Sea Limited Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

There are few companies that have had as much success in different businesses as Sea Limited.

Founded as a gaming company that leveraged a Tencent partnership to distribute games in computer Cafes, they eventually became a game developer of their own with a mega success in Free Fire.

Free Fire is a mobile-native first person shooter and has amassed a massive user base with over 100 million monthly users.

Since so few consumers in Southeast Asia has a means to pay digitally, they built a financial services business on the back of their gaming division.

AirPay, as it was originally called before Sea Monee, would allow users to pay in cash for their in-game purchases at physical top-up points — essentially converting cash into digital currency.

They used their gaming user base and payments functionality to launch Shopee, an e-commerce marketplace in 7 countries simultaneously in 2015.

They incentivized gamers with free virtual items if they tried the e-commerce app. Then used their digital payments business to enable transactions.

This was only the beginning of their e-commerce efforts.

They would aggressively use subsidies and promotions, as well as gamification, to acquire users and incentivize activity.

Then Covid hit and every one of their business’s boomed.

Free Fire and Shopee exploded in use as people were stuck sheltering in place.

They raised over $6 billion in 2021 and aggressive went after new markets. They would offer customers steep discounts and gamified promos to shop on the site, while offer sellers very low commissions to list.

They launched Shopee in India, Brazil, Argentina, Chile, Colombia, Mexico, France, Spain, and Poland in rapid succession.

At peak, Sea Limited was valued at $200 billion, making it one of the most valuable tech companies in all of Southeast Asia.

Then almost everything went wrong.

As Covid restrictions were lifted, gaming activity fell.

Quarterly gaming active users fell from 729mn in 2021 to 490mn in 2022.

India, one of Free Fire’s largest markets, banned the game when they blanked banned a lot of apps considered Chinese (Sea Limited is based out of Singapore and pushed back against this ban with no success).

In a 1,000 word memo, CEO and Founder Forrest Li said, “With investors fleeing for ‘safe haven’ investments, we do not anticipate being able to raise funds in the market”…

He pushed the company to be cash flow positive in 12 to 18 months.

Without the support of capital markets, they curtailed ecommerce promos. And this came alongside consumer’s being able to shop offline again.

Shopee’s GMV growth slowed from 77% in 2021 to 7% in 2023.

Shopee pulled out of India just five months after launching, then exited France, Spain, Poland, Argentina, and scaled back operations across Chile, Colombia, and Mexico in rapid succession

Business travel was banned. Hotel stays for business trips were limited to $150 a night. Top management forged their cash salaries.

The stock, which peaked around $360, was not trading around just $35.

But the plan started to work.

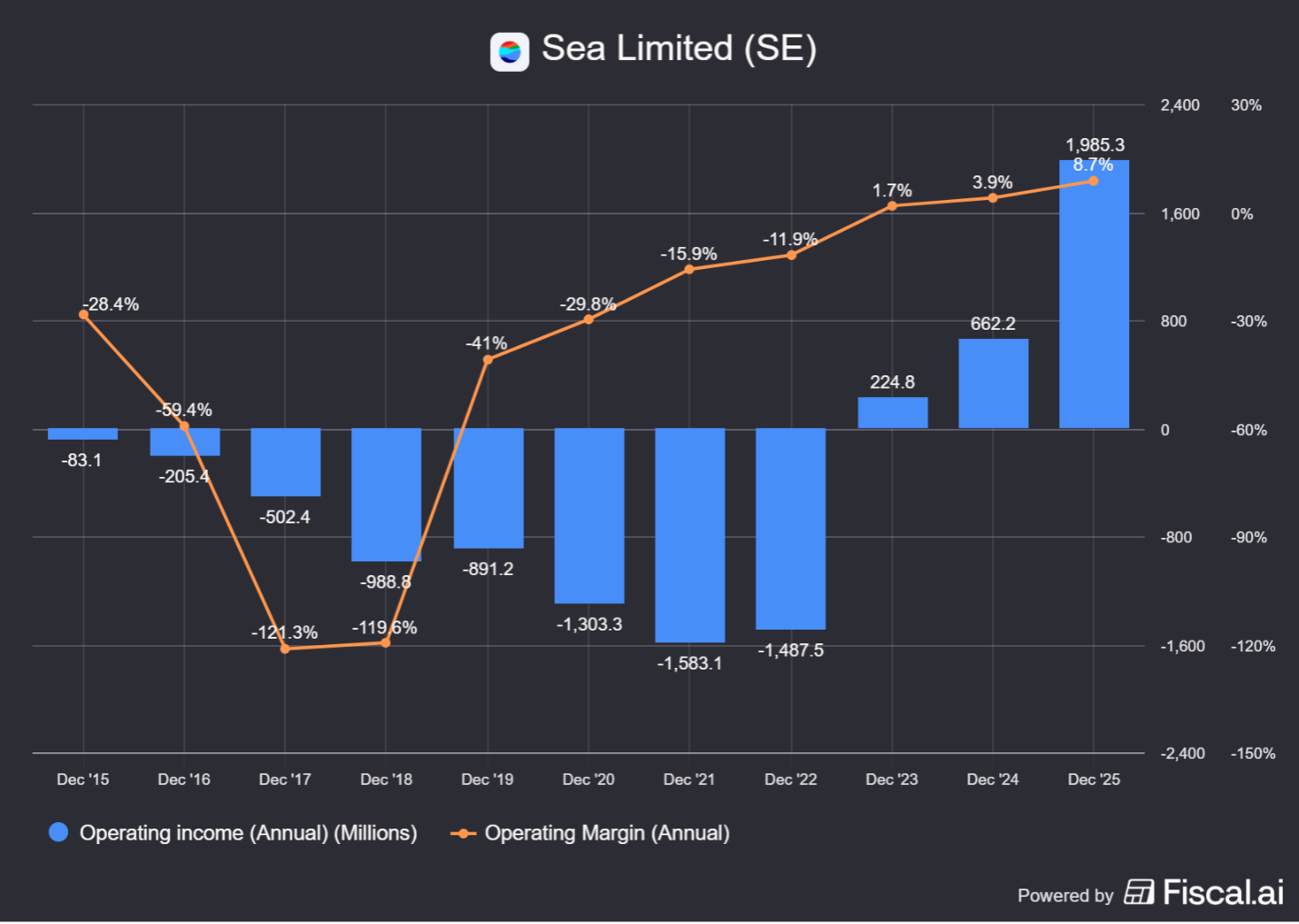

In 2023, they posted their first operating profit as a public company at $225 million, up from a $1.5 billion loss a year prior.

They continued to double down on markets that were working—their core 7 South East Asian markets and Brazil.

To many investor’s surprise they even became EBITDA positive in Brazil.

This was especially unexpected given that they focused on the lowest end of customers—the least affluent customers in Brazil who would order very cheap goods, often with promotions.

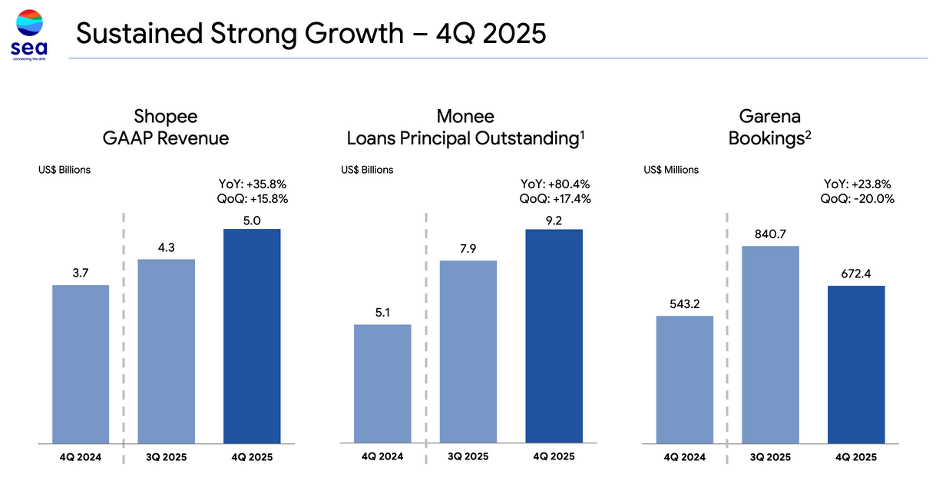

As they continued to clamp down on expenses, they posted their first ever positive operative income for Shopee in 2025 at $580 million, up from a -$140 million loss the year prior and a -$2 billion loss in 2022.

At the same time, their Sea Monee division continued to post strong growth, generating $970 million of EBIT, +47% y/y.

And even their gaming operations started to grow again with operating income of ~$1.2 billion, +21% y/y.

Despite their improved profitability and continued strong growth—top line grew 36% y/y in 2025, Sea still faces significant investor doubt.

This stems from the segment of the market they have focused on and the fact that a lot of their markets have less affluent shoppers.

In contrast to Amazon or Coupang, whose average consumer is well off and seldom ever expects a discount, Shopee’s customers were acquired in a heavily promotional period—and the fear is that they have been habituated to those discounts.

Additionally, Southeast Asia is a wide geographic area with over 25,000 islands. How can you offer fast shipping across all of that area in an economic way on orders that have an AOV (average order value) of $9?

Their solution has been to create their own in-house logistics arm—SPX Express—and focus on the “Tier 1” cities first.

In-housing logistics has allowed them to save a lot on costs and provide faster delivery in the process.

80-90% of their orders are already next day (per AlphaSense expert call)

Investors started to appreciate the massive scale of Shopee and it’s leading e-commerce position in Southeast Asia, as well as the growing profitability of it’s Sea Monee Arm.

From the 2023 lows, the stock was up more than 400% to $195…

But then they guided 2026 EBITDA to be at least flat compared to 2025.

Investors started to worry that they were entering another investment phase and margins wouldn’t improve for some time…

This was compounded by fears that TikTok Shops is gaining a lot of traction in their South East Asian markets—was some of this investment to defend their turf and thus throwing new doubt on long-term profitability?

Add in fears of rising oil prices, which could have a negative impact to SEA economic growth and a growing loan book that has yet to be tested in a recession was enough to send the shares back down 55% to $90 today. So what should an investor make of Sea Limited today?

But first we will touch more on their business.

Business.

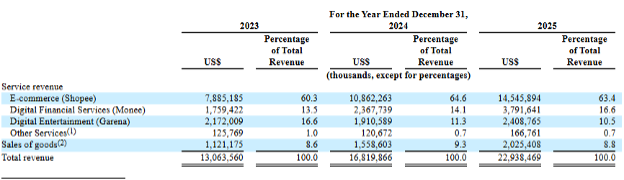

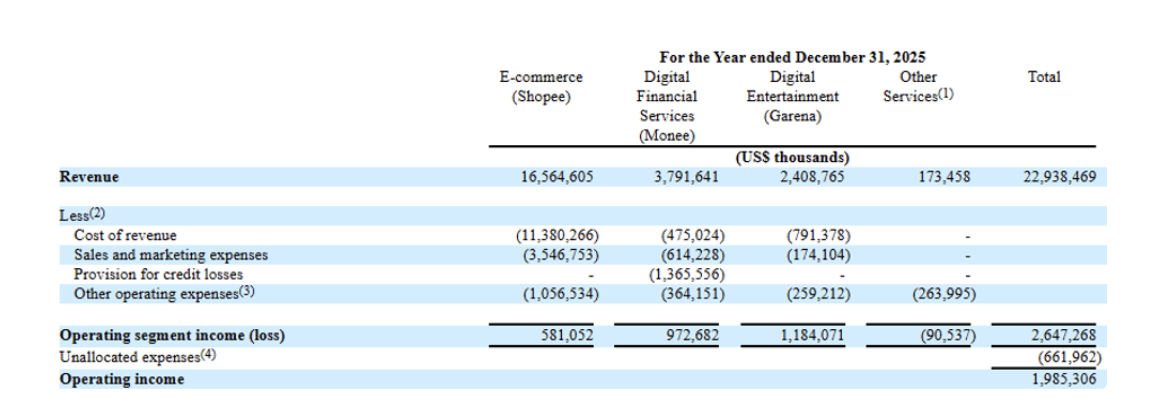

Sea Limited generated $22.9 billion in revenues in 2025 with an operating margin of 9% or ~$2 billion in EBIT.

They have 3 primary segments:

1) E-Commerce (Shopee) which is 63% of revenues

2) Digital Financial Services (Monee) which is 17% of revenues

3) Digital Entertainment (Garena) which is 11% of revenue

The last revenue segment listed below is “Sales of goods” and is from their 1P ecommerce operation, where they are the merchant of record. Relative to their GMV, this is a small portion of sales (about 1.5%).

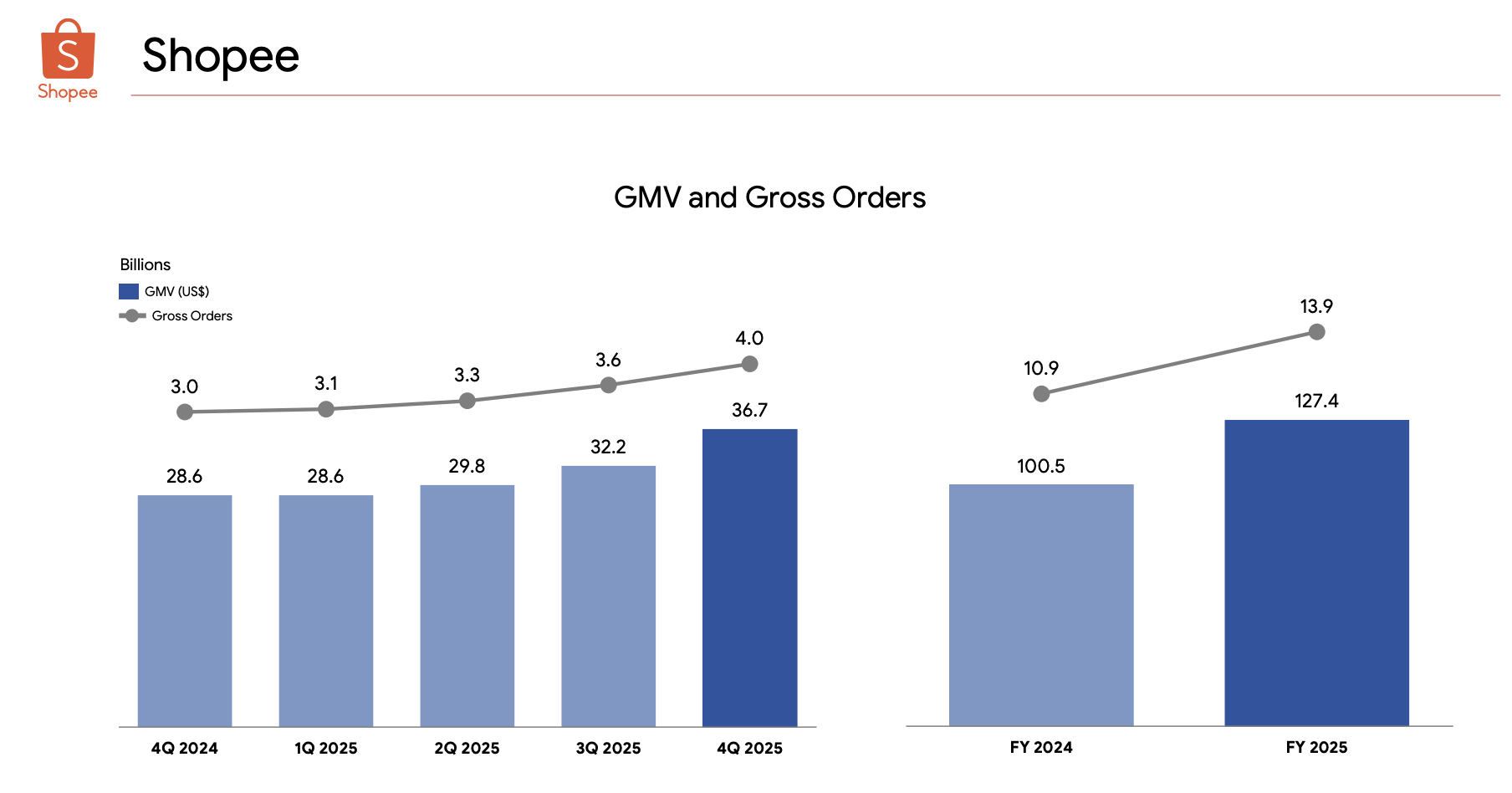

Shopee has 400 million buyers and 20 million sellers. Most recently their monthly active buyers increased 15% y/y and frequency grew 10%. Their logistics arm, SPX Express, processes 30mn parcels a day. Their Shopee VIP program (similar to Amazon Prime) has over 7 million members now, and members spend 30-40% more after joining with total VIP Members now contributing to 15% of GMV in 4Q25.

Shopee makes money by charging a seller commission, which ranges from 8-18% depending on category and country, but averages around 13%. They will also charge sellers for shipping and advertising.

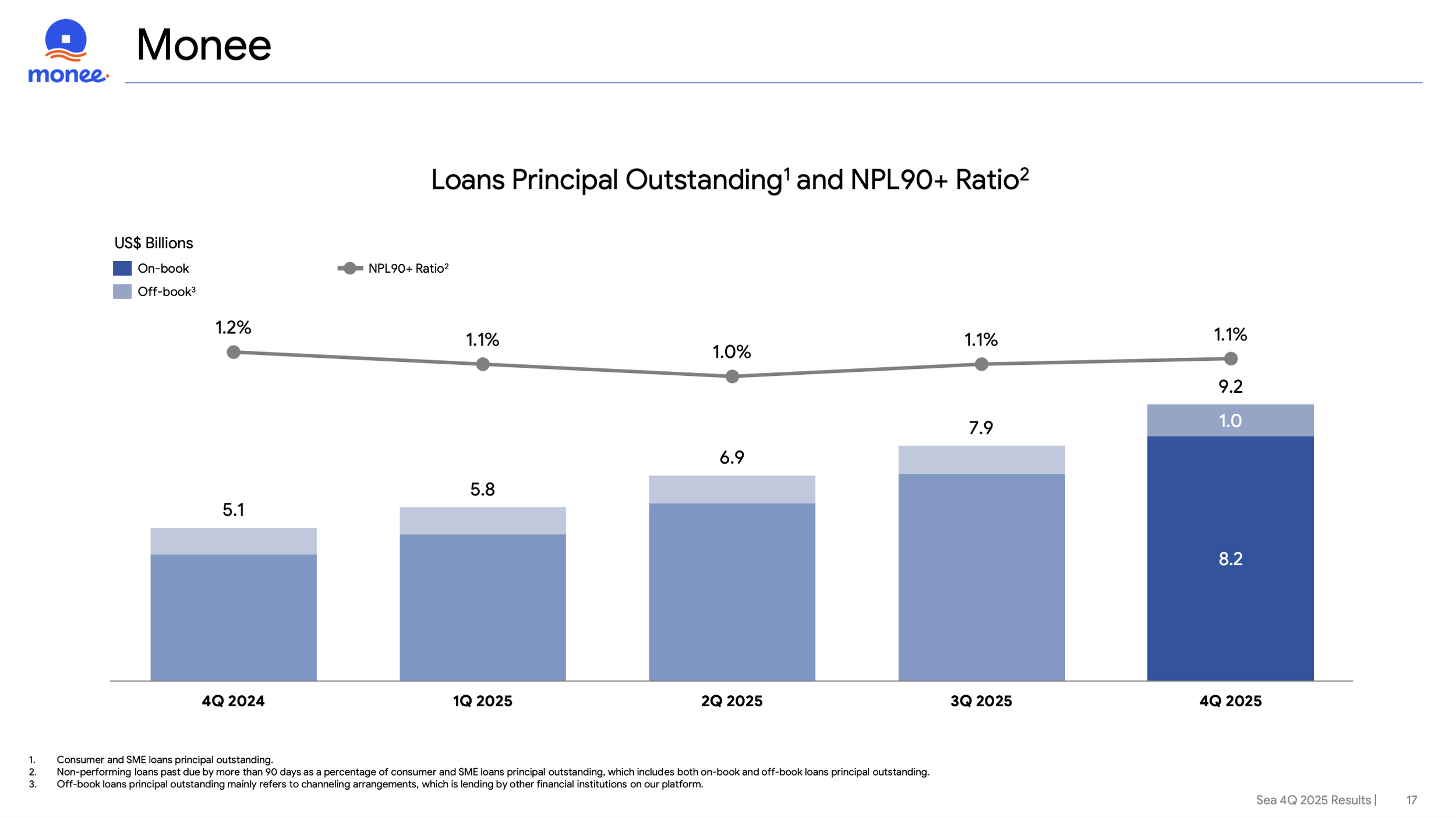

Monee’s products include mobile wallets, QR payments, merchant payment processing, BNPL, personal loans, merchant financing, micro-insurance policies, as well as banking services.

They have various bank licenses in Singapore, Malaysia, Indonesia, the Philippines, and Brazil, with Thailand pending.

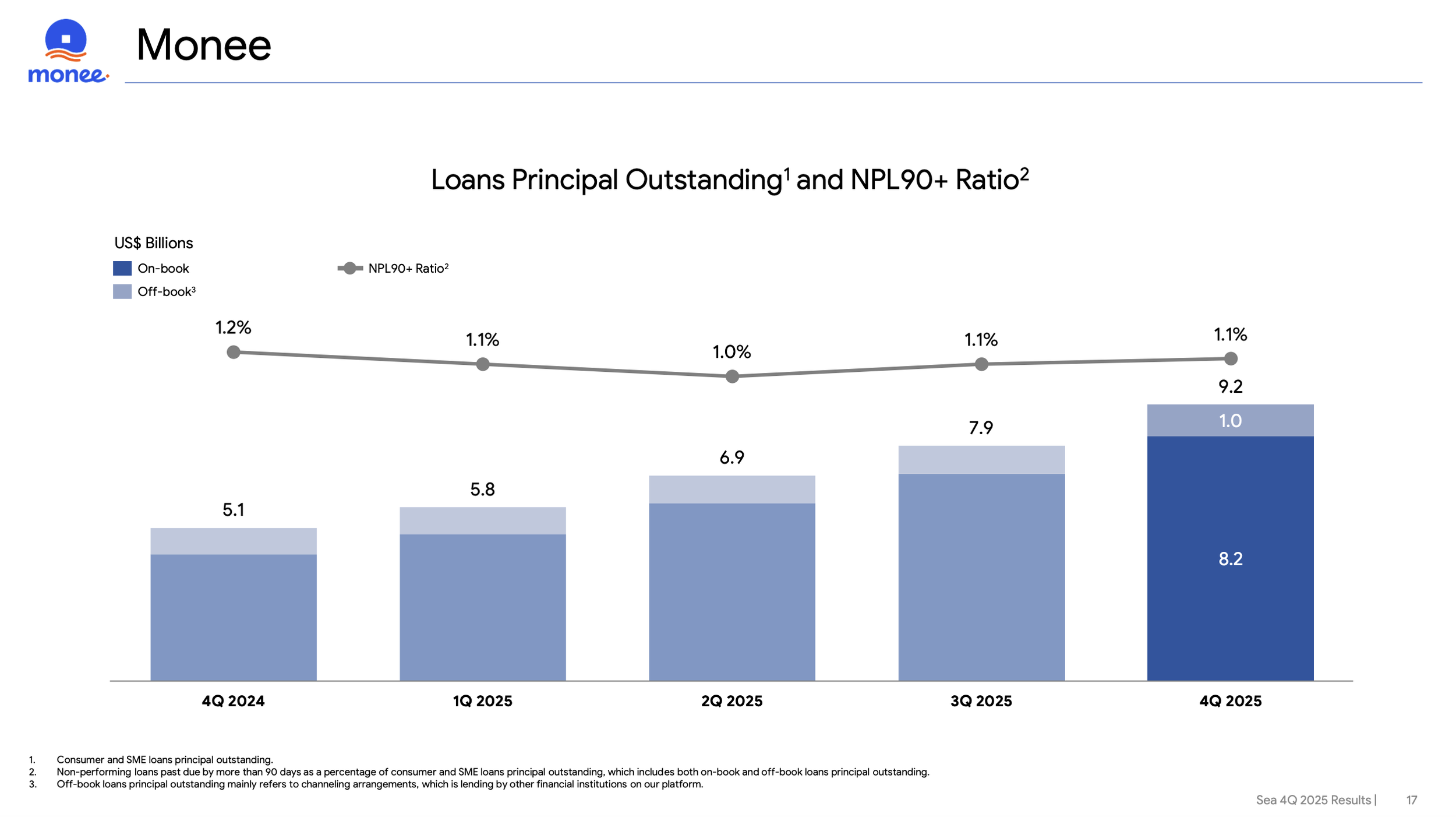

Their biggest money maker though is lending—particularly BNPL or ShopeePayLater loans where the consumer takes the loan out at the time of purchase on Shopee. They also have been growing their consumer personal loan book.

Lending activity has increased 80% y/y to $9.2 billion.

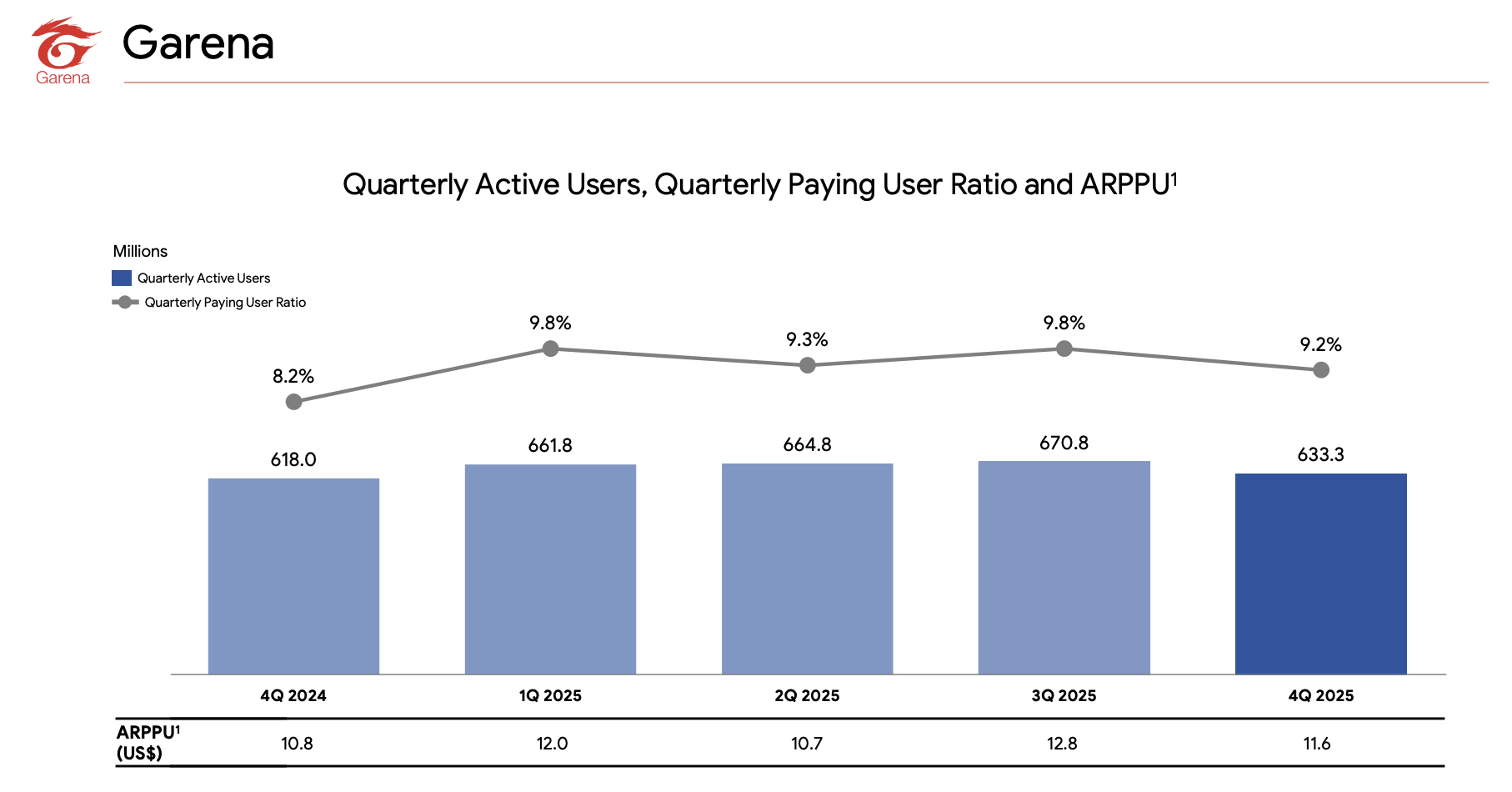

Garena is a publisher and game developer. Their largest owned IP is Free Fire (and they have essentially no other games). Nevertheless, Free Fire is a massive mobile game and they monetize it through microtransactions for digital items and selling season passes.

As a publisher they help other game developers with localizing their IP, running promotions, e-sports leagues, and maintain the payment infrastructure that allows numerous native payment methods—including infrastructure that lets people pay in physical cash at various top up points to convert to digital currency.

They have a partnership with Tencent, who owns several massive games such as Arena of Valor, Call of Duty Mobile, among others. They also recently struck a partnership with EA Games to distribute FC Mobile (Football game).

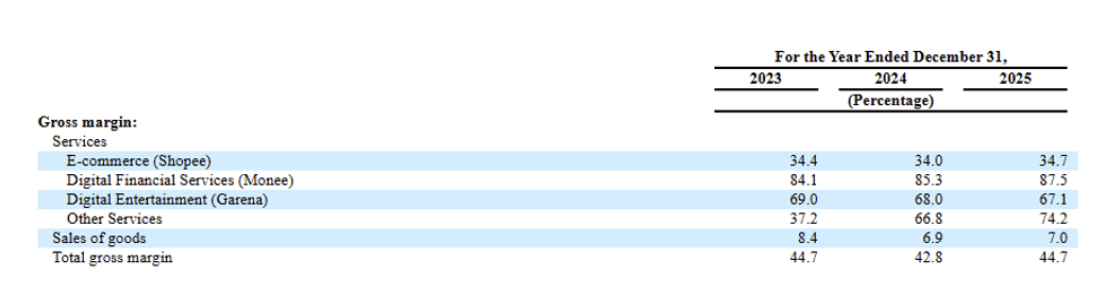

We can see that gross margins for Monee is the highest, at 88%, followed by Garena at 67%, and Shopee at 35%. (Loan losses aren’t included in cost of goods sold though)

In terms of operating income, Garena is their largest contributor at $1.2 billion, followed by Monee at $1 billion, and Shopee at $600 million. In total they generated about $2 billion of operating income (after unallocated expenses).

Despite Garena being their largest money-maker today, Shopee is really the key to the business because it’s success will not only drive a lot of seller commissions and advertising revenue, but it is critical to acquiring customers for Monee with a low CAC.

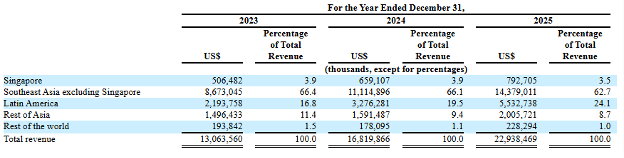

In terms of what geographies are the most impactful, South East Asia is 63% of revenue with Indonesia being the most impactful country within that, followed by Thailand. Latin America, which is primarily just Brazil (they do have cross-boarder trade in other countries) is 24%.

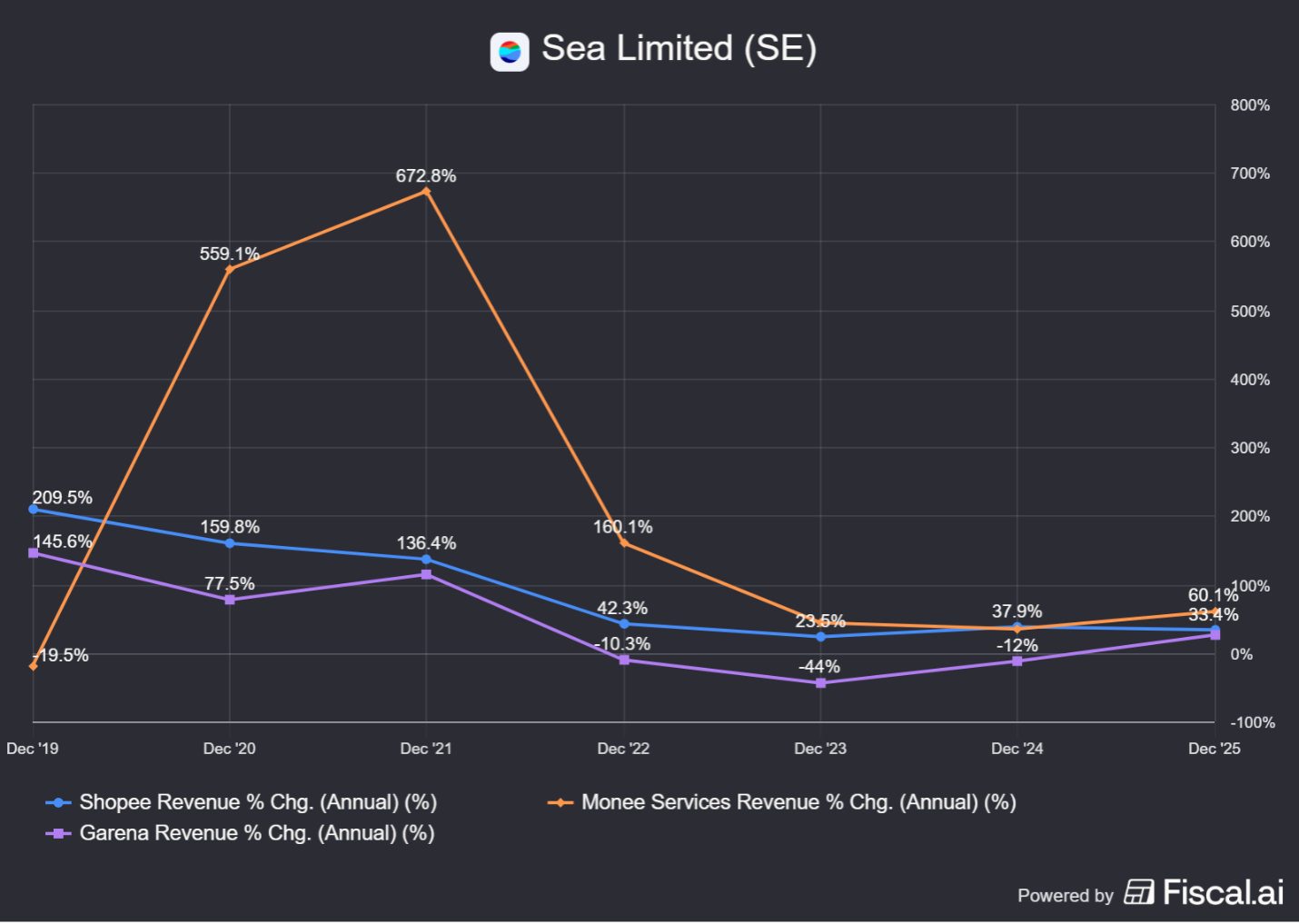

We can see each segment is growing strongly now—Garena at 25% y/y, Shopee at 33%, and Monee at 60%.

Profitability has also been improving.

Let us now touch on competition.

Competition.

We will focus on competition in e-commerce and Monee separately.

E-commerce.

In e-commerce, their biggest competitor in Southeast Asia is currently TikTok Shops.

The other largest player is Lazada, owned by Alibaba. However, after becoming an early leader over a decade ago, they have been bleeding share as their focus is elsewhere and Shopee was far better able to localize the experience for native shoppers.

Tokopedia was another notable player in Indonesia, but they have since been acquired by TikTok Shops (because it became illegal for a social media company to mix entertainment with shopping. Acquiring Tokopedia and using their infrastructure got around this though).

In Brazil, Sea also competes against Mercado Libre, who is still the dominant player there. Mercado Libre also recently lowered their free shipping threshold and announced a “slow shipping network” that can better compete against Sea’s value prop of cheaper goods but with worse delivery.

Zooming out, a lot of this “competition”, isn’t really direct competition to Shopee.

There is a difference between high-intention commerce and discovery.

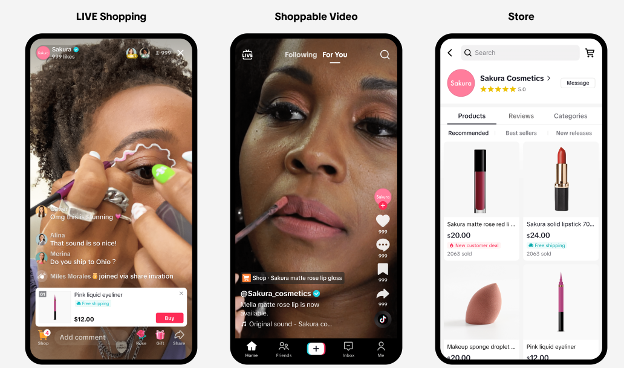

High intention commerce is when you search in app, knowing exactly what you want. Discovery is when you have no idea that you wanted to buy something, but were either browsing for fun or an item was pushed to you like in a TikTok or Instagram ad.

Most of the time when a user opens the Shopee app, they want to buy something. They also usually know what that is.

In contrast, almost no one ever opens up TikTok with the intent to purchase something. Rather they are shown a TikTok of a product or a live stream and get convinced to purchase something.

While it is true that Shopee does try to gamify the shopping experience to make it more fun and entertaining—and they also have their own live streams—all of which does push them a little more in competition with TikTok. Still though, the majority of their buyers are not on the app for entertainment.

By virtue of this different customer intent, different categories of purchases follow.

Customers will tend to purchase more essential goods on Shopee, whereas they buy more spontaneous goods on TikTok. The best ecommerce platforms tends to own the “essential” purchases because they tend to repeat and thus are higher frequency, as well as higher trust transactions.

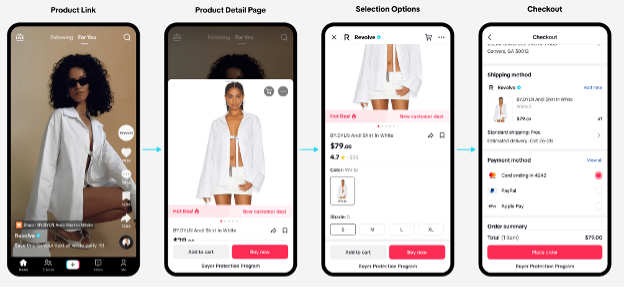

Discovery transactions are great for sellers though because it allows them to sell something they would have struggled to otherwise. In this respect, TikTok Shops is very similar to an Instagram ad.

Discovery commerce also works well with slower shipping times because these are items the customer didn’t even know they wanted moments ago, so they are fine waiting.

However, if they want to move to more intention-driven commerce then they will need to work on shipping speeds.

Here Shopee has TikTok beat with faster shipping across far more items and is also able to do so at a lower cost.

Aware of this shortcoming, TikTok is rolling out fulfillment by TikTok.

Shopee in turn has partnered with Google and Meta to help sellers find customers on those platforms. Sellers can also pay for search ads on Shopee to help their results surface.

Since there are so many small sellers and they all need an audience, something like TikTok Shops makes a lot of sense for them.

Still though they have to come up with creative content or pay influencers/ KOLs (key opinion leaders) affiliate fees, which eats into margins.

Both Shopee and TikTok should be able to do just fine in the Southeast Asian market, but if growth slows for some reason in the future for Shopee, the reason is most likely TikTok.

FinTech.

Sea Monee has much stronger competition in this segment.

There are a few regional players and then several local champions.

Both ride-hailing giants Grab and GoJek (now GoTo after merging with Tokopedia. They only sold a 75% of Tokopedia to TikTok) have their own financial services arms.

Grab is one of the largest regional players and GoTo is one of the largest players in Indonesia.

DANA is another large player in Indonesia.

GCash, which is a partnership between Ant Group (AliPay) and Global Telecom is the biggest in the Philippines.

TrueMoney, backed by AntGroup and CP Group, is a dominant player in Thailand.

MoMo and ZaloPay are two large players in Vietnam.

Touch ‘n Go is a payment leader in Malaysia.

And South America has their own dominant players including Mercado Libre’s Mercado Pago and NuBank.

Generally speaking, Sea Monee is a #3 player or #4 player in most markets. They primarily leverage users on Shopee to try to acquire fintech users who could become borrowers either through their BNPL product or personal loans.

They don’t need to be a dominant player in order to make money though. South East Asia is a very underbanked market so there is ample room for multiple players to grow. Sea Monee just needs to keep their customer acquisition costs low and not reach on their credit underwriting.

We will now touch on a few other risks before moving into valuation.

Risks.

Credit Risk.

The bigger concern than competition with fintech is that they grow too quickly and get loose with their loan underwriting when reaching for market share. This could result in much larger than anticipated losses down the line.

Even if they try to grow prudently, it should be stressed that they have never undergone a significant credit event, so we don’t know how conservative their underwriting is—in fact neither does Sea Monee!

The disclosures they do give around their lending activity, do not give us good visibility into how each vintage (cohort) of credit borrowing is doing. They also do not disclose what their net interest margin after losses is—a key figure to gauge lending profitability.

Generally speaking the idea is that the interest rates in these markets are more than high enough to offset the ample losses that come with lending to consumer subprime borrowers with no credit history.

This is why those these credit markets are wildly more profitable today then the equivalent credit products in a more developed economy like the U.S.

Customer Acquisition Costs.

It is also worth mentioning that historically a lot of eWallets used to have more rewards and those were in part bank funded. Since an eWallet transaction doesn’t have a large merchant discount rate they cannot self-fund rewards with it. There also isn’t much room for profit.

Most of these fintech platforms offer this service in hopes they can later cross-sell consumers a higher margin product. This adds a new vector of fintech competition (the eWallet) and fintech players may decide to fight for market share again in the future, increasing the customer acquisitions costs of this business.

Monee does have a unique CAC engine with Shopee where they can acquire the customer right on platform and sometimes at check out.

Regulation.

The other consideration is regulation. Various countries have moved to regulate interest rates. While regulation has still allowed companies like Sea to make a good lending margin even after taking into account losses, this count change in the future.

Self-Publishing.

Garena still publishes many titles for Tencent, but Tencent created their own publishing arm focused on SEA in 2021 called Level Infinite. Tencent has started to self-publish some games like Honor of Kings through their own self-publishing arm.

Riot games, which is owned by Tencent but operated independently, recently opened offices throughout Southeast Asia and decided to self-publish their League of Legends game.

A further push to self-publishing could weigh on Garena’s earnings. Free Fire will still remain their property no matter what though.

We will now turn to valuation.

Valuation.

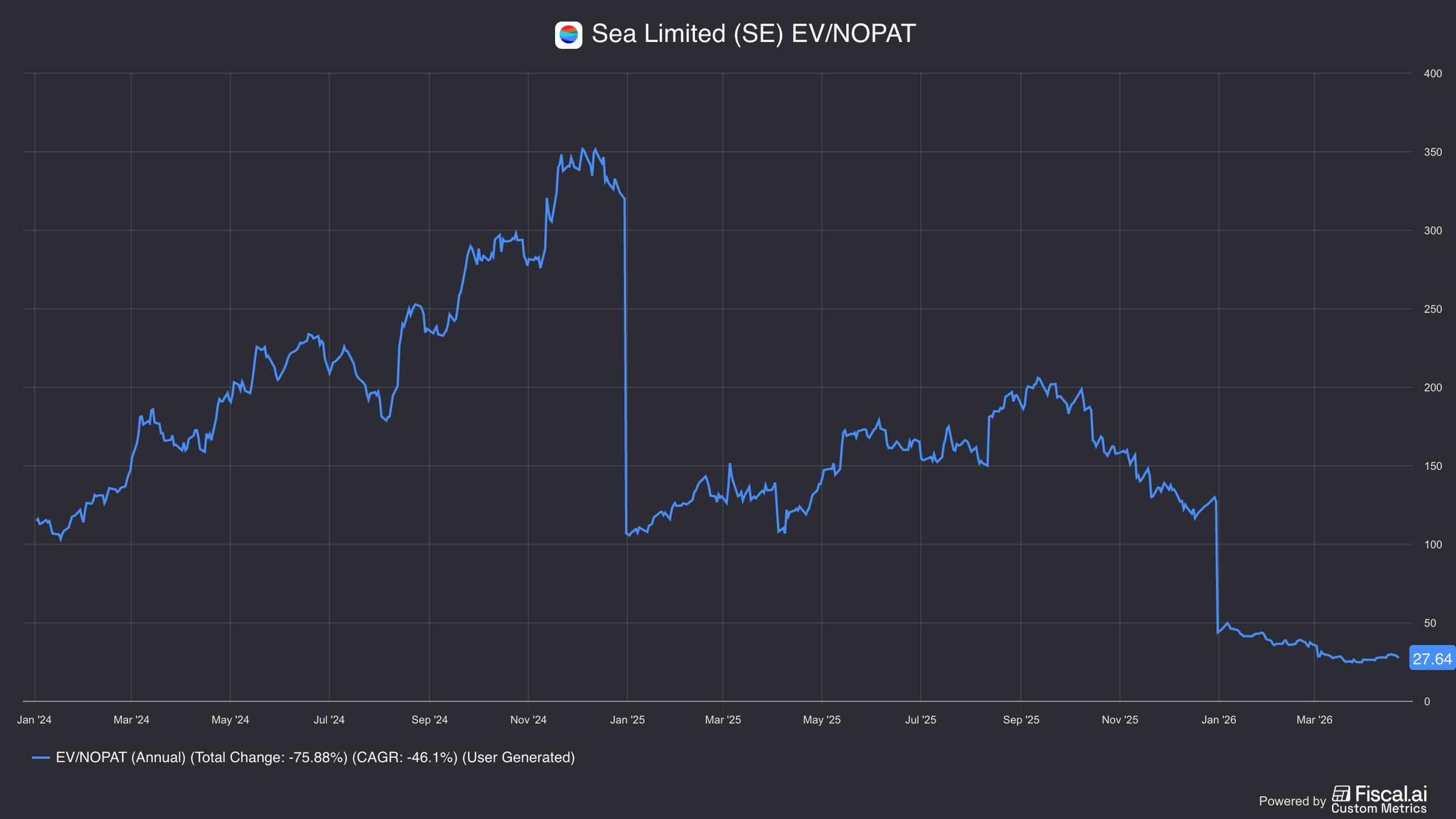

At a stock price of $86, Sea Limited’s market cap is $53 billion. This drops to an enterprise value of $43 billion after about $10 billion in net cash.

With about $2 billion in GAAP operating income, this is an EV / NOPAT of about 28x.

An investor would only need about 1 year of 30% growth for Sea to trade at a market multiple. While 2025 revenues did grow 36% y/y and operating income grew 200%, they guided 2026 EBITDA to be at least flat, suggesting there will not be a material profit improvement next year.

But if you believe that Sea is investing to grow the business (and not just defend it) then they have latent power to raise margins by cutting expenses when they are ready to.

Getting a mature margin figure is particularly hard for Sea given that they have 3 different businesses and operate in markets with no mature comps.

Below we will create a framework that allows investors to think about long-term earnings power, but an investor should slot in their own assumptions that they are comfortable with.

Sea has noted that they have a long-term margin goal of 2-3% GMV. While some of their GMV may be inflated do to brushing and cancellations, this is likely part of the reason why this figure is lower for them versus other ecommerce peers.

On the other hand, it is true that their markets do have on average less affluent customers and the population density is less. Still though they should be able to continue to improve profitability from the 0.45% EBIT as a % of GMV they are at today (this figure is about 70bps on EBITDA but I prefer to look at EBIT).

Simply layer in advertising and benefiting from operating leverage as revenues grow should get them there.

If we assume 1.5% EBIT as a % of GMV, that gets us $1.9 billion in EBIT.

Their $127 billion in GMV is likely inflated though and that figure still seems conservative on their inflated number. (See this Tweet for more).

If we assume 30% of their GMV is transactions that aren’t completed, then that is about $90 billion of actual GMV. A 2% EBIT margin on this seems fair if not rather conservative with advertising. That gets us about $1.8 billion or a similar figure.

Fred Liu of Hayden Capital made the point in his investor letter that China is the worlds most competitive ecommerce market and companies can still make ~2% EBITDA / GMV (probably closer to 1.5% on EBIT).

A conservative investor would want to assume 1.5% EBIT as a % of GMV. A more optimistic investor could be comfortable with 4%. On 4% margins and the $90 billion “real” GMV estimate their Shopee mature earnings are $3.8 billion.

South East Asia’s e-commerce penetration is around 20% whereas China is closer to >45%.

In addition to that, total retail spend is growing around 5%.

If it takes 10 years for Southeast Asia to match China’s penetration, that implies an e-commerce growth rate of about 14%.

If Shopee just maintains their market share, they will grow that amount. That could be about $330 billion of “real” GMV (or $470 billion in reported GMV).

On 1.5% EBIT to GMV, that is $5 billion in EBIT. (With upside if they can monetize better).

Sea Monee is also hard to model, but we will similarly create a framework to think about it. We are taking some liberties with these estimates because of limited disclosures.

Monee EBIT was $970 billion last year with a 25% margin.

At maturity, this could be in the 30-40% range as they stop acquiring so many new borrowers.

They should be able to grow this at least as fast as GMV grows as a lot of lending is tied to e-commerce activity.

However, they are moving more to off-platform loans, which will further increase their growth.

In 4Q25 15% of total SPayLater loans were off-platform (not tied to Shopee). This figure for personal loans and SME loans is over 50% in 2024.

For simplicity, we will not assume off-platform grows quicker than on-platform lending, but it is very possible that it does.

Right now, if 60% of their $9.2 billion in loans is on-platform, that is about 6% penetration of their “real” GMV.

If this grows to 15% and the 40% off-platform loans at 40% stays flat, in 10 years that implies a lending book of $83 billion.

With a Net Interest Margin 25% (estimated), that is $21 billion. At a 35% margin that gets us $7.3 billion.

Garena is probably the hardest to estimate as it’s success if very tied to a single game—Free Fire. Growing at just 5% just us just shy of $2 billion in a decade of EBIT.

Between Shopee generating $5 billion , Monee generating $7.3 billion, and Garena at $2 billion that is $14.3 billion in EBIT.

If we subtract $1 billion of unallocated costs and tax it, we get $10.2 billion in NOPAT.

If they are only growing low single digits, a 20x multiple could be fair. If they are still growing at a teens rate, then 30x may be appropriate.

That gets us a 10 year out future value estimate of $205 billion to $305 billion. From today’s enterprise value, the implied returns are 17% to 22%.

Now the one thing I can say for certain is that these estimates will be wrong. An investor should sensitize multiple different estimates and scenarios to gain comfort with the return profile.

Of course, all of these estimates assume a high degree of success. The downside for Sea is much more prosaic.

Competition continues to weigh on Shopee’s ability to monetize and could push down lending rates significantly.

In a bear scenario Shopee’s margins could struggle to improve from here as they have to continue to offer subsidies to fend of TikTok Shops.

And Monee’s margins could be squeezed. Losses could also be much higher than they anticipate.

Garena’s Free Fire could start to lose interest as a new generation of players prefer a different game.

There is A LOT that could go wrong.

On the other hand, a lot has already gone wrong for Sea Limited and they have proved to be quit apt at adapting to different markets and opportunities with Founder Forrest Li at the helm, who owns about 16% of the company.

Ultimately, it is up to an investor if they are comfortable making such high growth assumptions over a long period of time and trusting Forrest Li to navigate shareholders to success.

For more on Sea Limited, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.