Meta Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

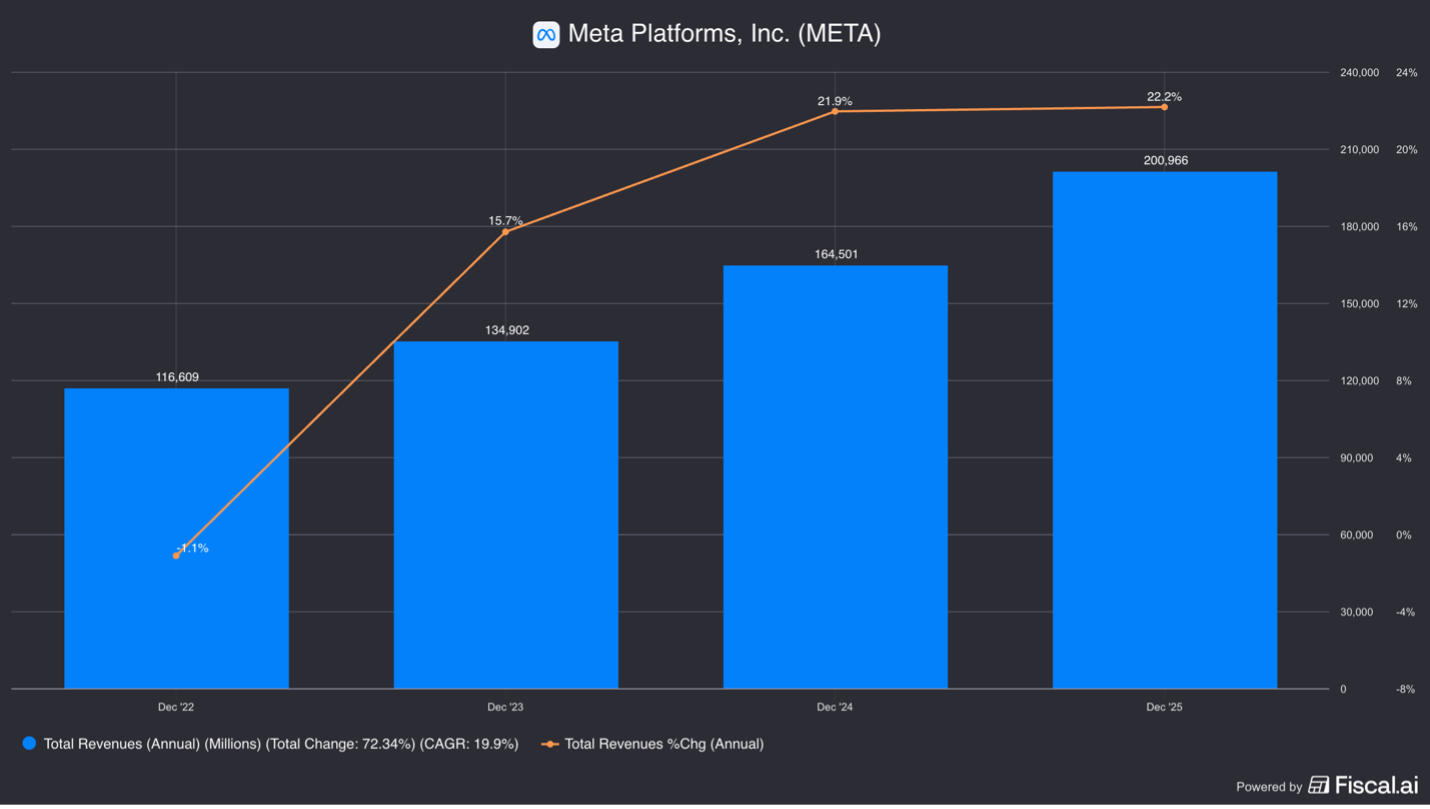

Meta is the cheapest stock among all of the big tech names.

Trading at 22 times trailing earnings, while also growing faster.

They grew over 20% last year.

And management is guiding toward an acceleration to roughly 30% in the coming quarter.

The apparent disconnect between growth and valuation has prompted investors to question…

What am I missing?

Several prior overhangs have diminished.

Competitive pressure from TikTok appears more manageable than feared in 2022, and the probability of a forced divestiture of Instagram or WhatsApp by the FTC has receded relative to earlier regulatory rhetoric.

At the same time, Meta is one of the few large-cap platforms demonstrating measurable financial returns from AI.

AI-driven improvements in ad targeting, content recommendation, and measurement are not merely experimental, they are contributing to revenue and operating profit.

There is also a longer-dated strategic option embedded in the business.

Meta’s Ray-Ban smart glasses have reportedly sold multiples of the unit volume compared to Apple’s Vision Pro headset.

While both products remain early-stage, Meta’s traction suggests it may be establishing a foothold in the AR wearables category.

If augmented interfaces become the next platform shift, that position could prove valuable.

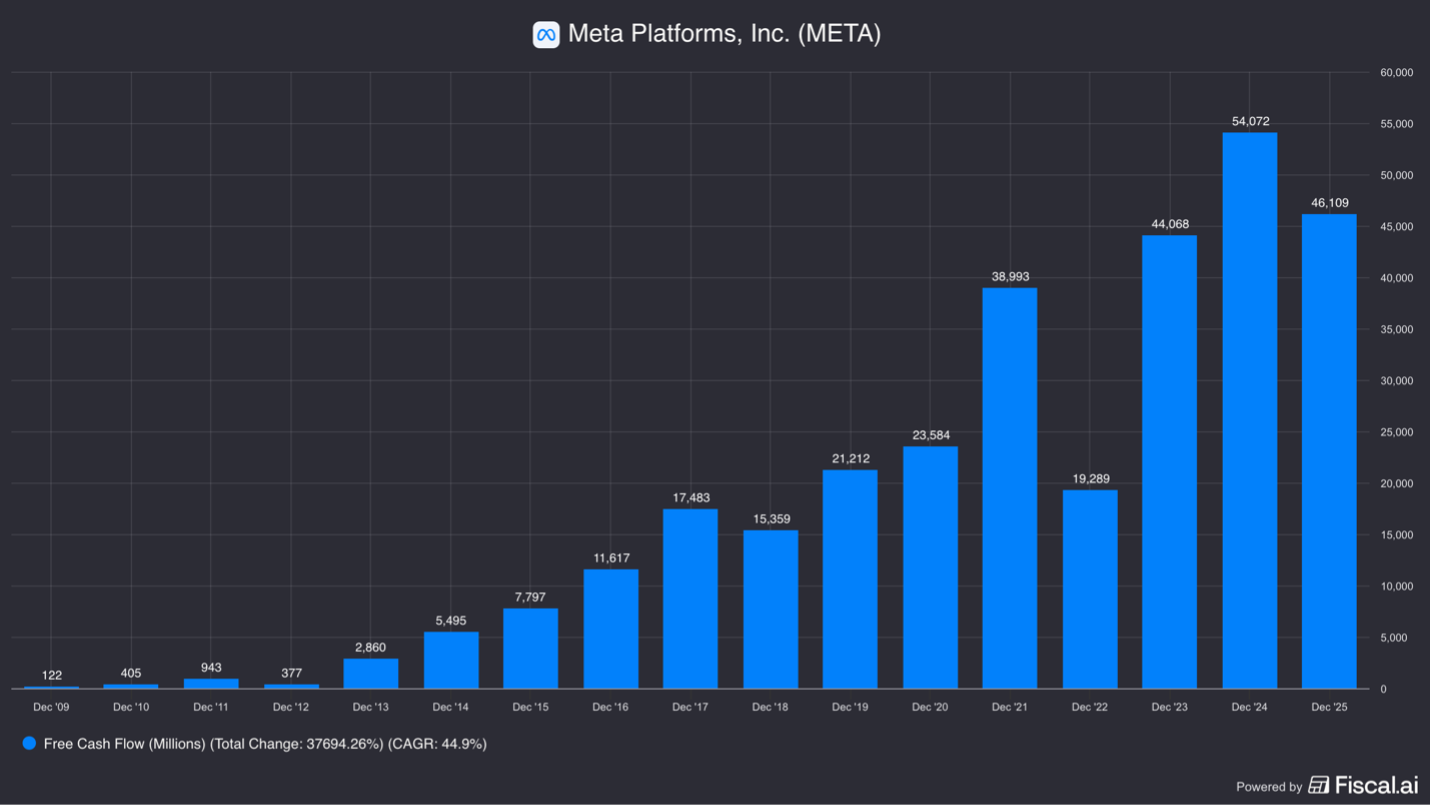

Cash Flow Gone.

The counterargument centers on capital intensity.

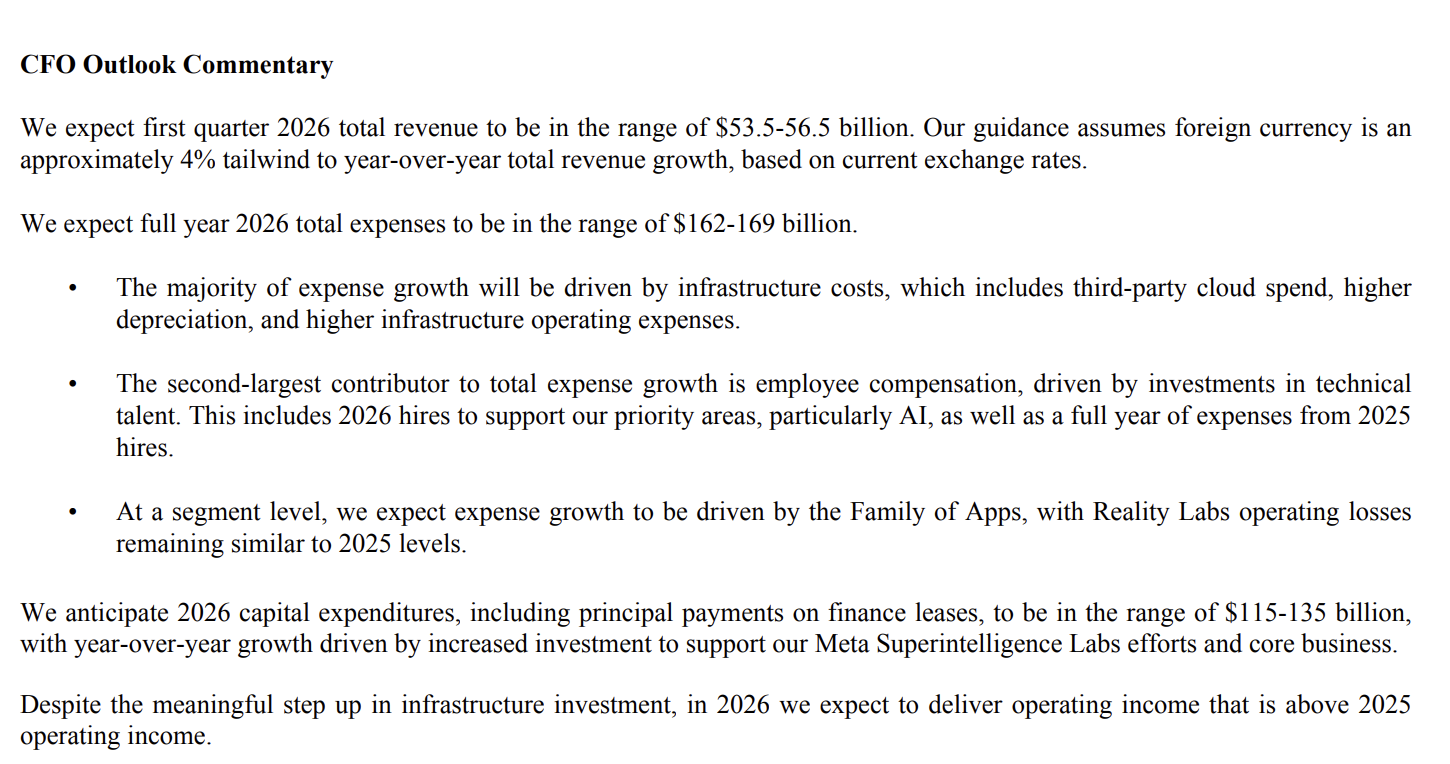

Meta expects capital expenditures to reach approximately $135 billion next year, largely directed toward AI infrastructure—data centers, advanced GPUs, networking, and related capacity.

At that level of spending, free cash flow could approach zero and potentially turn negative for the first time in the company’s public history.

This marks a sharp departure from Meta’s historical profile.

Free cash flow conversion once exceeded 100% of net income.

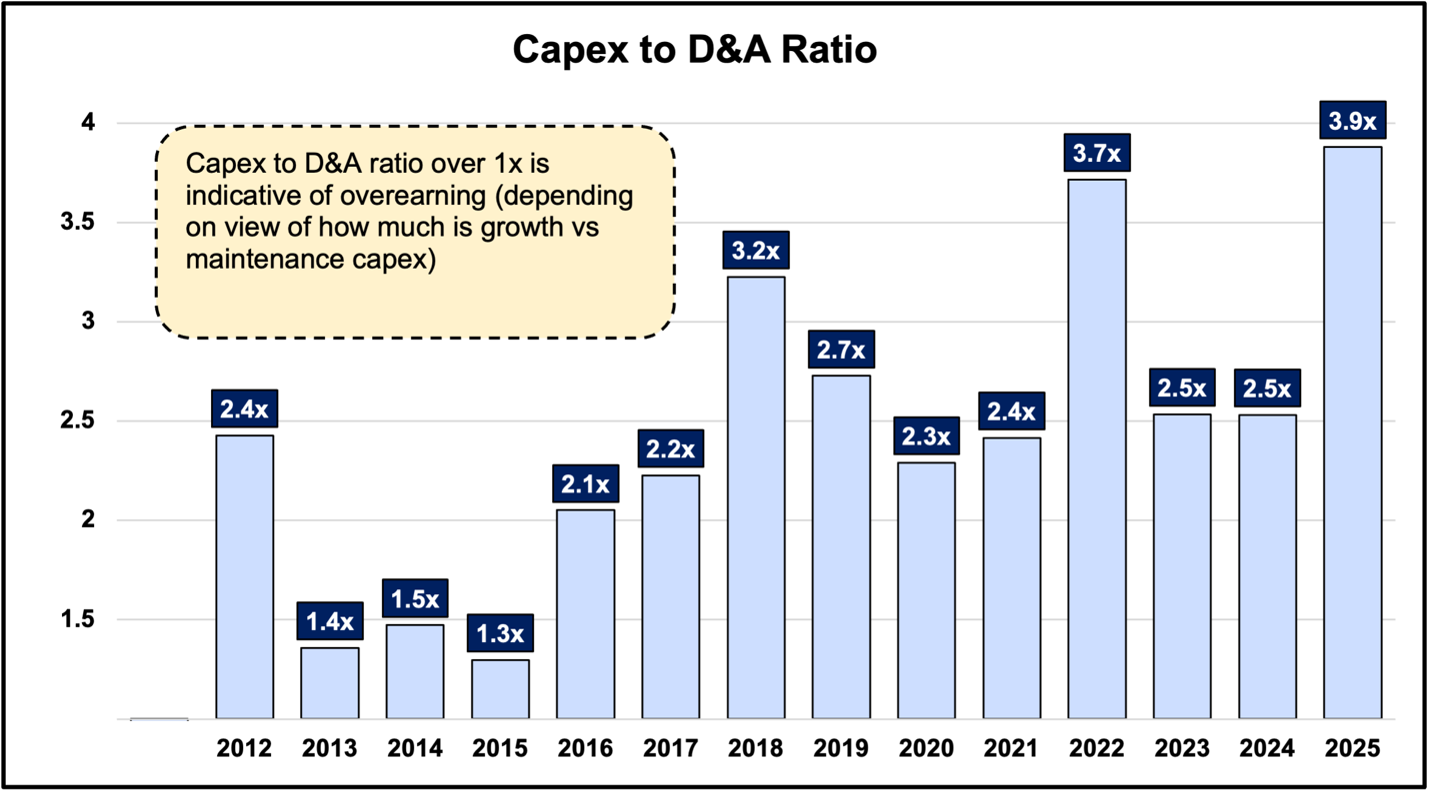

It has since declined materially as capex have run well ahead of depreciation.

For every dollar of depreciation currently recorded, 4 dollars of new capital are being deployed.

That dynamic implies higher future depreciation expense, which will result in an earnings headwind as capex works through the P&L

Time Spent War.

Meta’s product strategy has also evolved.

The company is less focused on facilitating social interaction between friends and more oriented toward maximizing time spent across its applications.

That distinction matters.

Competing as a social network is narrower than competing for attention against short-form video, streaming platforms, gaming, and emerging AI-native experiences.

In effect, Meta is now in the broader “time spent” market.

That widens the competitive field and increases the importance of algorithmic relevance.

YouTube, Netflix, and potentially AI generated content are all competitors to user’s time.

In a recent interview, Sam Altman made the distinction between ChatGPT and social media in terms of user experience, where he said...

“In Meta, people think ChatGPT as like a Facebook replacement because people are just spending all their time talking to it and they like it more like a source and attention.

People like doom scrolling on the internet feels like it’s making you worse. It may feel good in the moment, but it’s making you feel worse, and when people talk about ChatGPT, they’re like, I like myself better. It’s like helping me accomplish my goals.”

Despite management stating time spent on Meta apps are increasing, one question that should be asked; will people spend more time on LLMs than social media?

We will cover what this means for Meta later, but first we need to understand how they make money.

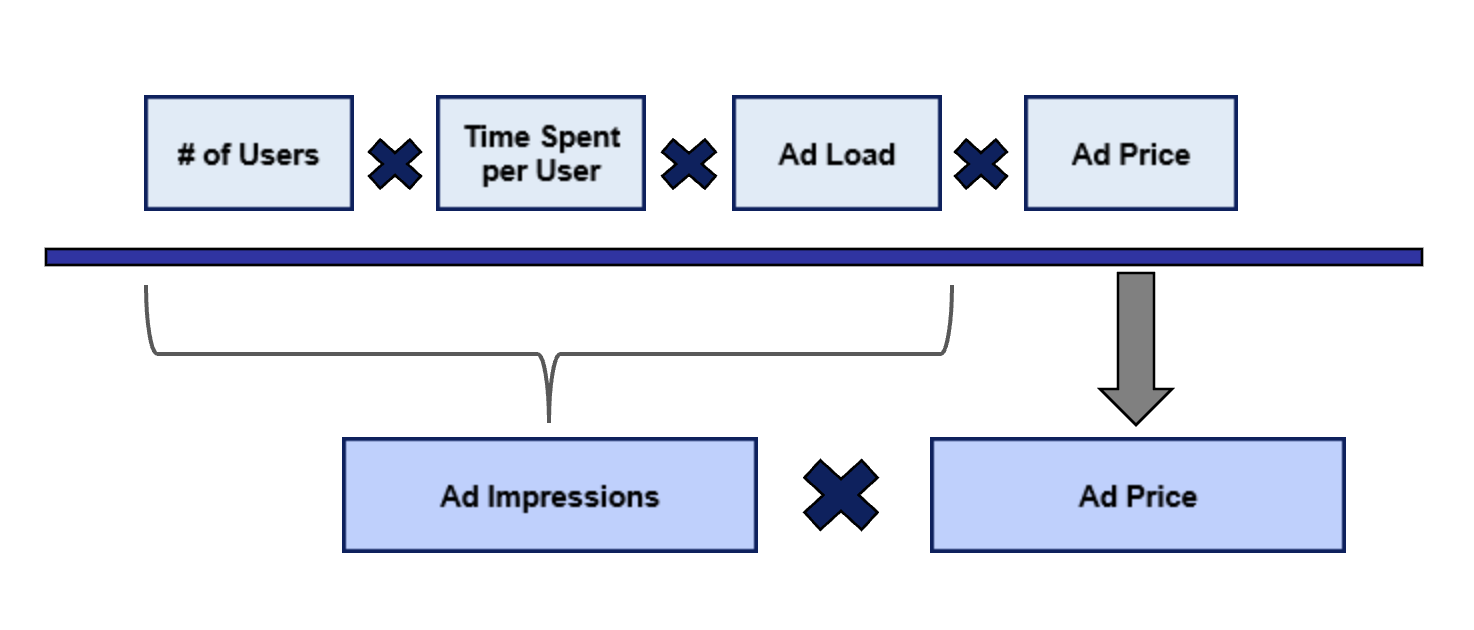

Understanding the Advertising Engine.

Meta’s core economics remain rooted in advertising auctions.

The company does not directly set ad prices.

Instead, revenue is driven by four primary variables:

1. User growth

2. Time spent

3. Ad load

4. Ad prices

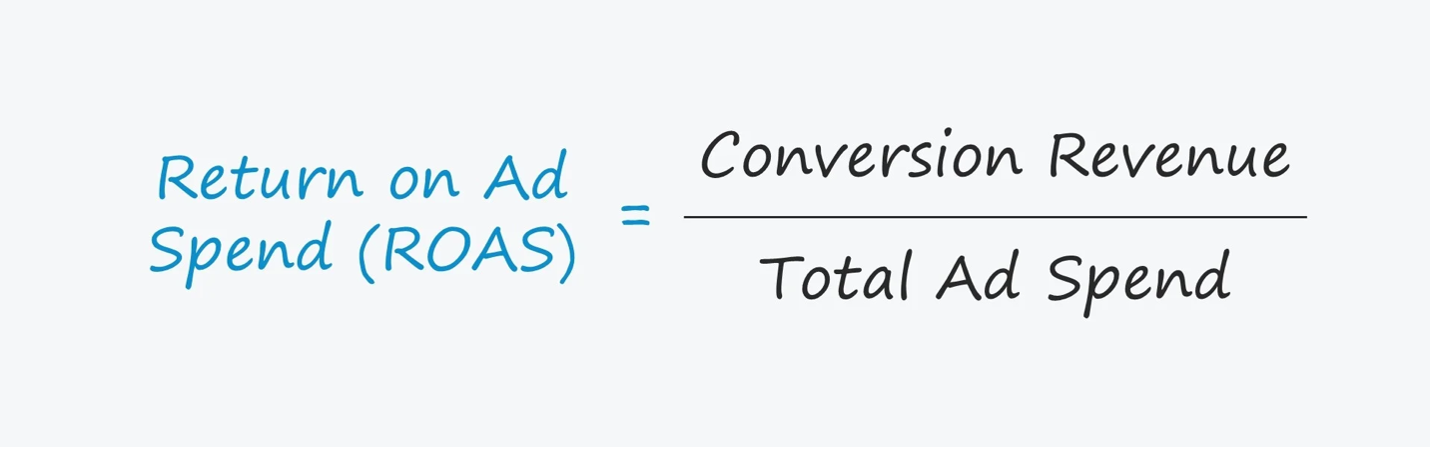

The auction model depends on advertiser return on ad spend (ROAS).

As long as advertisers can generate attractive returns, they will continue to spend on advertising.

Meta’s AI investments are designed to enhance targeting precision and attribution accuracy, thereby improving ROAS and encouraging greater advertiser participation.

Scale is critical here.

With more than 10 million advertisers, Meta benefits from bid density, multiple bidders competing for each impression, supporting pricing resilience.

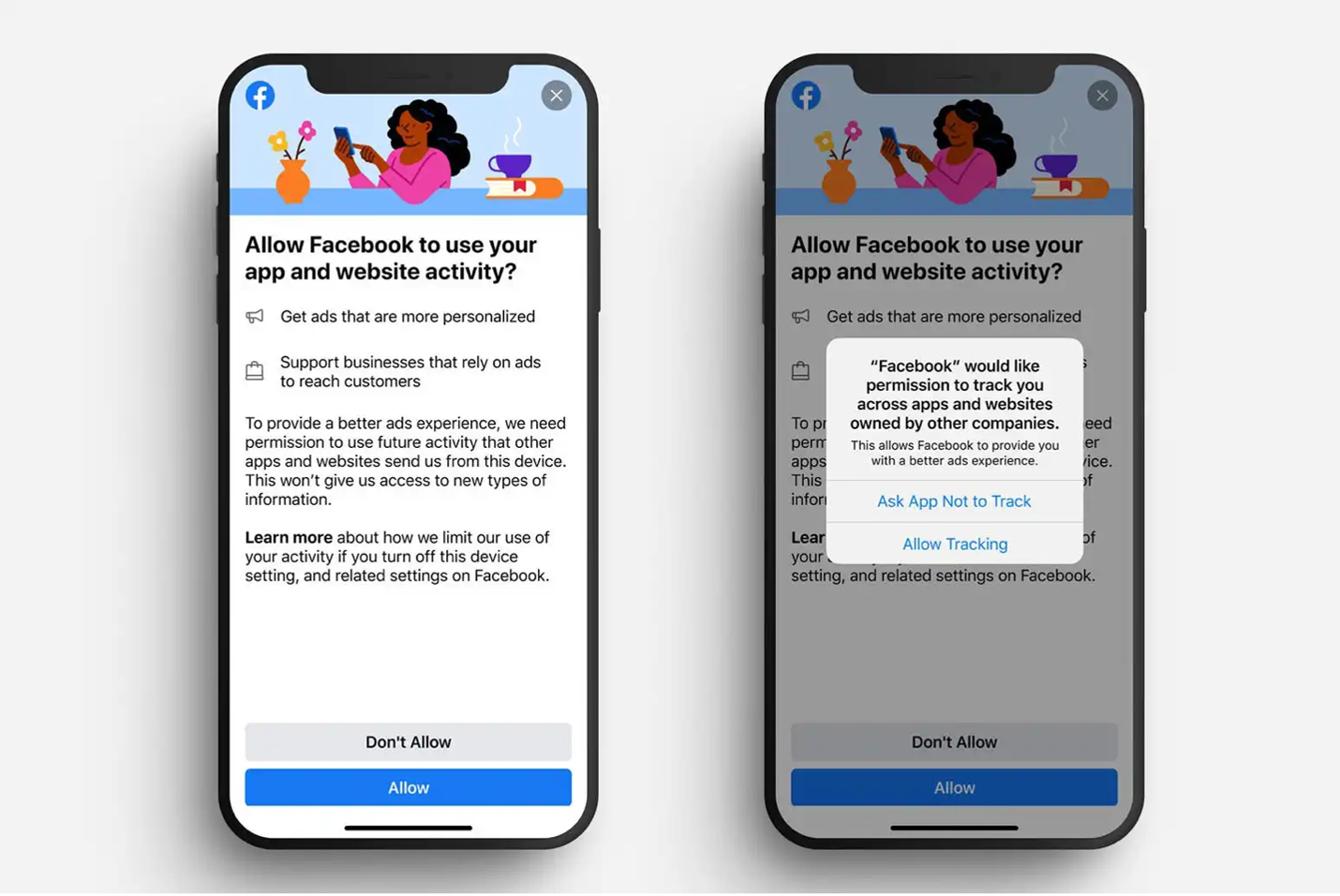

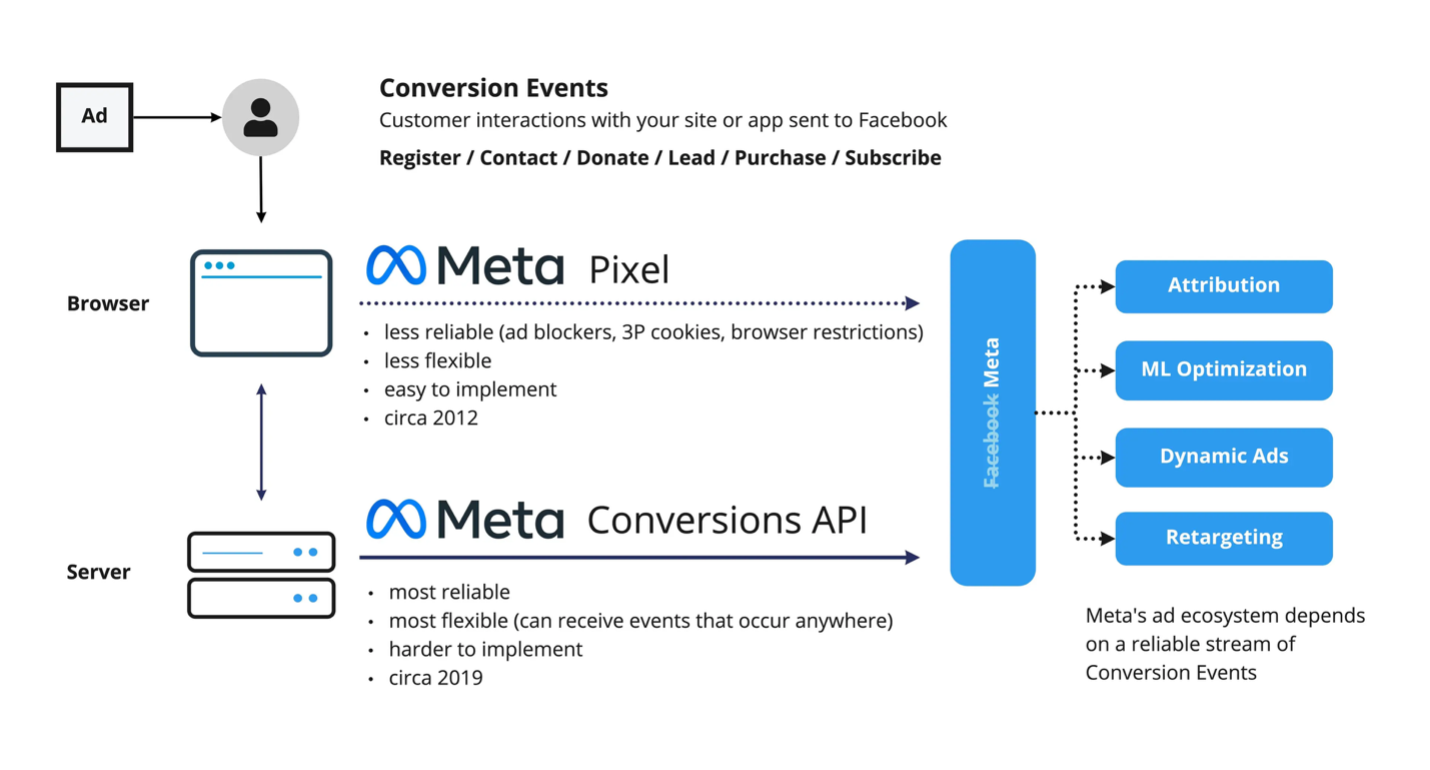

However, the vulnerability of this model was exposed in 2022 when Apple’s App Tracking Transparency (ATT) restricted access to device-level identifiers.

That reduced signal quality and impaired attribution, leading to Meta’s first revenue contraction as a public company.

Meta responded by investing in server-side conversion tools and deeper integration with advertisers’ backend systems with a tool called CAPI.

The recovery since then underscores both the fragility and adaptability of the model.

Platform dependence remains a structural risk.

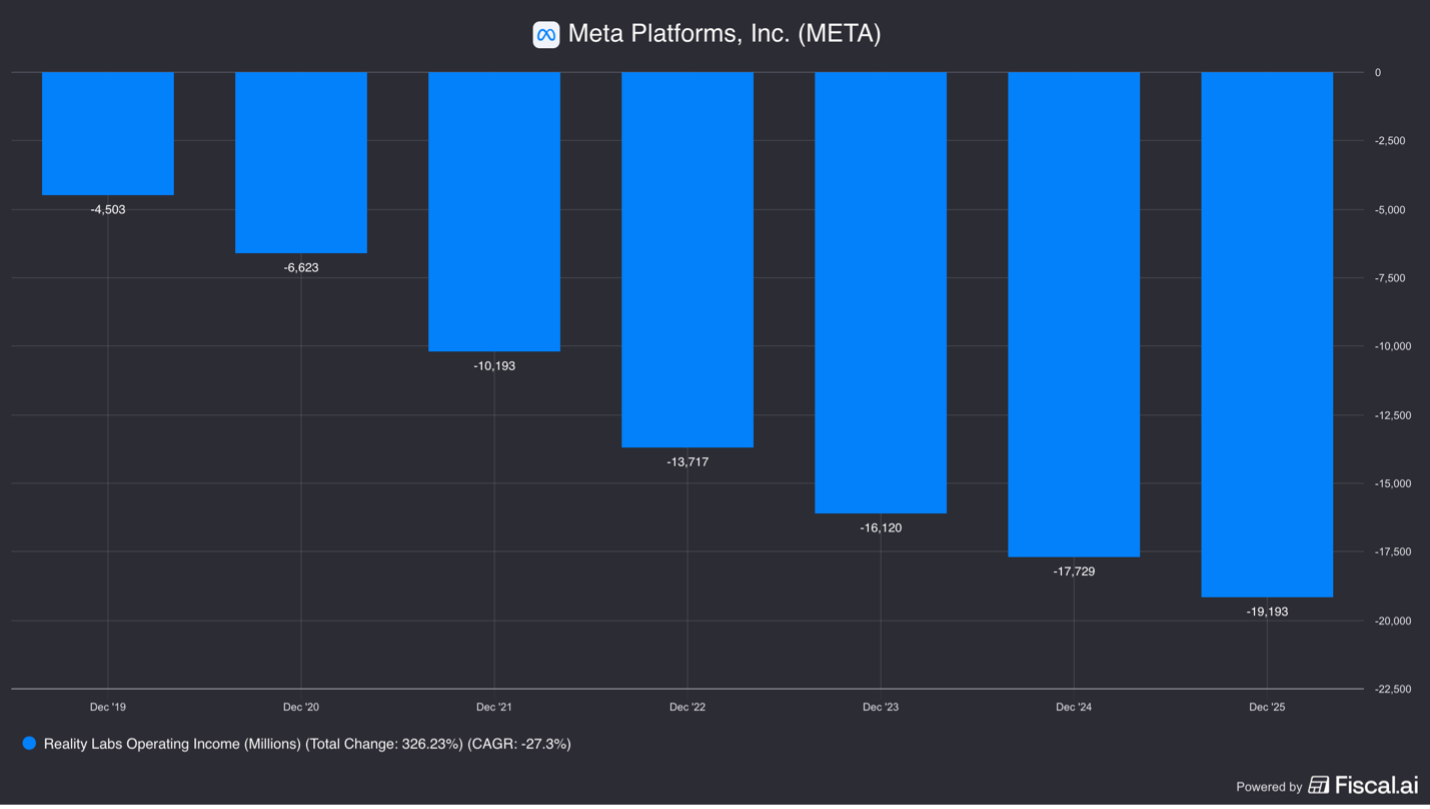

Reality Labs.

Meta’s Reality Labs segment continues to generate multi-billion-dollar annual losses.

The rationale traces back to an earlier strategic shock: the transition from desktop to mobile.

During that shift, platform owners controlled distribution and economics, limiting Facebook’s developer ecosystem ambitions.

Mark Zuckerberg views AI and immersive computing as potential platform shifts.

Owning the next interface layer, whether through AR glasses or proprietary AI models, reduces dependence on third-party gatekeepers like Apple and Google.

From that perspective, current spending is defensive as much as opportunistic.

However, cumulative investment in Reality Labs now exceeds $100 billion.

The longer monetization remains elusive, the more challenging it becomes to justify the return on invested capital.

On the call, they did note that Reality Labs has peaked and losses in this segment will start to revert.

Investors are effectively underwriting a long-duration call option.

AI.

AI spending serves two purposes.

First, it enhances the core ad engine through better targeting and generative ad creation tools.

Better targeting and attrition means users spend more time on their apps, while advertisers earn higher return on ad spend.

Second, it positions Meta to compete in user-facing AI applications.

Management has described AI as existential.

If generative AI becomes a dominant consumption interface, Meta cannot afford to be disintermediated.

As a result, the company is investing aggressively in proprietary models and top-tier AI talent to create “Super Intelligence”.

Alexandr Wang, Meta's Chief AI Officer

This ambition comes with operating leverage risk.

Management expects operating expenses to grow faster at than revenue in the near term, implying margin compression even amid strong top-line growth.

Maintenance vs. Growth Capex.

A central analytical question is how much of Meta’s capital spending represents maintenance versus growth investment.

If most of the $135 billion in capex is growth-oriented, it can theoretically be moderated in future years, allowing free cash flow to rebound.

If instead a large portion becomes structurally necessary to sustain ad performance and AI competitiveness, capital intensity may remain elevated.

Assuming revenue grows approximately 30% and incremental margins remain robust, the implied return on incremental capital appears attractive.

Even with conservative assumptions, the return on invested capital may exceed mid-teens percentages.

However, that outcome depends on sustained revenue expansion and disciplined deployment.

Valuation.

At $655 per share and a market capitalization near $1.6 trillion, Meta generated approximately $200 billion in revenue last year and over $80 billion in operating income.

If we assume revenues grow 30% next year, revenues will be $260bn.

If we take their opex guidance of $165bn, operating income falls to $95bn.

If we apply tax (20%) and divide by the number of shares outstanding, we get ~$29 in EPS.

Which results in 22x earnings.

If we adjust out the Reality Labs losses, we get to around $35 in EPS.

This drops the multiple to ~18x earnings.

It is important to note that we are not valuing Reality Labs at all.

We are assuming it is not a net-negative value to the business.

If Reality Labs does become a positive value to the business, that could be another source of upside here, plus whatever they figure out with AI long term.

But an investor should be aware of some key risks…

Key Risks.

There are 7 key risks an investor has to understand.

1. Worse Margin Compression: Expenses are growing faster than revenue in the near term. A revenue shortfall would result in worse margin compression.

2. Revenue Growth Durability: Even though Meta is seeing benefits from AI and are expected to grow revenues 30%+ next year, how durable is that growth? How long will this growth last?

3. AI Targeting Blackbox: We don’t know the limits of the AI targeting and ad model will be. Will the AI targeting stop improving? If so, we won’t know when it will and when it does it could happen suddenly.

4. Platform Shift: Meta could be hit by a platform change just as it did before with the shift to mobile.

5. Apple Ad Tech Change: Apple could change its ad tech or contractually enforce the ability to not collect user data on the backend.

6. Drop in Ad Budgets: Advertising remains economically cyclical, though direct-response formats are more resilient than brand advertising.

7. AI Content: AI is so good at serving up content and users are glued to their phone since the content is made specific for them, and the AI content is not Meta’s.

Meta presents a complex profile...

A dominant, high-margin advertising platform enhanced by AI, coupled with an aggressive capital deployment strategy aimed at controlling future computing interfaces.

The stock’s relative valuation reflects that tradeoff.

Investors are being asked to exchange near-term free cash flow for long-term strategic positioning.

Whether that exchange proves attractive depends less on next quarter’s growth rate and more on the durability of Meta’s competitive advantage in an AI-driven landscape.

But that is on you as an investor to decide if this is an opportunity or not.

For more on Meta, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.