I Set Price Targets at Goldman Sachs — They're Not What You Think

Get smarter on investing, business, and personal finance in 5 minutes.

Every so often, a headline flashes across CNBC or Yahoo Finance:

“Analyst raises price target on Netflix to $650.”

The stock ticks higher. Commentators nod. Retail investors take it as validation.

It sounds simple. Almost authoritative.

But very few investors actually understand what that price target means...

Because it is NOT a valuation

It also is not designed to help a retail investor know whether or not they should own a stock.

You need to know how these price targets are built and what their true purpose is before you mistakenly take it for free advice or even an opinion from a knowledgeable analyst.

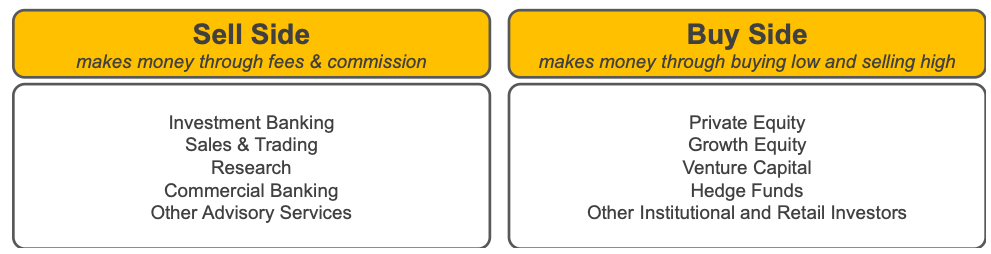

Sell-Side vs Buy-Side.

Sell-side equity research, a core function within major investment banks such as Goldman Sachs, plays a central role in shaping how public markets interpret corporate performance.

Its most visible output—price targets and stock ratings—is widely cited across financial media and often treated by retail investors as a proxy for intrinsic value.

In practice, these metrics are better understood as products of institutional structure, incentives, and relative positioning rather than standalone valuation conclusions.

At a high level, the distinction between the sell side and the buy side defines the framework.

Sell-side institutions, including global investment banks, generate revenue by underwriting securities, facilitating transactions, and providing research.

Buy-side firms—such as asset managers, hedge funds, and pension funds—consume this research as inputs into capital allocation decisions.

Price targets and ratings are therefore not designed in isolation; they are embedded within a broader ecosystem intended to support client activity and engagement.

Historically, the objectivity of sell-side research has been shaped by regulatory intervention.

The Global Settlement.

Prior to the Global Analyst Research Settlement in 2003, research departments operated in close coordination with investment banking divisions.

Analysts were, in some cases, directly incentivized through deal-related compensation, creating clear conflicts of interest.

For example, Henry Blodget, he is famous if not infamous, for during the tech bubble, having a lot of very positive ratings on a lot of different stocks that he would call in private emails as “P.O.Ss.”

And the reason why he would have a different public rating and what he would say publicly versus what he would say privately is because of the pressure from the investment bank to say something publicly on a company that is their client and they're collecting fees from.

At the time, the investment bank was also allowed to actually give a portion of these fees to the research analysts. So, research analysts at this point in time, some of them were making $10-15 million plus a year.

So that was a lot of money for a research analyst to be making and all they had to do was to say something positive.

As Charlie Munger always says, show me the incentives and I'll show you the outcome.

The outcome of this was a lot of these analysts were saying very positive things on companies that maybe were big bankruptcy risks.

Then in 2003 came the Global Analyst Research Settlement.

The settlement introduced formal separation like a “firewall”, between research and banking functions, limiting direct financial ties and restricting communication channels.

While this reduced explicit conflicts, it did not eliminate the structural incentives that continue to influence analyst behavior.

The 4 Influences of Price Targets.

Four factors remain particularly relevant in understanding how price targets are formed.

1. Career Risk

2. Corporate Access

3. Marketing/Building a Reputation

4. Influence From Client Compensation

Let’s break down each of these one by one.

Career Risk.

First, career risk continues to shape analyst output.

Even in a post-settlement environment, analysts operate within large institutions where maintaining internal relationships and advancing professionally requires a degree of alignment with broader organizational priorities.

This can lead to more measured or incremental deviations from consensus, rather than sharply contrarian views.

Corporate Access.

Corporate access represents a key component of the research value proposition.

Analysts facilitate meetings between institutional investors and company management teams, including CEOs and CFOs. Maintaining this access is critical.

Negative or overly critical coverage risks limiting engagement from corporate executives, which in turn reduces the analyst’s utility to clients.

As a result, research coverage tends to skew constructive, with downside risks often framed more cautiously.

Building a Reputation.

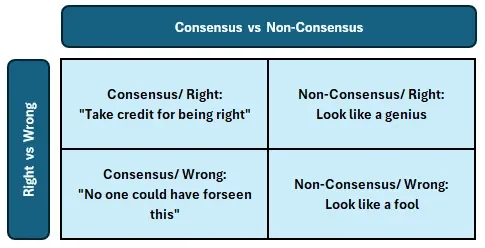

Reputational considerations influence how far analysts deviate from consensus estimates.

Let’s look at the chart below to explain this further.

Whenever an analyst makes a call that is out of consensus, they're sticking their neck on the line and potentially their job and career.

Publishing a materially divergent view introduces asymmetric career outcomes: being wrong while out of consensus can damage credibility, whereas being wrong within consensus carries limited reputational cost.

If you are going to come out with a call that is non-consensus, then you better be right.

And if you're right, then you could really kind of build your career on that.

Adam Jonas, who was very bullish and vocally bullish on Tesla for a long period of time, that kind of built his career by being out of consensus and very vocal on that, but then also being right because, the stock ultimately did go up a lot.

So that is one way a sell side analyst can kind of build their career, but they're going to be very careful on the kind of calls and the times when they want to do that, and 90% of the time you're going to just want to be in consensus and not stick your neck out.

You're not going to want to take 20 different opinions on everything.

You're going to want to take one opinion on one thing that you feel really strongly on.

So this is part of the reason why you can't always get this great, honest, independent opinion because it could potentially go against their career incentives.

If they stick their neck out, say what they think, but they're not that confident and they're wrong, and so instead, what ends up happening is these analysts will actually look at what consensus is and they'll cluster their estimates to where consensus is.

Part of this is anchoring bias. The consensus becomes the anchor.

This dynamic creates a feedback loop in which published estimates both inform and are informed by peer expectations.

Influence From Client Compensation.

Finally, client-driven compensation mechanisms introduce another layer of influence.

Institutional clients—particularly hedge funds—frequently evaluate research providers through broker voting systems, which can affect analyst compensation.

These evaluations are not purely objective; they may reflect alignment with client positioning or the perceived usefulness of research in supporting existing investment theses.

As a result, analysts face subtle incentives to produce work that resonates with their audience.

Price Targets Are a Pricing, Not a Valuation.

Against this backdrop, the construction of a price target becomes more contextual.

Contrary to common perception, a price target is not a direct statement of intrinsic value.

Instead, it typically reflects a forward-looking estimate of where a stock may trade over a defined horizon—most often 12 months—based on applying a selected valuation multiple to projected earnings or other financial metrics.

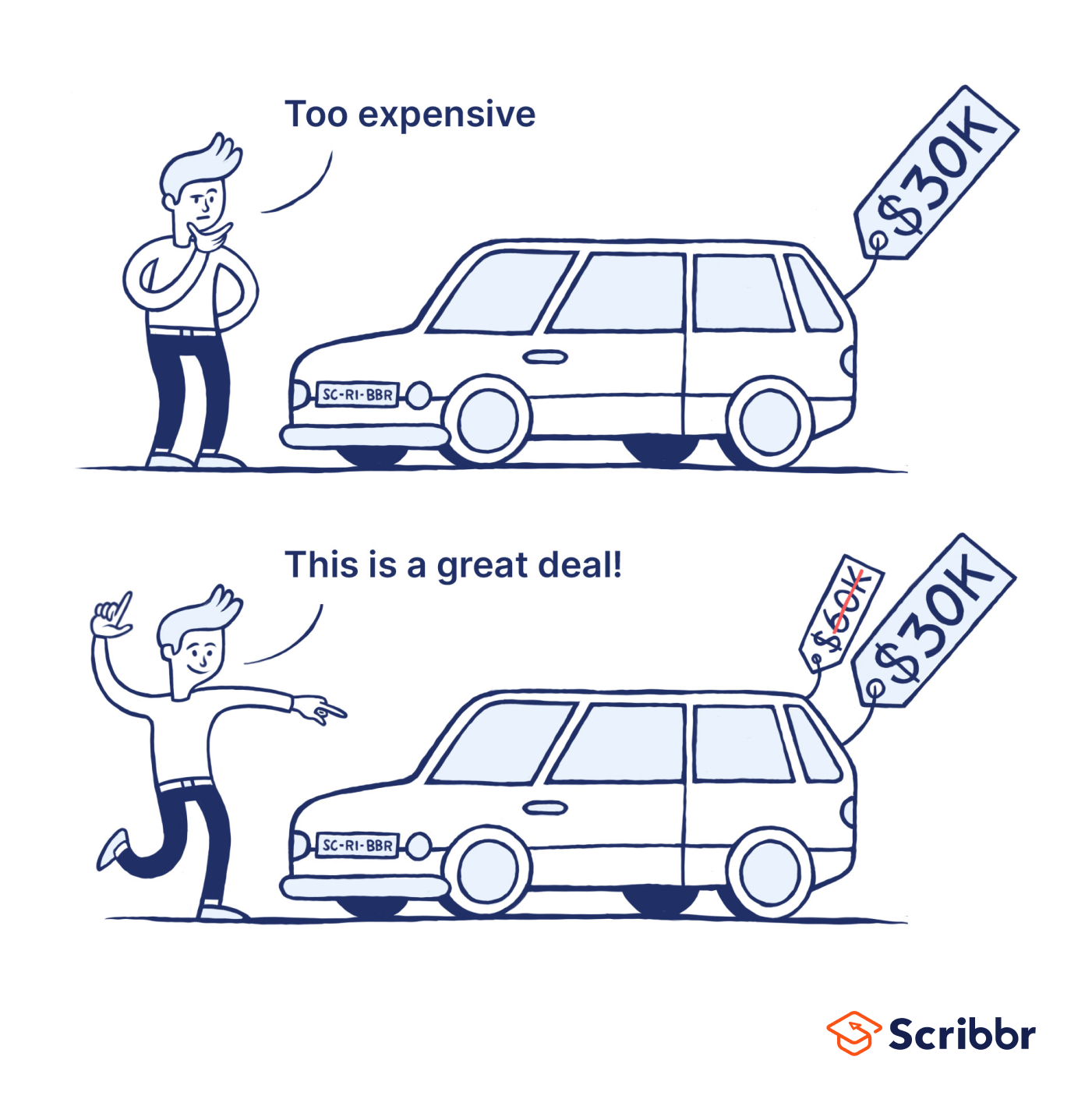

Let’s say a stock is trading at $90.

A sell-side analyst publishes a $120 price target.

On the surface, that looks simple:

$90 → $120 = 33% upside.

So the instinct is to think: “Okay, they think this stock will return 33% over the next year.”

But that’s where the interpretation starts to drift away from how valuation actually works.

Now step back and think about how most investors value a stock.

You might build a DCF model.

Or more simply, a reverse DCF.

That reverse DCF is really just asking:

“What return does the current price imply if my assumptions are correct?”

And that return is your discount rate.

Most models break that discount rate into two parts:

Risk-free rate + Equity risk premium

The risk-free rate is usually tied to government bonds. Let’s say that’s around 4%.

Then you add the extra return you demand for taking equity risk. Maybe 5%.

So in total:

4% + 5% = 9% expected return

That 9% is basically what the market is implying you earn per year for holding the stock, given current pricing and assumptions.

So far, everything is internally consistent.

But how did the analyst get the 33% upside?

If you try to defend the price target intellectually, the closest explanation looks like this:

The analyst is implicitly saying the stock is mispriced relative to a “fair” required return.

In other words:

Right now, the implied discount rate might be too high.

Maybe instead of a 9% expected return, the stock is effectively priced to deliver something like 11%.

That suggests the stock is “too cheap” relative to what they think is fair.

So in order for the market to reprice the stock, it has to rise.

And if it rises enough—say 33%—then the implied return compresses back down to something like 9%.

This framework inherently emphasizes pricing rather than valuation, as it incorporates assumptions about future market sentiment and multiple expansion or contraction.

Price Targets are “Relative”

Equally important, stock ratings—buy, hold, or sell—are relative within an analyst’s coverage universe.

For example, an analyst covering the automotive sector may assign a “buy” rating to one company and a “sell” rating to another, not because the latter is expected to decline in absolute terms, but because it is less attractive relative to peers.

This relative framework is particularly relevant for hedge funds employing long-short strategies like a pair trade, where the objective is to identify outperformers and underperformers within a defined sector.

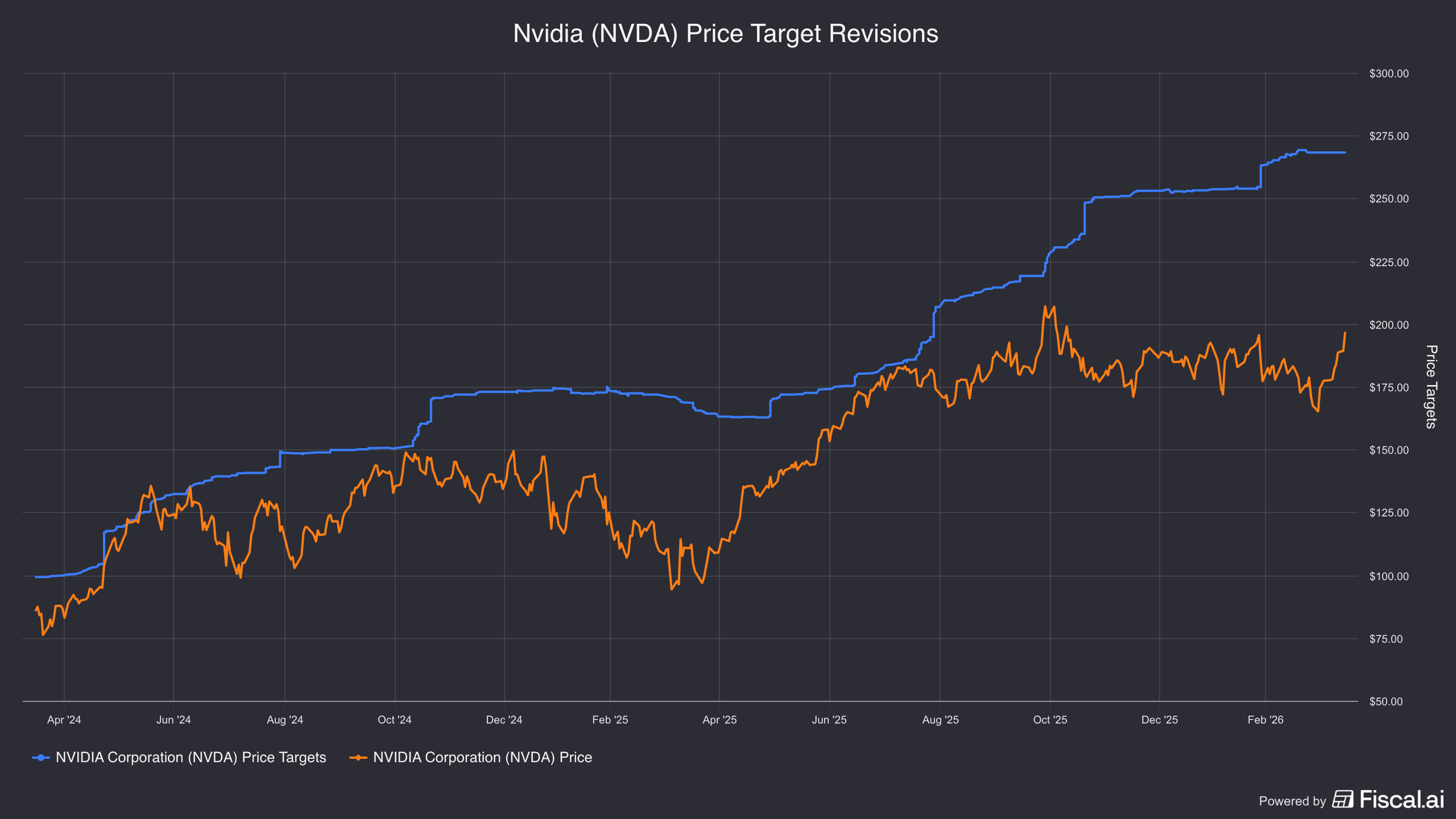

This structure also helps explain why price targets often move in tandem with stock prices.

Maintaining a given rating requires preserving a certain implied level of upside or downside.

As prices change, targets are adjusted accordingly to sustain that relationship.

The result is a system where price targets can appear reactive rather than predictive, reflecting shifts in positioning and relative attractiveness rather than independent reassessments of intrinsic value.

So when a retail investor hears a price target on CNBC or some news channel, “Oh, Netflix is a $100 a share and it's a price target of $150” and they go out and buy it, they were totally missing all of these other incentives that were going into the price target that we're influencing it.

Now you understand what price targets are.

Hopefully you will never be convinced or dissuaded or persuaded by a sell side analyst talking about them upgrading a stock to a certain price target.

You could listen to their arguments and maybe their estimates too, but not the actual price target itself or the rating without taking into account everything else we mentioned already.

The big theme here too is understanding that just because someone works on Wall Street, and they might have a prestigious title they don't really know that much more or if anything, more than an individual investor.

In fact, often because of all these perverse incentives that we talked about, they’re actually worse off because all of those biases that influences them in negative ways.

Lucky for the investor though you have an easy solution: ignore them.

For more on Sell-Side Price Targets, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.