How Chris Mayer Finds and Invests in 100 Baggers

Get smarter on investing, business, and personal finance in 5 minutes.

Below are key takeaways from my recent interview with Chris Mayer of Woodlock House Family Capital.

Investment Philosophy.

Chris Mayer’s investment philosophy is built on the 100 baggers approach: own high-quality companies for a very long time.

How Chris defines a high-quality company is “have high returns on capital, lots of reinvestment opportunities, there’s skin in the game, great balance sheets.”

To protect against permanent loss, he avoids leverage and businesses that are overtly cyclical.

He also invests globally and runs a concentrated portfolio with 10-12 names.

Why Chris Mayer Concentrates His Portfolio.

Usually, when investors are looking at opportunities with higher potential returns, that tends to come alongside more diversification.

An example would be a venture capital investor where they would have a huge portfolio and they expect 90% of them to fail, but the other 10% do really well.

In the same way, Chris Mayer is looking for companies that grow 100x, but he differs in that he is concentrated.

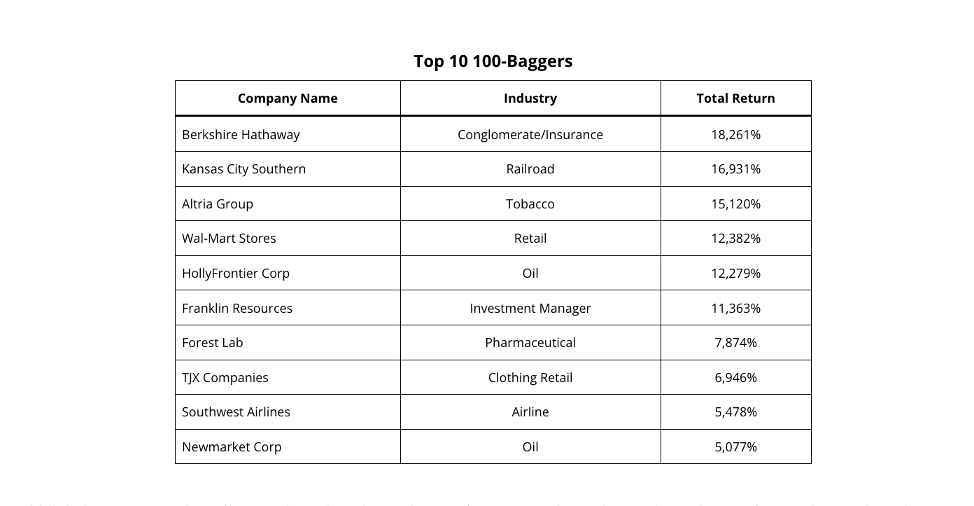

Chris states that most of the 100x baggers he studied, it takes 20-25 years to reach that milestone.

In contrast to a VC investor where they are looking to get those types of returns sooner, Chris Mayer is willing to wait longer and be more “focused more on the internal engine of compounding.”

In short, he has more confidence in the companies he owns and there’s a shorter left tail probability distribution where there’s not a big bankruptcy risk for example.

And when you are concentrated it narrows your investable universe.

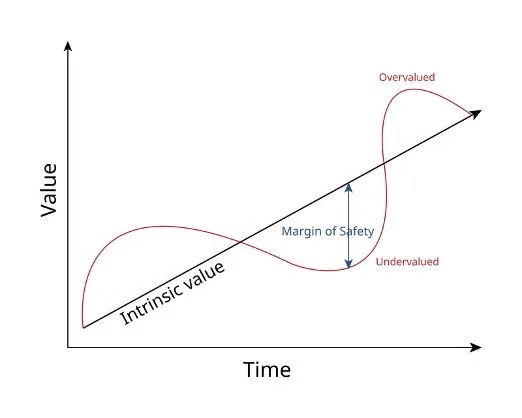

Margin of Safety.

To Chris Mayer, “margin of safety comes primarily from the quality of the business with a combination of a good entry price.”

Margin of safety doesn’t come from price along, but it comes from owning quality assets.

Chris Mayers states how in his 100 baggers study that drawdowns are inevitable.

Berkshire Hathaway was the best performing stock in that study and got cut in half at least 3 times.

Which means that “margin of safety doesn’t mean that the price doesn’t go down but it means that the business is not going to be impaired.”

The margin of safety comes from having a higher confidence in a company’s ability to compound.

Chris spends a lot of time studying the competitive advantage of the business and the industry to help increase his confidence and thus margin of safety.

He mentioned how commercial insurance brokers and Swedish serial acquirers have been around for a long time and has a long track record of compounding capital.

By focusing on the internal engine of compounding and investing in high quality businesses he has a margin of safety from loss.

This perspective also shapes how he thinks about valuation.

Valuation Framework.

Great businesses often look expensive, and it can be a risk if an investor pays too high of a price.

A lot of times these businesses carry a premium multiple for years and years, decades above the market premium.

And over a long enough period of time, the importance of that multiple, it doesn’t go away entirely, but it starts to shrink over time.

“If you have a business that compounding at 20% a year, after a decade it like a 6x increase in cashflow, so it doesn’t matter that much you pay 20 times or 25 times.”

Be a Reluctant Seller.

Mayer’s willingness to hold for many years, makes him reluctant to sell and/or trade around positions simply because valuations appear stretched.

Selling introduces multiple layers of risk: the possibility of mistiming the exit, the challenge of finding a superior replacement, and the inevitable tax drag.

“What are the odds that you’re going to get the right?” he asks.

Investors often underestimate how difficult it is to make both the sell and subsequent buy decision correctly.

By reducing the number of decisions he must make, he is effectively “cutting back on the potential to make a lot of mistakes.”

In most cases, he prefers to let his winners ride.

That said, he recognizes there is no universally correct approach.

Some investors are more comfortable trimming positions when valuations exceed their comfort zone, even if that means leaving gains on the table.

Others are willing to endure the occasional multiple compression in exchange for the possibility of greater long-term returns.

“There’s no real answer,” Mayer says.

“It’s how you want to play the game, what your goal is, and what your skill set is.”

Indeed, being a good seller is probably the hardest thing in investing.

Sale decisions are rarely easy, most often, the decision for him to sell a position comes down to changes in the business itself or the emergence of a significantly more attractive opportunity elsewhere.

Even then, conviction must be balanced with humility, as an investor must always recognize the possibility of being wrong.

Constellation Software Reinvestment Risk.

Just like how investors have reinvestment risk, companies do as well.

A great example of this is Constellation Software, which Chris Mayers owns.

Over the years, Constellation Software has grown bigger and bigger and the opportunity to deploy capital at high rates of return is decreasing.

He sees it as both an opportunity and a risk.

He is confident that Constellation Software is “going to at least double free cash flow over the next five years.”

Despite its size, he believes the company remains “a relatively small fish in a very large pond,” with ample opportunities to continue deploying capital across the fragmented software landscape.

Will Constellation’s Culture Change Due to Mark Leonard Leaving?

While culture can deteriorate as companies scale, Mayer believes Constellation’s decentralized model is resilient.

“There’s no one culture across all of Constellation, I think what unites them is they do have that framework that they use for acquisitions and the framework they use for running companies.”

With many tenured people in management that have been there a long time, they can carry that same culture forward.

He doesn’t think we’re going to see any big changes in the way they do business for a long time still.

Current Opportunities That Excite Chris.

In the beginning of 2026, the market has sold off many quality stocks that are in his portfolio.

In particular, he is interested in a Swedish serial acquirer called Röko, which was started by the previous CEO of a business he’s invested in called Lifco, commercial insurance brokers like Brown & Brown, and Copart.

Many of these quality stocks have been selling off along with software.

Software Selloff.

The market is pricing in that most of the software stocks are going out of business due to AI.

Chris Mayer thinks that while there AI risks are real for some, “the market sometimes gets in these modes where it just throws out everything altogether. The AI risks fall unevenly across different kinds of software.”

He lists how commercial insurance brokers like AJ Gallagher listed that they could experience a 6 point increase in their profit margins due to their AI iniatives, so it could also be a tailwind for some software companies.

Chris Mayer thinks it’s the incumbents battle to lose, so if an incumbent doesn’t innovate they will be in trouble.

“You have to think about why the software exists in the first place,” he says.

In terms of vertical market software it is an outsourced solution.

People use vertical market software because they don’t want to do it themselves, “Just because you have that capability doesn’t mean you’re necessarily going to do it.”

The AI risk is something that you need to stay on top of and watch and when you get disconfirming evidence, that’s when you’re going to have to change your opinion.

Right now, a lot of the AI talk is just “hand wavering” and “nobody can really point yet to a specific AI product that has made a dent in anyone’s business yet.”

It will be interesting to see when that happens but it will also be interesting to watch how companies use AI to make their businesses better.

It reminds him like the ‘90s where big box retailers made their business better because they adopted the internet and created an online business.

So AI could help make improve a business’s margin.

It’s important to have companies that are implementing AI that they can have an ROI on those investments.

Chris gives the example of how he is confident that Constellation Software can figure out how to get an ROI and not just implement AI just for the sake of doing it.

A lot of business will implement AI just so they can say they have it and it may cost them extra but it won’t give them any return form it.

Thoughts on Copart.

Copart has been selling off recently duo to two factors: 1) the risk of AV (Autonomous Vehicles) and 2) a decline in insurance volume due to some IAA market share gains.

When diving deeper on the Copart selloff, Chris Mayer agrees that the AV “at some point it is coming, but I think for now it’s not something to worry about.”

The reason why he is not worried right now is that as he explains that these adoption curves take a long time.

Chris mentioned that there are over 280mn registered vehicles in the U.S., “how long is it going to take before autonomous vehicles make even 10% of the fleet? I think those adoption curves tend to be slow. “

He read a stat from a SVP from GEICO that when front prevention crash technology was introduced in 2000, by 2009 it was only in 1% of the fleet, then by 2024 it was in 70% of new cars.

Waymo is only active in 4-5 cities and there is a lot of legal issues to work out before adoption improves.

The metric you want to look at if you are a Copart investor and are worried about the risk of AV, is how many new cars are autonomous vehicles.

Chris Mayer states that Copart does have offsets where it is much easier to total a new car, which increases total loss frequency, and they have other verticals that they can get into if they want to.

When asked if he was surprised by IAA and how they have shrunk the gap between them and Copart he says, “should have given more credit to Ritchie Bros as operators.”

But the insurance industry dynamic is that they don’t want to give all their volume to one company like Copart, “You could be the top performer and stile you could lose a little market share here to IAA.”

“It’s easy to look back now and say that Copart was probably over-earning for a stretch of time there, where they were just sort of feasting on IAA and winning all that volume. And that’s no longer going to happen.”

He doesn’t see the volume going 50/50 between Copart and IAA, it is Copart’s advantage to where the market could go 60/40 in favor of Copart.

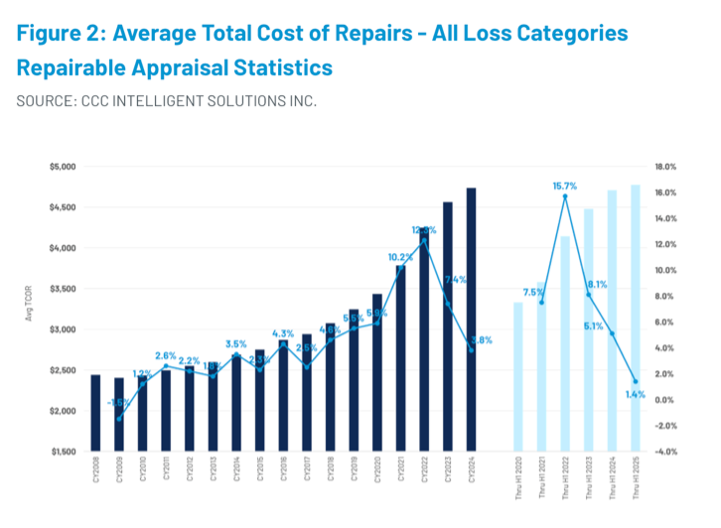

Copart has been a beneficiary of a higher loss rates due to costs to repair new modern cars.

When asked how he has the confidence that severity is going to continue to offset frequency, he states that “It’s a data point you need to watch as a Copart shareholder. That number can fluctuate as well.”

Chris Mayer mentioned that in 2020, there wasn’t a lot of people driving, but severity went up because there was a lot of speeding and distracted drivers.

He doesn’t see the cost of repairs going down.

However, he did say that “If severity does flip, that would change the story quite a bit.”

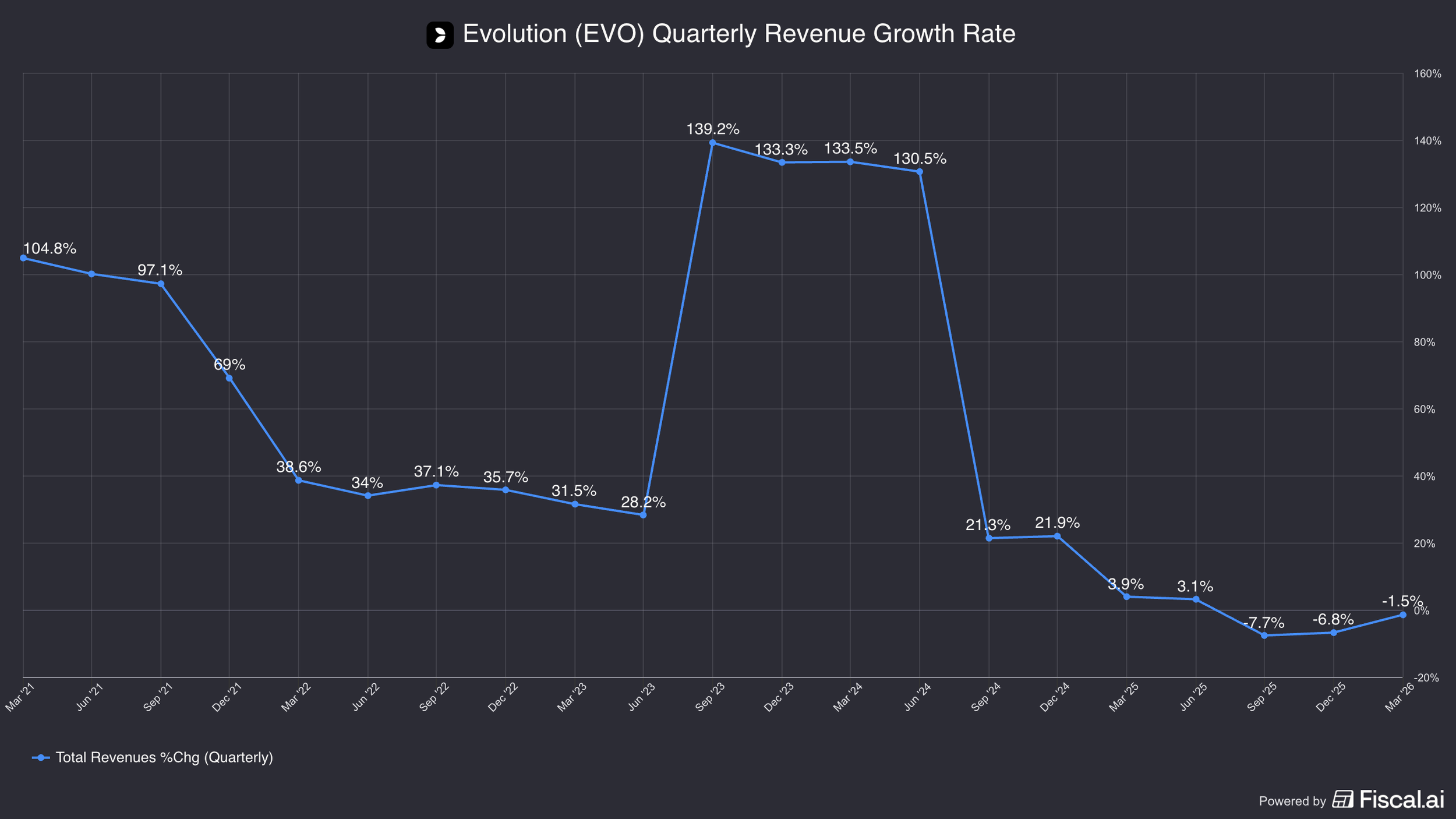

Selling Evolution Gaming.

Going back to his thoughts on selling, one notable company he did sell was Evolution Gaming.

Evolution is an online casino game maker with very high margins, where those high margins became a “honeypot” for competition.

Chris prefers to own businesses that are “middle of the road” where competition is not attracted to enter.

Most of the time, he sells a position for a company specific reasons.

Chris Mayer sold his position in Evolution for 3 reasons; 1) he noticed revenue growth was declining below 20% and that trend was continuing, 2) the company was paying out a very large dividend which he didn’t think made sense, and 3) got uncomfortable with their exposure to gray markets.

This was an example where he started a position, learned more as he owned it, then got uncomfortable with the assumptions he had when he first invested in the business.

Research Process.

How Chris Mayer finds his ideas is not systematic.

It is through years of experience, by reading a lot, talking to other investors, reading other investors’ letters, and exploring adjacent ideas.

How he found out about Röko was that he was invested in Lifco and wanted to know where the previous CEO went and found out that the previous CEO started this business called Röko.

When he finds an idea he likes, he wants to know them well.

It depends on the company, but he also likes to talk to management as well, because they can explain some things about the business which helps him gain more clarity in how the business works.

How Much Research Do You Have Before You Invest?

When you are investing other people’s money, there has to be a high hurdle rate.

If you are investing in your personal account, you can take a “flyer” position.

When you manage other people’s money you have to have a high hurdle and have a high understanding of the business before starting a small starter position.

However, the learning doesn’t stop there.

You learn a lot when you own something than when you’re just following it.

You’re learning different things that you maybe don’t appreciate as much when you don’t own it and you were just looking at it from the outside.

As Chris Mayer states, “The main reason you do all this research is to build up our own conviction, you increase the odds that perhaps down the road that you’ll make the right decision because a lot of things happen, you’ll get news and if you know it really well, you’ll know how to correctly interpret it that news and you’ll react differently that someone who doesn’t know it as well.”

Think Independently.

Chris Mayer cautions against blindly following “smart” investors because you can’t borrow conviction from them.

There’s no way to copy someone like Stanley Druckenmiller because he changes his mind so often.

And in some cases, these “smart” investors are involved in big blowups.

That is why an investor needs to think independently.

Conviction must be earned through one’s own work, not outsourced to someone else.

Make Mistakes Early.

The most valuable lessons in investing are not the ones you read in a book but the ones you experience yourself.

He encourages younger investors to make mistakes early, when the financial consequences are manageable, so that you don’t repeat those same mistakes when you are older when the sums are larger and the financial consequences are heavier.

Ultimately, Chris Mayer views investing as an exercise in patience, discipline, and emotional resilience.

There will inevitably be periods when your strategy appears misguided.

“There are definitely going to be stretches where you look like a fool,” he says.

“And if you’re not comfortable with that, then investing is going to be tough for you.”

For those who can endure that discomfort, the rewards of long-term compounding can be extraordinary.

For more insights from Chris Mayer, check out this interview with him below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.