Duolingo Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

Duolingo is one of the only mobile app businesses to ever reach a billion in revenues.

They are cash flow positive and growing fast.

But also facing a new threat that sent them down 60%.

Let’s break it down 👇

What does the business do?

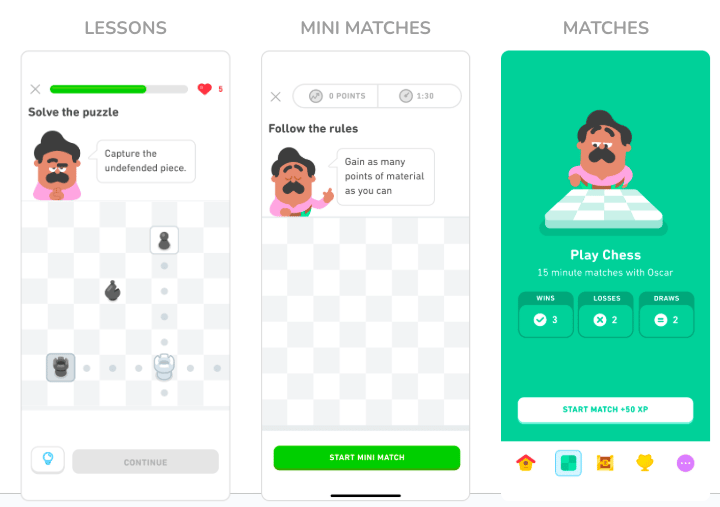

Duolingo is a mobile app that helps people learn new languages. The app is uses a freemium model, which means it is free to download with some ads. Users can pay to get rid of the ads and get some more features.

They currently have 135 million monthly users and 11.5 million paying subscribers.

Duolingo is popular because they gamify users. That means badges, sounds, and a lot of animations to encourage a user to stay on the app.

50 million users open the app every day.

How do they create value?

Duolingo is not about teaching. Knowledge is free and abundant. There are thousands of free ways to learn.

What Duolingo really sells is engagement. By helping make learning more fun, users are more likely to actually learn.

Social media has shortened attention spans. With gimmicks like streaks, leaderboards, and gems, users get a bit of dopamine release for progress—this helps keep users coming back.

The opportunity?

There are 1.5 billion people learning a language!

But Duolingo wants to expand beyond just languages. They have rolled out courses in math, music, and chess.

Chess is currently growing faster than their original language courses.

If Duolingo is successful in dominating more categories, they could have many years of strong growth.

The Problem?

AI.

Well… maybe.

Investors are now concerned about three things:

1) AI chat like ChatGPT or Gemini will replace the need for users to go to Duolingo.

2) AI translation will eliminate the need to ever learn a language because Airpods will be able to live translate different languages.

3) AI makes it easier to make apps and so their will be more competitors.

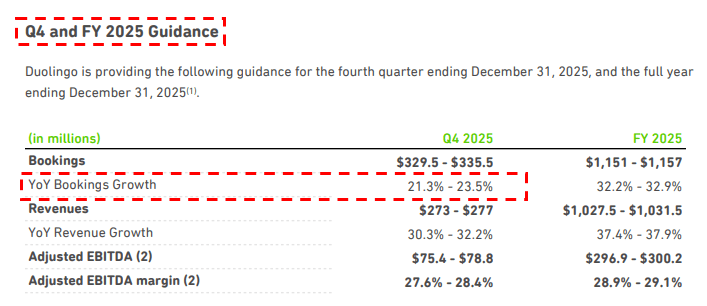

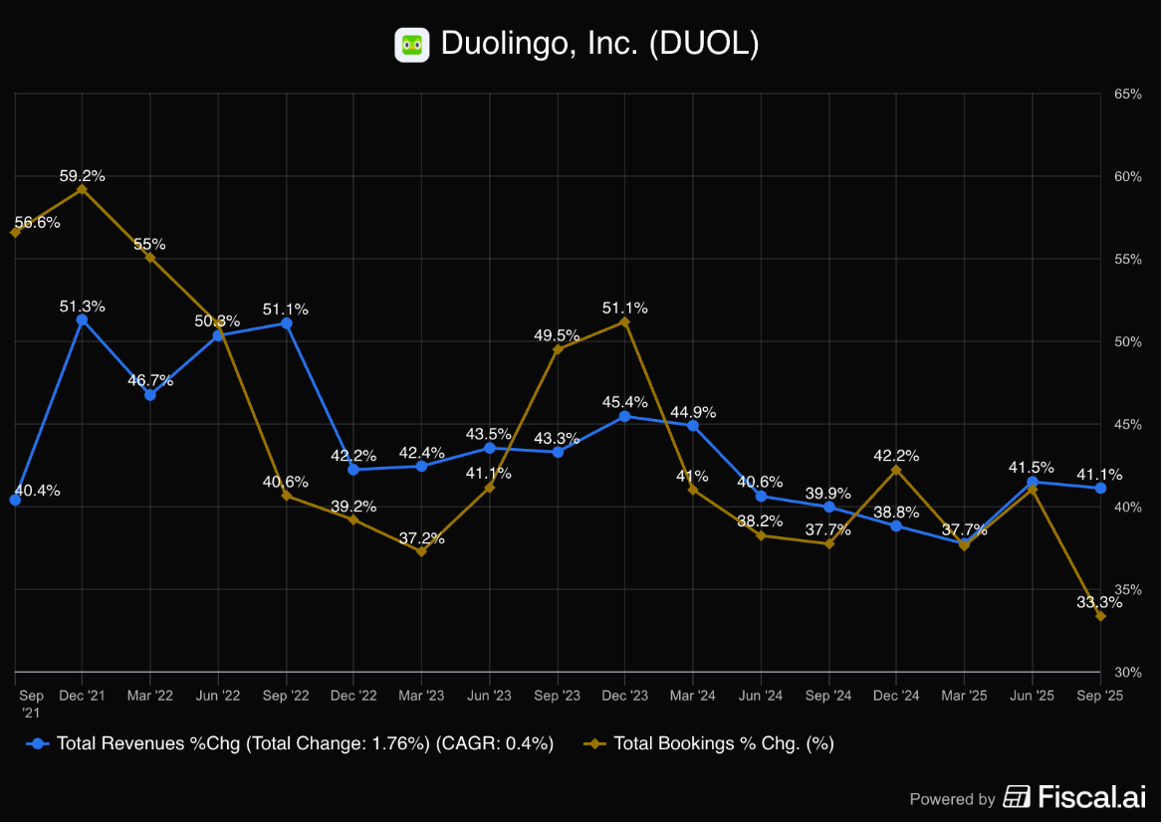

Investors are worried this is what caused growth to slow. Revenue growth was 41% last quarter and now management is guided Bookings to 20%.

Bookings is a LEADING INDICATOR. This is because when someone signs up for an annual plan, the full amount is “booked”. The revenue is then recognized over the next year.

TLDR: Revenue growth is going to slow to 20%, HALF of what it was just two quarters ago.

BUT, is this REALLY because of AI?

Growth Slowing

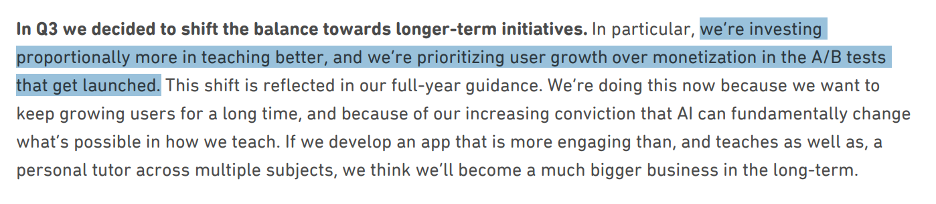

CEO Luis von Ahn said in their investor letter that they are focusing on long-term growth.

1) Focusing on improving the product with AI and user growth, not monetization

2) Posting less “unhinged” marketing content to avoid hurting the brand

So what about the 3 AI risks?

In my opinion, that’s not the risk.

AI Risk 1 Rebuttal:

It is a lot of work to use ChatGPT to learn a language. People like Duolingo because it is more fun to use with graphics, animations, and noise. All things not present on Chat Apps.

Could that change? Yes. Will that be a priority for them. Probably not.

AI Risk 2 Rebuttal:

People don’t learn languages just to communicate, but because they like learning and the connection of talking to someone in a local language. Putting a phone and earbuds on does not address this need.

AI Risk 3 Rebuttal:

It is already easy to make apps. It is hard to get people to use them.

Why would someone pick an unheard of language app instead of a better known brand that some of their friends probably already use?

So is it a buy?

I don’t give recommendations because I don’t think you’d be learning if I just told you what to do at the end.

However, here is what you need to believe for an investment to work.

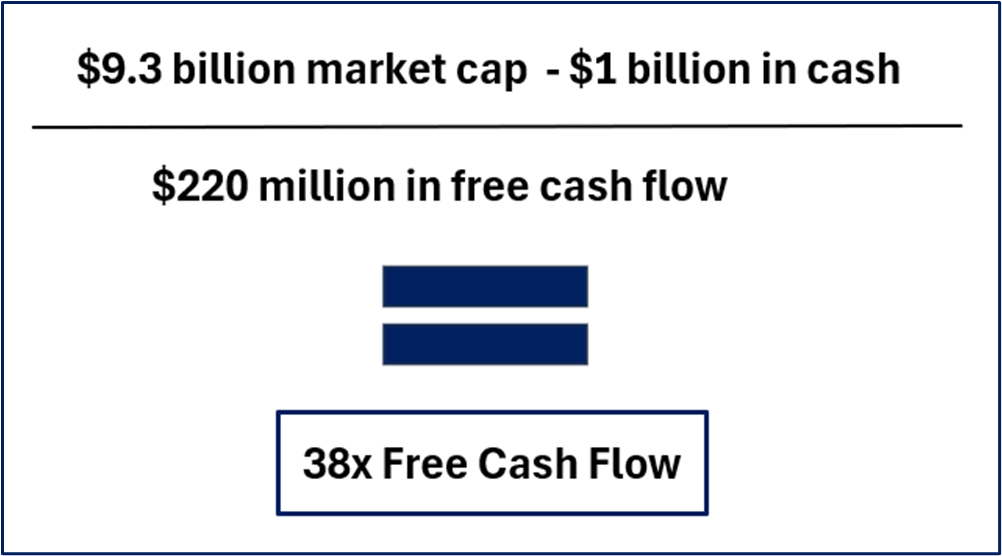

At $200 a share, they have a market valuation of $9.3 billion.

They have no debt and $1 billion in cash.

After subtracting stock based comp, they have $220mn in free cash flow.

That is about a 38x free cash flow.

If they can continue to grow at 20% (or faster) this is a fair multiple to pay.

In 3 years, they would grow free cash flow to $380 million.

That means that 38x multiple drops to 22x in 3 years.

If they can still grow high single digits in 3 years, then 22x is a fair multiple to pay.

If they can grow at least low double digits as they exit year 3, then 30x is a fair multiple to pay.

The difference between the 30x, or the "fair multiple" and the current estimated multiple, or the 22x, is what your return could be.

30x / 22x = 36%.

However, these are just some assumptions.

And every investor needs to make their own assumptions.

It could be even better… or worse.

For more on Duolingo, including a risk I did not discuss here, check out this YouTube video below.