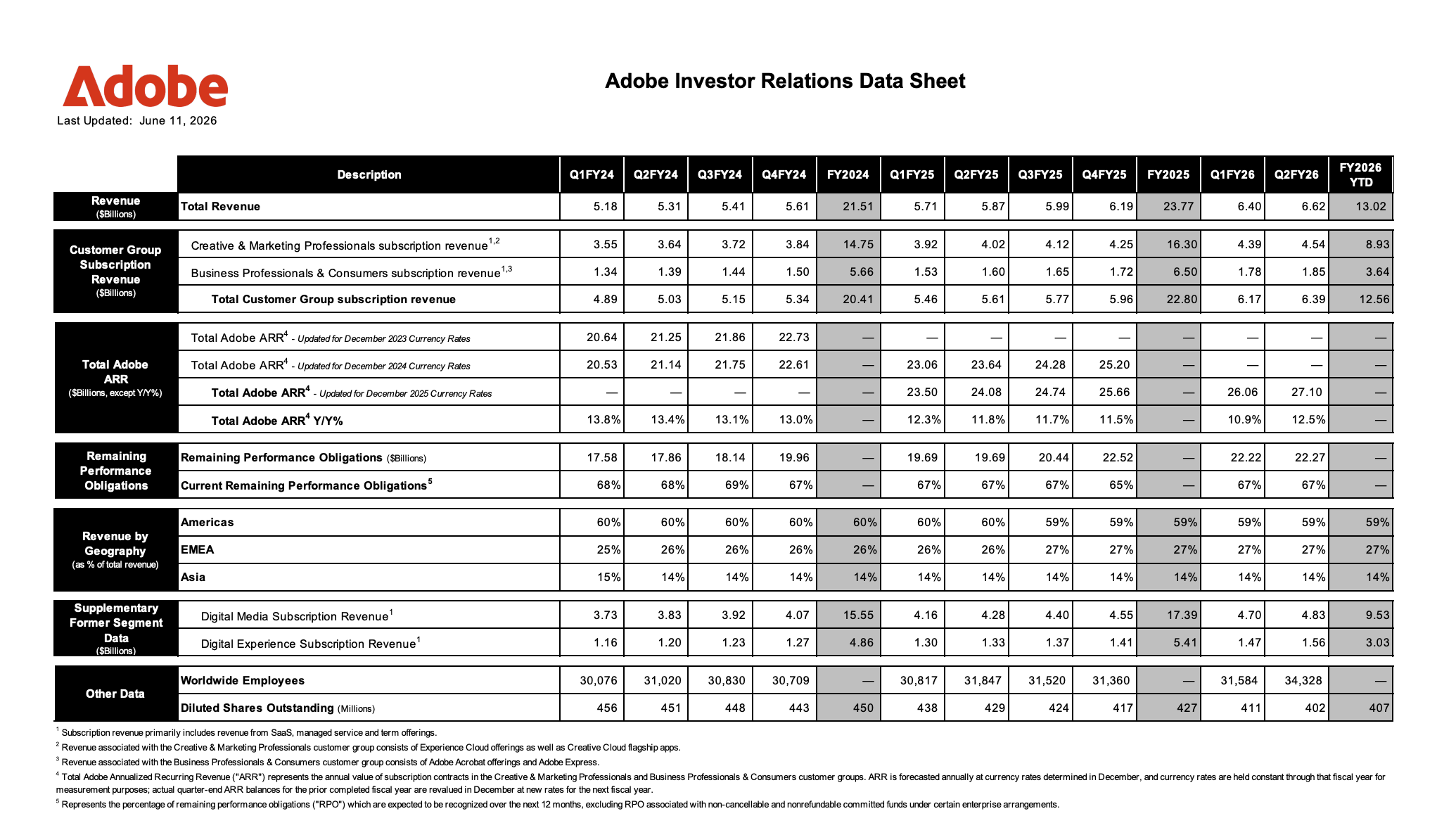

If you look at their ARR, which is their annualized recurring revenues, that has fallen every quarter for the past ten quarters.

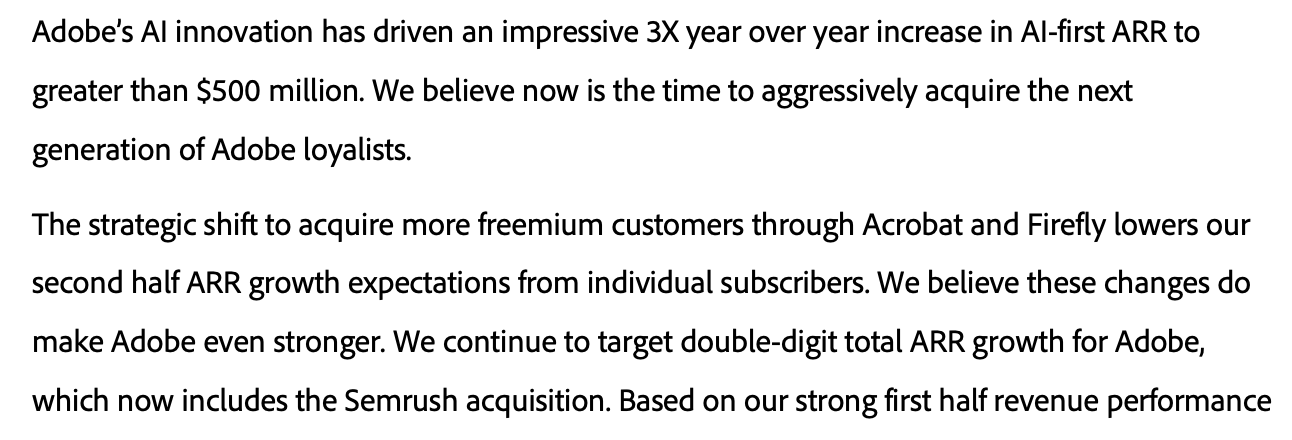

This last quarter, ARR growth was 12.5%, which may look like an inflection, but that's not true because it includes $480mn of ARR from the Semrush acquisition.

Backing that out, the ARR number is really 10.5%.

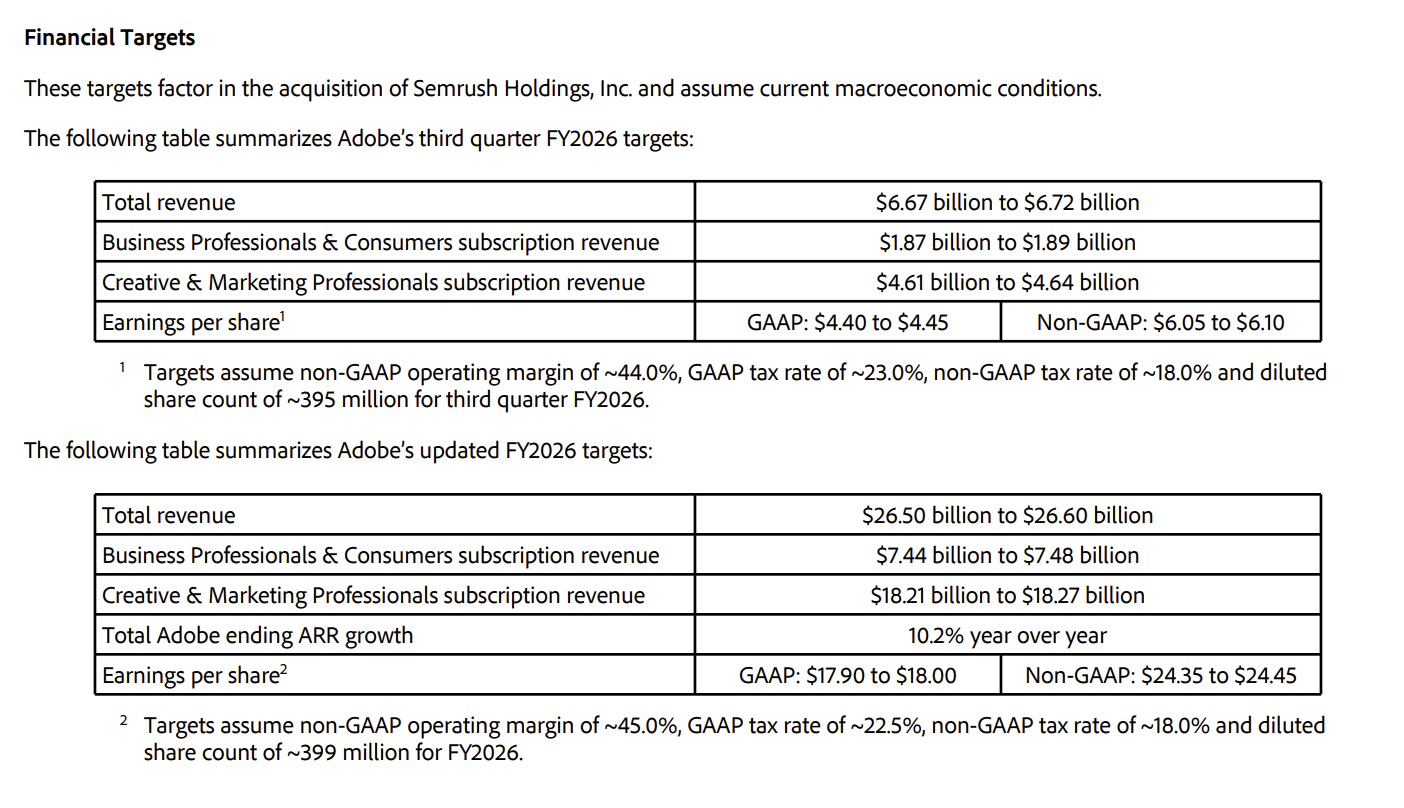

They put out full year 2026 of about 10.2% in ARR, before the Semrush acquisition, and even after it closed, they did not update that guidance.

You could take that as a suggestion they've basically downgraded guidance, since they added $480mn of ARR and didn't change their guide.

So the bearish point here is that revenues are growing at a slower rate, which could suggest impact from AI or from other things going on, like freemium competition from Canva.

There are two explanations as for why ARR has slowed down.

2 Reasons Why ARR Slowed.

We have ARR falling every quarter for the past ten quarters.

We know that's true, that's a fact.

What we don't know exactly is what to attribute that to.

We have management's explanation, and then we also have investors' fears, which is that maybe what management is explaining is part of it, but not all of it, and maybe they don't themselves fully know everything that is happening.

Whenever you're running a business, just because you are the person running it doesn't make you all of a sudden omnipresent, that you know every single reason why a consumer picked your product or didn't.

You certainly hope a management team has a better tap on that than you do, but it happens all the time that what's really happening in a business is not quite what management thinks, and management has their own prerogatives and biases that can blind them to certain realities.

Especially if your job depends on certain things being successful.

I'm not trying to suggest any sort of malfeasance here.

This is just what happens when you run a business and see certain negative things happening: you have certain hypotheses as to what could actually be causing that downturn, but you don't know for sure.

If you take what the Adobe CEO has said, they've said basically this ARR deceleration is the result of two things.

Reason One: The Shift to a Freemium Model.

One, it's the focus on the freemium model: getting a lot of users to just use their products for free.

Business Professional & Consumer traffic into all their products is up 35% y/y, and they now have 90mn creative freemium users across Adobe Express, Photoshop, and Lightroom.

That's the new strategy they're stepping into, and when you step into a freemium strategy, you're delaying the time it takes to monetize it.

Someone could push back and say that's suggesting it's a little bit of a worse business if you have to give more stuff away for free than you did in the past, when they would just automatically come to you and pay.

On the other end, you could say that the freemium model opens up the market to people that would have never been Adobe customers.

They test out the product, see it's a lot easier to use, and decide to pay for some more premium features or AI tokens.

If their claim is that the longer they do this strategy, the better they get at monetizing these users, I think that actually makes sense, and you could see this becomes a boost to revenue growth over time.

The problem is now this market, with Canva in particular, has a freemium player offering all of these things for free.

If you get too aggressive on paywalling features, there's another competitor happy to take those users.

Once you get stuck on a service, though, it tends to be pretty sticky, especially for just a few dollars.

Management did a similar thing with Acrobat, the free PDF reader, eventually converting people to paid.

The key takeaway is that they're making the claim this is self-inflicted: they could have increased revenue growth by being more aggressive with paywall monetization, but decided not to.

A framework here is that businesses create value on one end and extract a portion on the other, needing a good balance, since extracting too much makes customers pissed off.

You could also say maybe management doesn't feel confident yet in more aggressively monetizing this offering, which I don't necessarily believe, to be honest.

Reason Two: Delayed Price Increases.

The second reason management gave as to why ARR is going to slow in the back half is that they are delaying or deferring the release of several Creative Cloud product optimizations, which is kind of coded language for saying they're going to take up pricing.

One of the analysts asked the question more directly on the last earnings call, and they basically are delaying price increases.

With the SaaS model, you're already getting features automatically, it's not like rolling out a couple new features is going to give them a huge bump in subscribers.

So it's really the price increases that's the main thing they're deferring.

That also suggests a little cautiousness with their position in wanting to charge more right now.

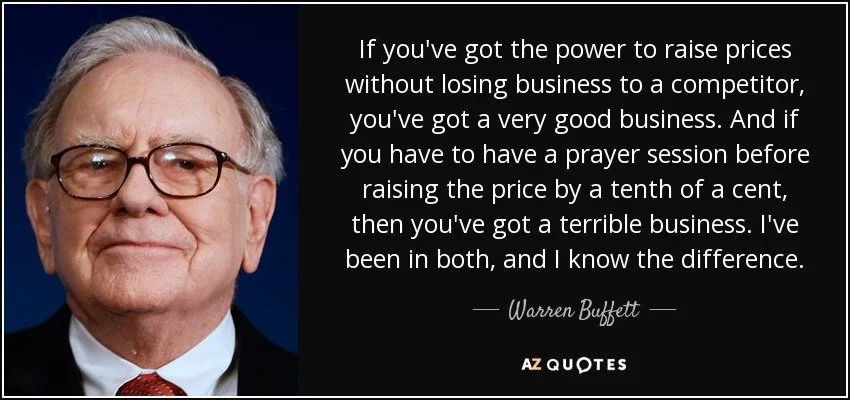

If a company felt really confident in their products and competitive position, they would not delay raising pricing.

Warren Buffett has a quote that if management is holding a prayer session right before raising pricing, that's not a business you want to own.

I'm not saying that's the case with Adobe, but these are now open questions: why is management deferring increasing pricing?

Are they seeing something in the market that worries them?

They have more competition now than in the past.

If you believe management, you might believe it's in their power to transfer these freemium users to monetized users, and when they do that more aggressively, you'll see ARR increase.

Then you may believe they were just deferring it and shouldn't read into a bigger conspiracy theory about the competitive environment.

So that maybe what you believe, and you also believe the overall Adobe franchise isn't really threatened, and AI is not the real threat here, it's just getting these more prosaic business mix and strategy moves correct.

AI Risks.

On the other side, you could have investors that are worried that creative work is actually going elsewhere, and that is the real reason why ARR is slowing down.

There still is some erosion in the actual business from all of these different AI generative products.

You can't maybe see it that obviously yet, but there's just a little bit of signs weighing on revenues, and it could get worse in the future.

Two of the biggest AI risks that I came up that are most pertinent here are below.

Risk One: AI-Native Asset Generation.

The first is that AI generative capabilities are good enough that you don't actually need any sort of changes to the creative asset.

It doesn't seem like AI's going to get there anytime soon, and even if it does, humans want to make very minute adjustments to the actual picture, and you can't do that in a chatbot, so you're going to need a set of tools.

For enterprises, which is where most of their revenue is, they're going to still need very precise tools, stuff that could do shade lighting, all sorts of very complex things.

Adobe still is number one in a lot of those respects, so that risk is, to me, a little less formidable.

Risk Two: Changing Customer Journeys.

The more formidable risk is that customers' journeys change.

Let's say before you were an e-commerce company with a product catalog of 100 different products you're selling on Amazon, and you used to hire a photographer.

The photographer would take photos, put them into Photoshop, make them look pretty, and then you'd put them online.

Now, you can snap a crappy photo with your iPhone and feed it into Amazon, and Amazon themselves has their own AI to make it a product listing ad, without the need of any photographer using Photoshop.

Another example could be Wix: instead of hiring someone to create a logo, you could just use Wix's AI generative features directly.

If you're a realtor who used to hire a photographer and put furniture in showroom listings, now you snap a photo of the empty room and AI fills it with furniture.

A lot of this is probably targeted more towards the lower end of the consumer market, but Adobe has never disclosed what their enterprise revenue mix is.

I’ve estimated that number to be somewhere between $3-7bn of revenue is this consumer revenue, on a business doing $27bn in ARR.

So it could be a pretty material amount of business that is this lower-end consumer business more at threat of being displaced.

If you are bearish on the stock, what you would suggest is that the ARR slowdown is actually the result of some of these end markets eroding, as people who used to go to photographers no longer feel a need to own Photoshop.

Asset Modification, Not Asset Creation.

It's very important to remember Adobe is not in the business of asset creation, they are in the business of asset modification, and so long as there is a need to modify an asset, they will have a business.

At the high end, that's still really important.

If you're doing high-end photography for a big brand campaign, you're going to want the best tools available, and in a lot of respects that's still going to be Photoshop and Lightroom.

It's thought that the majority of Adobe's revenues are still enterprise.

But there is this open question: if that was the case, how come they would never disclose this revenue number?

There's a very formidable bear case that a lot of revenue is at this low-end consumer segment, which is the most susceptible to AI, to customer journeys changing, and to competition from players like Canva.

If that wasn't a really big part of revenues, how come they would never disclose it?

I think what they are not saying has created more questions with investors than what they are telling them.

Leadership Turnover.

The stepping down of CEO Shantanu Narayen is a great example of this.

If they were so confident in their AI strategy, why was the CEO made to step down?

It really does leave an open question, one of the biggest ones in my mind.

If everything is so strong on their AI strategy and they're so confident they're going to reinvigorate growth with their freemium strategy, why was the CEO made to step down?

Now, it is true that whenever a stock goes down a lot for some period of time, you get investor pressure to do something different.

But that on its own is also not that positive of a signal, and it doesn't seem like he's stepping down for another opportunity, willingly to retire, or for medical reasons.

So the whole thing seems like the board felt like they needed a new leader to do something differently than what they were currently doing, which is kind of a mixed message.

Are they really strong on their AI strategy, or do they need to change it?

And, unfortunately, the CFO also stepped down in the past couple days.

As a result, the stock went down even more.

This one I don't find quite as concerning because he left to go to Marvell, a pretty hot semiconductor company right now, so it seems like a better career move for him.

But the CEO stepping down, and they still have not named a successor, it's been over half a year, and they don't expect to announce one until 2027.

Also kind of interesting that they decided to take potential price hikes off the table for the rest of the year.

Maybe it's because they want to make that a decision the next CEO gets to make, or maybe because he doesn't want potential backlash before he leaves.

Valuation.

But growth is still pretty strong.

They're still generating low double-digit revenue growth, even with the ARR guide of 10%, which if you back out the Semrush acquisition falls to maybe 8%, still pretty good if they could sustain it.

10x free cash flow, mid to high single digit revenue growth, that could still be a recipe for a good return for investors over the long run.

You don't have to do a crazy reverse DCF to know that's going to get you an above double digit return.

The real concern is just the rate of growth and how much it's been falling.

Ultimately, whether or not you are interested in Adobe relies on whether you think they could stabilize this business, if it's true the deceleration is really self-inflicted from the freemium strategy and delaying releases.

Or perhaps you believe that even if revenues continue to decelerate, they're not going to go into negative growth, and you only need a little bit of positive growth to get a good above double digit return.

Someone who's bearish would suggest this revenue is going to continue to decelerate, they have not stabilized it yet, and you don't have any evidence so far that it's going to be stemmed.

You have a good explanation from management why it could turn around, but no figures that support that yet.

The Value Trap Question.

The idea behind some stocks being value traps is that they look optically cheap, like let's say Adobe at 10x free cash flow, but ultimately the discount that looks like it exists today never closes to the actual intrinsic value the way an investor wants it to.

Usually what you hope happens is that the price increases to the intrinsic value of the business, or even better, the intrinsic value continues to increase as the price increases too.

The concern with a value trap is that the business actually continues to deteriorate over time, and that is how the price meets the intrinsic value, because the intrinsic value continues to shrink.

Now, I'm not telling you that's what's happening here with Adobe.

I will say that despite hundreds of hours of researching Adobe and looking at all of these AI risks, none of them were a kill shot, but a lot of them I could see weighing on the business just a little bit, which could give investors a lot of doubt about the future.

On the other end, I also know what the math shows, and you don't have to do a fancy reverse DCF to show a pretty strong return, which is exactly why this stock is so polarizing.

As an investor, you're going to have to make your own decision, or make a decision to not make a decision.

You don't need to hit every ball that is thrown to you.

It is perfectly acceptable if you feel some of them are outside of your safe zone and you don't have high confidence in them.

For more on Adobe, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.