Palantir Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

There aren’t that many cult stocks.

And Palantir is no doubt one.

There are whole YouTube channels and newsletter devoted just to Palantir stock.

For a lot of investors, that level of almost religious fervor instantly turns them off…

And the shear amount of buzzwords you need to learn to understand Palantir makes it easy to think how many Palantir investors actually know the business instead of being drawn into a momentum trade.

However, you don’t have to look to hard to see that Palantir is actually a phenomenal business.

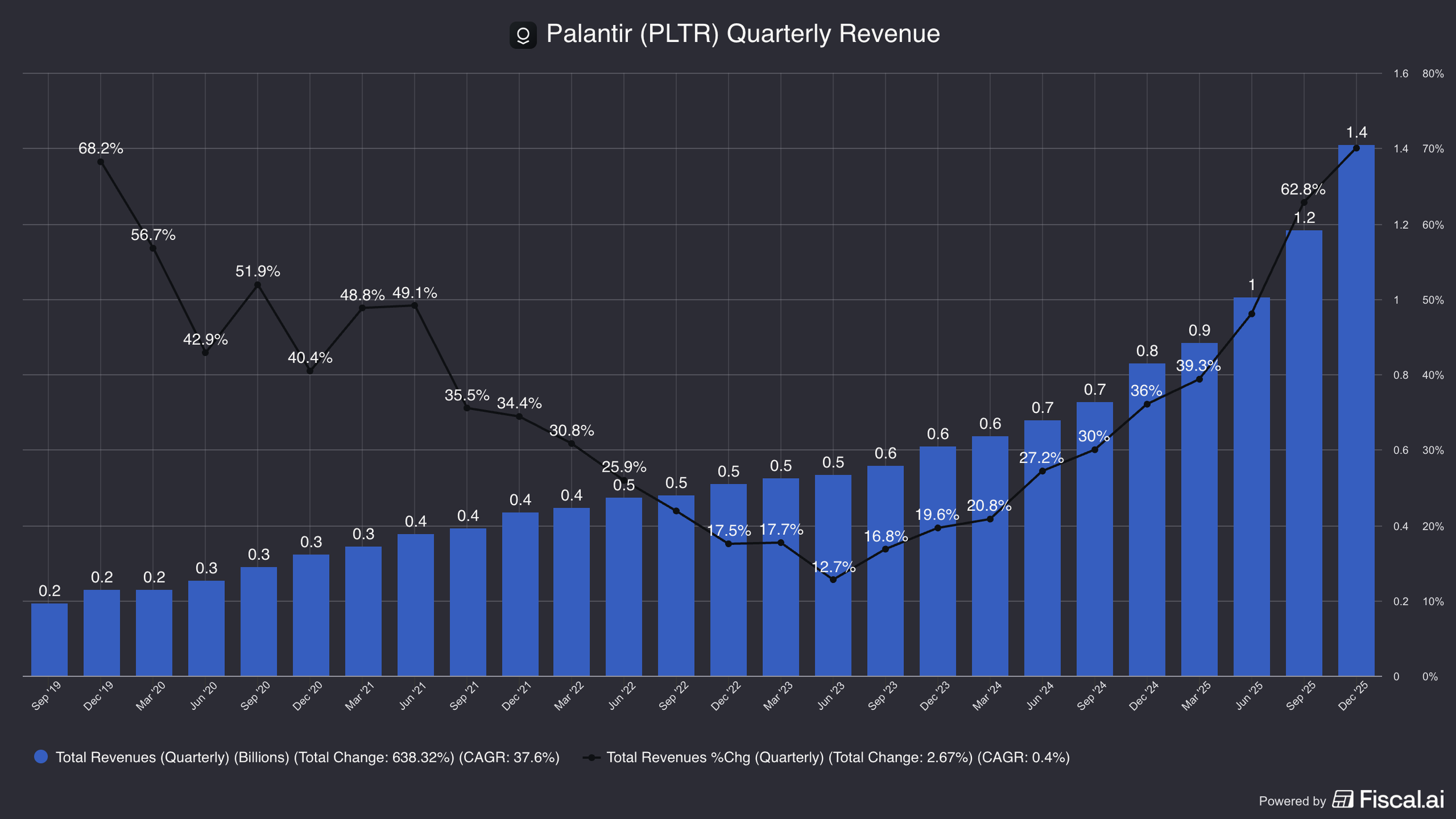

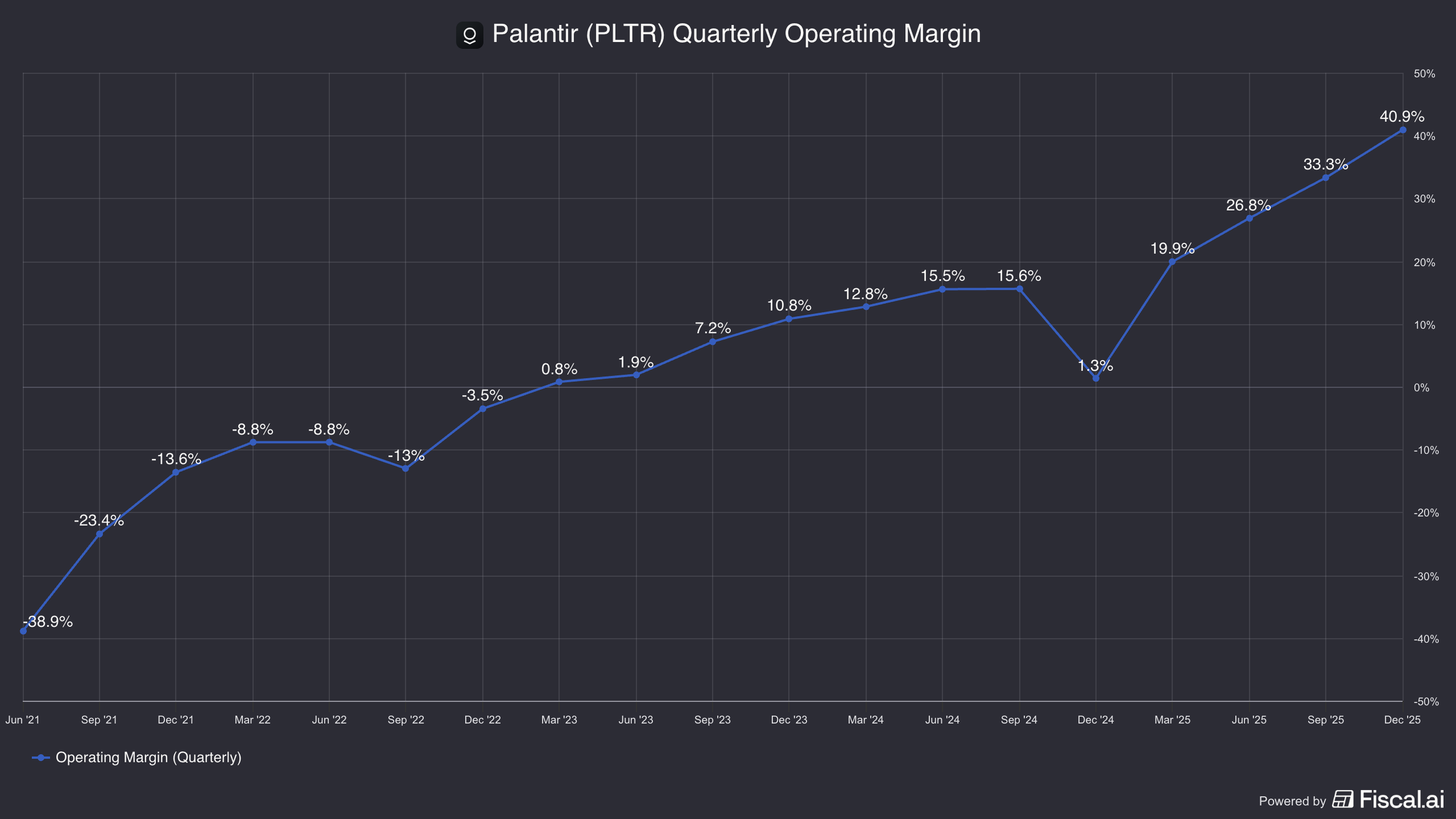

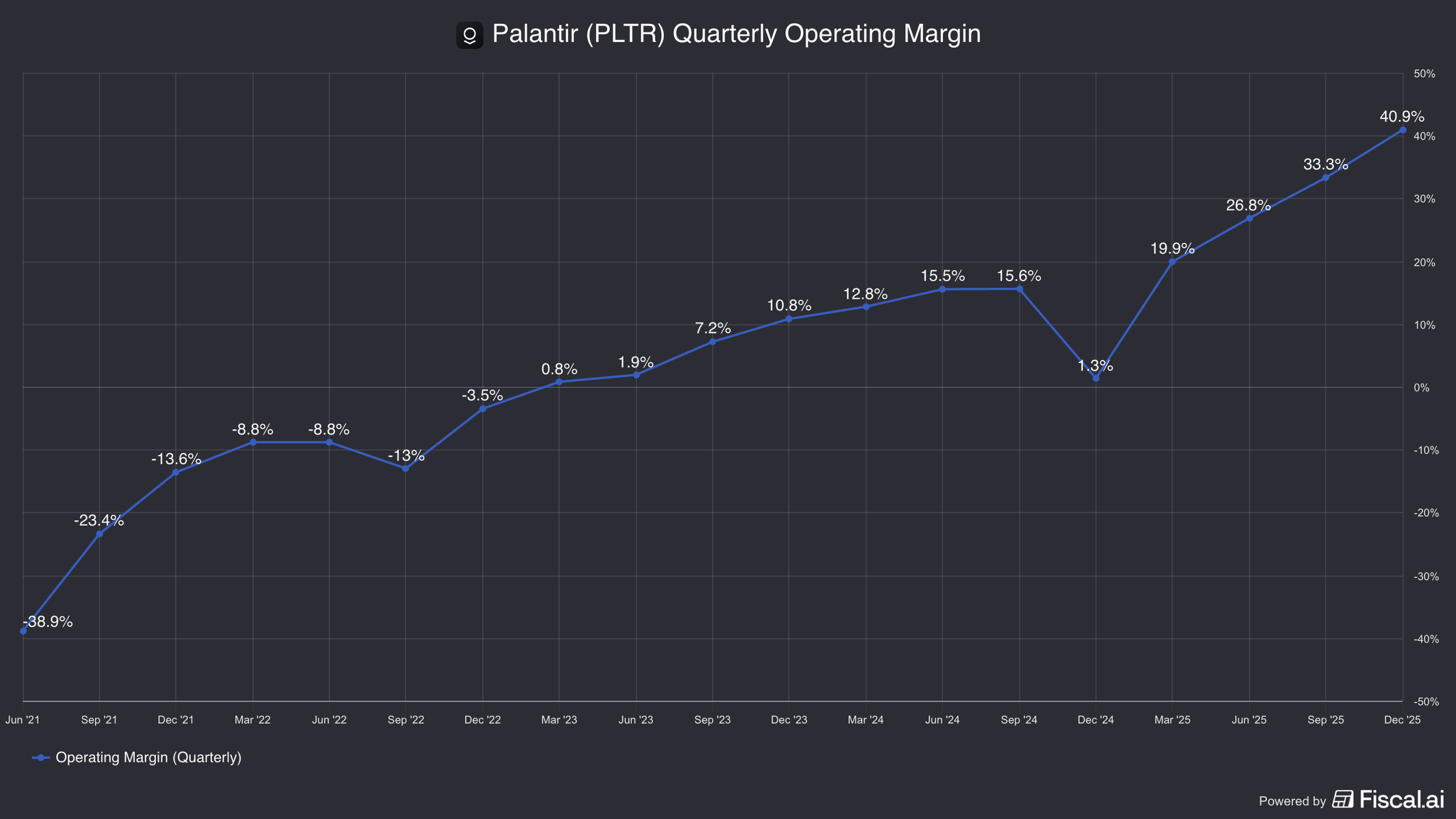

Revenues grew 56% last year with operating margins of 31%.

And in the last quarter alone revenue growth reaccelerated to 70%...

While margins actually expanded to 41%.

These aren’t funky non-GAAP adjusted margins, but actual GAAP margins after stock-based comp.

And they have a clean balance sheet with over $7 billion in cash.

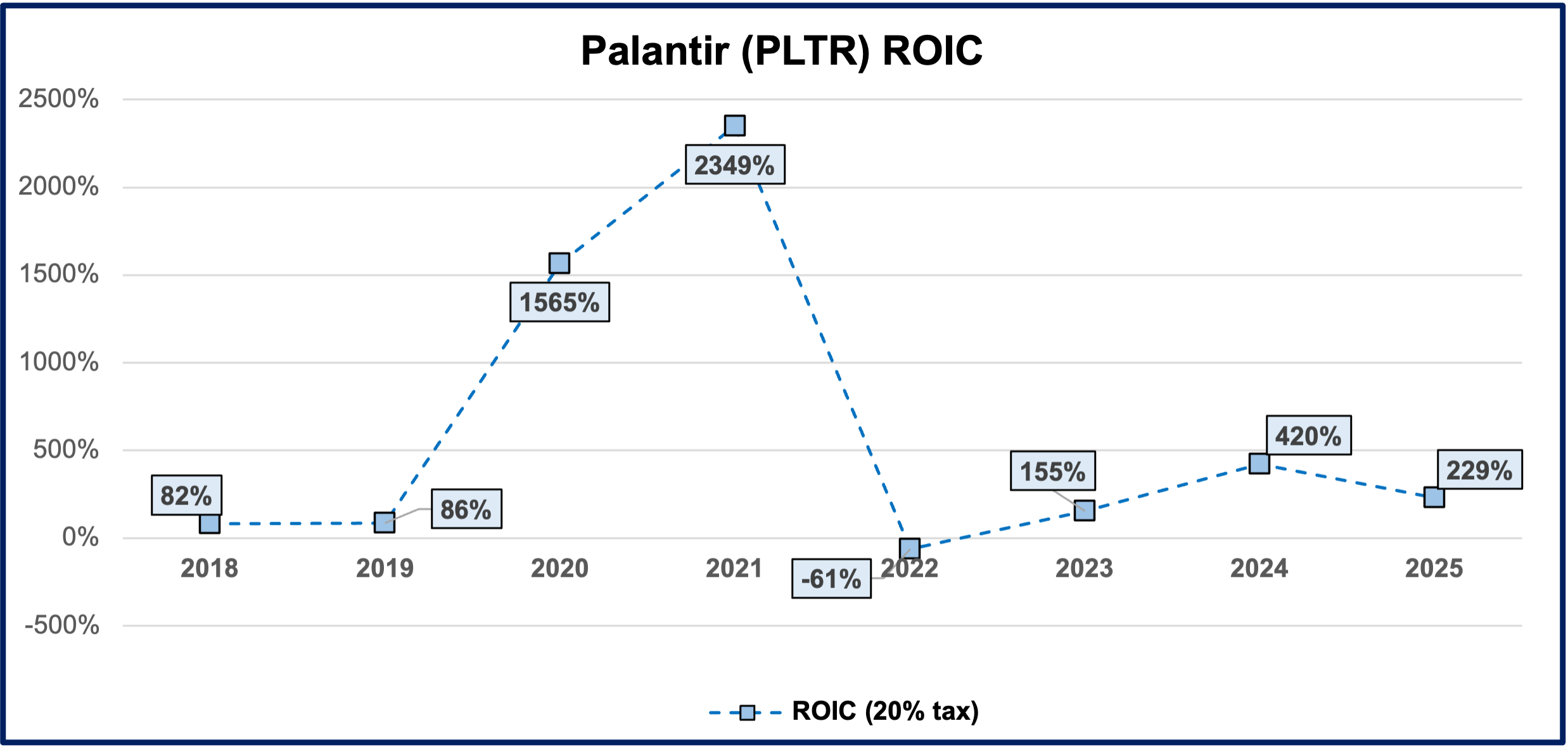

Their ROIC (return on invested capital) is an insane 230%.

Free cash flow conversion is 87%.

This is not some lightweight software tool riding a temporary AI wave.

Palantir built its products in some of the hardest environments imaginable—defense, intelligence, and mission critical government work—where software has to ingest messy data, preserve strict permissions, and actually help people make real world decisions…

Often life or death ones… but more often death…

Which is not a hyperbole.

Founder Alex Karp is a unabashed in their role in helping the U.S Military make lethal decisions on the battlefield.

The government was a hard customer to win. They had to literally sue to get considered for contracts.

And now they are taking that same platform to enterprises, so they can actually get the most out of AI.

But this isn’t anything the market hasn’t already figured out, with them trading at 80x…

Not 80x earnings… but REVENUES

With a $355 billion market cap, Palantir might be one of the most expensive large cap stocks in public market today… and by a good margin.

They have a 230x P/E ratio…

Which would require many years of very high growth in order to rationalize.

So how does an investor make a return at current price levels?

And what does the business actually do?

Could they be a threat to incumbent enterprise software providers like Salesforce and ServiceNow?

We cover all of this and more in this week’s Five Minute Money!

Business.

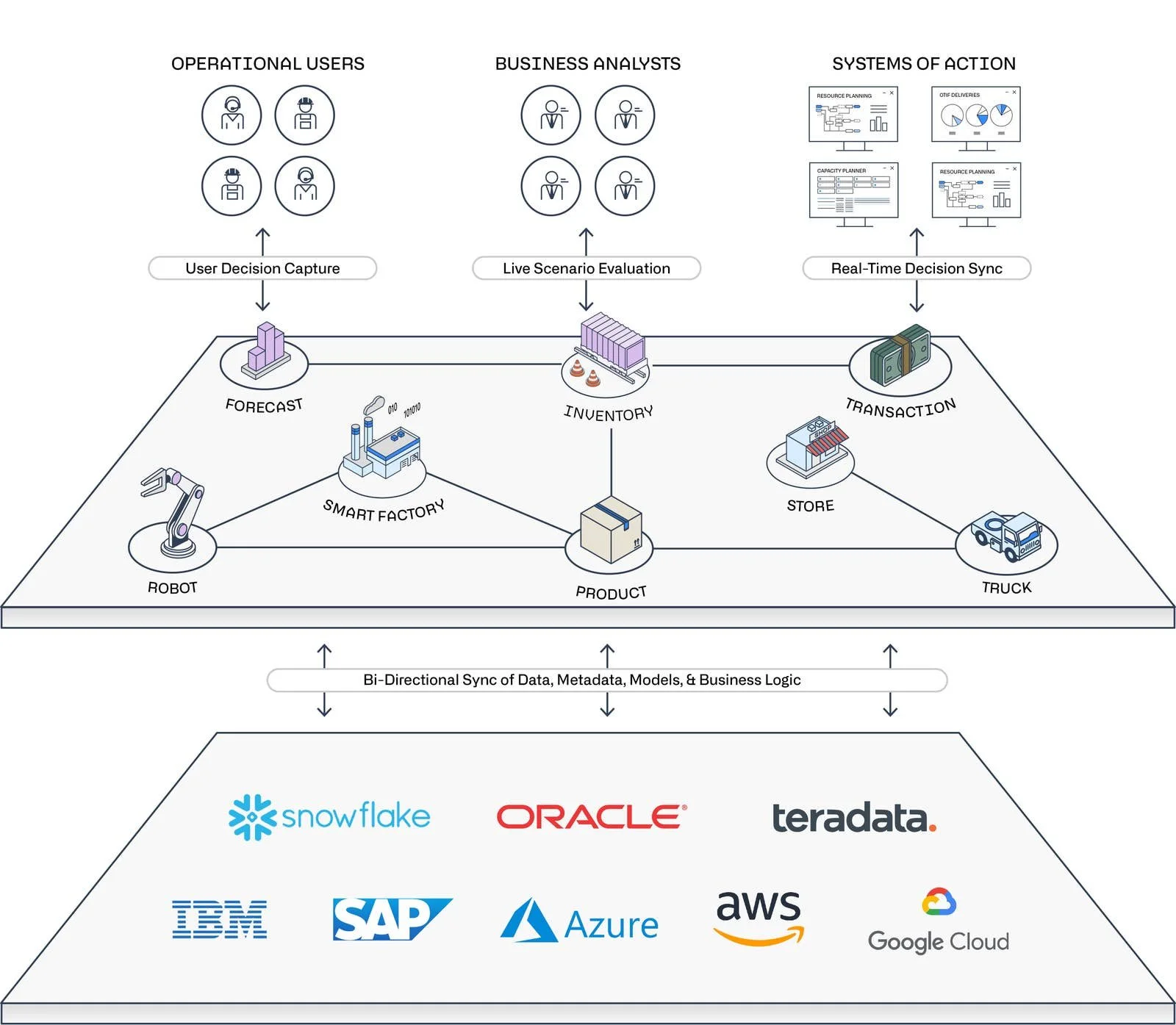

Before we get into their 4 Core Software Platforms, we need to learn a little vocab.

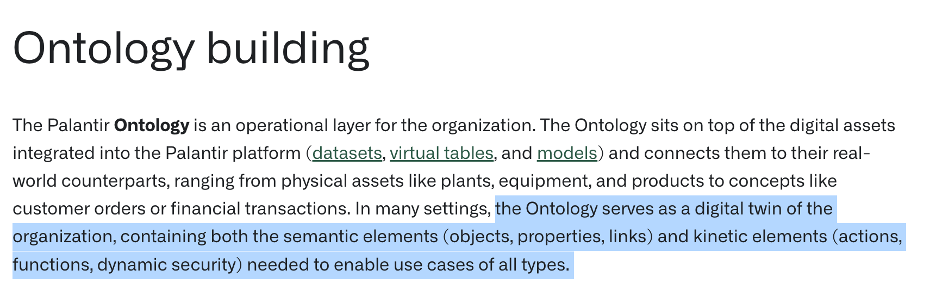

Palantir often talks about “ontology”.

This is basically the structure that takes messy raw data from different systems and organizes it into a model of the real business.

It maps things like customers, orders, suppliers, equipment, or employees into software objects so the company can actually see how everything connects and operates.

They will basically take all of this raw data and turn it into a “digital twin” of the business.

That means turning rows of data into real-world things like a delivery truck parked in Port 3 at the Southern District warehouse.

This basically allows the users to then see where all of their “digital assets” are across the platform. This makes it extremely easy to see how every thing maps together.

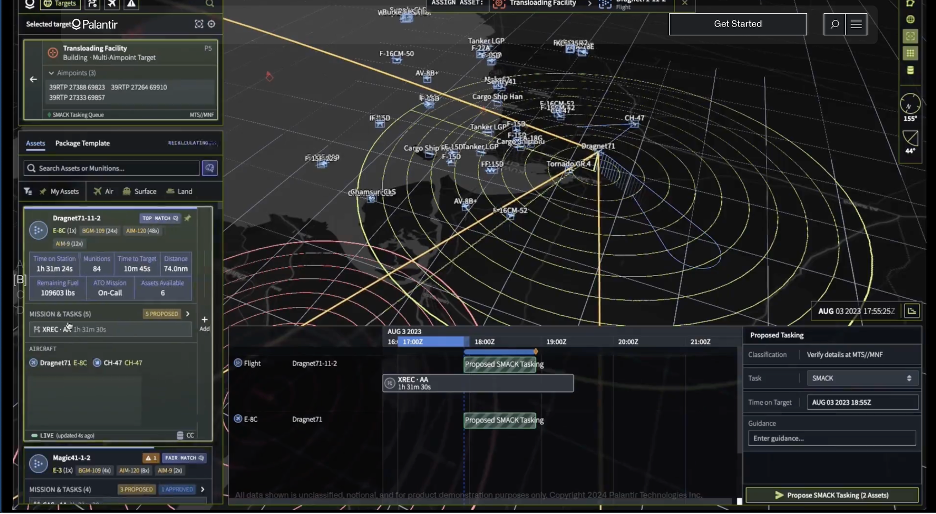

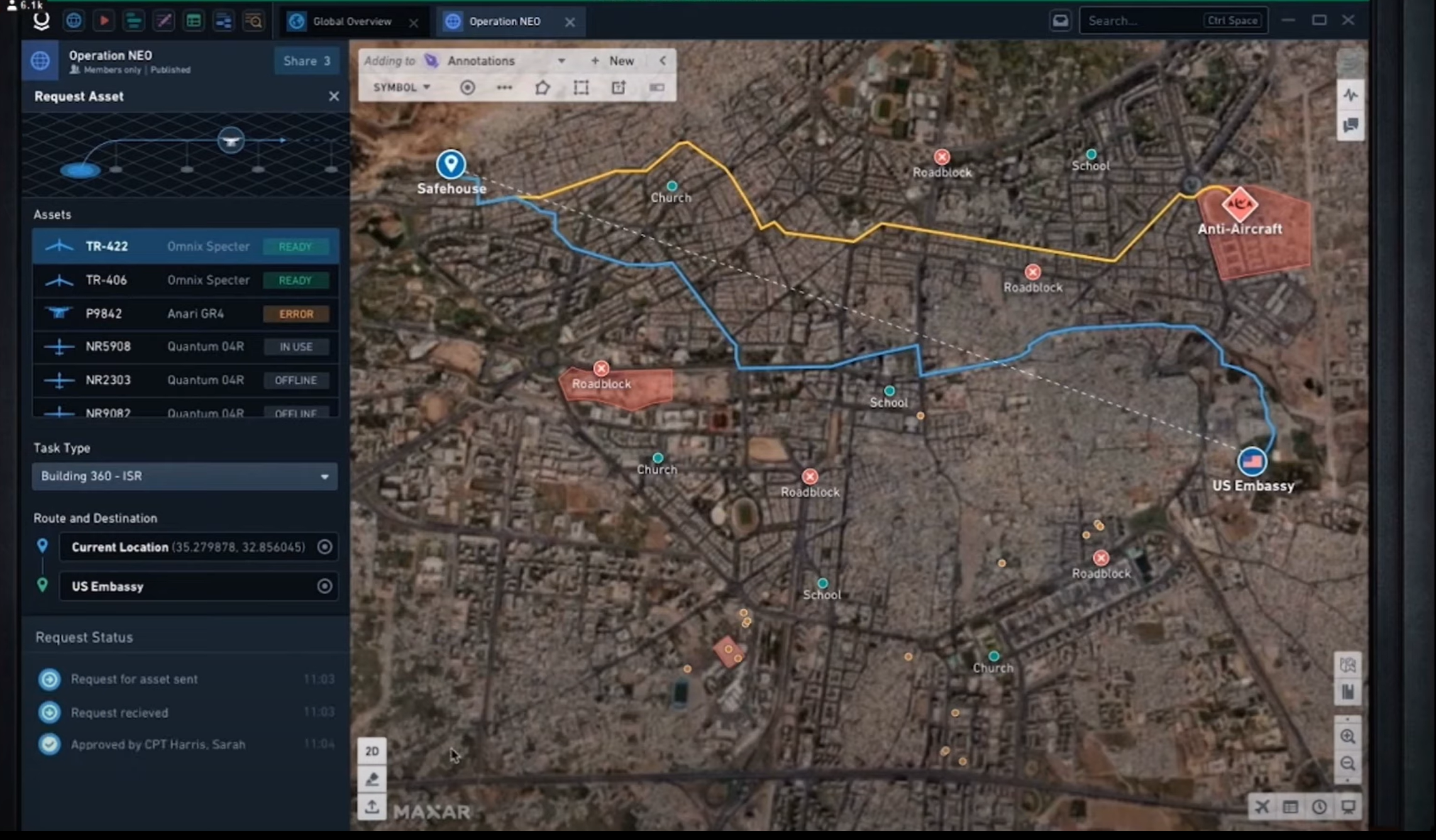

Below you can see an image from their Gotham platform (more on it in a moment), which shows where the military has various assets out in the field.

It is almost like Google Maps, but with the live positions of aircraft, ships, drones, and other assets all mapped together.

The ontological layer is what turns all of that raw data into a usable model of the real world, so the system understands not just dots on a map, but what each asset is, where it is, how it relates to other assets, and what actions can be taken.

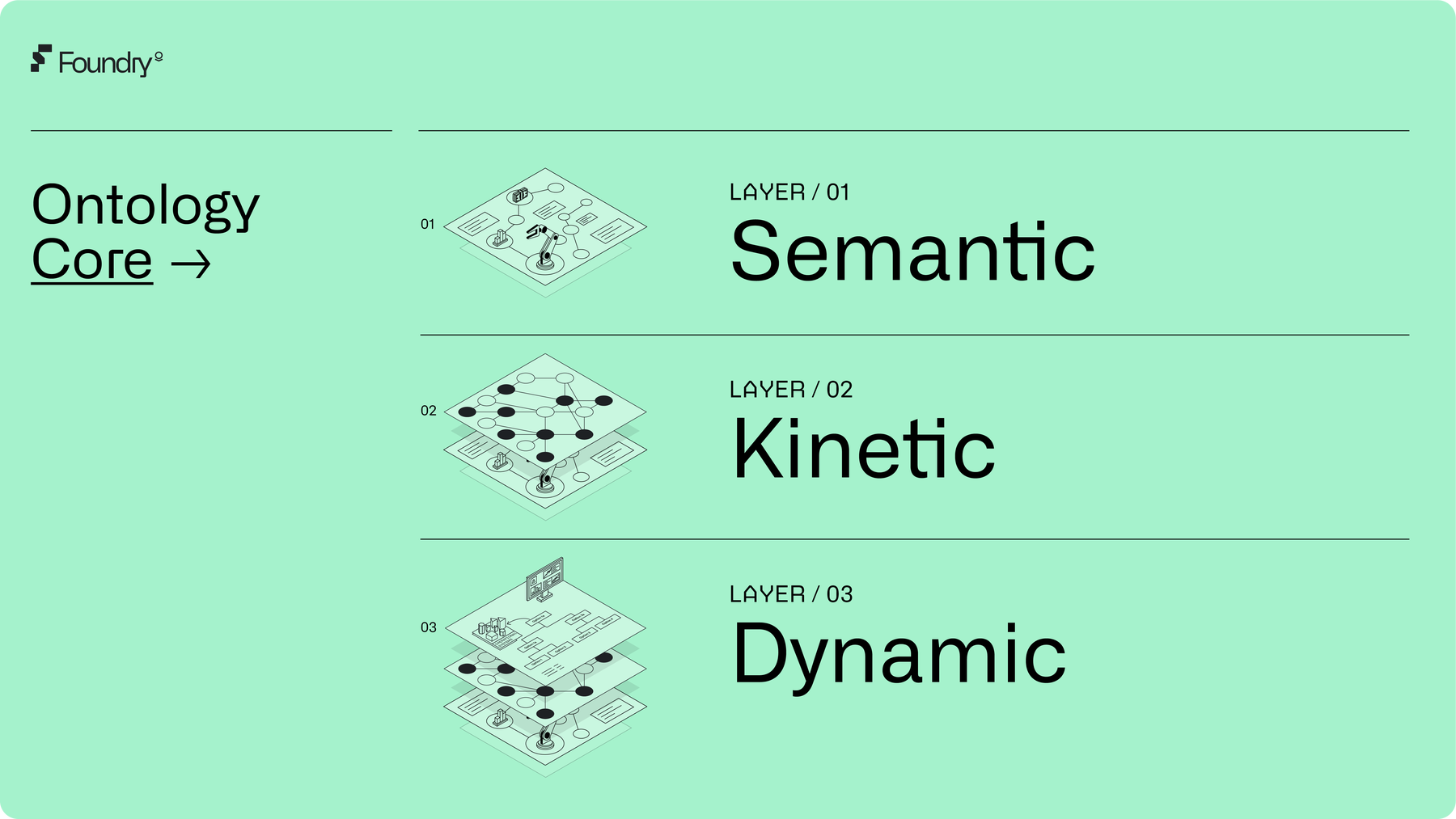

Palantir breaks the Ontological layer down into 3 parts:

1) Semantic: This is the mapping of data. For example, there is a truck, it is at Warehouse A, and it is linked to Order 123. Palantir describes the semantic elements as objects, properties, and links.

2) Kinetic: This is the action layer. It will let a user click into a truck for example and reroute a shipment, update its status, assign a driver, or trigger a workflow in another system.

3) Dynamic: This is how the system changes in real time with visibility into all of a business’s or government digital assets.

Now with that understanding, let us talk about their 4 Principal Operating Platforms.

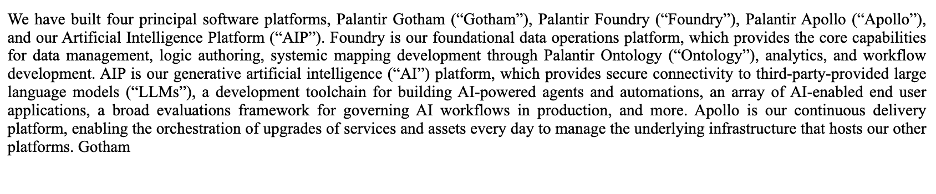

Foundry

· Palantir’s core commercial platform for integrating and organizing data from many different systems.

· Helps companies build a digital model of their business and run workflows on top of it.

· This is the main platform enterprises use to understand and operate their business.

· It is a system of operations

Gotham

· Palantir’s platform for government, defense, and intelligence customers (but doesn’t necessarily need to be restricted to them).

· Helps users map assets, analyze situations, and support mission-critical decisions.

· Think of it as the operating system for military and intelligence workflows.

· It is a system of discovery (this idea of finding the one missing piece of info that can help a government thwart a terrorist attack)

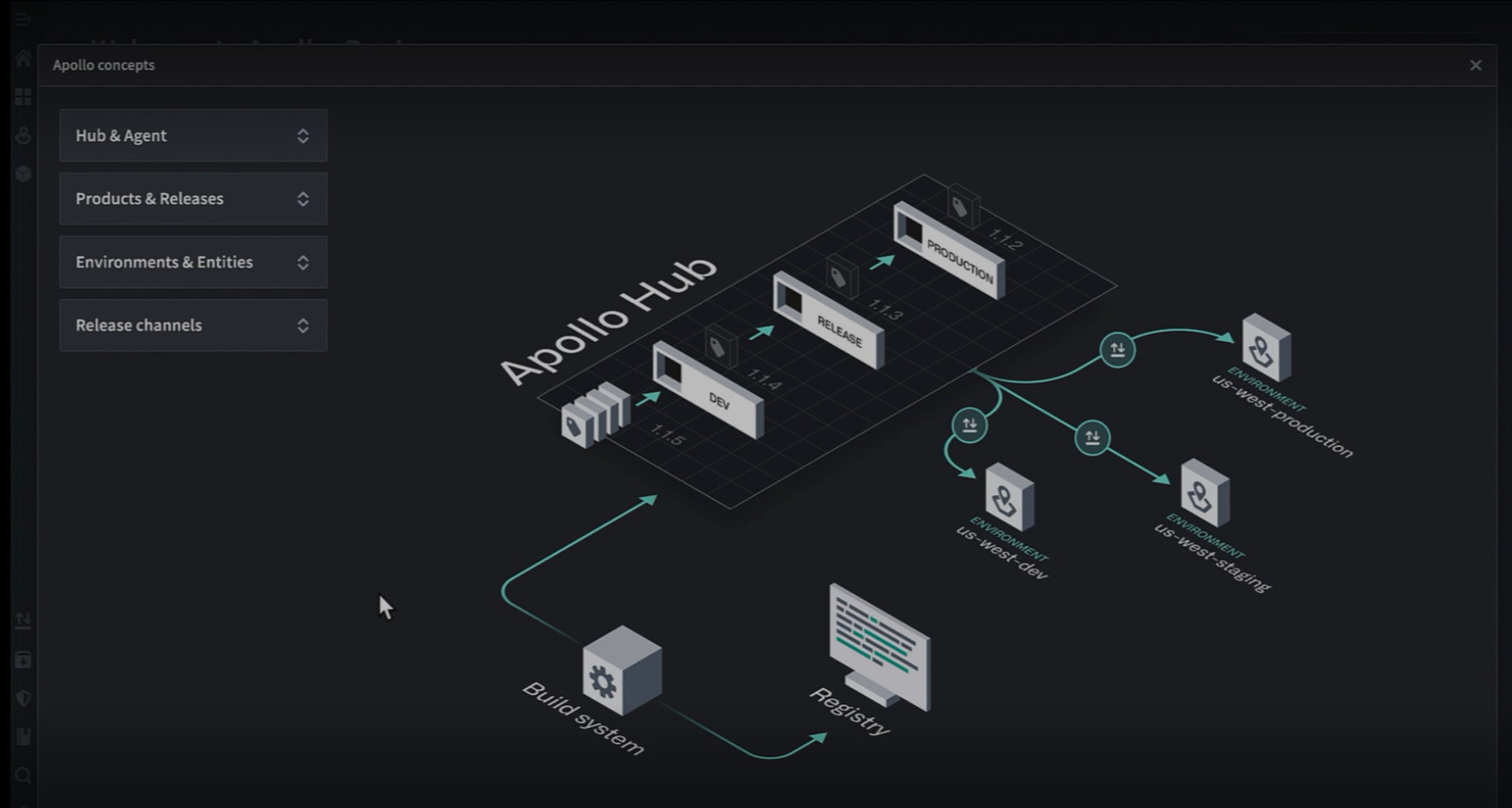

Apollo

· Palantir’s software delivery and deployment platform.

· It helps Palantir push updates, manage software, and run its platforms across cloud, on-premise, and secure environments.

· This is a big reason Palantir can operate in complex and highly secure settings.

AIP

· Palantir’s Artificial Intelligence Platform.

· Connects LLMs and AI tools to a company’s actual data, workflows, and operations.

· In other words, it helps turn AI from a chatbot into something that can support real business decisions and actions.

All of these products are reported in one reportable segment, but they do disclose that 54% of revenues are from government customers.

They have special security clearances to work with all levels of the U.S. government (FedRAMP High, DoD Impact Level 5, and Impact Level 6)

You may have heard of different names like Maven, ShipOS, or Warp Speed.

These are all specialized purpose built applications that sit on top of these platforms.

Maven is the Pentagon’s flagship AI targeting, intelligence, and battlefield awareness system.

ShipOS was built for the Navy specifically to accelerate the time it takes to make a ship by doing everything from schematics to identifying supply chain management to identify potential delays before they happen.

Warp Speed is for material resource planning, factory floor execution, and product lifecycle management for manufacturing and industrial production.

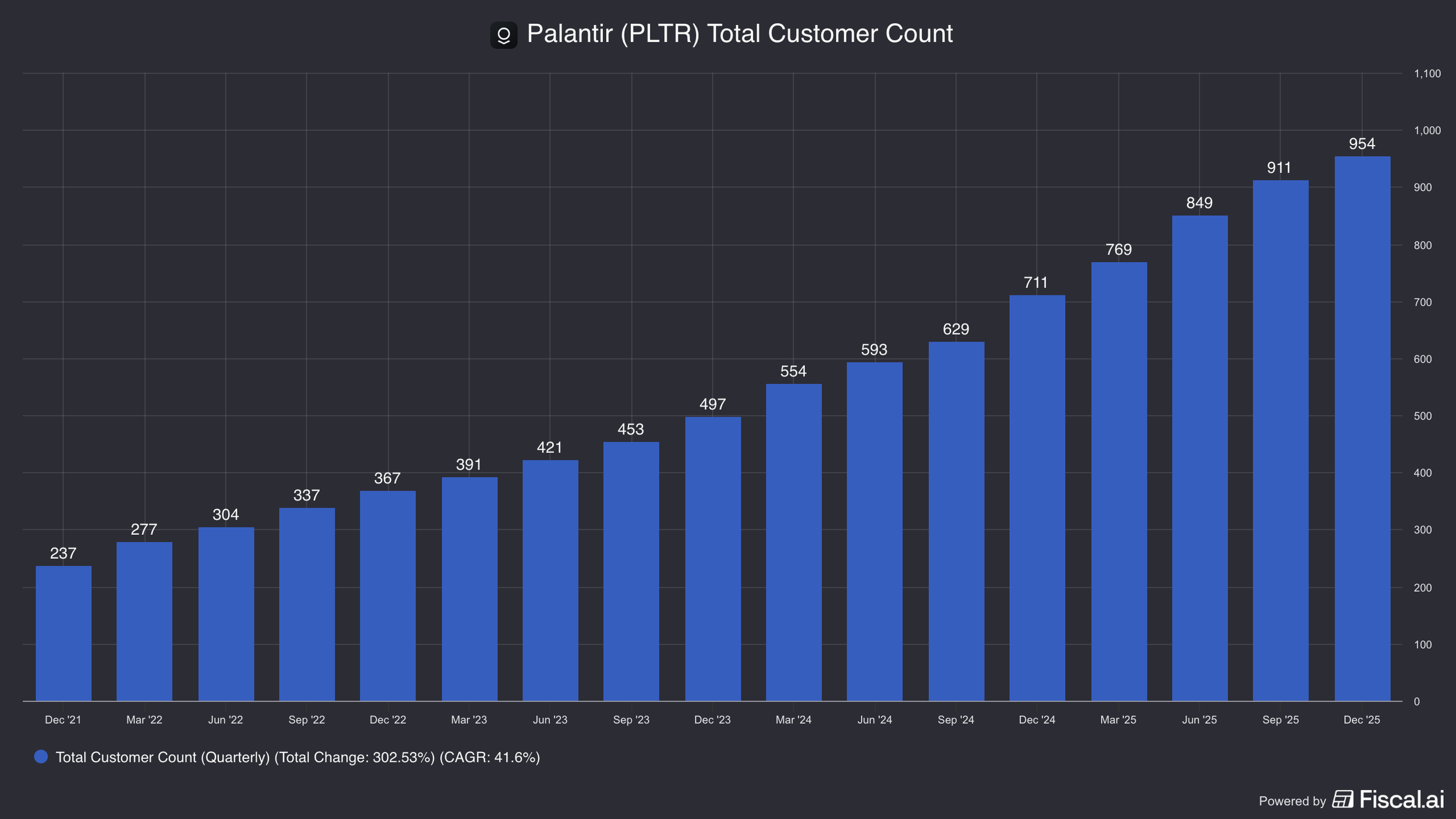

In total they have just 954 customers, so they tilt heavily toward large enterprises and governments.

They typically price contracts in the millions and strike them at the enterprise level with unlimited usage.

This means that they don’t charge on a per seat basis, but instead set up the platform for the whole government department or business.

They are known to have premium pricing and part of that is because of the upfront work involved in setting a customer up.

They have to integrate all of the different data silos a business may have into the Palantir and then help create the ontological layer. Afterwards they may create custom applications and dashboards for the customer.

In order to do this they deploy “Forward Deployed Engineers” who actually go the physical site the business is at and embedded themselves in the business while they take a few months to set them up.

This model has certain benefits:

1) Customized software is hard to rip out

2) Customers like hand-holding

3) It ensures the customer gets the full benefits of the platform.

On the other hand, it inhibits their ability to grow quickly and sales cycles are long.

They would have to create proof of concepts and demos to convince a customer the undertaking, which could take months was worth it.

Palantir is addressing this in part with “AIP Bootcamps”.

Here clients bring their actual data and in 1-5 days they help them set up a real world prototype.

They try to find very easy use cases for quick wins in their business, so the executive can leave with an actual cost saving or efficiency improvement.

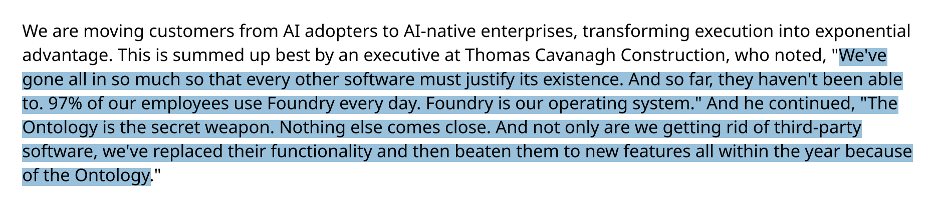

Palantir’s software platform is so powerful that it is able to replace a lot of the other software a business may have been using.

And since they have a platform to create their own software, plus the FDEs to help a business do so, they often are able to create products that replace existing solutions.

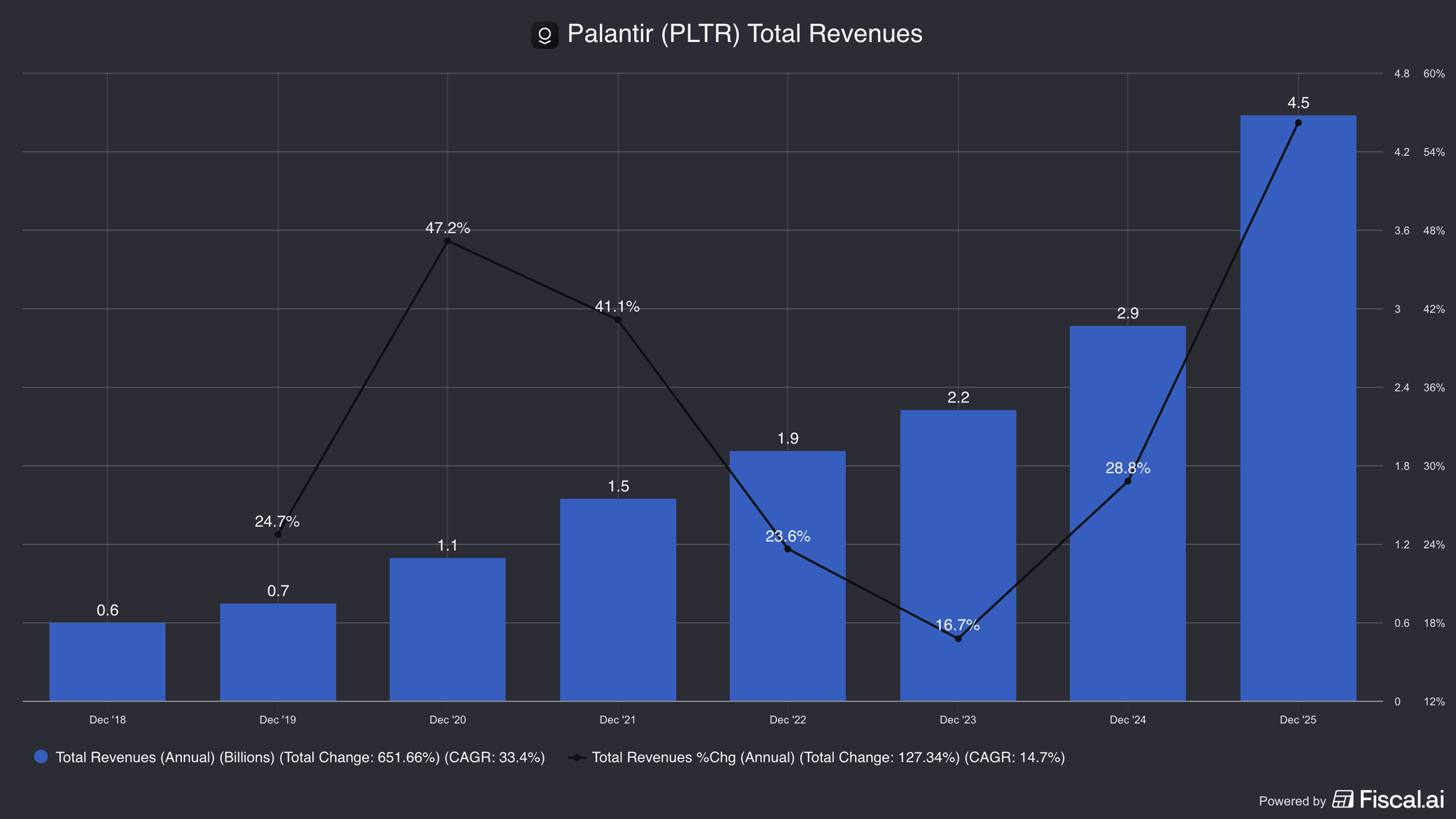

All in all, Palantir today has $4.5 billion of revenue and is growing 56% y/y.

Revenue growth can be a little lumpy because of the contractual nature and sales cycles.

However, sales have reaccelerated in the past 11 quarters, really driven by AIP.

And alongside that the stock has moved from a ~$10 stock to >$150.

What drove this business reacceleration was AI.

With their AIP platform and the AI bootcamp they were able to show ROI to customers much quicker and implement their platform faster.

Instead of using a generic LLM, Palantir could use their proprietary Ontological layer to actually make it much more useful and insightful for a government or business.

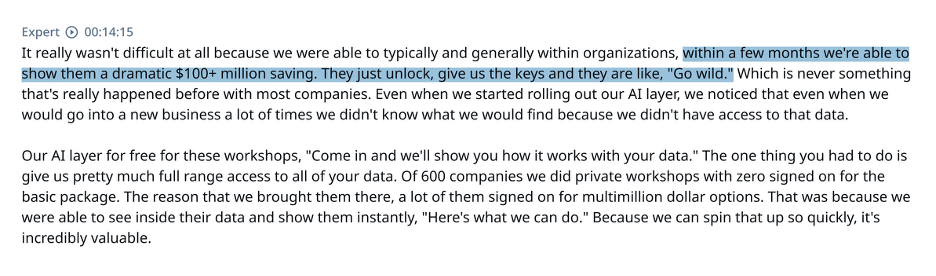

In this AlphaSense Expert call below, a former Palantir head of growth notes how once they were able to prove massive cost saving (+$100 million) they were gaining access to all of a business’s data, which helps increase the contract size and scope.

It also helped them increase contracts with existing customers—net dollar revenue retention hit 139% in 4Q25.

U.S. commercial revenue grew 137% y/y and U.S. government revenue grew 66% y/y in 4Q25.

International is growing less though as those customers are slower to adopt and preference home-grown solutions (which don’t really exist in the same form). International commerce grew 8% y/y in 2025.

All of this topline growth improved margins, which hit 41% in 4Q25, up 21 points y/y.

We will now move into competition.

Competition.

One of Palantir’s biggest competitors is their customer’s.

While the idea that AI created software will displace SaaS is a new risk, Palantir has been fighting enterprises trying to create their own in-house solutions for literally decades.

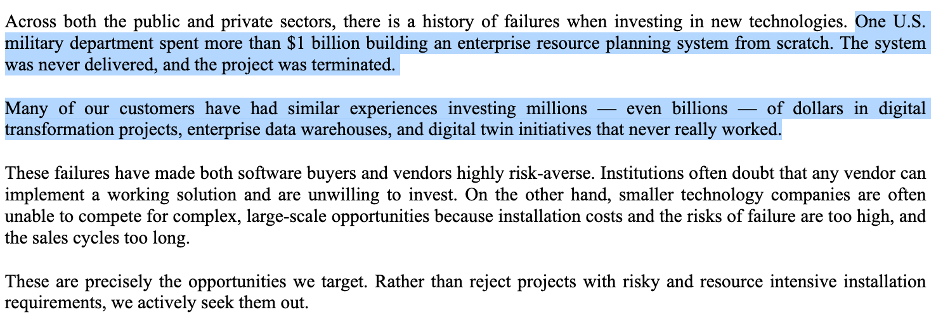

As they note in their 10-k, it is common from governments or large enterprises (especially governments though) to create their own systems from scratch.

They are usually over budget and fail to deliver.

After they fail, they consider Palantir.

In this context, it also makes sense why they differentiate with FDEs because a lot of the set-ups are very bespoke.

Generally speaking, there is 3 sets of competition.

1) In-house solutions

2) Incumbent Software Providers

3) New AI Native Start-Ups

We touched on in-house solutions, which usually fail.

But it is also worth mentioning that the more complex (and old) an organization’s data architecture is, the more they gain from Palantir.

They may have data siloed across several instances of SAP and Oracle for different geographies and departments, and Palantir is able to integrate all of that into their Foundry platform so a company has visibility into all of it.

SAP or Oracle stays as the system of record, and Palantir is the “System of Intelligence”.

While AI can make a data migration faster, it can’t recreate all of the business logic that has been written over decades.

Here is an example of business logic that may be written in SAP code that the person that has written has since left:

“A chemical company has a rule written into its inventory system that If the stock of Chemical X drops below 5,000 gallons, automatically halt all shipments to Tier 3 distributors and divert all remaining stock to the Detroit plant—unless the Detroit plant is undergoing its annual Q3 maintenance, in which case route it to Dallas.

This is why they are not touching the System of Record.

Instead, they work with it.

An internal team might try to stitch together a solution using Databricks for processing and Azure for LLMs, but they still need to create the ontological layer to map all of the data and that is the hard work Palantir has already done.

Incumbent Software Provider Competition.

Many of the software companies we have already covered are competitors to Palantir including ServiceNow, Salesforce, and Microsoft, but also to a lesser extent Snowflake, Databricks and C3.ai.

Snowflake and Databricks are more frenemies, but they have tools that allow data engineers to help build software directly on their data warehouses. This still requires a lot of work, and they don’t have that ontological layer built out the same way.

C3.ai is a legacy rival and does not have the same chops at the operation and mapping layer.

Microsoft

Microsoft already has a lot of companies and governments data in Azure.

They have a newer product called Fabric IQ that is trying to build that ontological layer in a unified data lake (OneLake).

It doesn’t have decades of improvements in actually operational, high-stakes environments like Palantir’s platform does.

Palantir is particularly good at mapping physical assets and real world supply chains. In theory, Fabric IQ could eventually do this as well, but it is still a new product (~ 1 year old).

For many businesses, though, that could eventually be good enough. Microsoft also has integrations with all of their existing productivity apps, Dynamics (their ERP and CRM systems) and can let users interface with Copilot.

Microsoft already powers 20 million businesses' dashboards and in a way Fabric IQ is going to be a big upgrade to that. These dashboards are not a system of action like Palantir is and it will take Fabric IQ some time before they get there and can win businesses' confidence.

Overtime, it seems plausible though that Microsoft will win a large portion of corporations and middle market enterprises.

ServiceNow

ServiceNow is a formidable competitor, but their targets don’t totally overlap (yet).

They want to become the AI control tower that sits on top of everything and is a system of action for a business.

ServiceNow though has much more experience with digital workflows, given their roots in IT departments. They have since grown to other departments in a business, but do not really have much experience with physical real world assets.

ServiceNow has Operational Technology Management, which connects to factory sensors and can send an operational workflow if it detects an issue.

They also have CMDB (configuration database management), which is a map of all of the servers, devices, and sensors in a business.

Right now, ServiceNow is better at linear solutions where a sensor detects a problem in production and can halt it and dispatch a maintenance worker.

Palantir is better at connecting all of the dots and maybe would pick up that the problem came from using a material from a supplier D1 and can then mark all of that raw material that sits in the warehouse as defective and order new materials from the other warehouse in. Then Palantir can also connect that to telling customer B that their order will be delayed.

ServiceNow is very good at workflow automation, but Palantir is better at connecting all of the dots and then taking action.

They currently integrate though and both could co-exist with ServiceNow becoming a sort of nervous center that can monitor everything and send workflow, but Palantir as more of the brain that can produce next level insights and actions.

ServiceNow does has Now Assist AI agents that aim to take over more of these actions, so that could change in the future. They still don’t have that full map and same easy to use UI that Palantir does.

Salesforce

Salesforce is more focused on the front end in the marketing and sales department.

Agentforce is their AI agent service that can take actions, but they don’t have a focus on the physical real word assets and supply chain that Palantir excels at.

While Salesforce is trying to be the orchestration layer of a business that takes action on they still don’t have an ontological map of real world assets.

So in short, Palantir doesn’t actually have any direct competitors. ServiceNow and Microsoft are close, but their current offerings are lacking.

These software incumbents could branch out into some of their lanes, but nothing exist currently. Microsoft ‘s Fabric IQ seems the most likely to take a direct shot at Palantir for businesses, but even that could take years to get the same level of validation and edge real world cases that allows businesses to trust it at the same level.

There are some start-ups like Digetiers and Datawalk that are trying to do something similar.

And other start-up like Neo4j and PuppyGraph that are trying to make it easier for a business to build the ontological layer in-house, instead of relying on Palantir to do that, but Palantir has much more experience with this and is battle hardened (literally).

It seems though that competitors have woken up to the importance of the ontological layer and the importance of data mapping and are no doubt not finished here.

But today, Palantir is in a really strong position to continue to win.

The problem?

The market has already priced them as a winner many times over.

So in order to make a return as an investor, you need them to grow even more than what the market is pricing in…

Valuation.

At a stock price of ~$155, Palantir has a fully diluted market cap of $398 billion. (We were using undiluted market cap in the intro).

It’s worth mentioning, share count has grown 33% since 2021.

Stock-based comp is about 15% of revenue, which is very high.

Last year they did $4.5 billion in revenues with $1.6 billion in net income.

This gives them a sales multiple of ~88x and an earnings multiple of 244x.

By any benchmark, this is incredibly high and only makes sense if they continue to grow at high rates for a long period of time.

Let’s say that at maturity, margins can expand to 50%, which would make them one of the most profitable software companies in the world.

Based off of today’s market cap, in order to trade at 25x earnings, they would need about $40 billion in revenues.

(A 25x multiple is picked because this is around where a lot of software companies with still high single digit to low double digit growth trade around).

We can think of this being roughly what is priced into the stock today…

Which means they basically need to grow revenues 9x to justify their existing valuation.

However…

If you want to make money as investor, they will need to grow more than that. (Or still be growing at a very high rate after they have $40 billion in revenues to support a higher multiple).

They are guiding revenues to $7.2bn for 2026, which is about a 61% y/y growth rate.

How big can they get a decade out though?

It is a very hard question to answer.

Salesforce currently just has $41 billion in revenues and ServiceNow has $13 billion.

This is where an investor is really going to have to lean heavily into how much they believe their value prop and ability to entrench themselves globally in corporations and governments.

Because the IT budgets certainly exist globally for Palantir to be a >$100 billion revenue business…

But that is also a big leap from their base of revenues today.

If you were comfortable assuming they would reach $100 billion in revenues in 10 years, that would be a revenue CAGR of 36%.

If we assume 50% margins and a 25x multiple at that point, that would be a trillion dollar valuation…

Or about a 9.5% annualized return.

Now this math doesn’t count the cash flows they generate in the next 10 years, which after accounting for SBC, could add maybe 1-2% annualized return to that figure.

Maybe a very bullish investor on Palantir though thinks these estimates are too conservative.

On the other hand, maybe you can appreciate how great of a business Palantir is, but think the assumptions needed to get an adequate return are too lofty.

There is of course a lot of risk that revenue growth simply slows down. Or new competition enters the mix.

It will be up to an investor to decide if they believe in the story enough to put a lot of faith in Alex Karp to bring Palantir to corporations and governments around the world…

Or if they want to wait for a better pitch.

For more on Palantir, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.