Wealth Builder or Destroyer? Company Stock Explained

Get smarter on investing, business, and personal finance in 5 minutes.

This newsletter is adapted from a recent video Drew Cohen did on Employer Stock

Should you invest in the stock of the company you work at?

This could potentially be a life-changing decision.

However, the average person is not that well equipped to answer this question.

Getting this right could mean tens of millions of dollars, as participants in Apple or Nvidia's ESPP found out.

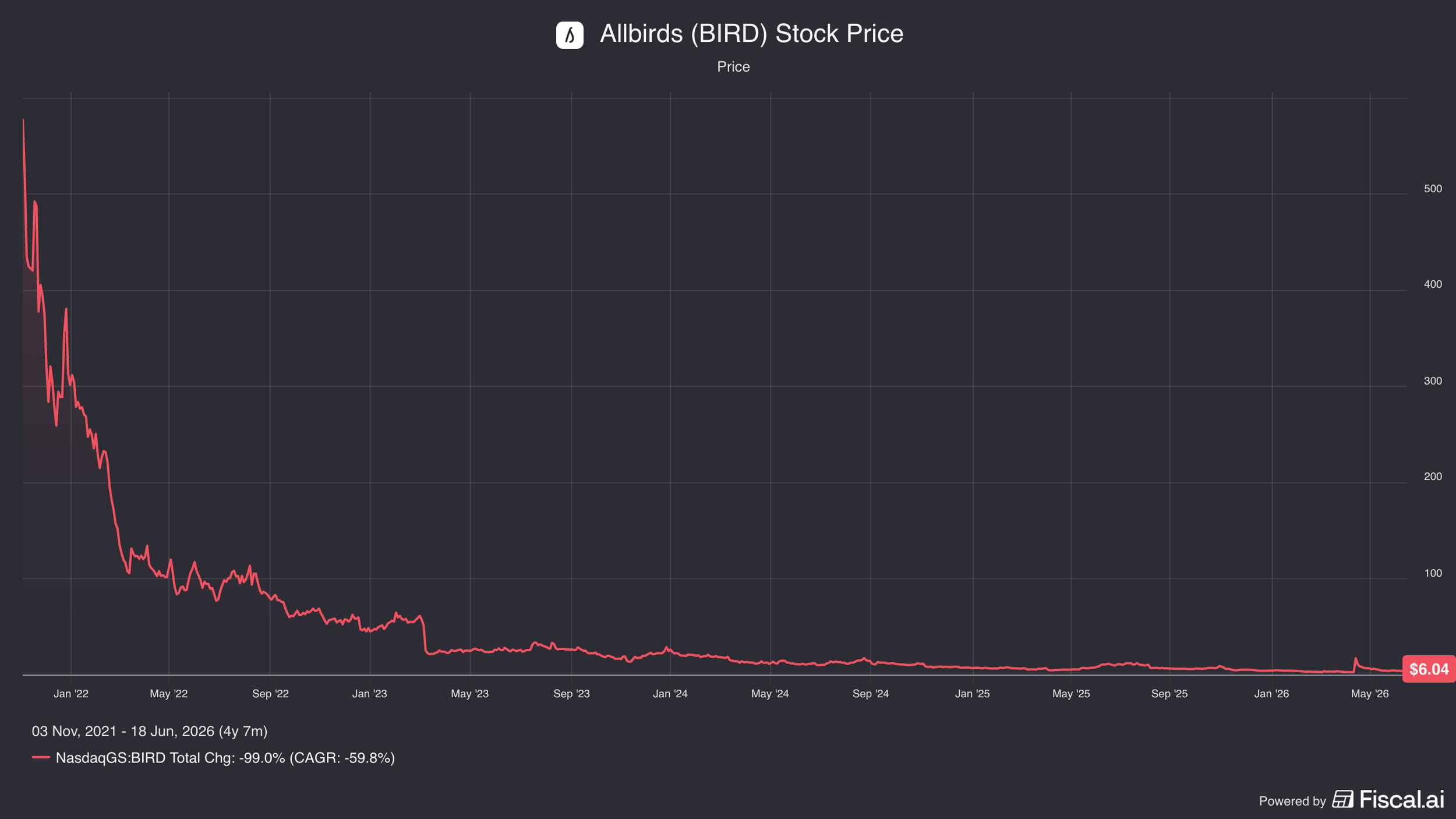

On the other hand, it could also mean total decimation of your investment, as unfortunately employees in Lucid, Bumble, and Allbirds had to endure.

In this week’s Five Minute Money, we will cover all things employer stock, whether you are at a pre-IPO startup or a public company, and provide you 5 rules to keep in mind before you do anything.

The Default Bias Behind Equity Decisions.

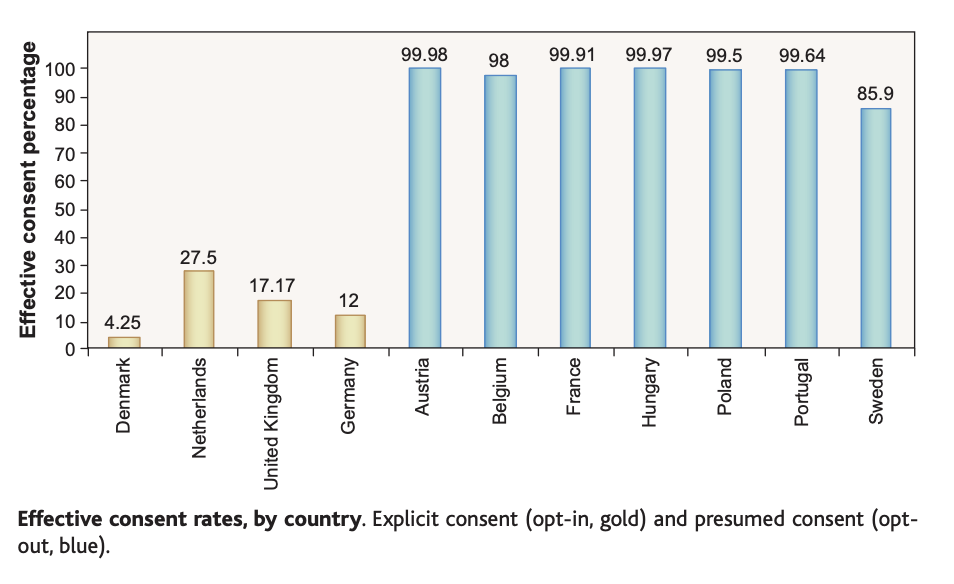

In a 2003 study called "Do Defaults Save Lives", they looked at organ donor enrollment rates across different countries in Europe: Sweden had an extremely high enrollment rate, well over 90%, while Denmark and the Netherlands had rates much lower, between 5% to 20%.

The answer has to do with defaults.

A form might say, "Check this box to become an organ donor," versus, "Check this box to not become an organ donor," and just by switching that verbiage, you can see how it leads to a very different outcome in behavior.

This is because when faced with a complex and hard decision, it is very common to just opt for the default.

If you are given RSUs or PSUs or options, very often it's going to feel like the default thing to do is to simply keep these things, when you should be treating that decision the same as if someone handed you cash and you went out and bought the stock.

If you weren't willing to take that cash and go buy stock in that business, but you were willing to keep the RSUs, you have just fallen prey to a psychological bias, because these two decisions should not be different.

Be aware of this default mentality: if you're given RSUs, you're much more likely to keep them, and if you're given cash, you're much less likely to want to go out and buy stock.

Risks That Apply to Every Employee.

Now, the decision of whether or not you should keep stock, I want to split it up between whether the company is going to be a pre-IPO company or a public company.

But a couple things generally apply to both situations.

You Become Your Own Investment Analyst.

The first thing that applies to both is that when buying or keeping stock, you essentially are becoming your own investment analyst, doing something no different than going out into the public markets and picking a single stock.

If you work at the business, you might have better information, a better sense of customer reception, whether you believe in the product.

But you may not have a great sense of valuation or whether this is a financially viable product, because if it's a private company the numbers and insights you can get are limited, and if public, you're stuck doing the same analysis as every other equity analyst.

It's a weird position, where you have to become your own investment analyst, a decision you can't outsource the way you could outsource financial advice to an advisor or obviate the decision entirely by just buying an ETF or mutual fund.

This decision is something you really cannot offload.

Concentration, Career, and Healthcare Risk.

What applies whether pre-IPO or public is that you already have your income coming from this company, an added layer of concentration risk: your salary plus a chunk of your savings tied to the same business.

If the business does poorly, you also could get fired or not progress in your career, the second risk: career risk.

When you go to a company, its success has ramifications for your future: a growing company means a better chance of promotions and raises, and a better opportunity if you ever leave.

A struggling company makes that harder, even if someone will still hire you.

Picking an example, you're a Google engineer in 2003, while a friend went to Yahoo, an even more widely known company at the time.

You'd have thought the Yahoo engineer would have better exit opportunities, but that wasn't the case, if you were there 5-8 years, you had better options as a Google engineer.

So the company you're at can influence your opportunities thereafter, another form of concentration risk people don't think about.

And your healthcare's also tied to your employer, typically, so your income, career, and healthcare are all tied to the same company, which becomes very risky when a large portion of your savings is also put into it.

Pre-IPO Companies and Startup Equity.

A lot of times when people join a startup, it's because they want access to equity with very large upside.

It's acceptable, because you're going to keep those RSUs and a disproportionate amount of your wealth will be tied up in one company, on top of betting your time and career on it, if you really believe in the company.

It's very hard to make a blanket statement on what to look for there, since it's basically everything we do in these business deep dives.

When you're deciding to work at a startup, you're also deciding, because of all that equity comp, do I want a lot of my net worth tied up here?

That decision to go to a startup is also an investment in that startup itself.

You have to have a lot of confidence in it, and it's hard because most people don't fully know everything going on within the startup.

The financials aren't made public, and you don't really know if the valuation makes sense.

You have to be okay with that level of uncertainty.

Covering Your Tax Obligation.

Now, the thing I will insist is that when you get RSUs, you absolutely should sell enough to cover the taxes.

Restricted stock units are taxed as ordinary income, and they'll withhold usually 22% percent at the federal level, not enough to fully cover what you'll owe.

You should be aware that if the stock price falls from the date you're awarded RSUs, it doesn't matter for the tax liability, you still owe the same amount as if the shares were at the grant price.

That is one thing you really should not take a risk with.

Often, if it's a private business, they'll help with secondary sales or let you adjust your withholding, since they're aware of this issue.

Saliency Bias and the Startup Lottery.

Now, the thing I want to emphasize here is that there's something called saliency bias: when something works very well for someone, we get more news stories and exposure to that, so we overweigh the likelihood of these things happening.

A lot of people, when going to a startup, are thinking of the successes of people who went to Facebook early on, Google early on, more recently SpaceX, getting tens of millions of dollars in stock value by the time the company IPOs, and that is not typical.

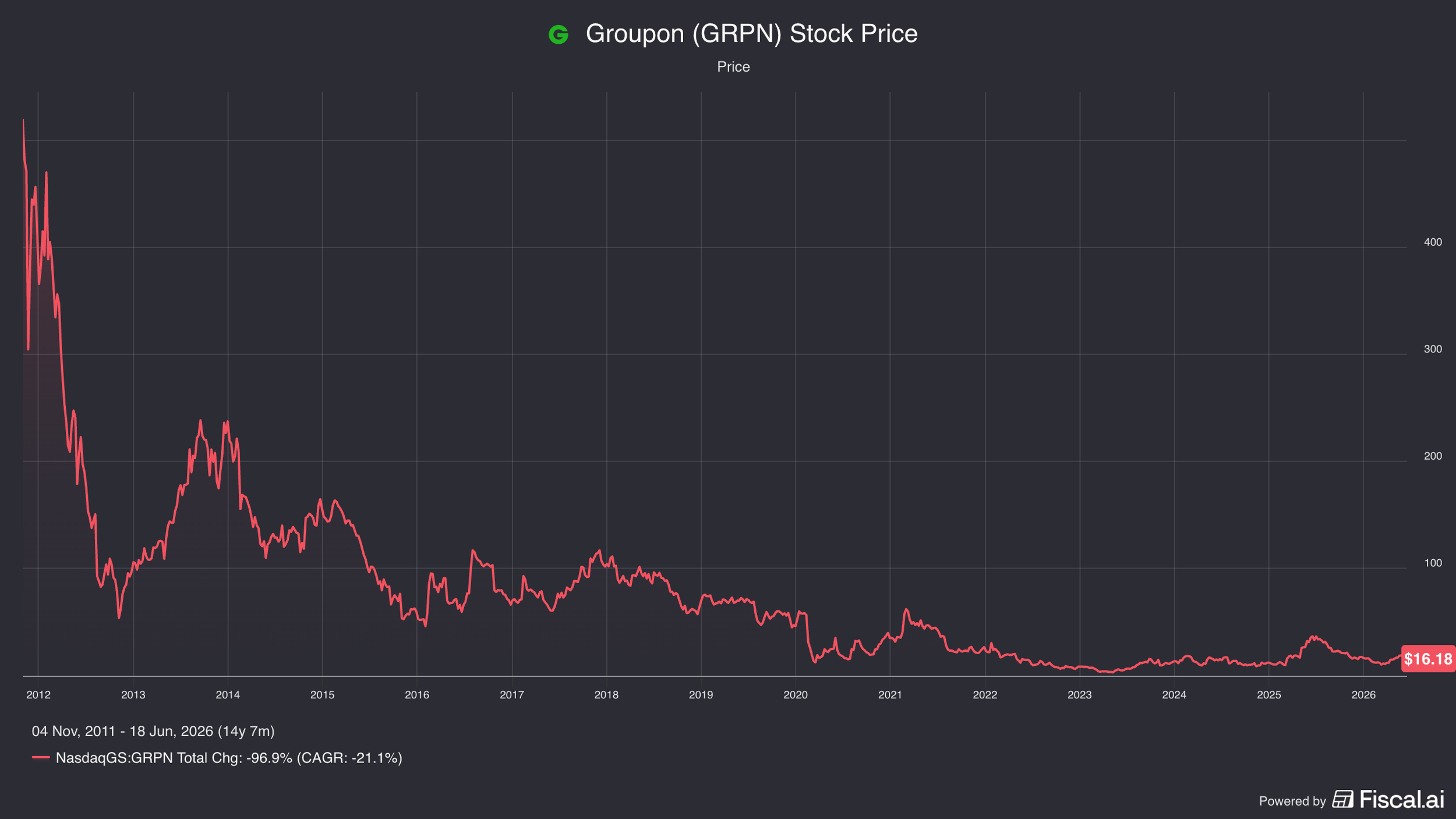

For every SpaceX and Google, there are many, many more Snapchats, Lyfts, Beyond Meats, Lucid, Rivian, Allbirds, Peloton, Blue Apron, Groupon, Affirm, businesses where employees had a disproportionate amount of their savings in stock that ultimately was worthless or down 90%.

I want you to weigh both of these possibilities before you make this decision.

Working Backwards From the Worst Case.

I think the best way to figure out how much employer stock I should own is you work backwards.

Assume instead of making $20 million, everything went wrong and your RSUs were worth 90 to 100% less.

How much does that set you back financially?

If you're younger, right out of college, this is a risk you can stomach for a few years.

If you worked a corporate job for 10 years and are going through five years of not being able to save in your late 30s, when you're supposed to be saving well, this could have a more adverse financial impact.

I'm not saying don't make that bet, just be aware it might mean retiring later.

If you're okay with that downside, do it.

A simple way to figure this out is to assume a worst case scenario and see what your financial future looks like, how many years you're willing to stay at the startup if things don't work out, and how that affects your ability to retire.

This is why I always like doing financial planning with clients, it gives a much better sense of potential outcomes.

If you get a 10X, easy, you don't have to worry about it.

If you don't, maybe you're working another several years, not the end of the world, as long as you're okay with that.

That's why financial planning is helpful.

Keeping an Emergency Fund and Avoiding Overconcentration.

Now, if you are making this big bet on a startup, make sure you still have your emergency savings fund, ideally 9 to 12 months of fixed expenses in case the startup goes under.

You want to give yourself enough time to get back on your feet, especially if you have dependents.

A conservative thing to do is to just not have a majority of your net worth tied up in this company's stock, especially if you're not that bullish on it.

Usually there's still an option to sell stock in secondary markets once vested, taking some money off the table.

If you don't believe in this company, you really shouldn't have any net worth tied up in it, and you shouldn't keep the money there just because by default they gave it to you, the same psychological bias as the organ donors.

Public Company Stock Plans and ESPPs.

On public stock, there are a few different considerations.

A lot of public companies have something called an ESPP, an employee stock purchase plan, which very commonly works where they give you a 15% discount if you own their stock, and maybe with a look-back period giving you the cheapest price the stock traded at in the past six months.

A lot of people gravitate towards this 15% discount and think that translates to a good deal, anchoring to that, another bias.

What matters most is all of the other considerations we've talked about: the risk in the stock, the moats, the returns potential, every factor from those company deep dives.

A 15% discount shouldn't sway your decision, since if you own a stock for five or ten years, 15% isn't going to make or break it.

It could push you over the edge if you're already on the fence, but that alone isn't sufficient investment merit.

Instead, do it backwards: start with, "Is this a business I want to own?"

And only as the last step ask what the valuation is and whether that 15% makes the difference.

I know the average person isn't going to do this, which is a reason you maybe shouldn't buy your employer stock if you're not willing to do that analysis, and I don't think you should have to.

Why Public Companies Have a Different Risk-Reward Profile.

The thing to keep in mind that's very different about public companies versus pre-IPO startups is that the risk-reward profile is very different.

If you get a couple hundred grand of startup stock, there's a chance it could be a 10x, a 20x, sometimes much better.

Of course, it could also go to zero, but that's how the risk-reward curve is skewed.

With a public company, the positive end tends to not have quite as much upside, generally speaking, though some companies go public earlier now, which skews that.

Once a company becomes public, you don't have these crazy asymmetric return opportunities.

If you're in a big, mature business like Procter & Gamble or Disney, I would argue most often the stock plan doesn't make the most sense.

Because when you're invested in a mature company, your upside isn't that much, but your downside is still very real.

There are still plenty of mature companies that can get cut in half, which would be disastrous for your savings.

Layer in the concentration of your earnings, healthcare, and career all in one place, and that makes it even more unattractive.

The difference versus a startup is that you have potential for a very high return to offset a lot of that risk, but that asymmetry doesn't exist when you're investing in Disney.

I don't think many people expect Disney to be a 20x from here.

In fact, if you participated in the employee stock plan, your investment would be flat to slightly down over the past decade.

It's not that there's any concern they won't be around, it's just that it doesn't make sense to blindly buy into their stock unless you did some analysis and had high confidence in the return profile being better than what the stock market has historically returned, 9-10%.

If you're not doing that, I don't advise you invest in single stocks of your employer, even with a discount, because the concentration risk can just be too much.

Generally speaking, I don't think this is the best financial decision for most people, given the concentration between your net worth and your income.

Now, there are exceptions to these ESPP plans, if it's a company with a lot of upside that you really believe in.

Apple is an example of one and Nvidia is an even bigger example, a public company for a couple decades, where employees could have slowly accumulated a lot of stock that then 20x in the past couple years.

This is certainly a very rare circumstance, but it exists.

If you were working at a business like this, you'd know it isn't a maturing business without much upside.

If you were working at Nvidia even five years ago, they were talking about huge end markets, very ambitious.

It doesn't mean you knew for a fact the stock would go up that much, but it means the decision of whether to participate probably felt more like investing in a startup than investing in Disney.

And if not, that's fine too, it's a pretty tricky thing to know when you yourself are not an investment analyst.

So conservatism makes sense here, not having a majority of your wealth in a single stock is always great advice.

But if you're very optimistic about a business, there's no reason you have to go 100% or 0%; you could gain exposure commensurate with your confidence in the business.

If it's a startup and you're younger and want to YOLO into something, go for it, knowing you have enough time to make it up if you have to.

You might have to batten down and control expenses for several years to make up for that time period.

These are not easy decisions, so if you need help, reach out to a financial advisor.

Five Rules to Remember.

Rule One: Treat It Like Cash.

If you are given an award, do not think of it any differently than if someone gave you cash and you went and bought the stock.

If with cash you would never own the stock, that should be the same case here.

You should not just keep the stock because someone gave it to you.

Treat it no differently than a cash purchase.

Rule Two: Cover Your Taxes First.

Make sure you cover your taxes first, especially with private businesses.

You're going to want to sell enough stock to cover whatever your tax obligation will be, and get ahead of that.

If you get private stock and the business goes public before you have time to sell it, and the public stock price falls a lot, you're still on the hook for the original stock price at grant date, which could really put you in a bad position.

Rule Three: Apply Normal Diversification Rules.

Concentration and diversification rules still apply.

Just because it's a private business and you have a lot of faith in something working out doesn't change the fact that you have extreme concentration in a single stock, no different than putting 90% of your money in a single stock.

That is the same sort of risk whenever you put all of your money in an individual business.

Some people are going to want to roll the dice with that one, that's fine, just be aware of it.

Rule Four: Plan for the Worst Case.

Plan for a worst-case scenario or at least be aware of what a worst-case scenario can look like.

And so, you should do that financial planning if the stock options, the RSUs, they don't pan out as expected.

Rule Five: Become Your Own Investment Analyst.

It is your responsibility to do the analysis on the business you are joining.

If it's a startup and you're going to get a lot of stock units, treat it no differently than doing investment analyst work on a public company, the same competitive factors apply: growth opportunities, valuation, everything.

You basically have to become your own investment analyst to have confidence in this decision, and it's hard because there's a lot of factors involved.

But the good news is I have a ton of newsletters on my website that'll teach you how to analyze a business and become a better investor.

For more on what to do if you have employer stock, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.