How to Research Stocks Like a Wall Street Analyst

Get smarter on investing, business, and personal finance in 5 minutes.

I wrote investment research at Goldman Sachs.

I was a stock analyst at one of the world's largest funds, and I've sold investment research to various hedge funds.

Today, I'm going to teach you everything I know about how to research a stock.

This newsletter is split into four parts:

1. Where to start.

2. What to look for.

3. Crafting an investment thesis.

4. How to find the information we're looking for.

Before we get into it, I want to give a disclaimer.

I'm going to do my best to provide a formula for you and give you guardrails of where to go with this, except I want to give the disclaimer that you should get to the point that you move beyond a formula, that you move beyond copying anything.

It should become natural to you.

You should get beyond needing to do a SWOT analysis or check a box using a checklist.

You should get to the point that all of these things become very apparent to you, kind of obvious.

I want you to actually get to the point that you no longer need a formula, and you become a better investor.

Where to Start Your Stock Research.

When you're a newer investor, you're trying to figure out what stocks to research.

You're kind of stuck with four different ways you can find stocks.

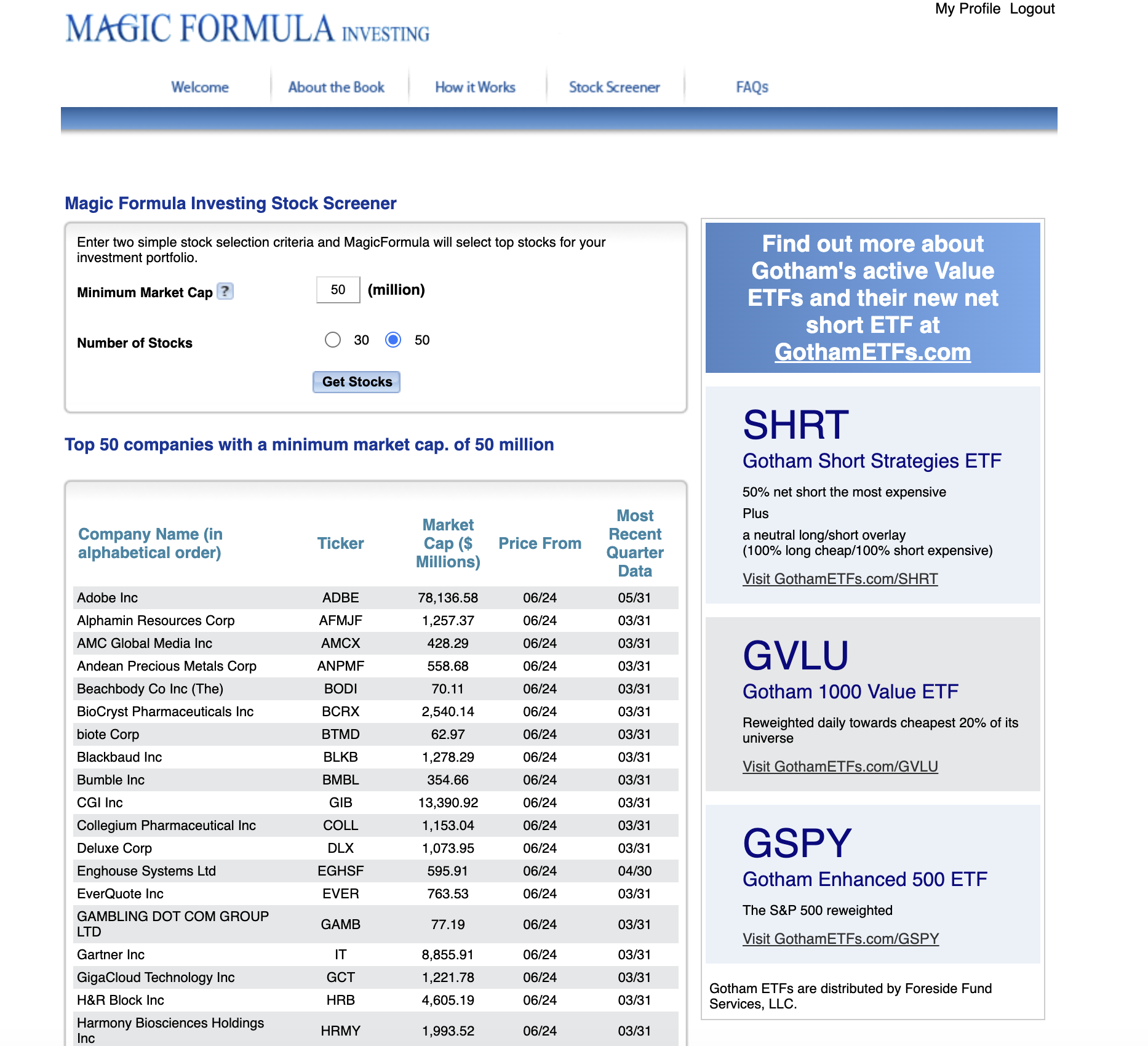

The first way is a stock screener.

I personally don't find this to be the most compelling way to find stocks, but this is exactly where I started, on the Yahoo Finance and the Magic Formula stock screener.

If you're just looking for a place to start, it works.

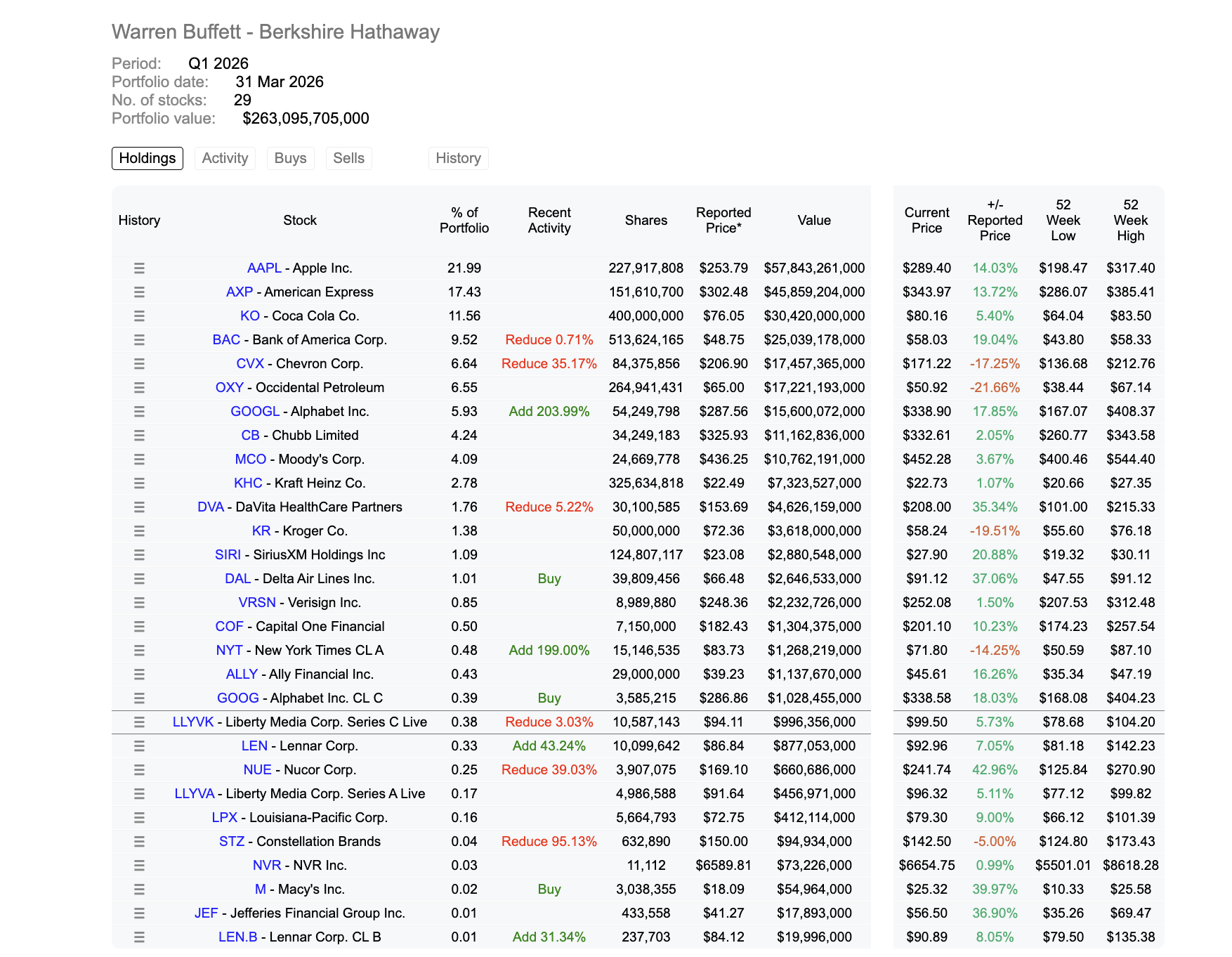

The second place to find stocks is the 13F.

Whenever you're an investment manager, you have to file a 13F, which discloses your positions.

That gives you an idea of what the best investors are doing, so you could copy them.

The third thing you could do is go to Twitter or Substack and look at different people's ideas.

There are a lot of great Twitter and Substack accounts that post great business analysis that you can read.

The fourth thing, and I really recommend this, is look at the things you're using in your everyday life and see if they're a public company.

If you really like a product, there could be something called consumer surplus, which means the business is providing more value than it's taking in pricing.

This is not a foolproof way to invest, but it's a pretty good way to source ideas.

Like myself, I really liked the iPhone and Apple products.

I realized there was a narrative out there that Apple products were going to be replaced by cheaper alternatives from Dell, from PC, or from an Android phone made by Samsung.

This to me was crazy, because I loved the iPhone.

That was how I initially found Apple and decided to invest in that company, because of my experience as a consumer.

Narrowing Down Your List.

That's just the beginning, though.

What you want to do at this stage is kick stocks out as quickly as possible.

If it's something you feel like you're not going to be able to understand, kick it out right now.

You should stay with stocks you feel like you could fully understand.

If you're talking about biotech, you have to know the science.

If you're talking about semiconductors, you need a strong fundamental basis before you can properly look at the stock.

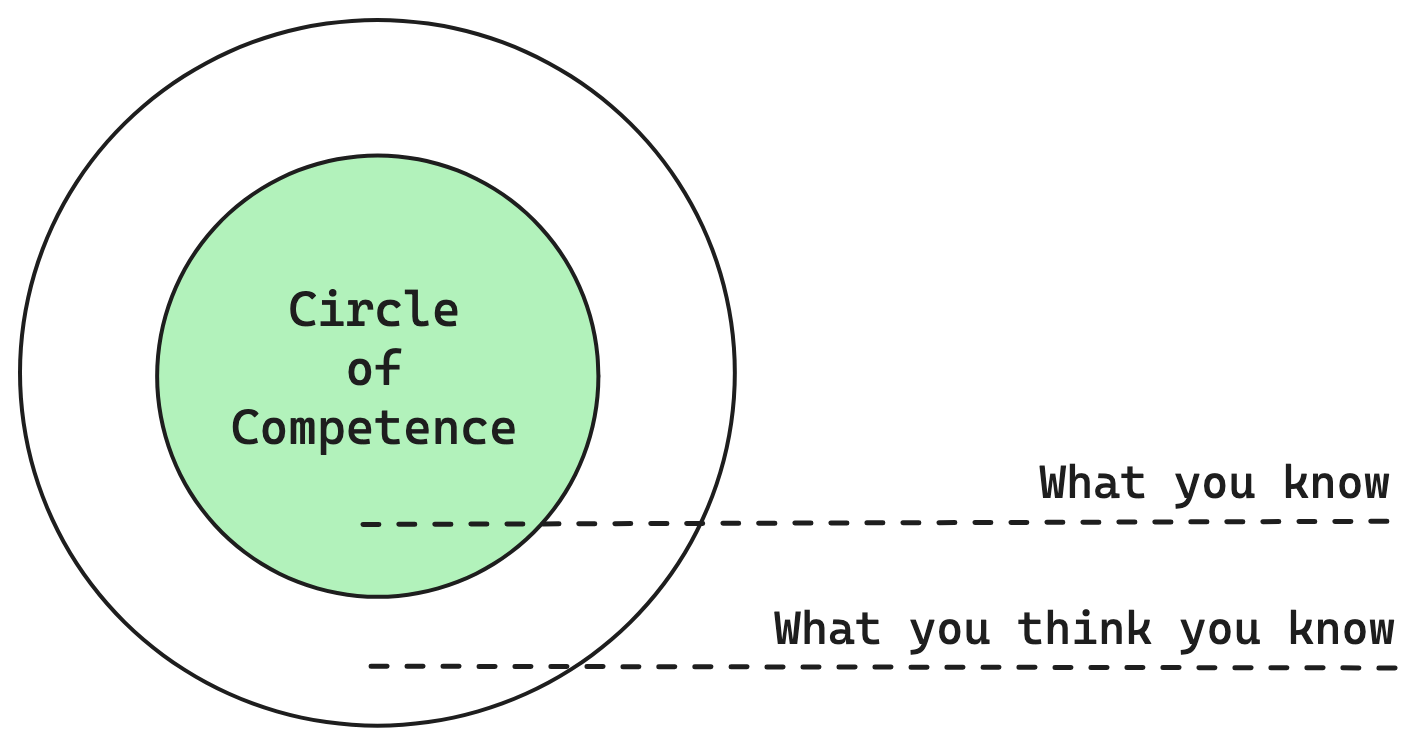

For most people, I'd advise you to stay within your circle of confidence, which could be retail companies or food service companies, pretty easy to understand.

I think you can understand Google and Amazon.

NVIDIA might be a little harder.

It's a little tricky, though, because you might have a list of a hundred companies, and you might ask which one you should look at first.

This is where intuition comes into play.

Maybe you see a stock trading at a much lower multiple, and that's drawing you toward it.

You should still look at some really great companies, even if you're not going to invest in them now because of high valuations, because they could sell off in the future, and it's a good way to learn what a great company looks like.

One last thing you can do to weed out companies on your list is look at their financials, the profit and loss statement, the balance sheet, and see if the company has a lot of debt or is loss generating.

If it's been consistently loss generating, that's going to be a harder investment to analyze.

When you're a beginner, this is going to feel overwhelming, and that's normal.

Over time, you'll start to create your own map of things that look good and bad.

What to Look for in a Business.

Now you've narrowed down your list of stocks and have a business you want to research more.

This is not an easy question to answer, and we can't list everything, so I'm going to give you guiding principles that will help you think these things through on your own.

I've read a lot of investment checklist books, the kind that list a hundred things to check on every investment, and I'm not doing that.

Instead, I've looked at enough businesses that things that look wrong pop out to me a lot clearer, and that's what I want you to develop.

I don't want you to need a rule book you're constantly referring to.

Three Guiding Questions.

The three things I want you to think about are, first, what is the business?

Why do customers come to them, what do customers value about them?

In the past I talked about a framework I created called the consumer hierarchy of preferences.

If you go to Chipotle, you're buying it because it's healthy enough, quick, convenient, and relatively cheap.

A lot of the time people don't take the time to realize why a customer goes to one business versus another.

If I asked you why someone goes to Moody's versus S&P Global, versus Fitch, why don't they go to any of the others?

Continuing to ask questions until you hit something you're confident in, that's the first piece of advice.

The second question is how do they make money?

You might think Meta just sells advertising.

Are they just taking a budget from an advertiser, or selling a specific return on ad spend?

Take Amazon for example, they take a percent commission on items sold, but there's a different commission across categories, on top of different fees for logistics and advertising.

That's three different businesses we just unpacked.

The third question you should ask yourself is how defensible is the business?

This is the idea of moats.

Is this business doing anything anyone else couldn't do?

A great company creates value, captures a portion of that value, and then protects it.

I want you to do all of this from first principles.

I want you to think through everything as if you know nothing, because when you go to a checklist and just check a box, you're not really critically thinking it through.

You could say, oh, eBay has a network effect, so it has a great moat.

Are you sure about that?

Forget everything you've learned about investing and just stick to those three principles.

How is a company 1) creating value, 2) capturing it, and 3) protecting it.

I promise if you do that analysis for eBay, you'll come up with a very different answer than a Porter's Five Forces or a SWOT analysis.

The Frame Problem and Building Business Common Sense.

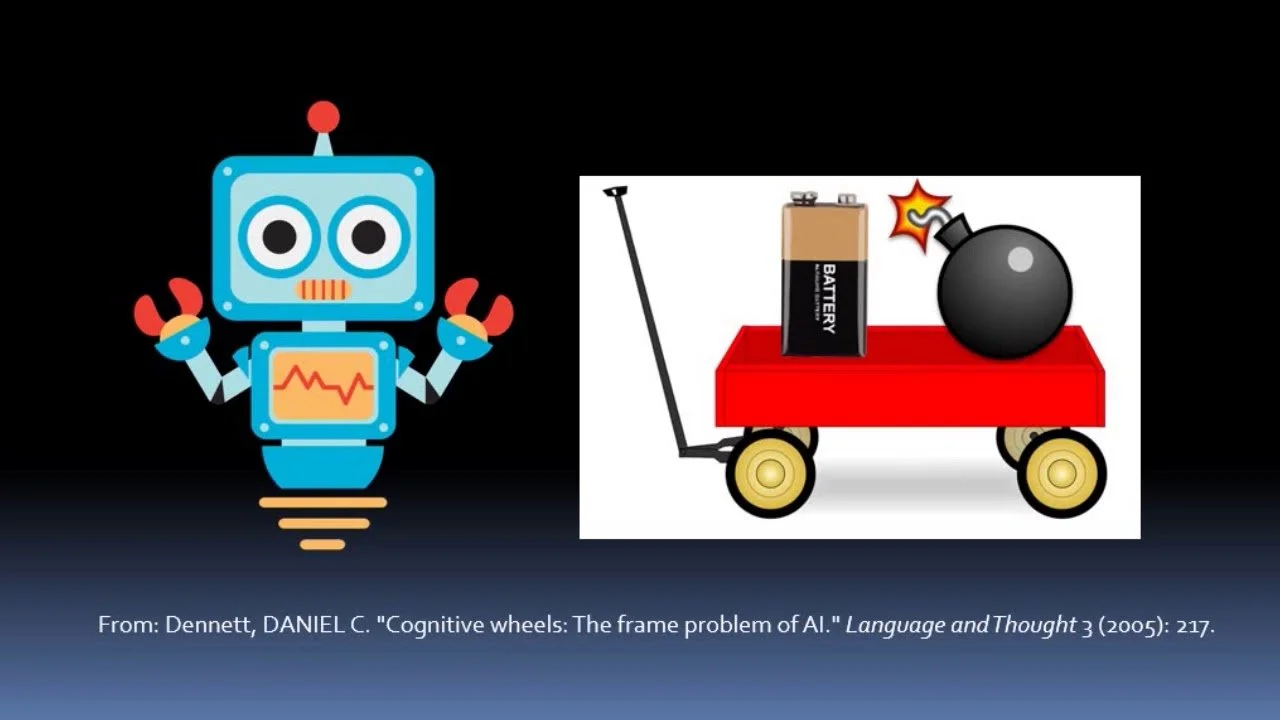

Now, there is the frame problem, and this makes it tricky, the idea that you don't actually know what is relevant when you're initially starting.

This comes from computer science.

There's a bomb and a battery sitting on a wagon in a room, and you go to a robot and say, can you remove the battery.

The robot doesn't know what is relevant, and some robots just pull on the wagon, which brings the wall down, and it blows up.

When you're going through an annual report, you have your own version of the frame problem, what is relevant.

What are the wagons in the story, what are the batteries, what's the bomb.

You have to be able to tell, because there are only so many avenues you can research.

Sometimes you'll come up with an ad hoc thesis while looking at a company.

Maybe it's Mercado Libre, and you notice it's suspicious how much they're increasing their credit cards.

That's called pulling on a thread, and you research it to see whether it's really an issue.

You'll eventually face the question of how much research is enough.

You could also go off on rabbit chases that lead nowhere.

If you're doing your job well, you want to destroy this investment, checking delinquencies or lending standards.

Doing this enough builds your confidence in the business.

When I researched Meta, back in January 2023, there were a lot of issues facing the company; TikTok competition, App tracking transparency, the FTC asking for a divestiture, issues with the EU, plowing money into Reality Labs, and the transition to Reels, showing negative revenue because they weren't monetizing it yet.

You had to figure out every one of those issues and come up with an opinion on each.

This is all part of building a narrative, how the company creates value, captures it, and protects it.

Then you build a hypothesis and start destroying it.

What can go wrong?

How am I wrong about this?

The most critical thing is to build common business sense.

If I told you I have a plan to bring cupcakes to dogs in space, it doesn't take long to tell me that's a bad idea.

Over time, you develop that same reaction for investments.

A lot of this is building understanding of what's worked and hasn't in different businesses, and applying that to something like SpaceX, where businesses have never tried to scale in space before.

Build your business common sense.

Crafting an Investment Thesis.

By the time you're through with this research process, this has already kind of happened naturally.

I've never actually sat down and asked, what is my investment thesis on this stock, not since I did a stock pitch in college.

You don't need to spend a lot of time coming up with something very novel.

If you're doing research on Meta, it could be, “This is the valuation, I think earnings are going to continue to grow, I don't think they're going to spend all their cash flow into oblivion on the Metaverse.”

That could be your investment thesis, and that's fine.

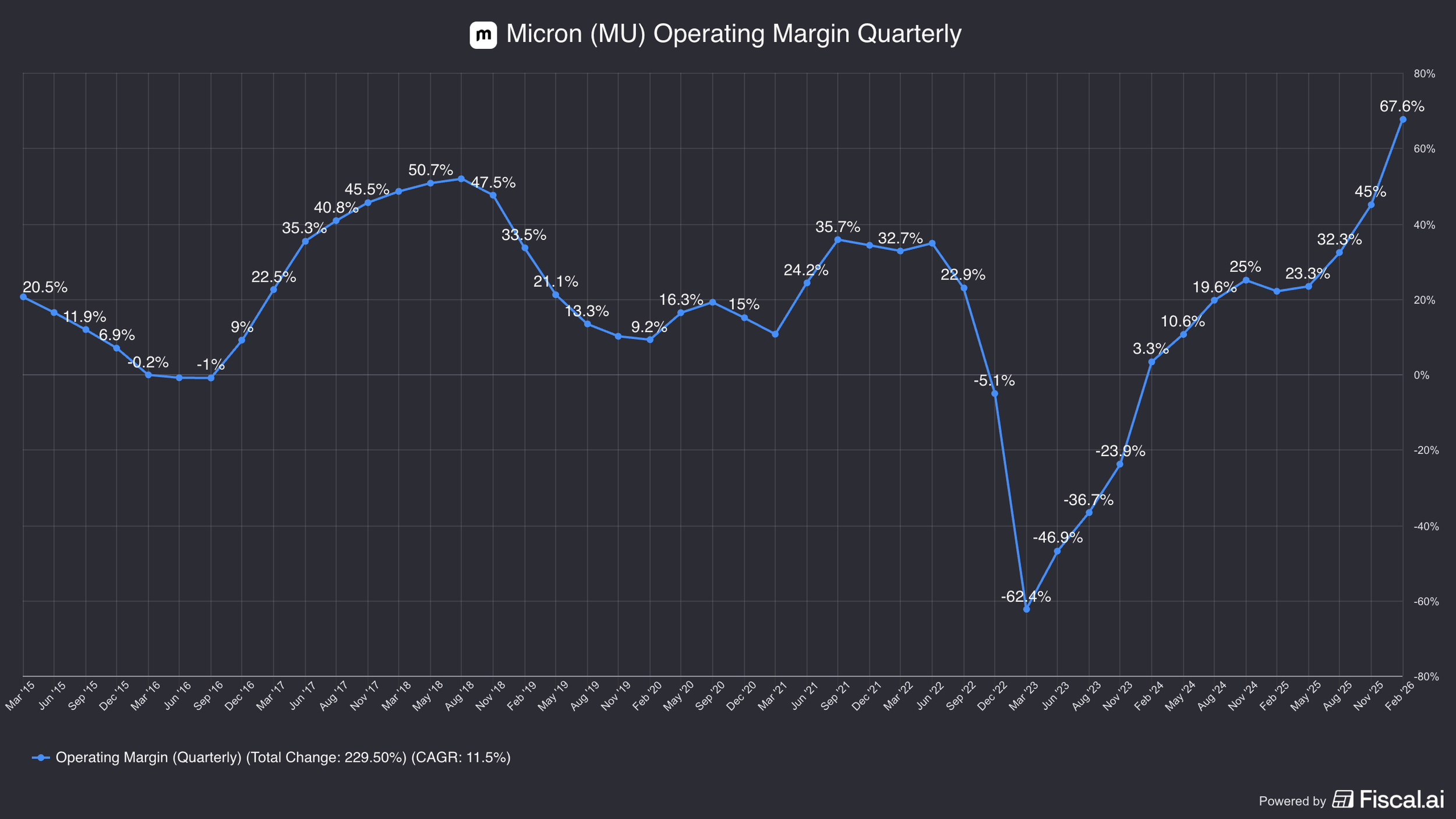

A lot of times people feel like they need something really creative, like memory is actually going to be the bottleneck in AI, so Micron is going to have a 65% operating margin.

This actually gets back to an idea from David Deutsch.

The more specific you are in a thesis, the more likely you are to be wrong.

That might sound really smart, but it opens up more areas where they could be wrong.

If you caught Micron three years ago, congratulations, hats off to you.

That's not how I invest, because I don't think it's realistic.

A lot of the people who got the mortgage crisis right and were short mortgage backed securities never been able to translate that into reproducible success, because that's a trade at the end of the day.

What you can do is find stocks and great businesses in a reproducible way so you can hold them for a long time.

I'm not looking for the next one-off catalyst that could change everything.

At least that's my bias, that a thesis needs to be really smart and cute, and that's not really the case.

It could be plain vanilla and simple.

This is why it's a great company, this is why it's defensible, and the valuation seems attractive to me.

Tying Your Thesis to Numbers.

The next thing you're going to want to do is tie your investment thesis to numbers.

I do this at the end of almost all of my business breakdowns.

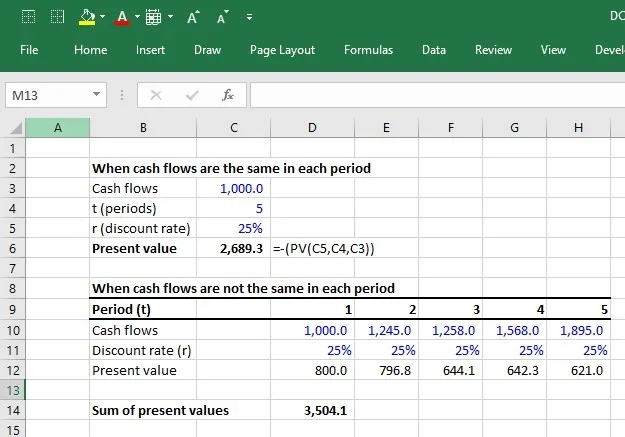

Keep in mind, a multiple is just a shorthand for a discounted cash flow model.

If you're wondering what multiple is right, you need to create a DCF.

You can look online how to do it, and Claude can even help you with this now.

Once you have that done, adjust the assumptions so you're comfortable with them.

Then go to Excel and set the equation so the sum of all the discounted cash flows equals the current market cap, and solve for the discount rate that makes those numbers match.

That's a reverse DCF, the return being priced in today.

High growth assumptions paired with a low return aren't attractive, but conservative assumptions paired with a high return could be.

Something else you could do is go out a year and see what multiple you're paying, by dividing the market cap by your earnings estimate.

That's ultimately why we pay multiples for stocks, it goes back to the DCF.

Sometimes people want to buy below the current market multiple, but if it's growing quickly, they're willing to pay up.

As a rule of thumb, don't go out more than three years for the multiple to normalize.

How to Find the Information You Need.

Start with Regulatory Filings and Company Sources.

The first question you need to ask yourself is whether this information exists or not.

If you've never looked at the business, you don't know what they're disclosing or not disclosing.

You should start with the annual report.

Just get comfortable.

The first thing I like to do is skim it, trying to understand the segmentation and basics of the business.

I like it if there's an investor day, that's a pretty good source of information.

From there, go to the earnings transcripts and read back the last year of them.

Sometimes, when I do really deep research, I would read every single earnings transcript and annual report for a business.

When I researched Copart, that was over two decades worth of transcripts and reports I read.

I knew they mentioned market share only twice in their entire history, in 2003 and 2004, and never again since.

If you're using AI, it's not necessarily going to know to check that, because I didn't know to ask, which goes back to the frame problem.

I don't think you necessarily need to read twenty years of transcripts to invest in a business, but it might be helpful to understand what research overkill is.

Now I'm more of a skimmer, since once you know what they're going to say on a call, you move through it a lot quicker.

You're going to go to SEC Edgar, where all the documents are.

Companies also have their own investor relations websites, usually prettier versions of the documents.

Sometimes they'll put disclosures in an earnings release that don't exist in the annual report, so check all of these sources.

You can also check out the proxy statement which is a great and commonly overlooked resource.

Getting Creative with Alternative Sources.

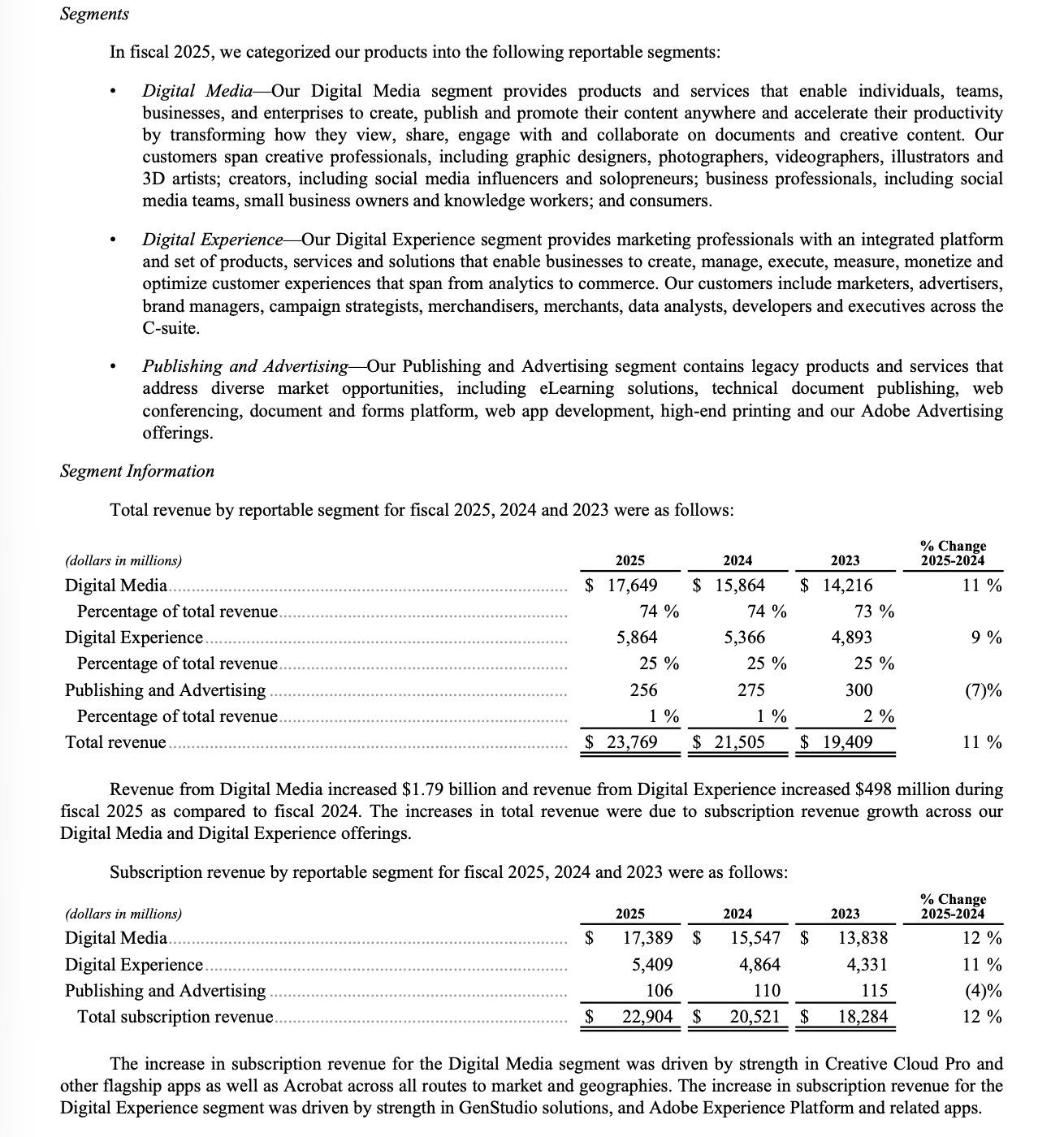

Now, if you're researching Adobe, and it hits you that enterprise is a lot stronger than consumer, how big is Adobe's enterprise business?

You go to the 10-K, read the segments, and search for it, and you're not going to find it there.

You go through earnings transcripts and find they've said a couple things, but not directly what you're looking for.

Otherwise, you can look at alternative sources.

When it's business to business, it gets harder.

I use expert call networks, talking to an expert at a business, or someone at Adobe.

It's expensive to access, and if you don't have it, you have to get creative.

Either pick businesses you'll have higher confidence in, or get creative.

If you're a college student, you have an advantage, because people are more likely to talk to you than to me calling up trying to make money off a stock for clients.

Otherwise, get creative.

Reddit is great.

Check different social media platforms.

Don't just stop at Google, because it doesn't have access to these walled gardens.

If you're looking at a company in a different language, search in their local language.

When I looked up Coupang, I searched a lot in Korean.

I commissioned a survey of over a 150 Korean consumers, to understand whether it's really like the Amazon of South Korea.

Going back to the Adobe question, you'd circulate from disclosures that it's anywhere between 20-50% of revenue, a wide range, and it comes down to your discretion as an investor.

You may look at Mercado Libre's credit history and whether losses are going up, and not find anything, so you make a judgment on management.

The key thing is, 1) does the information exist, and 2) can you find it somewhere else, through a network, or messaging people on LinkedIn, Reddit, or YouTube.

If you can't find it, does it kill the thesis?

A lot of times you'll say, I don't know if I'm confident in this, and that's fine.

You go back to step one and go again.

That is everything involved in the research process, and I really want to emphasize learning for yourself and taking time to practice.

Continue to research stocks but also learn about businesses that have succeeded and failed, because that helps you know what to avoid.

The best thing to do is get started.

Good luck.

For more on How to Research Stocks, check out the video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.