Bill Nygren Has Beaten the Market Over the Past 25 Years: Here's How He Finds and Invests in Winning Stocks

Get smarter on investing, business, and personal finance in 5 minutes.

Below are key takeaways from my recent interview with Bill Nygren of Harris Associates, where he manages the Oakmark Fund.

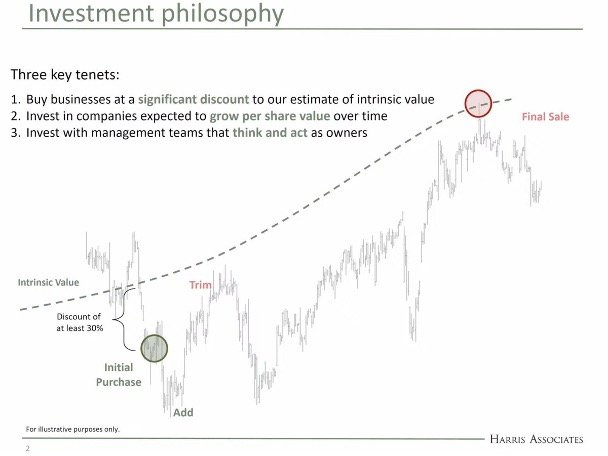

Investment Philosophy.

Nygren describes Oakmark's approach in a single line: "We bring a private equity perspective to public equity investing."

What that means in practice is looking further into the future than most public market investors, discounting that future value back to the present, and buying only when the gap between price and estimated value is wide enough to matter.

Three conditions must all be present for a stock to enter the portfolio: 1) a 40% discount to business value, 2) management aligned with shareholders, and 3) an expectation that value growth plus dividends will at least match the market.

In practical terms, Nygren is looking for businesses where a doubling over four to five years is a likely scenario, roughly a 15% annualized return against the 50% he expects from a broad market basket over that same period.

Oakmark doesn't restrict itself to the lowest-PE or lowest-price-to-book names.

Many ideas in the portfolio would never appear on a traditional value screen, because the businesses make growth investments through the income statement, expensing advertising, R&D, and customer acquisition in ways that obscure real value.

Nygren calls the adjusted lens "Oakmark accounting instead of GAAP accounting."

The Seven-Year Horizon.

The most concrete expression of that private equity perspective is the time horizon Oakmark works within.

Seven years isn't an arbitrary number.

It represents the outer edge of where Nygren believes he can forecast with meaningful conviction.

He frames the philosophical divide this way: "The biggest difference between fundamental value investors and fundamental growth investors is how far out do we say our crystal ball gets so cloudy that our projections are really not important to the value case."

Some growth managers look out 15 to 20 years and discount at a high rate.

Nygren argues that approach creates a false sense of precision.

Beyond seven years, Oakmark stops assigning a company-specific multiple and defaults to something near a market multiple.

"We've settled on seven because that's a longer time period than most other investors are looking at. And it's not so far into the future that it feels like we're doing coin flips," he explains.

He points to landline telephones and newspapers as humbling examples.

Both were once considered so stable that investors believed they could model them out 20 years.

Both were dismantled by disruption.

The seven-year constraint is, in his words, a form of margin of safety applied to the forecast itself.

Rank Ordering Over Precision.

The seven-year cutoff shapes not just how far Nygren looks, but how much confidence he places in any single number that comes out of the model.

Fair value isn't a number you can compute with precision.

Nygren believes this sincerely, and built Oakmark's entire process around the insight.

When covering hundreds of businesses with consistent assumptions, what matters most is not determining whether a stock is undervalued by 40% or 38%.

It's correctly rank ordering all of them relative to one another.

As he puts it: "Precision in the number isn't nearly as important as rank ordering. And if you've applied consistent assumptions across a group of a couple hundred businesses, you look at the names that look most attractive, whether they're undervalued by 40% or 20%, or 60% isn't nearly as important as that you've identified the ones that are most undervalued."

"Our whole process is on making sure we've rank ordered our ideas in a way that we think reflects how attractive they are," he adds.

The 40% Discount Requirement.

That emphasis on rank ordering over precision is precisely why Oakmark demands such a large gap before buying.

The 40% haircut applied to Oakmark's business value estimate is not false conservatism.

It's a deliberate buffer against the unavoidable imprecision of any forward-looking analysis.

Nygren was direct when he said, "We don't want false precision. We're trying to get into the right ballpark, and 40% is a big enough number that if we're off by a standard deviation or even a little bit more than that on our estimate, we've truncated our upside, but we haven't created downside."

He finds it almost telling when other value managers report buying a stock at $60 with a value estimate of "$75 and 12 cents."

That level of specificity implies precision the analysis cannot support.

And when the range of plausible values spans too wide, say, a stock at $60 that might be worth $70 or $150, Nygren will wait, because he wants the lower end of that range to still clear the 40% hurdle.

Be a Disciplined Seller.

Buying at a discount is only half the discipline.

Knowing when to exit is equally important, and equally difficult.

Nygren admires the Buffett model of permanent ownership but he argues a subtle momentum bias creeps in when investors decide every stock they've bought is "now anointed as a hold it forever company."

As he puts it, "When a stock exceeds the price you think it's worth, just because you owned it is not a good excuse to continue owning it."

If Oakmark's edge is identifying businesses at large discounts, the natural funding source for new purchases is the stocks that have appreciated to fair value.

Holding past that point isn't discipline, it's anchoring and that bias can be a risk.

There's also a longer-term risk embedded in the permanent-hold philosophy.

If a stock is held forever on the assumption that a company's high ROIC will persist across a generation, that is, in Nygren's words, "a little bit like betting against capitalism."

The way capitalism works, pockets of high return attract new capital, which drives returns back toward average.

Reversion to the mean may be taking longer than it used to, but abandoning the concept entirely leads to "some really crazy outcomes on how you should be investing."

Adjust Your Estimates When You Get New Information.

The discipline of selling at fair value only works, however, if fair value estimates are continuously updated.

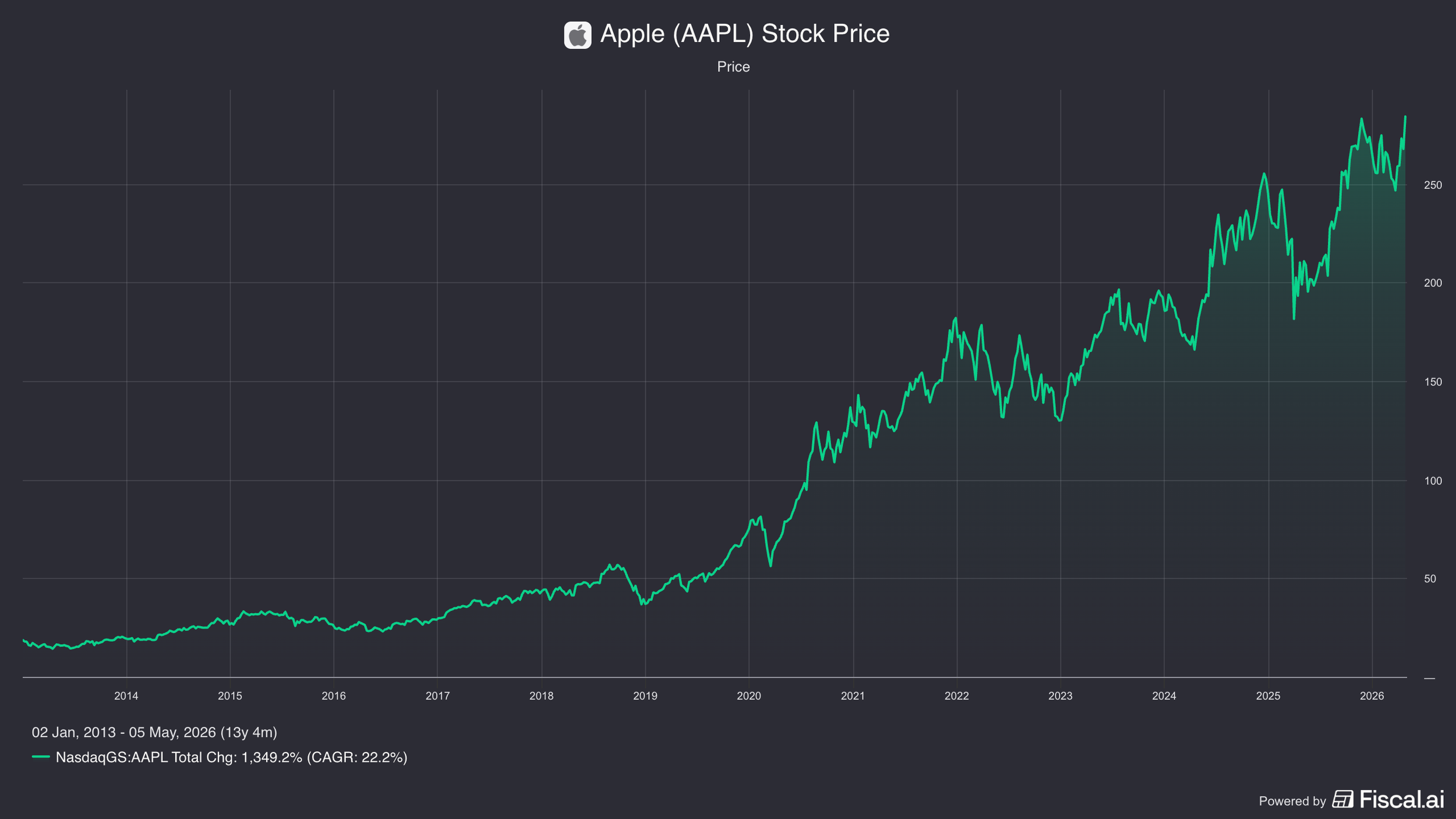

The Apple investment illustrates this principle as clearly as any example in Oakmark's history.

Nygren bought the stock at roughly 60 cents on the dollar.

The fund subsequently made approximately 20 times its money over the following decade, and at no point during that period did the stock trade above Oakmark's sell target.

The reason why was that their estimates were updated quarter after quarter as Apple's growth consistently exceeded expectations.

For most of the decade they held it, Apple was still trading below a market multiple.

"We would've sold Apple for a 50% gain and been out of the stock if we didn't adjust our numbers from what the analyst presented the first time we bought Apple," Nygren notes.

The consensus view at the time was that Apple was over-earning and due for mean reversion, the same pattern seen in countless consumer product companies.

What the market underestimated was the switching cost of leaving the Apple ecosystem, a moat that proved far more durable than the investment community expected.

Earnings Growth, Not Multiple Expansion.

Oakmark eventually sold Apple, and Nygren is comfortable with that decision.

The gains that came after were driven largely by what he is most skeptical of.

The post-sale returns came from PE expansion, going from roughly a 20-times multiple to a 30-times multiple, not from further earnings growth.

It's when PE expansion drives the returns, rather than earnings, that Oakmark starts to get uncomfortable.

The names he's held longest illustrate the preference.

Alphabet is one he cites: its stock price has largely just followed the growth of the underlying business, without meaningful multiple expansion.

That's the outcome he's looking for.

Why Banks Get Such Low Multiples.

This same focus on fundamentals over narrative is what draws Nygren toward one of the market's most mispriced and most misunderstood sectors.

Bank stocks, in his view, trade at deeply discounted multiples today for reasons that have more to do with investor psychology than business reality, and the misvaluation traces directly to lingering trauma from the 2008 financial crisis.

Before the GFC, banks were viewed as low-beta, risk-off holdings.

As Nygren notes, utility stocks used to aspire to get bank multiples.

Since 2008, that dynamic has fully inverted: banks are now treated as high-beta names that benefit from risk-on environments.

Nygren thinks that framing has decoupled from the fundamentals.

Today's large banks carry roughly twice the capital per dollar of assets they held pre-crisis.

Lending standards are tighter.

And the economies of scale have shifted increasingly in favor of large institutions, as the fixed costs of cybersecurity, anti-fraud systems, and regulatory compliance don't scale proportionally with asset size.

"The bigger the bank gets, the more of an expense advantage they have," he explains.

He doesn't expect a quick rerating.

"It's gonna take a generation for bank investors to stop focusing so much on the GFC and to think more about what normal recessions are like," he says.

His concern is that most current investors have only seen the GFC and COVID, both of which he calls "generational" events, not the kind that occur a couple of times a decade.

The Fed's adverse stress test scenarios, which many investors treat as baseline expectations, would in Nygren's view require a genuinely severe downturn to produce.

He adds a pointed observation: "If you're under about 45 years old, you weren't in the business for the last normal recession."

Valuing Cyclical Businesses.

Understanding what banks actually earn in a normal environment is also a valuation question, and Nygren has a specific methodology for getting at it.

For cyclical businesses, he discounts mid-cycle earnings, not peak, not trough.

Valuing a business on a boom period that occurs twice a decade, or on a particularly weak year, produces a distorted estimate in either direction.

For banks specifically, he looks at how much better-than-average a business performs in strong years and how far below average earnings fall in downturns, then discounts something calibrated between the two.

Applying that methodology consistently across all cyclical names is what makes rank ordering remain meaningful.

When asked whether he can ever truly know mid-cycle earnings before the cycle has passed, Nygren's answer mirrors his view on fair value: "Do you know exactly, of course not, but are you getting a better answer if you try to make those adjustments than if you don't? We think we definitely are."

Management: Alignment Over Access.

Getting the numbers right is necessary but not sufficient.

Nygren spends a lot time on the people running the business.

One-on-one management meetings at Oakmark are not primarily a tool for improving DCF accuracy.

They're a tool for assessing character.

The question Nygren is trying to answer in those meetings is not about next quarter, it’s "Is this somebody I want to be invested with?"

On incentives, he explains that management compensation should be tied to denominators.

"You don't want managements that just by making big acquisitions will hit sales growth or earnings growth targets. We want earnings per share growth, business value per share, return on invested capital, not just income."

Metrics that can be gamed through size alone are not the ones he wants driving decisions.

What distinguishes Oakmark's management meetings from the typical investor roadshow is that the team works to get executives off script.

"When we get them off script and talking about things that really matter to long-term rates of return, I think you're getting more transparency, more candor," Nygren explains.

The questions that make other investors in the room groan, focused on five- to ten-year ambitions rather than near-term guidance, are the ones he finds most informative.

Price Accuracy, Not Conservatism.

That same empirical mindset, focused on getting the answer right rather than being safely wrong, extends to how Oakmark constructs its scenarios.

One of Nygren's sharpest observations about value investing is that too many practitioners treat conservatism as a virtue unto itself, spending far more time building downside cases than stress-testing the upside.

"A lot of times you find value investors unnecessarily limiting their universe by the pride they have in conservatism, and they'll spend a lot of time looking at downside cases, but not offset that with upside," he observes.

Oakmark differentiates itself as he says "We price accuracy in forecast, not conservatism."

He acknowledges that complete risk identification before purchase is impossible.

"I don't believe you can ever get a hundred percent confident that you've identified all the risks before you purchase it," he says.

What an investor can do is minimize the probability of surprise: scrutinizing financial statements for gaps between reported earnings and cash flow, watching for expanding days sales outstanding as a possible signal of customer dissatisfaction.

Anything that reduces those risks, in his words, "is a return enhancer."

Take a Fresh Look When Something Breaks.

The same bias that causes value investors to over-index on downside cases also causes them to freeze when a stock drops, defaulting to the assumption that the market has overreacted rather than taking a fresh look.

Nygren has trained himself out of that instinct, and Oakmark's own internal data supports the discipline.

Once analysts begin lowering fundamental value estimates, there tends to be anchoring bias and downward momentum to those revisions.

"The knee jerk tendency to say the stock has overreacted is something we've had to teach ourselves not to follow and to say, this stock is now something that we need to take a fresh look at," Nygren explains.

The question he asks, about stocks already owned as much as new candidates, is simple: "Do I know enough today that I want to own it? And if I can't answer that affirmatively, then it doesn't belong in the portfolio."

The Netflix Lesson: When GAAP Gets in the Way.

That willingness to take a fresh look, and to abandon prior frameworks when the facts change, is what led Oakmark to one of its more instructive investments.

Nygren initially greeted the Netflix idea with an eye roll when an analyst brought it to Oakmark's weekly stock selection meetings.

Then he read the report.

The analyst had done an informal survey of friends and colleagues asking which subscription services they valued most.

Netflix won overwhelmingly over HBO, Sirius XM, and Spotify, while being priced at roughly half of what those services charged.

The analyst's punch line: if Netflix simply raised its price to $20 to match competitors that customers valued less, the stock would be trading at 14 times earnings.

The rest of the report laid out why Netflix was using a deliberately below-market price to build scale that would eventually become unassailable in streaming.

"One of the most important lessons for value investors out of all this is where gap accounting seems to deviate from where real value creation is. You have to be willing to make adjustments to that instead of taking pride that you're limiting your universe to low PE and low price to book stocks," Nygren says.

The thesis was later tested when Netflix reported one or two quarters of negative subscriber growth and the stock was cut nearly in half.

Oakmark flew to California, sat down with the CFO, walked through the path to recovery via password sharing monetization and the ad-supported tier, and came back convinced management was "thinking extremely economically about the future prospects of the business."

The position was fully restored, and that decision ended up more profitable for Oakmark shareholders than the Meta position they failed to size up aggressively enough.

Portfolio Construction.

That investment philosophy, built on concentrated conviction, continuous updating, and willingness to sell, is implemented within a portfolio structure designed to manage both risk and opportunity.

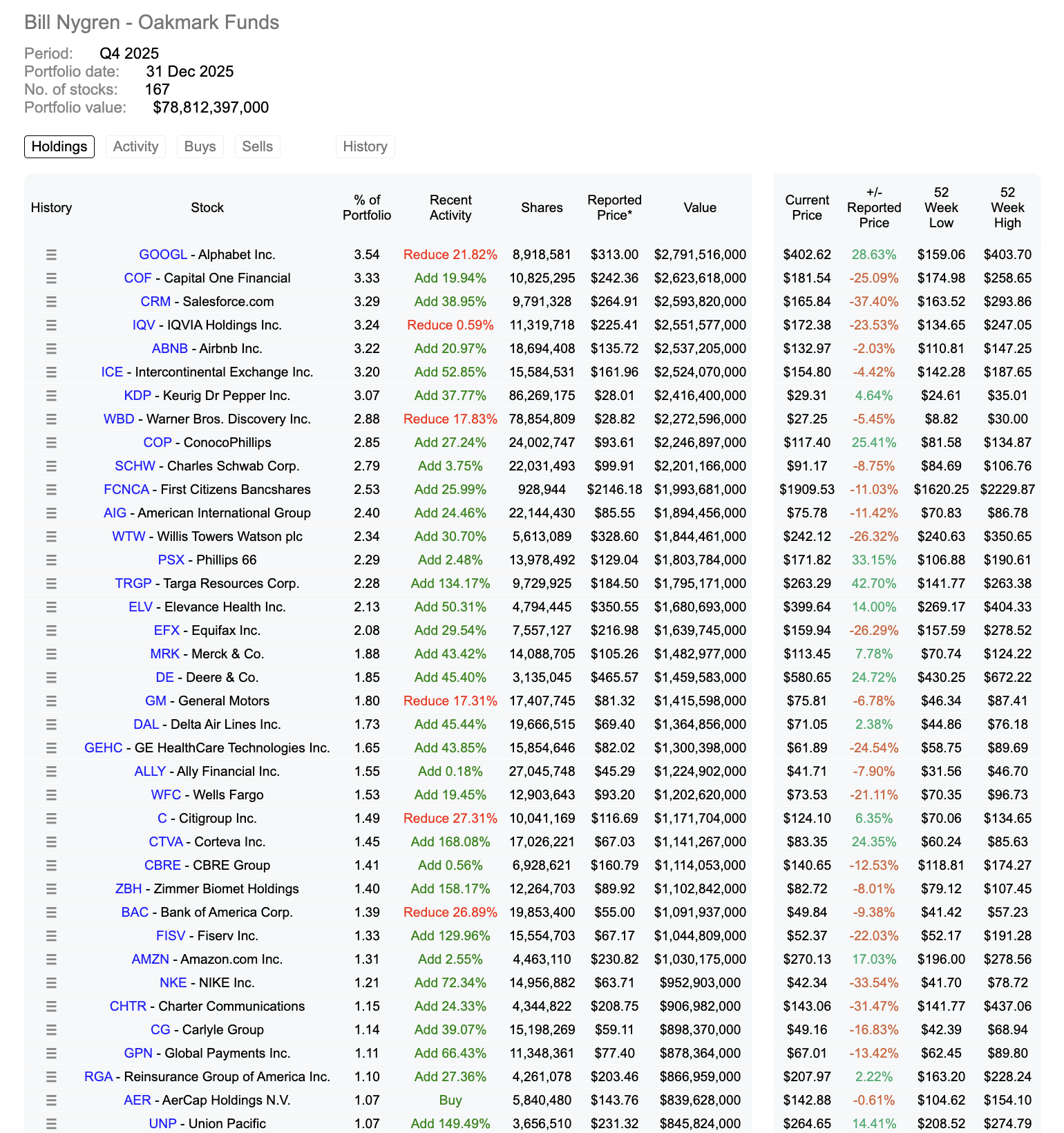

Oakmark runs 50 to 60 names, meaning the average position is around 2% of assets.

New names enter at roughly 1%, growing toward a normal weighting as conviction builds, stopping around 3%, with market appreciation carrying it higher from there.

When a position reaches roughly double the average size, automatic trimming begins.

The fund is designed to be one someone could put most of their assets in and check back on in five to ten years without closely monitoring it.

The bottom 30 names serve a diversification purpose: once the portfolio has four or five banks, for instance, adding a food stock at equivalent expected returns makes sense simply to reduce single-industry concentration.

Risk is measured by drawdown, not tracking error.

"We don't focus on tracking error as our primary risk. We focus on drawdown risk as the risk we're trying to mitigate," Nygren explains.

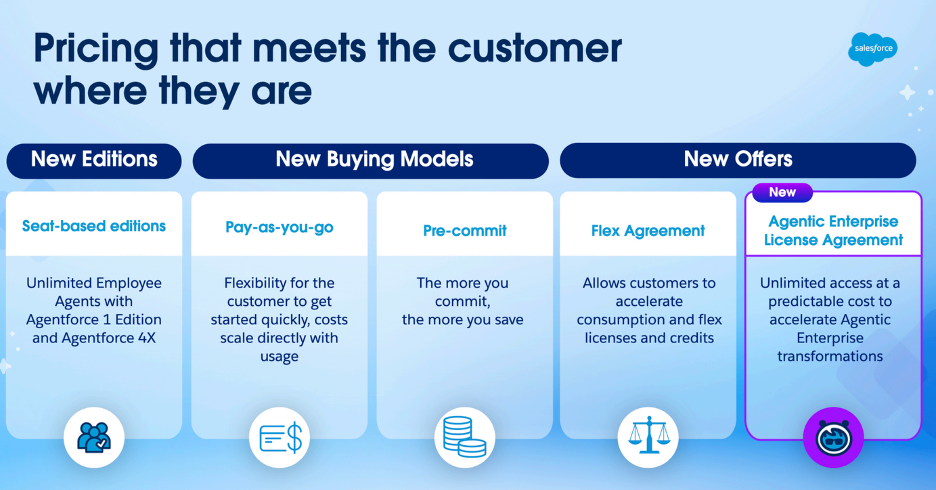

Why He Invested in Salesforce.

Within that framework, Salesforce is a current holding that illustrates how Nygren thinks about AI risk specifically, not as a reason to avoid a business, but as a factor to price properly.

The bear case is well known: AI will write the software, corporations will tear out their existing enterprise systems, and Salesforce loses its installed base.

Nygren pushes back on the timeline.

"We think we are many years away from compliance departments being comfortable with that," he says.

The long history of Salesforce being battle-tested for security vulnerabilities and operational errors is a form of institutional trust that can't be quickly replicated by an AI-generated alternative.

Nygren also addresses the seat-reduction risk directly: the argument that AI will halve the number of users paying for Salesforce licenses.

He expects the company to simply reprice.

Seat count, in his view, is a convenient proxy for usage, not the fundamental pricing principle.

"If there is a meaningful change in seats and not a meaningful change in the amount Salesforce is being used inside a company, we think they'll change the way they price."

The valuation case has also simplified.

Five years ago, owning Salesforce required believing it deserved twice the multiple of a high-quality bank.

Today, on a free cash flow basis, the gap has closed substantially.

He sees "a much lower hurdle that Salesforce needs to pass to give an average or higher than average return," and as a portfolio benefit, it doesn't correlate with the bank-heavy sectors Oakmark is already overweight.

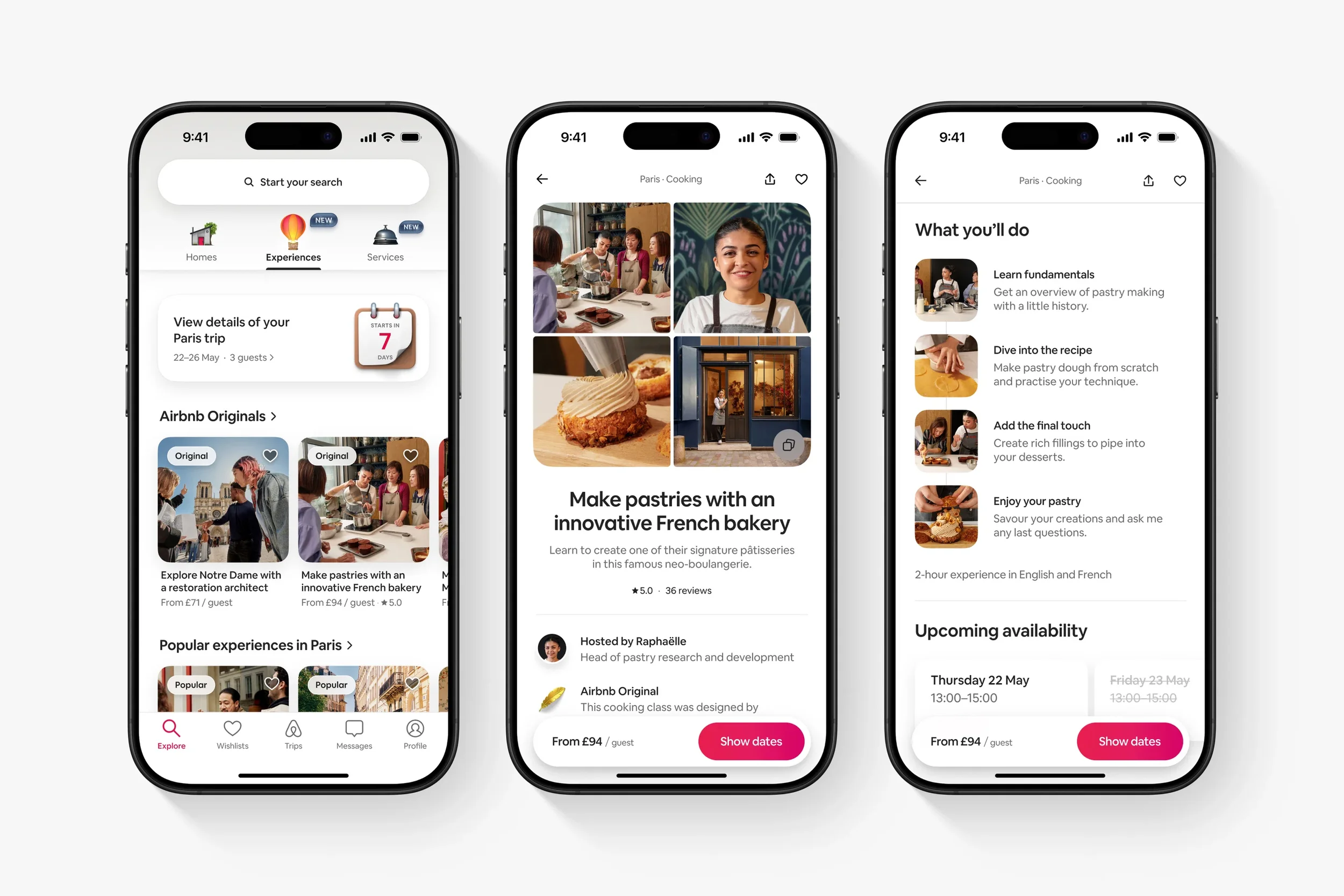

Why Bill Owns Airbnb.

A similar exercise in adjusting reported earnings to find true value drives Oakmark's position in Airbnb.

The fund currently owns Airbnb over Booking, though Nygren acknowledges the debate is genuinely live internally.

The fund has owned Booking at various points when relative valuations shifted.

The Airbnb case rests on two adjustments.

First, the company is spending heavily in areas where it isn't yet profitable but believes it has a right to win, such as in Experiences.

Adding that spending back to reported earnings, the stock looks cheaper than Booking.

Second, Airbnb's take rate, what it charges as a percentage of each transaction, is currently below Booking's, even though Airbnb primarily connects small buyers and small sellers, a market structure that arguably warrants at least a higher take rate.

"When we make those two adjustments, Airbnb comes out looking a little bit cheaper," he notes.

The key risk Nygren is watching is whether the growth spending in Airbnb's experiences segment eventually shows returns.

He is notably more comfortable with that bet than he was with Meta's metaverse spending, which at the time "sounded a lot like overgrown teenagers in their parents' basement, living in a fake world instead of the real world."

Airbnb's experiences expansion, by contrast, is a natural add-on to the core business, and management talks about it in terms that suggest economic discipline.

"I would bet within three years if those businesses haven't been able to show that they can be profitable in those businesses, they will redirect that spending," he says.

Dealing with AI Risk.

Both Salesforce and Airbnb bring us to the question Nygren is grappling with across the entire portfolio: how to price a risk you cannot fully quantify.

He is not treating AI as a pure tailwind, nor is he dismissing it as noise.

As the range of potential outcomes, in both directions, has widened, Oakmark has raised discount rates on affected businesses by approximately 150 basis points.

"That 15 year out future just isn't as sure as we used to think it was," he explains.

He is deliberate about framing it as a two-sided risk: the impact on any given business could be strongly positive or sharply negative.

What has definitively changed is the width of the distribution of outcomes, and a wider distribution demands a higher hurdle.

The 150 basis point adjustment is modest but principled, a response to genuine uncertainty rather than a capitulation to narrative.

It's the same logic he applies everywhere else: get the range of outcomes right, price accuracy over conservatism, and let the discount do its work.

What Stays the Same.

Across everything Nygren discussed, a few principles keep resurfacing.

The first is that precision is a trap.

Whether it's fair value, mid-cycle earnings, or risk identification, the goal is never to get the number exactly right.

It's to get it right enough, consistently, across a large enough set of opportunities, that rank ordering holds.

The second is that the accounting is often the last place to look for truth.

GAAP earnings penalize growth investments made through the income statement.

They reward businesses that capitalize costs and obscure economic reality.

Nygren's edge, in his telling, is the willingness to adjust the accounting rather than take pride in staying within a narrow, screen-friendly definition of value.

The third is that great investing requires updating.

The Apple story, the Netflix story, and the Meta story all share the same structure: a thesis is formed, reality arrives with new information, and the investor either updates or doesn't.

The ones who updated made multiples on their money.

The ones who didn't sold too early, or held too long, or sized a position too small at exactly the wrong moment.

The fourth is that the process has to be honest about what it can't know.

Nygren doesn't claim to identify every risk.

He doesn't claim to know mid-cycle earnings with precision.

He doesn't claim the seven-year horizon is exactly right rather than six or eight.

What he claims is that making those adjustments, however imperfect, produces a better answer than not making them.

That is, in the end, what separates a good process from a bad one: not certainty, but a genuine effort to be less wrong.

For more insights from Bill Nygren, check out this interview with him below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.