FICO Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

For years investors have placed a very high multiple on FICO.

The stock recently traded at a P/E ratio in excess of 80x.

What gave investors comfort was the reliance of FICO scores deep throughout the financial plumbing system.

Nothing perhaps showcases this better than their ability to aggressively raise prices.

For years they underpriced their value, but over the last decade they have swung to the other extreme.

A FICO Score that used to cost $0.60 in parts of their business, now can price at $43.

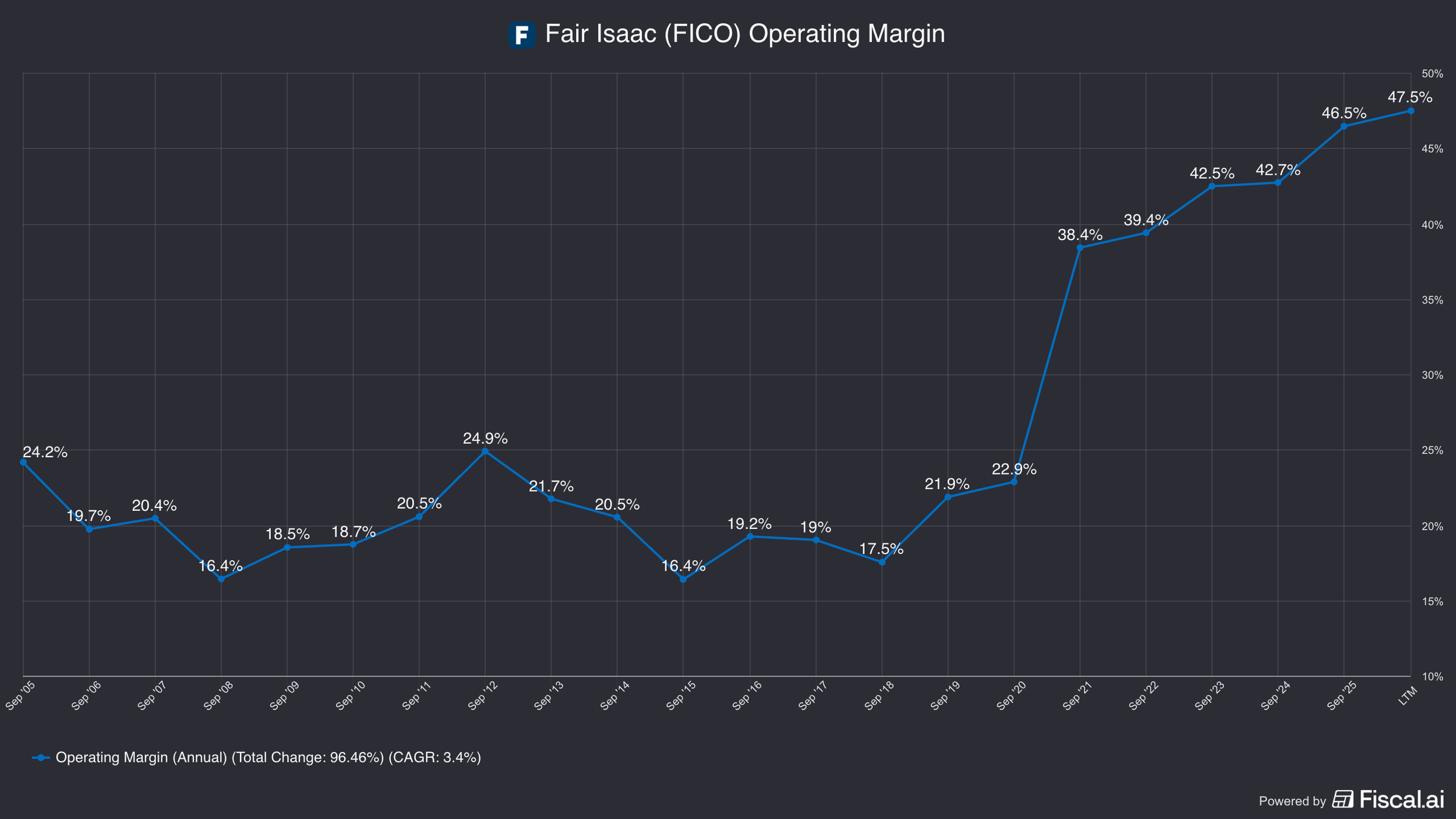

And unsurprisingly the margins of the business greatly improved.

Whereas they had a high teens margin under a decade ago…

Today they are closer to 50%.

And in the Scores part of their business, their operating margin is one of the highest I’ve ever seen at 88%.

So why is the stock down over 55% from peak?

Isn’t this supposed to be an indomitable business with insane pricing power that still has much more room to run?

Is it really selling off on AI fears alongside many other info data service companies, or is there something deeper happening here?

They have a competitor in the market for the first time ever in VantageScore.

And their partners are also their competitors now.

Plus a slew of fintechs have new models of gauging credit risk default, so isn’t the FICO score a bit antiquated?

Well… turns out no lending decisions really rely on FICO….

AND despite that narrative that FICO is aggressively raising prices, that is only in one part of their business…

In the rest they are actually very cheap.

But why? Who is their competition?

And what really are their moats anyway?

Business.

FICO has 2 reportable segments: 1) Scores and 2) Software.

Scores is 59% of revenues, but 82% of operating income (before overhead).

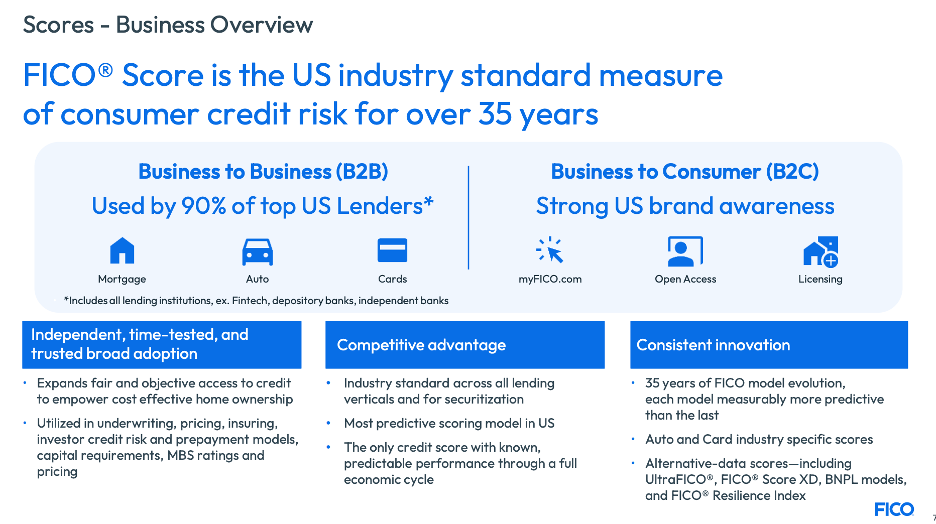

Scores is FICO’s core franchise and he standard measure of consumer risk in the U.S. It is used in most U.S. credit decisions, by nearly all major banks, credit card issuers, mortgage lenders, and auto loan originators.

A FICO score is a 3 digit score from 300 to 850, which is supposed to tell you your credit worthiness.

The FICO score is essentially an algorithm that is run on a data set.

FICO doesn’t actually hold the data, the credit bureaus do. They just sell them their model and ability to create a “FICO” score.

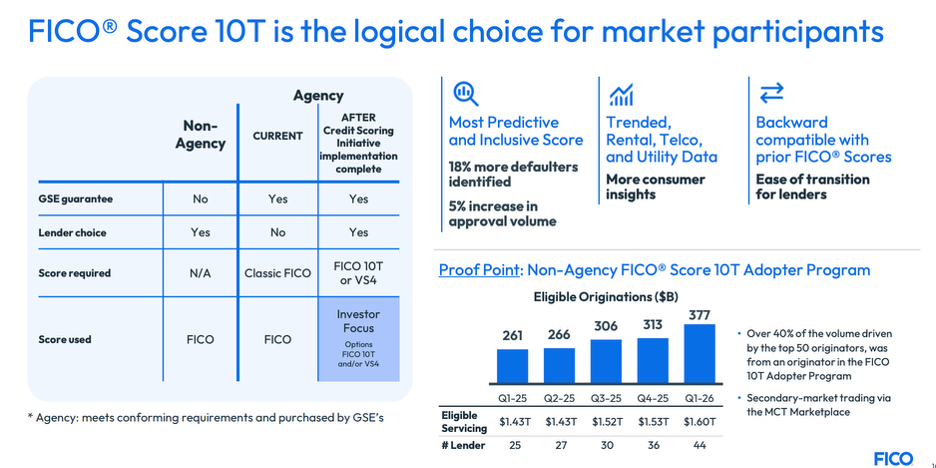

There is more than one kind of FICO score too. There are specialized ones for auto and credit cards. They also are rolling out a new FICO score called FICO 10T, that is supposed to be more predictive of defaults.

They have B2B scoring, which is 82% of revenues, and B2C which is the rest.

The B2C business is consumer checking their own FICO scores and they also have credit monitoring tools on myFICO.com that are sold through subscription. This also includes indirect royalty revenue for when a company like Experian offers FICO scores on their behalf to consumers.

The credit tools are most popular among customers when they are about to make a big purchase (a home) and want to monitor their credit to avoid any surprises during that process.

This business is only growing low to mid single digits.

B2B is the real driver of the Scores segment.

Their B2B scoring solutions are primarily distributed through major consumer reporting agencies worldwide.

· The three main credit bureaus are Equifax, Experian, and TransUnion.

The bureaus have their own data on consumers that they collect and some of it differs from bureau to bureau. FICO doesn’t exactly just sell them a score but rather a scoring methodology.

Key to understand though is that in order for it to be called a “FICO Score” it must use the FICO methodology. And most lenders want to see that FICO name in order to trust it.

The bureaus have tried their own hand at creating an alternative called “VantageScore”, which we will talk more about in competition.

Credit Reporting Companies (CRCs) / Resellers

· These are companies that take the 3 big credit bureaus reports and repackage them to sell them together, called a “Tri-Merge” Report and is primarily just for the mortgage market.

· There are many resellers including CoreLogic Credio, Factual Data, Equifax Mortgage Solution, and Meridian Link, but many others.

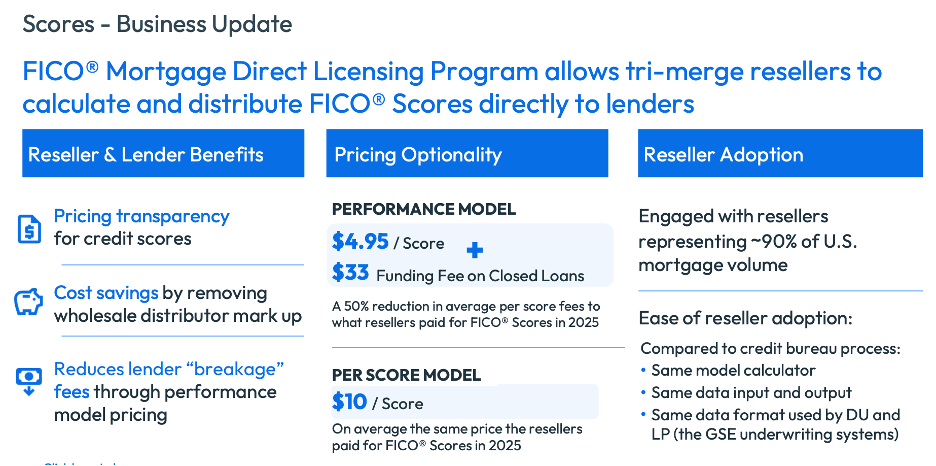

They are shifting this model to try to go direct to the resellers. Now the resellers will buy the raw unscored data from the credit bureaus and then score it themselves with the FICO algorithm.

The old model was the resellers bought the finished FICO scores from each bureau, but instead they are just buying the data now.

Under the old model the resellers had to buy three credit scores and the credit bureaus were charge $4.95 by FICO for each.

FICO raised their pricing to $10 per score, BUT offered the option to the resellers to go direct and only pay $4.95 per score plus a $33 success fee per borrower.

So if a mortgage didn’t close, the resellers only paid FICO ~$15, but if it does close they pay $15 + $33 = $48.

If a reseller doesn’t go direct, they now pay $10 x 3 for the scores, or $30. And this is charged regardless of whether the mortgage closes.

Only about 65-75% of mortgages close (called a pull through rate).

So if say 25% of mortgages don’t close, then out of 4 mortgages under the old model (with the new $10 price) the reseller is paying $120 to the credit bureaus versus $148 under the new model…

So why is this better?

It is because the fees are charged directly to the borrower, so the reseller is only actually paying ($15 for the lost mortgage that didn’t close instead of $30). The total cost is higher to the borrower, but the reseller is paying less, so they like it.

It is important to note that the closing cost of a loan may be $5,000 plus so stacking a $38 fee ($5 + $33 success fee) on that isn’t that impactful (or $76 if there are two borrowers jointly applying).

The credit report itself usually cost around $80 -120 (per borrower, so twice that if a married couple is applying)

We will talk more about the credit bureaus response later.

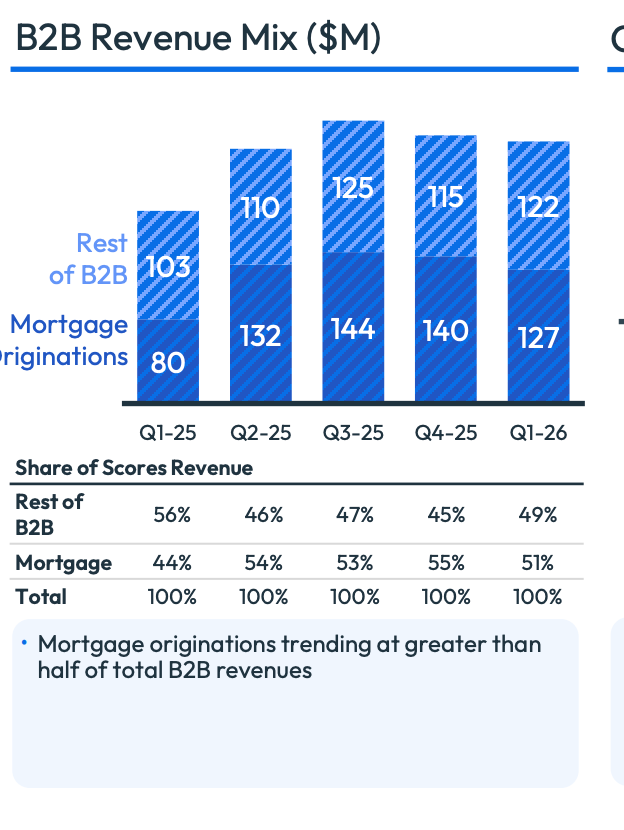

But this has been a big driver of their business. Mortgage as % of B2B revenue were just 24% in 4Q23 (which is after it was up 147% in the quarter from the price change).

Today it is 51%.

This is despite the mortgage market falling off from a peak of 13.6 million loans in 2021 to 4.6 million loans in 2023 and about ~6.5- 7 million for 2025. (2019 was 7.5 to 8 million).

These B2B revenues are the majority of the scoring business too, at around 82% of the total Scores segment. The rest of the B2B segment includes credit cards, auto loans, and personal loans.

These are much different (and worse) markets.

The reason why the mortgage market is so strong for FICO is because it used to be mandated by the FHFA that the underwriter use FICO models if they were to repurchase the mortgages (Fannie Mae and Freddie back are the two big government sponsored entities that buy a lot of mortgages and then resell them to make homes more affordable).

This forced the whole secondary mortgage market (this is the market that sells and buys mortgages) onto FICO standards.

Now the FHFA no longer requires FICO (they have also approved VantageScore), but most of the Mortgage Backed Securities Market (MBS) has decades of FICO models and data and so there is a lot of inertia to switch.

Mortgages without FICO scores may get lower prices, which incentives underwriters to stick to FICO since the few bucks saved could be thousands when resold. (Private Mortgage Insurers also have all of their models on FICO so that is another point of inertia to switching)

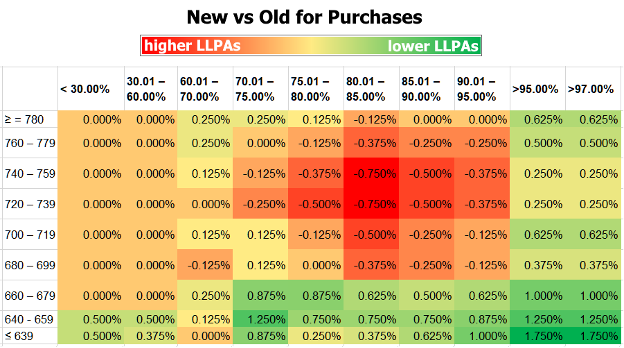

There is something called the LLPA or Loan -Level-Price-Adjustment that maps FICO scores and LTVs to help price mortgages.

This protects the FICO franchise in mortgage.

The other B2B markets never had this centralized authority that pushed a FICO standard in the same.

Credit Cards.

Credit card companies typically keep the loans on their balance sheet, so the secondary market is not a factor here.

The bigger difference is that banks send out millions of preapprovals for credit cards before the customer signs up. FICO charges just a fraction of a penny for pre-approval scores and then $0.10-$.20 for a “hard pull”.

In the pre-screen process the bank will ask a credit bureau like Experian to give them alist of 5 million customers with FICOs over 720.

Experian then runs the FICO model on their data set and sells it to a credit card company like Capital One.

Capital One then mails out the fliers of pre-approved credit cards. Then they will run a second hard pull if the customer actually fills out the application).

When they do this it temporarily dings the customers credit because it is a signal to the market that they are taking on more debt.

Because of federal privacy laws, Capital One doesn’t get that much data until they do the hard pull, even though the FICO score is the same (baring that 30-60 days could pass where it changes). On the hard pull they get the full credit card report and FICO score. (This is where FICO charges 10 to 20 cents.

For a credit card company, they have their own risk models for deciding who to give credit to and what the limit should be. The FICO score is just one part of it…

And surprisingly not even an important aspect of who they give credit too.

So why do credit card companies use them at all?

There is an aspect that it can “sanity check” a credit card issuers model, but the other big aspect is regulatory.

The CFPB (Consumer Financial Protection Bureau) and the OCC (Office of the Comptroller of the Currency) heavily scrutinize banks for discriminatory lending practices.

FICO has spent decades testing their models to comply with the Equal Credit Opportunity Act. So if a bank denies a customer credit and the FICO score is bad, they have a legal defense that it wasn’t out of discriminatory practice.

There is some credit card securitization as well that would want to see a FICO score, but this market is much less rigid and small than the MBS market so it’s not a big factor.

However, at a cheap enough price (10-20 cents a pull) it makes sense to keep them.

In this market they are so cheap that it isn’t worth bothering trying to replace them…

But they could be if they aggressively hiked prices…

But that’s also why they haven’t.

Auto Market.

The Auto market is also a worse market for them.

When issuing a car loan, the most important factor isn’t the FICO score, but the LTV, or loan to value ratio.

A borrower with a mediocre 650 FICO score who puts 20% down can be a safer borrower than a 720 FICO who puts 0% down.

What is key here is the value of the vehicle and how quickly it depreciates. That is because if a borrower defaults, they can repossess the car and resell it, recovering much of their loan.

When a customer is interested in buying a car, the dealer will “shotgun” the application to maybe 5-10 different financial institutions. The FICO score here is used to decide which financial institutions could be interested in the loan. So, it acts as a sort of “sorter” because some institutions specialize in sub-prime loans and others won’t touch it.

The 5-10 different financial institutions then do their own hard pull on the consumer and ingest the FICO score alongside their own proprietary models and make a loan offer.

The consumer they will take the best offer (lowest interest rate usually).

In this order of events, FICO is charging $0.15 -$.25 for each pull. So with 10 applications, plus the dealers pull, they may make $1.65 - $2.75.

The banks and auto lending institutions (including many manufactures that have their own captive finance arms) have their own proprietary data and models to decide the risk and default levels of the borrower.

Similar to credit card lending, the FICO score acts as legal protection from the CFPB and OCC in case a borrower is denied a loan.

It also is a helpful sorting function so dealers know where to send the loan inquiry too.

The secondary market here is more important because the ABS (Auto Backed Securities) market is bigger, and investors like to see weighted FICO scores.

However, it is nowhere near as big as the MBS secondary market is and many car manufacture’s captive financial subsidiaries as well as other financial institutions hold the loans on their balance sheet.

The ABS market is still important though, as FICO here is really competing against “trapped capital”.

Ford for instance could ditch FICO and still sell their auto loans and get the ABS rated by Moody’s and S&P Global, they may just require a “credit enhancement”.

In this case that means Ford will add maybe $5 million more in auto loans to a pool of $100 million to get the number up to $105 million.

This structurally protects the investors at the higher ends of the ABS (this is because there is more loans that would need to default before they would miss a payment).

Ford though would rather not trap that extra $5 million in loans (which remember for them are assets), so instead they pay FICO so they can get away with just the $100 million as collateral in that ABS structure.

If you are wondering why this doesn’t work in the mortgage market, it is because mortgage investors aren’t worried about default risk…

At least for the ~70% of mortgages that are called “agency” mortgages because they are backed by Fannie Mae or Freddie Mac. These agencies guarantee to pay back any losses on default (they have their own protection in the form of the borrower’s down payment and private mortgage insurance if it is under 20%).

These Agency Mortgages are actually purchased on TBA, or to be announced basis, which means the buyer doesn’t even look at the mortgages before they purchase them…

Or care what’s in them because they are backed by the agencies.

So, for these loans over-collateralization isn’t employed so it isn’t needed to protect against credit risk.

So then why does a mortgage buyer care about FICO scores at all?

It is because the risk they are more focused on is prepayment risk.

This is the risk that a buyer will pay down a mortgage early if interest rates drop (i.e. refinance the mortgage and pay it off).

This is bad for an investor who bought maybe $50 million of Fannie Mae 30-years at a 6% coupon because in a lower interest rate environment they suddenly get handed back their money and have to reinvest it at a lower interest rate.

To understand this prepayment risk, they have models that use FICO data (or WAFICO, which is weighted average FICO for tranche of MBS) that goes back 30+ years in different interest rate environments across different borrower credit scores.

In the non-agency MBS market still needs FICO to model the prepayment risk (even if they do use overcolletarization for credit enhancements).

The auto loan market does have prepayment risk, but borrowers don’t typically refinance their cars when interest rates drop. (A 2% drop in interest rates on a $20k outstanding loan is only $33 a month, which isn’t worth the paperwork hassle for most people).

Instead, the prepayment risk comes from consumers selling their cars and buying new ones or getting into car accidents… which FICO has no predictive ability over.

Personal Loans.

The last market we will talk about is the personal loan market.

This is perhaps the worst quality market for them because a FICO score is inferior for underwriting here and there are a lot of new fintech that utilize different proprietary models to underwrite credit risk from SoFi, Upstart, Prosper, LendingClub.

FICO is primarily used here as a top of funnel marketing engine to see where to direct offers too.

A fintech is sort of legally prevented from using their own models (which are superior here).

This is because of the Fair Credit Reporting Act prevents allowing Experian or another credit bureau to turn over raw data on million of Americans. They can only get that data after a consumer applies for a loan.

So they are stuck asking for just FICO scores (or VantageScores) that come with names and emails.

FICO gets fractions of a cent for each time their model is used in this vetting.

Once the consumer applies the fintech uses their own algorithm, FICO is not the decision engine.

It can also serve the same safe harbor function though as with credit cards.

It is worth emphasizing that a FICO score is almost never sufficient on its own to approve a loan. Instead it is more of a veto engine and a pricing engine.

Even more incredibly, a FICO score is LEGALLY NOT SUFFICEINT to approve most loans.

(The one exception is with micro credit decisions like a retailer offering a credit card at check out and the lender is allowed to rely on the consumer’s “stated income”… i.e. whatever the consumer says their income is).

Under the CFPB’s “ability to repay” law, a lender must include debt-to-income and loan-to-value metrics to issue a loan. FICO scores do not take into account income.

They also don’t know employment status or how any idea of much money someone has.

But that also isn’t really the function of the FICO score.

Instead it is meant to be a crude metric that can quickly do very high level screening.

Then it is also used in pricing decision, especially in mortgage, and safe harbor.

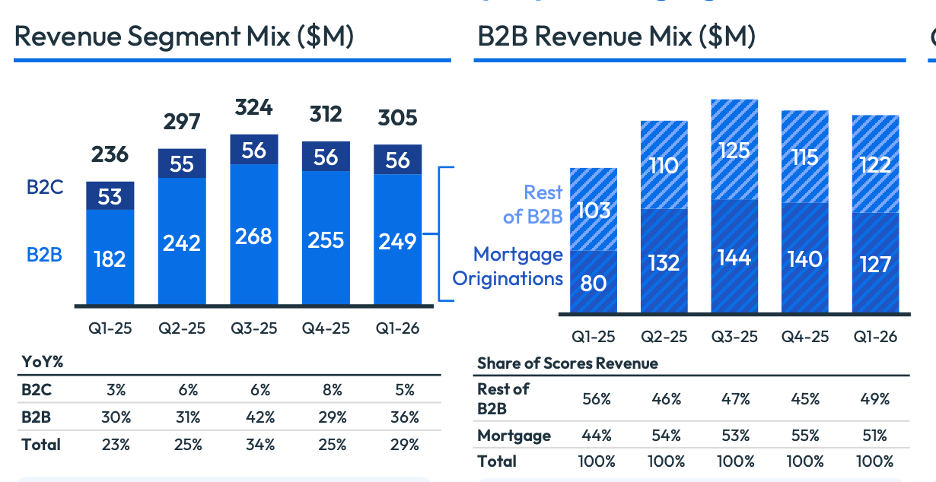

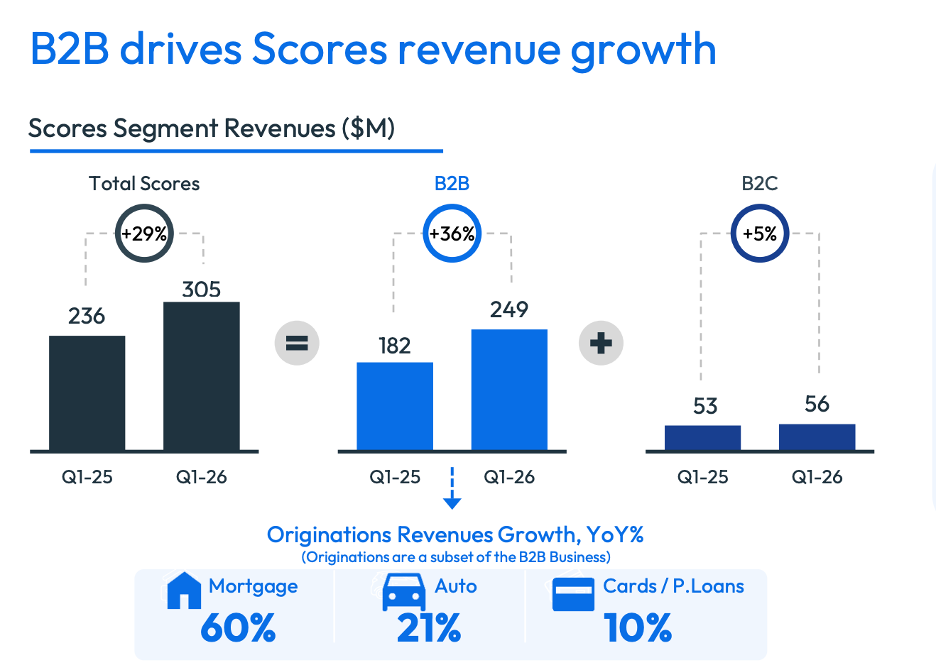

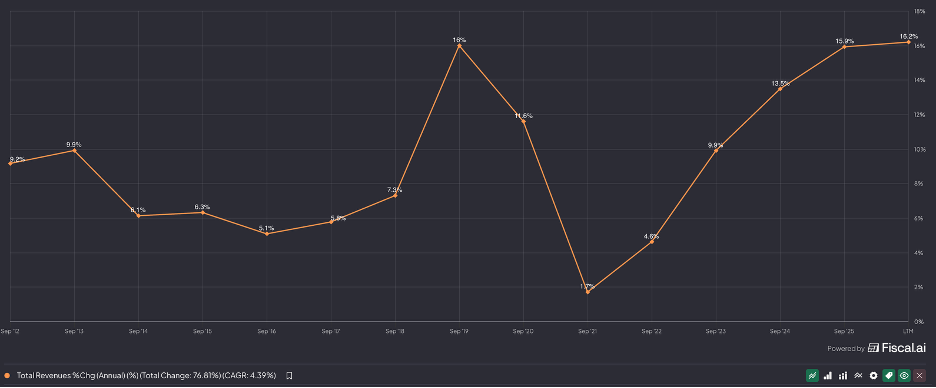

Scores revenue is $1.2 billion, +28% y/y.

Their operating income in this segment is $1.1bn, up 29% y/y.

This growth has primarily been driving by the price hikes in the mortgage business. Their direct efforts are still in early innings and if resellers start to offer that service, we could see more growth here as they earn that $33 success fee.

With this overview of the Scores business, let’s move into Software.

Software.

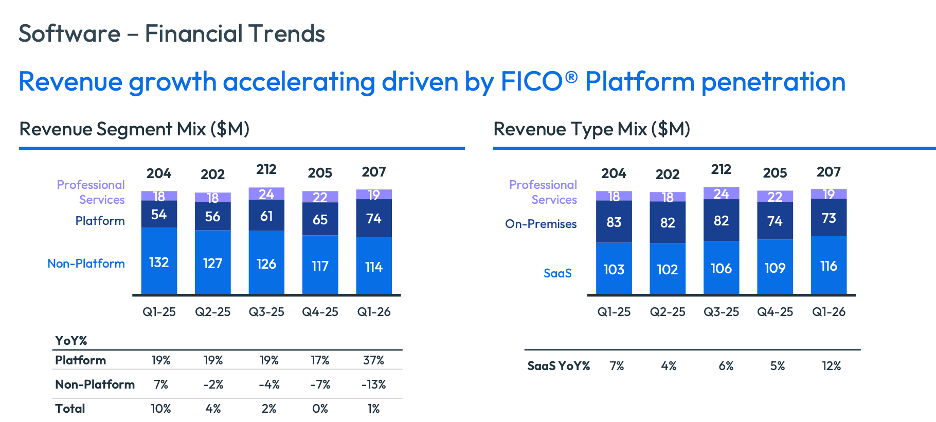

The software business has $825 million in revenues but is growing low single digit.

There are 3 parts to this segment: Professional Services, Platform, and Non-Platform.

Professional Services is when FICO sends their people to help set up and install the software on behalf of the customer. That could also include creating custom analytics and decision models.

Platform is there new unified software platform they are trying to transition all of their customers on to, whereas the non-platform is the legacy point solution software products they sold that don’t integrate easily together.

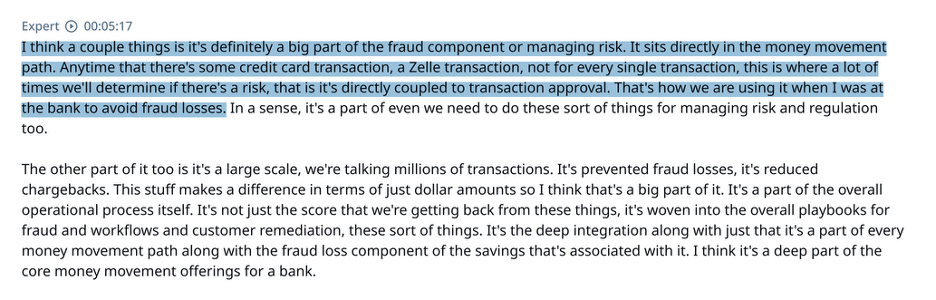

One of their marquee products is Falcon Fraud Manager, which is the global standard for credit card fraud detection.

Here is what a Bank executive had to say about it (courtesy of AlphaSense Expert calls).

For nearly 2/3rds of all payment cards globally (and virtually all cards in the U.S.), when you swipe your card and there is that few second delay, it is being run through Falcon’s fraud models to estimate the probability that the transaction is fraudulent before the issuer decides whether to approve it.

However, most credit card companies and banks also have their own models they will layer on top, so the two work together.

From their 10-k

Triad is another big product for account management and Portfolio Management.

This is a system that monitors a customers existing accounts and can decide to increase credit limits for example, or it may preemptively slash your credit limit if it sees worrisome activity elsewhere.

Xpress Optimization is a mathematical model to help solve complex logistical and algebraic problems like telling an airline how to reroute planes to save fuel in the midst of a blizzard.

Origination Manager, as the name suggests, manages the whole origination process of a credit card application or loan for financial institutions.

FICO Blaze Advisor is a custom built decision engine for financial institutions to approve or decline different loans.

They have many other products too that cover everything from collections and customer marketing to insurance claims, compliance, and broader enterprise decision automation.

Historically, they sold this as stand alone products, but are now all available on the FICO platform.

The idea is that even if a bank switches to just using Falcon and Triad on the platform, cross-selling other products down the line becomes much easier because it is as simple as turning an application on, instead of requiring all of the installation work under the legacy ecosystem.

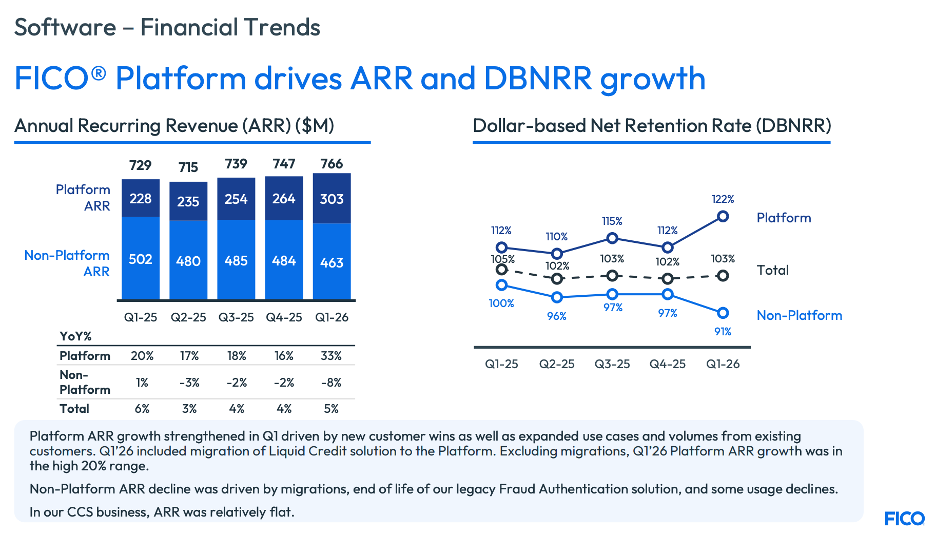

You can see that their Platform revenue is growing 33% y/y, whereas their non-platform revenue is contracting—this is the result of that shift.

They also show that dollar net retention rates on the platform reached 122% last quarter.

This means existing customers are spending more on the platform.

They have pretty bespoke pricing and will charge a base fee, plus various usage fees. Every time a credit card transaction is approved or decline it costs a fraction of a penny for instance. There are different other fees in each product group.

This business is generating $236 million of EBIT on $825 million of revenue for an operating margin of 28%.

It is a more competitive business, as we will talk about in the next section.

Competition.

FICO’s competition varies a lot depending on what market we are talking about.

In scores they have a competitor in VantageScore, who only recenty has been allowed to b be considered in Fannie Mae and Freddie Mac loans (before FICO was mandated).

VantageScore is a JV created by the credit bureaus to try to displace, or at least weaken, FICO’s grip on scores.

Their aim is really to weaken FICO’s competitive position, so they have less pricing power.

So far, it hasn’t worked well.

FICO is still a relatively small portion of the overall credit report that the resellers buy from the Credit Bureaus.

A report might by $80-120 and a FICO score is $10, or $5 with the $33 success fee which can be passed off the customer.

The resellers don’t really have a vested interest in switching, even though they are aggressively pricing it, including making it free for some period of time.

For the reasons listed above (secondary markets, longer history on pricing FICO prepayment risk, embedded in workflows) it is very hard to get the market to switch.

For the scores business in auto, they are really competing against the cost of over-collateralizing the ABS.

If having a FICO score can mean less capital needs to go into the structure, it makes more sense to just keep it then lose that cost of capital. (See earlier discussion in the business segment)

FICO has a better position here in Auto.

In credit card or personal lending, FICO isn’t really used to make credit origination decisions, but it is a good sanity check and covers them with safe harbor for applicants that are rejected.

VantageScore is trying to compete on price and in some cases it is winning.

On top of funnel marketing, some have already switched to VantageScore because the consequences are less and they really just need a list to market to.

On the hard pull, FICO still is what is used and doesn’t seem as threatened by the price competition.

Synchrony Financial (one of the largest credit card issuers) seems to be an exception though and they have started using VantageScores. They issue primarily private label credit cards for retailers that have low limits, but it still should be worrisome for FICO.

Since many card companies have their own models, they may be okay switching because VantageScores offer the safe harbor they need and can be a good enough second sanity check.

Consumer apps like Intuit’s CreditKarma and other financial institutions show VantageScore to consumer because it is cheaper.

The summary in short, is that they have the strongest moat in mortgage by far, followed by Auto. In credit card their moat seems to be eroding a bit and in personal lending it is as well for similar reasons in card.

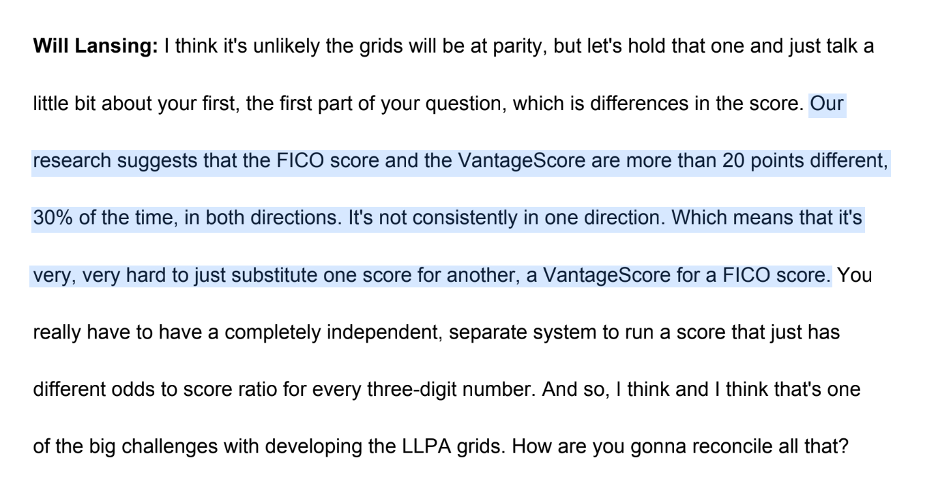

FICO CEO Will Lansing though notes that it is not an apple-to-apples comparison where the VantageScore is more than 20 points off in either direction 30% of the time.

This will prevent uptake in any area where looking across a long data series will be key to adoption (i.e. with mortgage and auto).

Since this isn’t a factor in credit card or personal loan, they don’t have a strong postion there.

Over a long enough time frame though, VantageScore could eventually have that data series, but it won’t be that meaningful unless they can get their usage up.

If you are a Wall Street analysis analyzing prepayment risk, you want the biggest data set that includes the most borrowers across the longest time period.

VantageScore doesn’t automatically just generate that data by “being around”, they need actual usage.

Right now Experian and Equifax are giving away VantageScores free alongside the FICO scores. The hope is that even if the VantageScore is ignored for now, in time this could build the data series that threatens FICO’s long history of know prepayment risk.

For now, they have only committed to giving it away for free for a year or so, but it doesn’t cost them anything really to run the model again on their algorithm and then attach that score to the report too.

In theory, they could it for a decade, which is what it may require to start to convince the secondary mortgage market to take it seriously.

However, even than FICO’s will be longer and have more data across for credit events. For the secondary market, it seems they will still want to see FICO a long time to come.

BUT, at FICO’s current valuation multiple of 42x trailing earnings, a lot of future growth and business longevity is already priced in (more on this in the next section).

FICO also is rolling out other scores that take into account alternative data and are meant to be more predictive.

They are also reconfiguring their marque FICO score with FICO 10T.

This takes into account trends of credit repayment and they claim it improves predictability by 17%.

Their software business is more competitive, which is reflective of their lower margins.

Unlike Scores, where FICO has something much closer to a standard, software is a real fight.

They compete against legacy vendors like SAS and Pegasystems, Experian’s PowerCurve offering, NICE Actimize, newer fraud players like Feedzai, Featurespace, BioCatch, and ThreatMetrix, and for the biggest banks they are even competing against the bank’s own internal engineering team.

The in-house competition is perhaps the most brutal because a lot of financial institutions consider these to be core to their business.

For a JPMorgan or Bank of America, FICO is not always competing against another software vendor, but against a build-vs-buy decision.

The mega-banks can afford to build their own decision engines and fraud tools, which makes them the hardest customers to fully lock in.

This is part of why FICO’s software moat is weaker than its Scores moat.

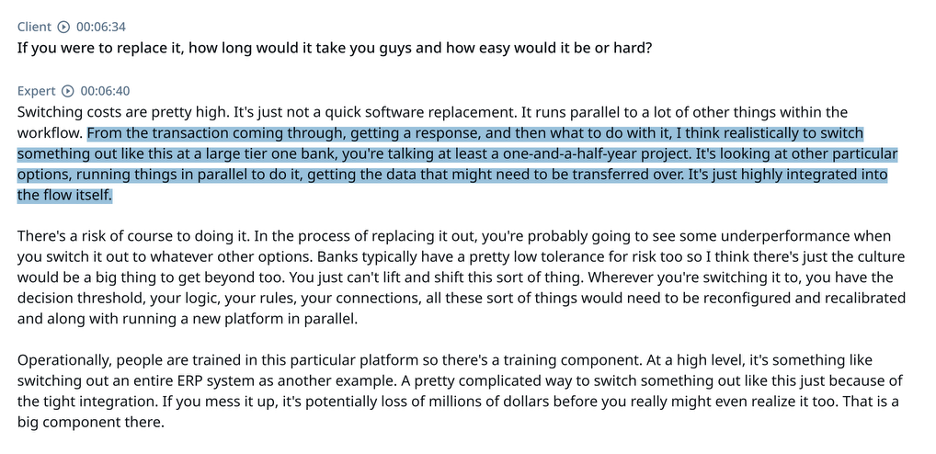

The real defense is not monopoly power, but switching costs.

Historically, FICO sold more point solutions like Falcon for fraud, TRIAD for account management, and Blaze Advisor for decisioning.

The risk there is obvious: if a competitor builds a better fraud product, a bank can rip out Falcon without replacing everything else.

That is why management is pushing customers onto the broader FICO Platform.

The goal is to make FICO the central decisioning layer across fraud, originations, marketing, and account management.

Once a bank is running its workflows through one shared platform, replacing FICO becomes far more painful.

So while software is clearly the more competitive part of the business today, the platform strategy is meant to make it much stickier over time.

Having said that, Falcon Fraud is a global standard and unlike to be replaced anytime soon…

Same goes for many of their other products.

Banks do not typically replace existing solutions and are very slow to make meaningful changes.

Their aggressive pricing practices in mortgage scores are also absent in this segment, so that isn’t as much of a consideration here.

AI does seem to be particularly powerful for analyzing data and default risk so new players could come up.

FICO of course isn’t standing still here.

They have the FICO Foundation Model for Financial Services (FFM) which is designed to be less compute intensive, eliminate hallucinations, and is trained on domain-specific financial data. It also provides audit trails.

This is all now a new part of the FICO platform.

While no doubt FICO is a very high quality business, an investor has to wonder if they will be a better or worse business in 10 years from now.

It is hard to think the entrance of competition into the Scores business is going away.

Even if they can weather it for years to come, is it impossible to think that VantageScores could gain a broader grip in a decade? Or even if not, will FICO really feel they have the same pricing power in the future?

All of these questions should be considered in the context of the valuation.

Valuation.

At a stock price today of $1,060, they have a market cap of $25.2 billion or enterprise value of $27.8 billion.

The stock is down from a peak of $2,375 in 2024.

Despite the 55% drawdown, they trade at 42x trailing earnings.

On their next year earnings guidance, they trade at 32x earnings.

Still an investor would need to see more growth beyond that.

They are still in early innings of reaping the benefits from their last pricing hike and the direct FICO score program.

Very few resellers are currently in the direct program and it hasn’t meaningfully hit results (the $10 price hike did, but not the $33 success fee with the lower $5 score price).

With even moderate success this could be a meaningful uplift to earnings, but it is hard to model exactly how much over a multi-year period.

It is worth keeping in mind that revenue growth has only more recently been this strong (mid-teens) on the price hikes.

Operating profits have grown, much more though, as most of that revenue growth has been in the very high margin Scores segment.

CFO Steve Weber is “really bullish on longer-term margins”.

If they could grow revenues say 10-15% for 4 years beyond 2026 and grow margins from 48% to 50-60%, that would be an earnings range of $1.4 billion to $2 billion.

If an investor was still confident in their moat at the time and they were still growing double digits, a 30x multiple could be fair for a market cap of $42 - $60 billion (for annualize return of 11- 19%)

If their moat was still strong, but they were growing slower in the high single digits, then a 20-25x multiple could be a proper valuation (for an annualize return of 2% at the low end using the $1.4 billion at a 20x multiple or 15% using the $2 billion and 25x).

In a more draconian scenario, where their moat looks to be eroding and VantageScore is starting to gain some ground in mortgage, showcasing terminal value concerns, an investor might place a 15x multiple on that earnings stream (for a -3% annualized return to a 4% return).

It is worth mentioning though that all of these scenarios still assume revenue growth and margin expansion, which is not a forgone conclusion.

There are also other risks, like the Tri-Merge Credit Report, turns into a Bi-Merge report, only requiring 2 credit bureau scores and not 3, cutting FICO usage down significantly.

Also the risk of regulatory or justice department action remains an ever-present risk (the 2020 justice department case against them was closed without any actions though).

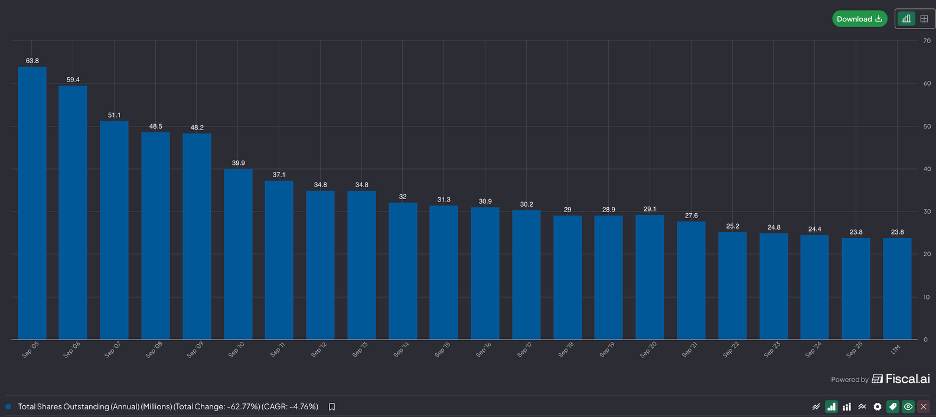

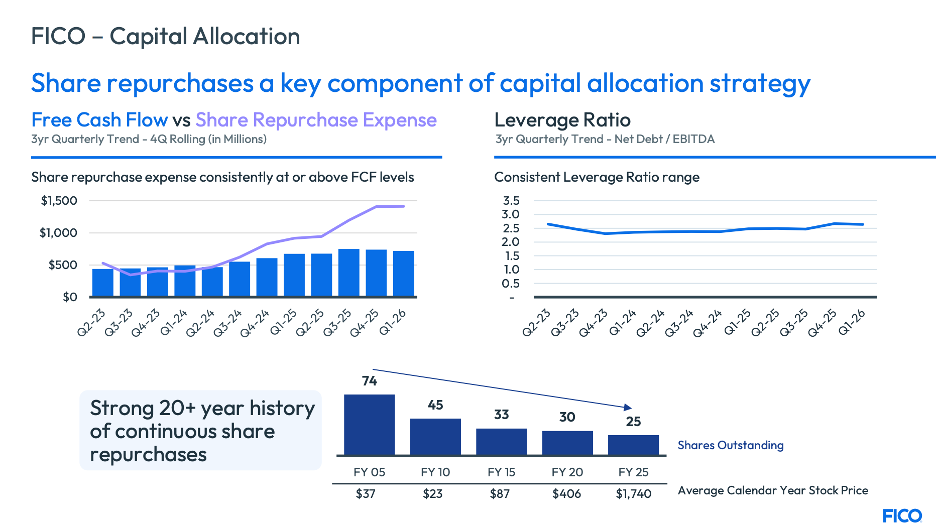

In terms of capital allocation though, they have been really good at avoiding large M&A that distracts from the core business and often results in write-offs.

Instead, almost all capital has been diverted to stock buybacks.

They have reduced their share count by 63% since 2006.

And plan to direct most excess cash to repurchases.

CEO William Lansing has been leading FICO since 2012 and currently holds about 1.5% of the company’s stock.

A position worth $400 million.

Investors should gain some comfort knowing that the key insider has a lot of skin in the game.

But executives could also be wrong.

While there may be no real way to kill FICO quickly, or even over a longer period of time…

Some investors may see the moats eroding and be unsure of whether or not competition will eventually weigh on growth and margins.

Any signs of this could trigger a further re-rated.

On the other hand, at a valuation less than half of what it was just a couple years ago, a lot of this could already be priced in.

An investor only needs to assume FICO stays a great business (and not a phenomenal one) in order to make a return.

Ultimately, it is up to you to decide what you are comfortable assuming.

For more on FICO check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.