You’re Focused on the Wrong Thing When Building Wealth

Get smarter on investing, business, and personal finance in 5 minutes.

Today’s Five Minute Money was adopted from a recent video and thus it may read more like an edited transcript.

There are three aspects to building long-term sustainable wealth that investors need to be aware of.

They are all simple, but it is a matter or actually doing them in a systematic process over time.

I know I talk a lot about picking stocks and a lot of individual companies and we talk about different questions an investor will face, but there's a lot easier ways to kind of set yourself up for success in terms of wealth, which I think is what we are all here trying to do, is to have more money in the future than we have currently.

And you don't need to know whether or not Vantage score is going to win out against FICO or Reddit is going to build a self-serve ad platform.

These questions while interesting to think about and you know, certainly questions that need to be answered if you want to invest in those names, they're not necessary to have more money in the future.

There are easier things.

Because if you are picking a portfolio of stocks and managing money yourself, there's a lot of other aspects that you need to consider beforehand that are going to impact your financial future to a larger extent than you know, potentially whether or not one stock's going to be a three bagger, a 10 bagger, or go down 50%.

There are three aspects of money management that need to work together in order to build wealth and have a secure financial foundation.

1. Financial Planning

2. Wealth Management (Asset Allocation)

3. Investment Management (Investment Selection)

While many focus on the last one, all three are needed because each work together hand in hand.

We will discuss of this in this week’s Five Minute Money!

Financial Planning.

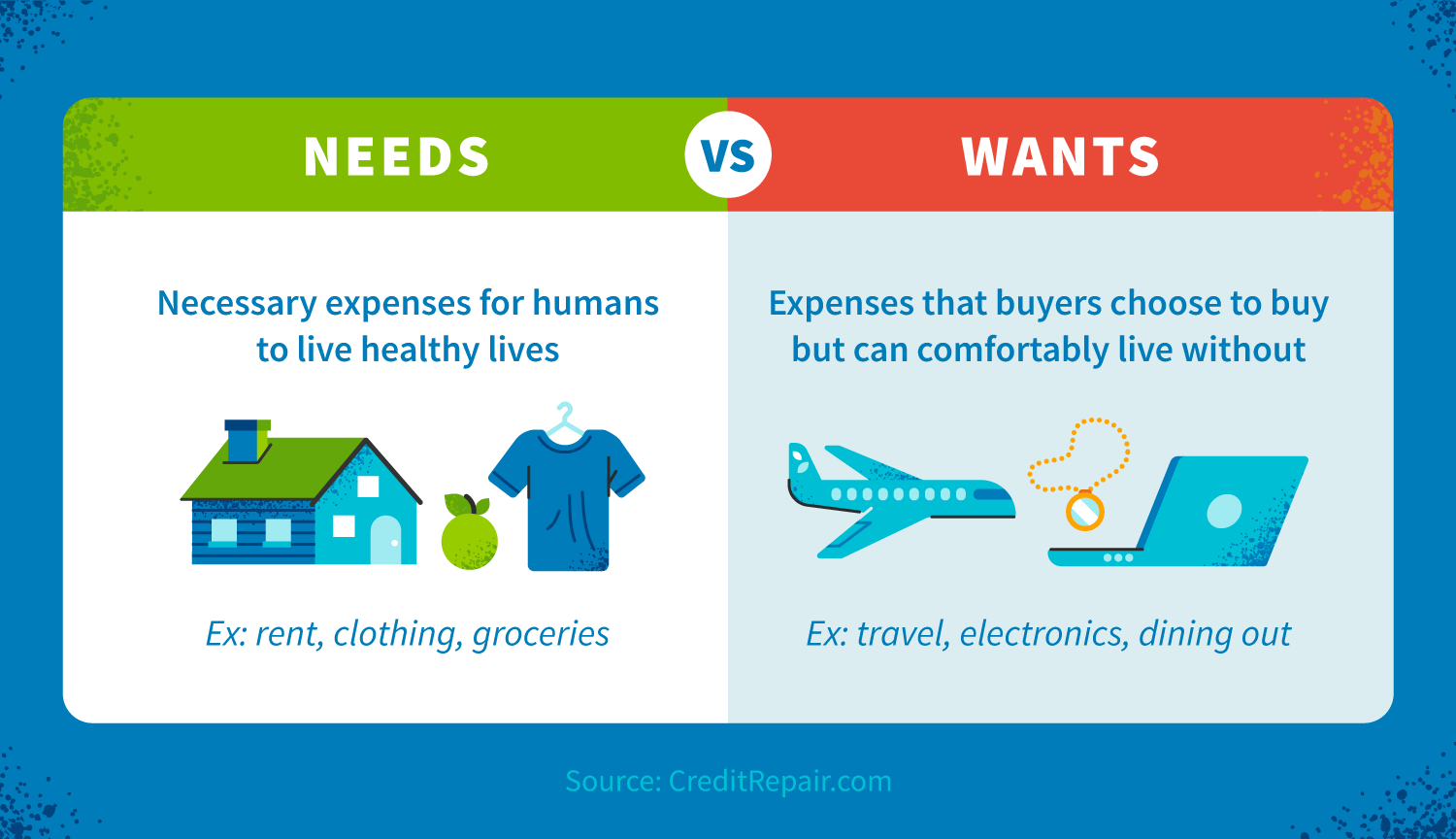

At a high level, what you should know is the difference between your essential and your non-essential expenses.

The reason why this is important is because when times are tough - you lose a job, there’s a really bad recession, it will allow you to know what your “burn rate” is on your own P&L.

You want to think of yourself as a business.

What would your profit and loss statement look like. Your cashflow statement, your balance sheet?

Just like a business that has growth expenses and maintenance expenses, there are expenses that you don’t want to cut.

These maintenance expenses are your essential expenses.

This is your rent, food, education etc.

A non-essential expense could be a $30,000 travel budget that you have.

If times get tough, you could cut that.

By understanding what your non-essential expenses are, that allows you to budget and understand what your emergency savings account should be.

Many people say you should have 3-6 months expenses in emergency savings.

However, if we think about this from first principles it depends on how much money you want to have and how much runway do you want to have in order to find that second job in order to start over if you need to.

You may want more than 6 months at least, especially if you have a family and other dependents that rely on you to bring money in.

There’s no right answer to this question, but I like to advise closer to a year in emergency savings.

When you’re calculating your emergency savings, I recommend you just do it on your essential expenses.

For example, you spend $100,000 in essential expenses a year.

You would want to have close to that amount or so in cash like a savings account or short term treasuries like T-bills.

You don’t want to take out duration on this because if you do, the value could potentially go down and you could have a loss there.

Now what should you do with the left over “profit” you have?

Well, if you are a good business, you invest that profit.

This is where wealth management comes in.

Wealth Management.

This involves making sure that the money you have is properly allocated into the right assets.

Said differently, we want to make sure the duration of our assets matches our cashflow needs.

Let’s say you are planning a wedding that will be in 5 years.

You put all that money in bonds and at the end of those 5 years, when you need that money, you get the money back.

Now the tricky part is most investments do not have an explicit date when they give you their money back, right?

If you’re invested in stocks, other than rare circumstances like a buyout offer, you don’t actually get back the principle amount of your stock and there’s no assurance you ever will.

It is like owning an open dated bond, and the only way you get liquidity from that is selling it in the secondary market, but you don’t know what price you will get for that in the future because we know that stock prices are very volatile.

So how much do you allocate to this asset class, where you don’t know when you’re going to get your money back?

Generally speaking, you don’t want to invest in the stock market unless you have a time horizon of 10 years.

That means, that the cash you invest in stocks is cash you don’t need until over 10 years into the future for some sort of purchase.

We will talk about the research that explains this later but what about the other asset classes that we could invest in besides equities?

First is bonds, which includes treasuries, corporate bonds, high yield bonds, junk bonds, private credit, etc.

The next asset class is alternatives which in includes everything from commodities, private equity, to real estate.

Let’s break each of these down one by one.

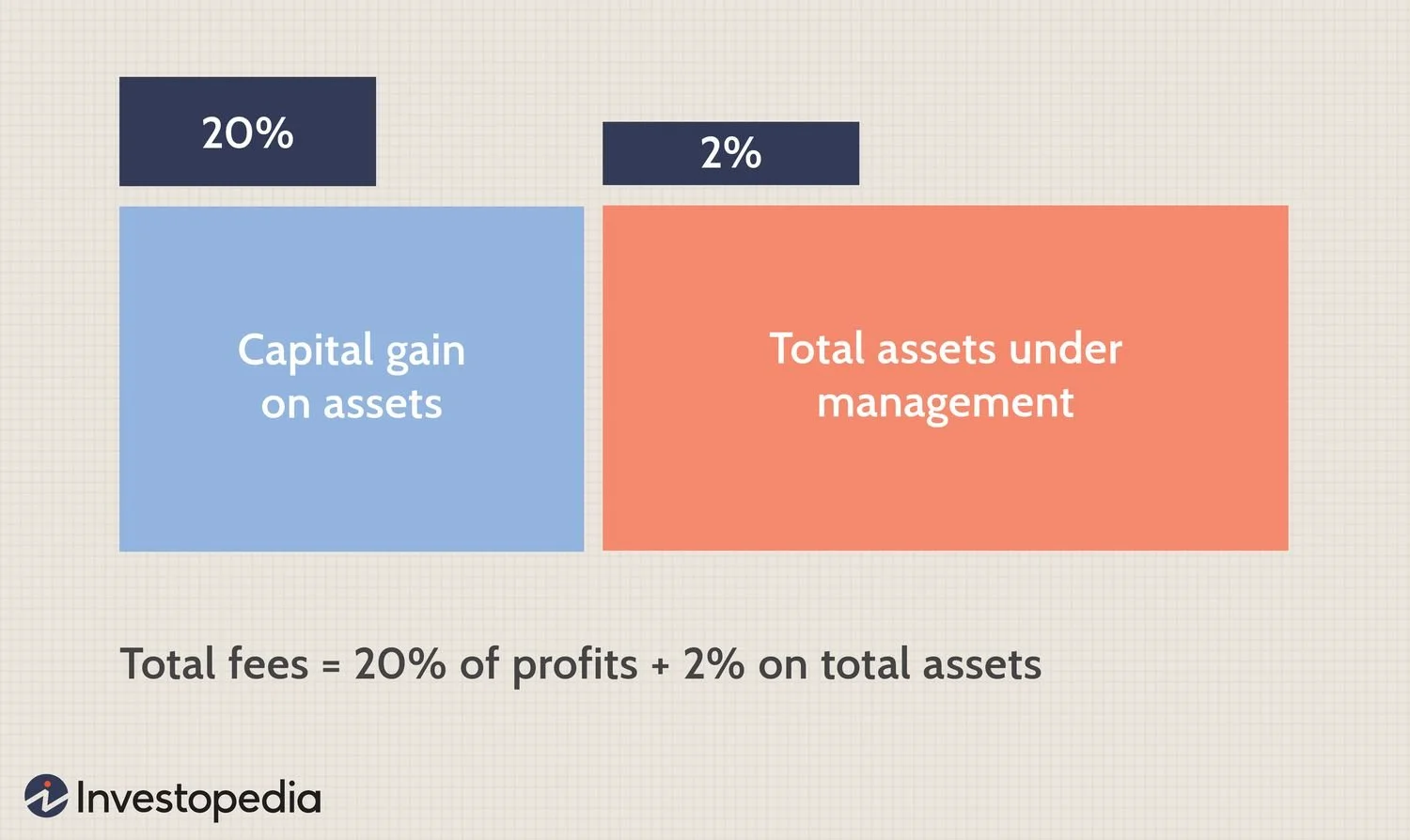

While private equity has the advantage of using leverage based on the underlying business cash flows, I’m not a huge fan of private equity generally because there’s really not a big difference between owning a company that’s public and private, as well as the fact of the layering of fees that they charge.

Usually these private equity funds have asset management fees where they charge a 2% for assets under management and 20% of profits as well.

In addition, these funds can take your money with a moment’s notice, which is called committing capital to a fund.

This means that if you committed $3 million into a private equity fund, the fund may not take it right then and there.

They may wait six months and maybe take $50,000 and then another $50,000 3 months later, then they wait and pull $100,000 when the market sold off, which could have been a great opportunity to buy stocks, but you can’t because you have this capital committed already.

In addition to capital commitments, the returns are “inflated” because they way they calculate the returns is based off of not when they capital was committed, but based off of when they received the capital.

So you could have money sit there that is not calculated in your return.

To add, many investors forget the fact that your money is locked up in these funds for 5 years, 7 years, 10 years, and a fund can extend that if they need to.

Now, if you want cashflow, real estate is the one of the best asset classes that you could get, but you have to be careful with how you get exposure to real estate.

You don’t want to directly own the property yourself because then you bought yourself a job.

And a lot of REITs (Real Estate Investment Trusts) have lots of fees and the returns get bid down so much.

However, there are tax advantages of owning real estate depending how you‘re owning it and if you want actual cash flow, real estate can be a good asset class to invest in.

Now, many investors get tripped up here where they think they need cash flow in order to live off of and their investments need to produce cash flow.

That’s not necessarily true, because if you own a stock that pays a 5% dividend but it’s a bad business in a declining industry conversely if you own a stock that doesn’t pay any dividend, but it’s continuing to reinvest all their money at very high rates of return, owning that second stock and selling a portion of it a year is better.

There’s usually a tax advantage here, depending whether or not it’s a qualified or unqualified dividend.

Qualified dividends will get a tax break on federal taxes, but som

So there’s a difference if it's a cash flow producing asset versus a capital appreciation asset.

If you do want to live off of cash flow, I do think real estate tends to be the best asset, because rents typically can be increased which can be an advantage if you own quality real estate properties.

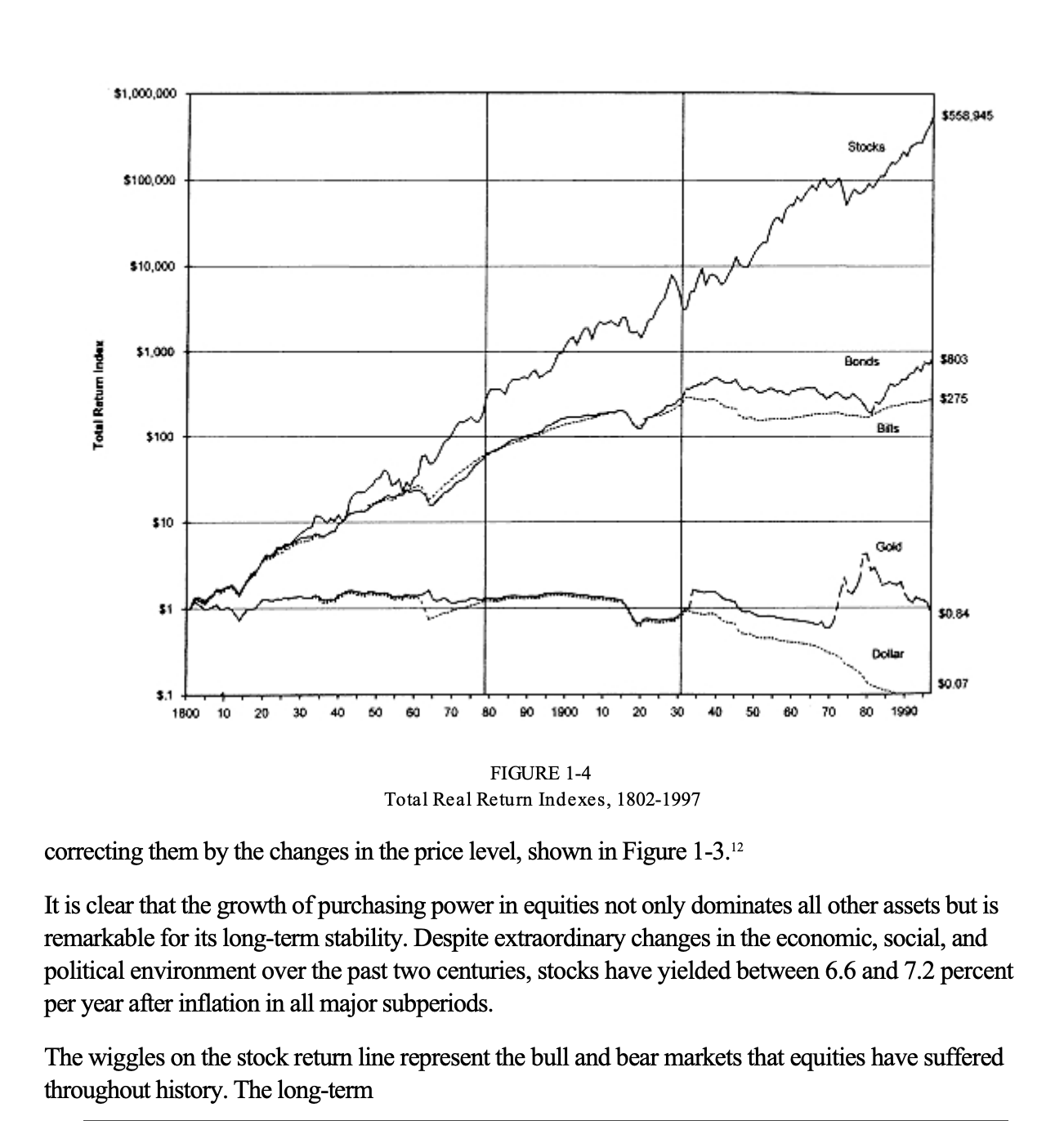

And since you’re getting a real return and you own a real asset instead of bonds, which during the Great Inflation of the 1970s, you would have over 20% of your money by being in bonds.

In the book, Stocks for the Long Run by Jeremy Siegel, he found that stocks in contrast to bonds over that same period, actually gain 2.6% in real terms.

So if you’re looking for income bonds can be a tough place to be in, since you could own a bond that has a 5% coupon, then all of a sudden inflation is 6% and that means you’re actually losing money every year you hold that bond.

Now, what about commodities?

Warren Buffet has said repeatedly said that he doesn’t want to own an asset that doesn’t produce anything.

Commodities like gold and cryptocurrency are just very speculative since there are no underlying cash flows it produces, which makes it hard to value it.

In addition, since it is very hard to value, you are hoping someone else in the future will pay a higher price for your asset.

That is a difficult game to play.

I can understand why people feel comfortable having a little bit of gold or silver exposure to sleep better at night, but it is a different game you are playing.

If we have a total societal meltdown, all of your securities could be worthless, money itself could be worthless.

The reason why investors choose to invest in these alternative assets like gold or Bitcoin, is the belief that they are a store of value in protection against inflation.

But what does history show over time?

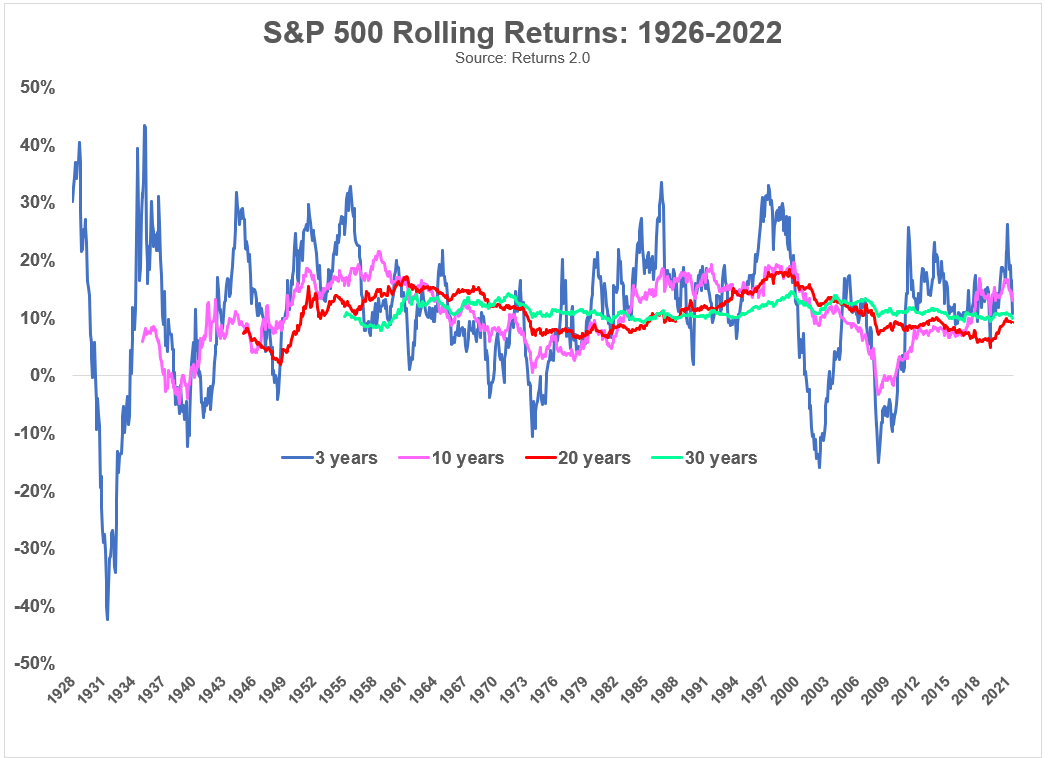

Time Horizon Matters.

As I mentioned earlier, if you don’t have a 10 year investment horizon for the cash you want to invest, and you need the money on a shorter term horizon, equities are not the right choice. Short-term bonds are probably the better choice.

Let’s say you have a kid that is going to college in 2 years.

You are going to need $70,000 for the next 4 years.

If you invest that money and in 2 years, the market sells off, that tuition bill becomes more expensive.

If you know you are going to need this money in a few years, risking it in the market could be a costly mistake because we know the market is volatile in the short term.

But if you have a long timeframe, equities makes the most sense.

Again drawing on Jeremy Siegel’s work, there’s been no 15 year period where stocks have not fully recovered, and no 20 year period where stocks have not been positive in real return.

So when people are worried about inflation, stocks are the best way to guard against it.

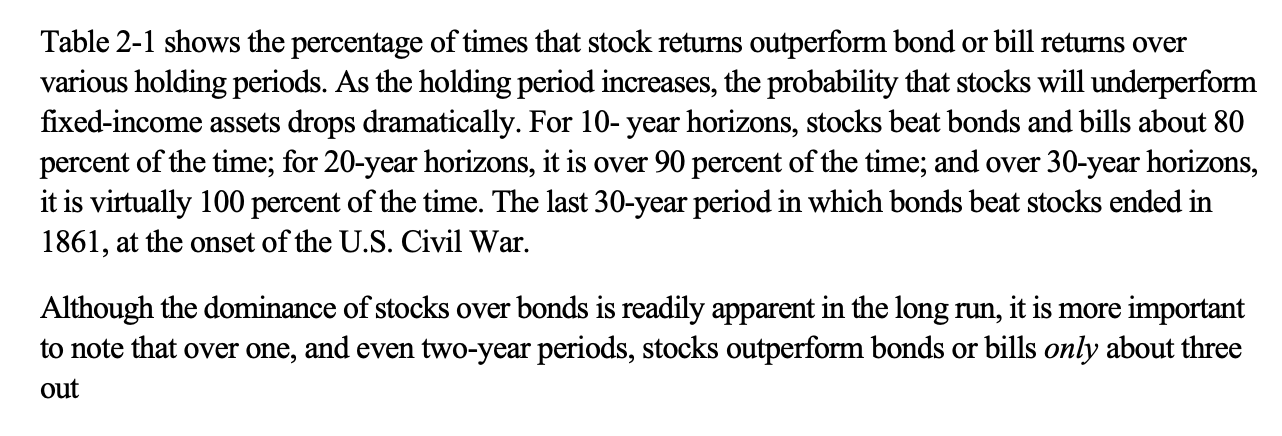

If we look at the returns of stocks versus bonds, in 80% of all scenarios, stocks return higher than bonds.

If we zoom out even more, over a 20 year period, stocks outperform bonds 90% of the time.

Then on a 30 year period, stocks have outperformed bonds 100% of the time.

Many think stocks are riskier than bond and while that’s true if your timeframe is only a year or two, because stock prices can be very volatile, but if you have a long time horizon, returns tend to gravitate towards a more consistent number of 6.5%, which is what U.S. stocks have returned for the past hundred years.

If we compare what bonds have performed over this time, it was 2.5%.

This is because stocks are consistent with how the business grows, how the economy is growing, how much earnings the business is retaining as a whole and their return on invested capital.

ETFs.

If you were to live a 100 lives, you want to be rich in 99 of them.

You don’t want to take the path to wealth that required a lot of luck like buying a bunch of out-of-the-money call options on a penny stock.

That’s not a reliable way to build wealth.

Whereas in contrast, saving money regularly, investing money in stocks, and continuing to not freak out whenever there is a market meltdown will lead to a great result in 99 of 100 lifetimes we look at.

So how much do you invest in single stocks vs ETFs?

ETFs provide a lot of diversification, which reduces your risk of things going very wrong.

When you invest in single stocks, you will miss a lot of sectors and industries that you might want to have some exposure to.

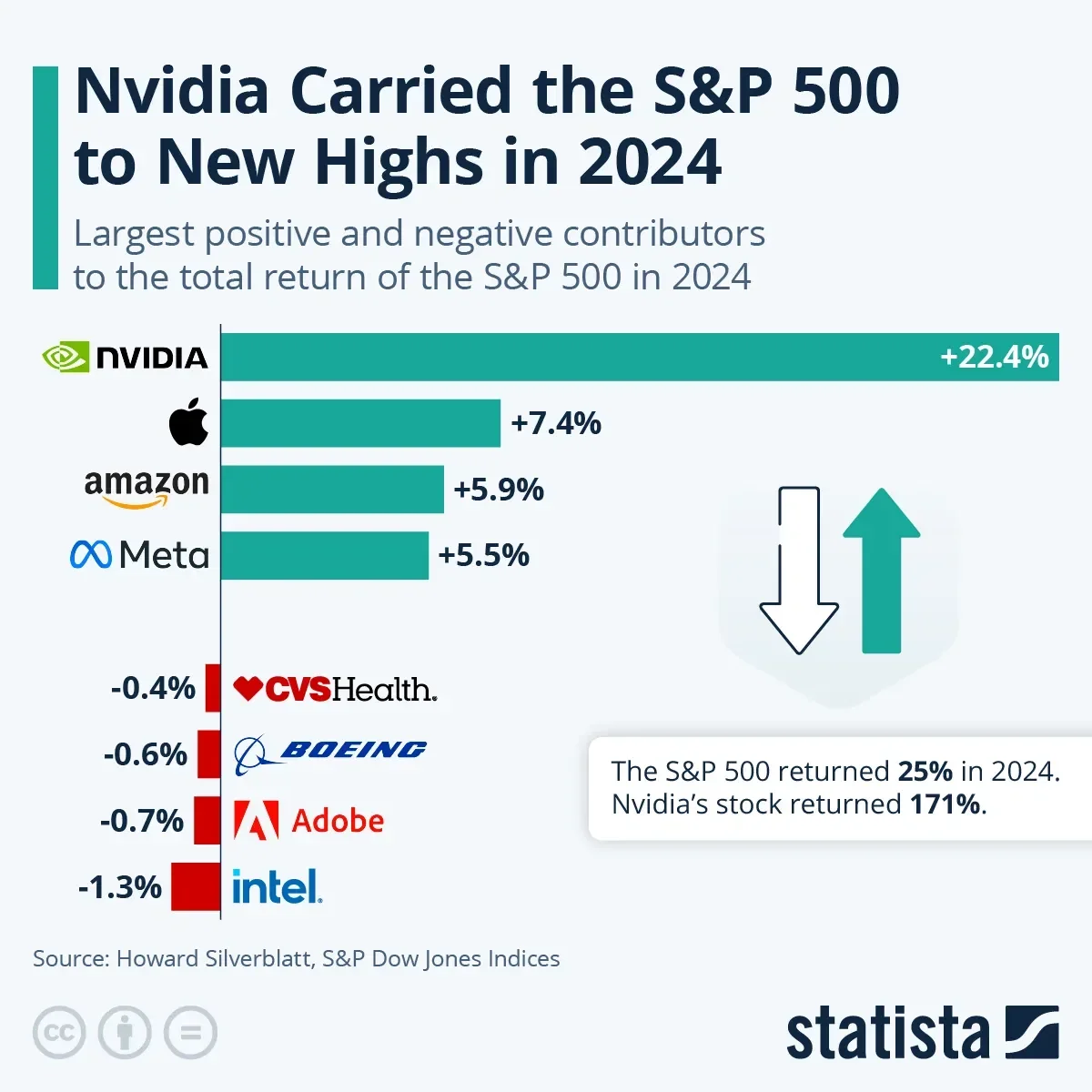

If you think about Tesla and Nvidia, you may not have be comfortable in assuming 100% growth rates, but because you own some ETFs that had exposure to Nvidia, you would have gotten some of the upside over the past few years where Nvidia contributed over got some of that upside.

ETFs also help you get exposure to other geographies that you may do better than the U.S. market in some periods of time.

A good way to think about ETFs is like an anchor in your portfolio, where it just helps you not worry so much.

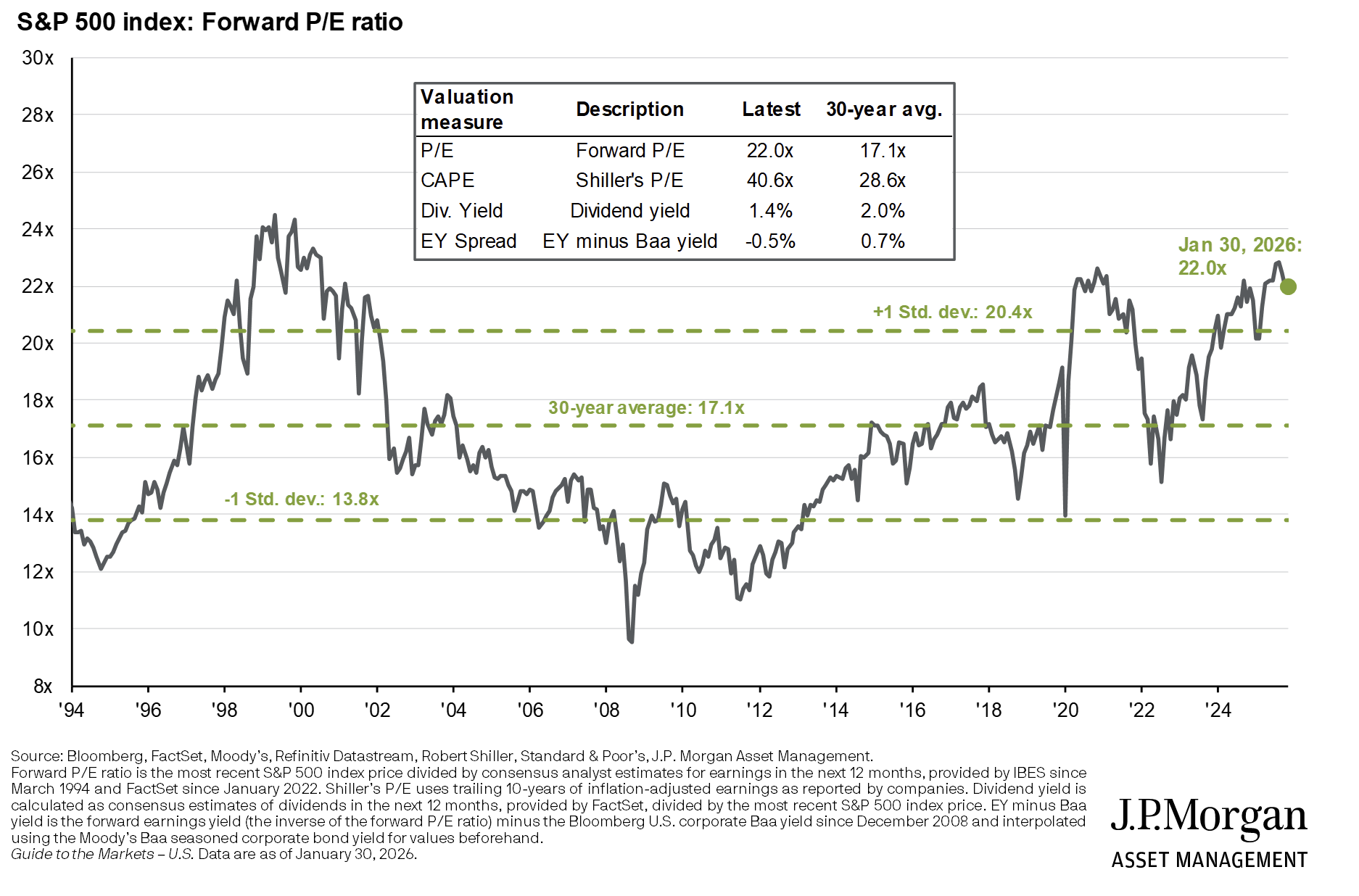

But there are downsides to ETFs too, especially right now with buying at all time highs.

While markets tend to spend most of the time near all time highs, valuations right now are 2 standard deviations from the historical norm of ~17x P/E.

Would you want to put a large lump sum in the market now or average it in over time?

The math suggests that lump sum investing tends to perform better since you want your money working for you earlier because markets usually go up.

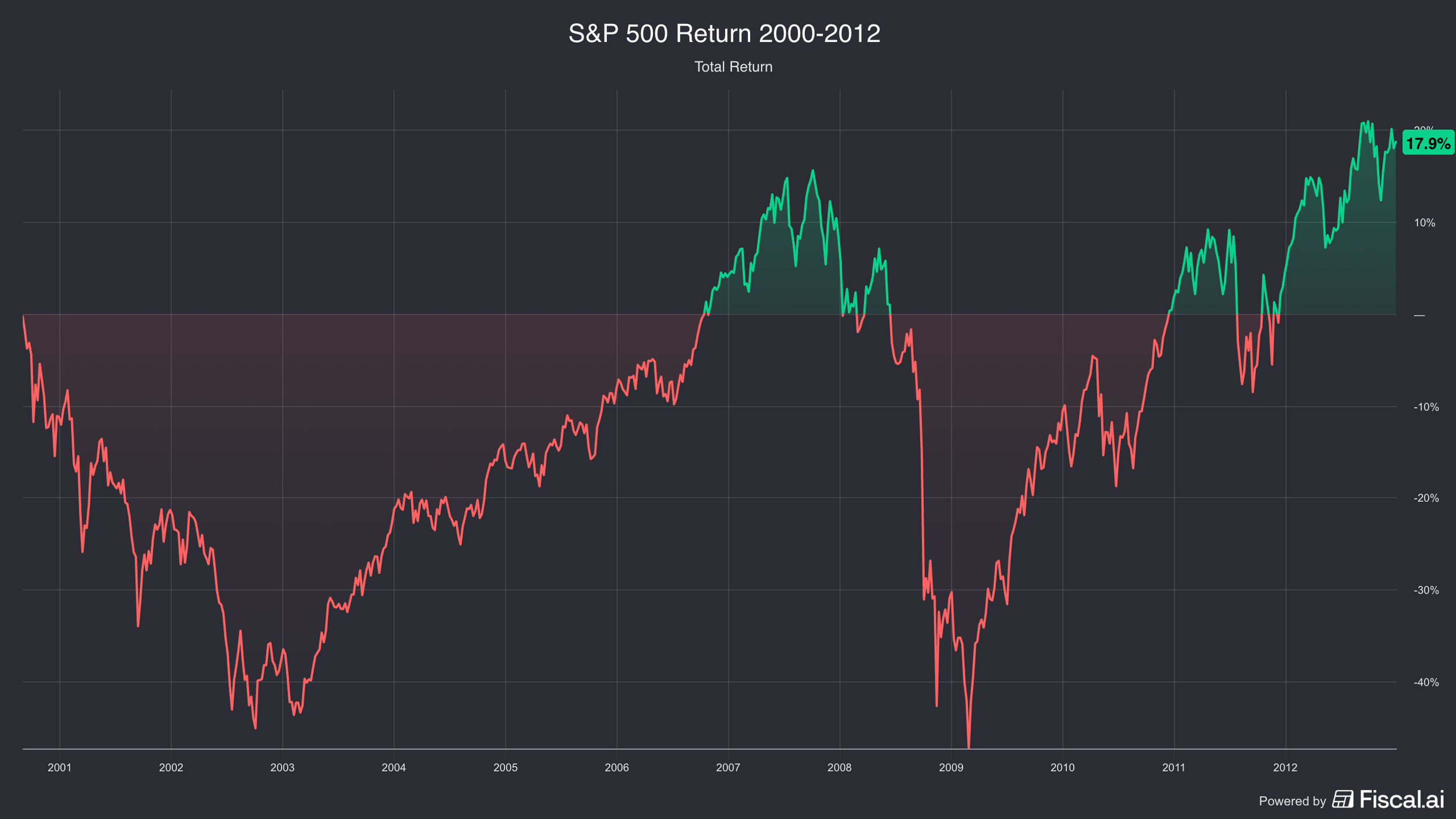

Now, there are times though where if you dumped your life savings into the market it can be risky like in 2000 for example.

If you invested your money in a lump sum, you would not be positive until 2012.

There is no right way and often times it’s doing a mix of both.

Investment Management and the Investment Matching Principle.

Many investment advisors are not well equipped to select individual stocks, and arguably should not be doing so.

That said, there are exceptions. Some professionals operate with a buy-side background and a more analytical framework.

However, this is not the norm. Most wealth management roles are relationship-driven rather than investment-driven.

When managing your own capital, the focus shifts to portfolio construction and diversification.

This is where the “investment matching principle” becomes important.

The idea is simple: you must match the risk of each investment to the number of independent bets in your portfolio.

A simple way to understand this is through bonds.

Suppose a bond portfolio has a 5% default rate. If you own one bond, there is a 5% chance you lose everything. That is unacceptable risk.

If instead you own 100 bonds, the outcome changes. On average, five may default, but the remaining 95 preserve most of the capital. Diversification reduces the impact of any single failure.

However, diversification alone does not create returns. It only reduces risk. To earn a return, you must be compensated for that risk. If the risk-free rate is 4% and the default risk is 5%, then a rough required return might be 9% or higher to justify the investment.

This leads to the broader question: how many investments should you actually own?

The answer depends on the nature of the strategy. Venture capital, for example, expects most investments to fail, with a few producing outsized returns. That requires a large number of bets.

In contrast, investors like Warren Buffett assume individual investments have a low probability of permanent capital loss. That allows for a more concentrated portfolio, where a handful of positions can dominate returns.

This is the essence of the investment matching principle: the risk profile of each investment must align with the number of independent bets in the portfolio.

“Independent” is the key concept. Correlation is often misunderstood.

During the financial crisis, for example, mortgage-backed securities were believed to be diversified. They were built across different geographies, income levels, and property types. Yet they shared a single underlying risk: rising home prices.

When housing prices stopped rising, losses became highly correlated across the entire system. What appeared to be diversification was, in reality, a single concentrated bet.

This same mistake appears in equity portfolios.

Ownership of companies in different industries does not guarantee diversification if they share exposure to the same underlying risk.

For example, Apple carries significant exposure to China through both revenue and supply chains. Any geopolitical disruption between the U.S. and China would impact that exposure across multiple holdings if not properly recognized.

Similarly, companies such as Snapchat, Pinterest, and Reddit were all affected by Apple’s privacy changes with app tracking transparency (ATT). Although these businesses appeared different on the surface, they shared a common dependency on ad targeting infrastructure.

More recently, AI has created a new form of correlation across markets. Software, analytics, and technology companies can all be affected simultaneously, even if their business models differ.

As a result, diversification cannot be assessed purely by industry or geography. It must be assessed by underlying economic exposure.

This also explains why multiple stocks in a portfolio can decline at the same time without necessarily indicating company-specific deterioration. Market-level factor exposure can drive correlated price movement even when fundamentals remain intact.

From a portfolio perspective, this is not necessarily a problem. What matters is whether the underlying business cash flows are actually impaired.

To reinforce the investment matching principle, consider a simple probabilistic example.

Assume an investment has a 50% chance of going to zero and a 50% chance of tripling in value.

If you own one such investment, your outcome is binary: either total loss or a large gain.

If you own two, the probability of total loss decreases.

If you own five independent versions of the same investment, the probability of losing everything drops significantly, while the probability of achieving partial or full upside increases substantially.

If the payoff increases further, for example from 3x to 5x in the upside scenario, the distribution of outcomes improves even more as the number of independent bets increases.

This illustrates the core idea: the risk-return profile of an investment must be matched to the number of independent positions in the portfolio.

Position sizing then becomes the practical extension of this principle.

Position size should reflect expected return, confidence level, valuation, and understanding of the business.

Higher conviction and more attractive valuations justify larger positions. Lower conviction or incomplete understanding justifies smaller positions or no position at all.

Importantly, passing on investments is a critical part of the process. The default answer should often be “no” or “I don’t know,” rather than forced participation.

Finally, position sizing must also reflect the reality of outcomes.

Even highly confident investments can fail. A small position that doubles has limited portfolio impact. A larger position, correctly sized, can meaningfully affect long-term returns.

However, concentration must always be balanced against the risk of error.

Even Warren Buffett has experienced situations where a high-conviction idea carried unexpected downside risk, when he invested in American Express during the Salad Oil Scandal.

In the end, all three of these pieces—financial planning, wealth management, and investment management—are really just different ways of doing the same thing: stacking simple, repeatable decisions over long periods of time.

And that brings us back to the original point.

There are easier ways to build wealth than trying to predict which company wins or loses in the next five years. Those questions are interesting, but they are not the foundation. The foundation is whether your personal financial system can withstand uncertainty, stay invested through volatility, and consistently allocate surplus capital in a rational way.

If you get that structure right, you don’t need to be right very often on individual ideas. You just need time to do its job.

Because wealth, at its core, is not built from a single great decision—it is built from a series of simple ones that you repeat long enough for compounding to matter.

For more on the 3 Aspects of Wealth Creation, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.