Private Credit Reckoning: What Investors Need to Know

Get smarter on investing, business, and personal finance in 5 minutes.

In the aftermath of the 2008 Financial Crisis, banks underwent regulatory changes that required them to hold more capital.

Given their more stringent capital restrictions and weariness of expose to higher risk corporate lending, they pulled back from the market.

Private Equity though still needed debt to fund their LBOs.

They saw the two as a business opportunity.

Private Credit.

A PE fund that was buying out a business, could have that business they just bought issue a loan that their Private Credit fund could buy.

This helped them move quicker with deals (banks are notoriously slow lenders) and gave them a whole new asset class they could clip an earnings stream from.

In a world of very low interest rates, this was welcomed development for investors.

Now investors could buy into private credit funds that had a much higher yield than their other fixed income options.

To boost yields even more, these Private Credit funds often borrowed money from banks.

This is called indirect lending and banks were happy to do it because their loans to the Private Credit funds were usually “senior” and “secured”.

This basically means that if there are any losses in the fund, the investors of the fund would lose money before the banks.

In turn the banks would lend a slightly lower interest rate.

For a Private Credit investor, they liked this because it levered their yields.

Leverage could turn a mid single digit interest rate, say 6% into a 9%, or sometimes higher.

Many of these Private Credit funds are legally structured as BDC or Business Development Companies.

A BDC can apply for to be treated as a “regulated investment company” which means they can avoid double taxation if they distribution 90% of their taxable income—similar to a REIT.

It also means they have strict debt limitations. It used to be 1:1 to debt to equity ratio, but in 2018 was increased to 2:1 under the Small Business Credit Availability Act of 2018.

That means they can have $2 of debt for every $1 dollar of equity capital.

But most BDCs still run closer to 1:1 debt to equity ratio.

And many of the assets they own are corporate loans that by and large do not seem to be under imminent risk of default.

So this is not the same as the financial crisis where the debt holders were backed by assets that have follow in value (often home mortgages on homes that were valued for less than the debt outstanding on them).

So why is everyone talking about stress in Private Credit a potential indication of further financial pain to come?

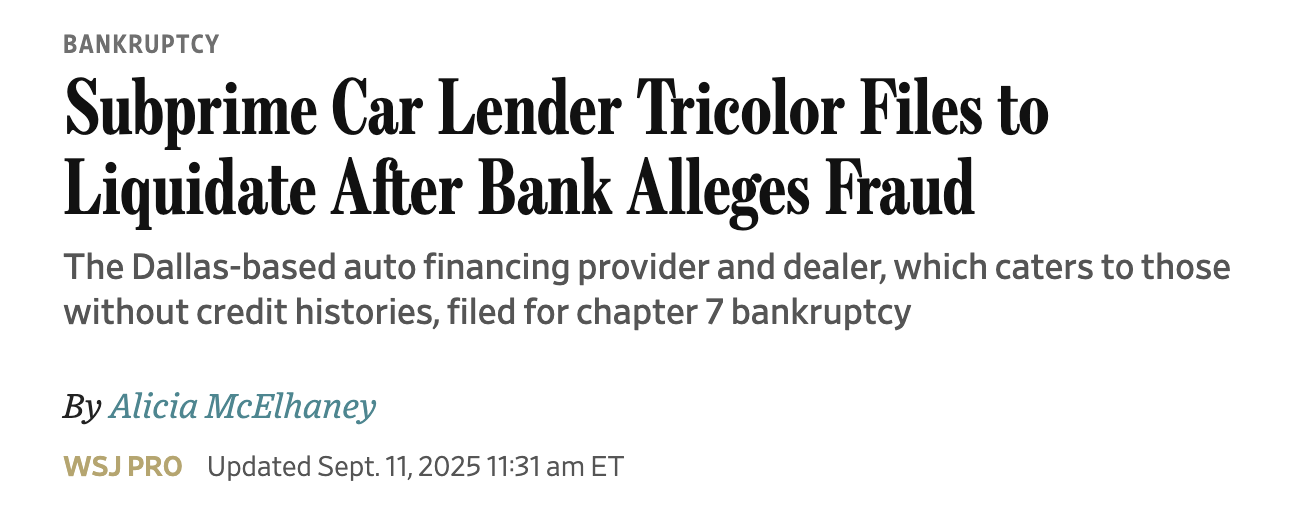

Jamie Dimon has said “when you see one cockroach, there are probably more” in reference to the sudden collapse of First Brands Group and Tricolor Holdings in late 2025, which wiped out investors.

Mohamed El-Erian, Chief Economic Advisor at Allianz, has called the redemption freezes at large Private Credit Funds (like Blue Owl) a “canary in the coal mine”, reminiscent of the early days of the financial crisis.

We cover all of this and what the true concerns are in this weeks Five Minute Money!

High Growth.

Any time an asset class grows very quickly, it should be met with skepticism.

This is especially the case in lending where the demand for the asset creates an incentive to get loose with the underwriting.

While institutional investors---endowments, pension funds, soverign wealth funds, and insurance companies—still account for 80% of the capital deployed in Private Credit, most growth in the past 5 years has been driven in the retail market.

This so called “democratization” of Private Credit meant more retail investors buying in.

The BDC is one means of which they gained exposure.

This can either be through publicly traded and listed BDCs like OBDC (Blue Owl Capital Corp), ARCC (Ares Capital Corp), or MAIN (Main Street Capital).

Or Blackstone’s BCRED or Blue Owl’s OBDC II, which is offered to the public but not listed on an exchange.

An investor will need to go through a broker-dealer, private bank, or Registered Investment Advisor to gain access to them.

Not every private credit fund is a BDC though. Some are un-listed closed end funds like Cliffwater’s Corporate Lending Fund. The debt to equity limits are stricter at 0.5 in debt per $1 in equity and they generally can’t gate redemptions (stop them temporarily for liquidity reasons), but they are otherwise very similar.

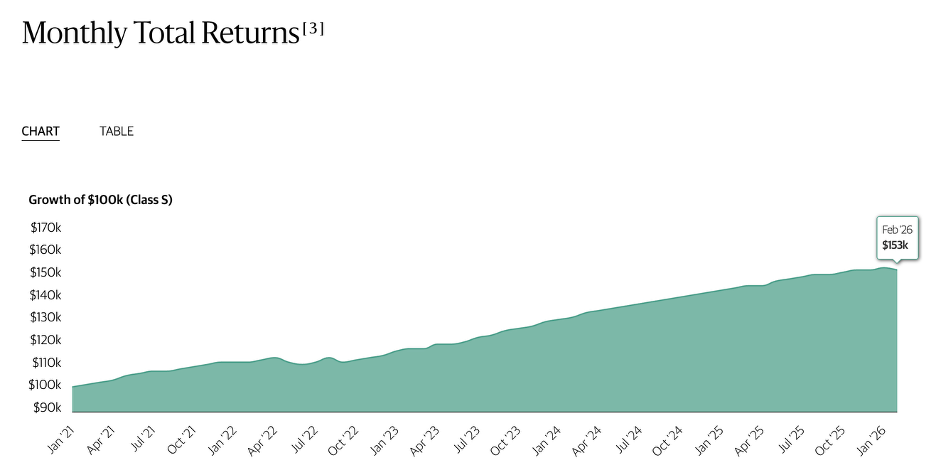

Below is the returns of BCRED’s S-Class shares. An investor who made this hypothetical $100k investment would have $153k 4 years later, for about a 11% annualized return.

Managers like it because it is a new stream of fees for them.

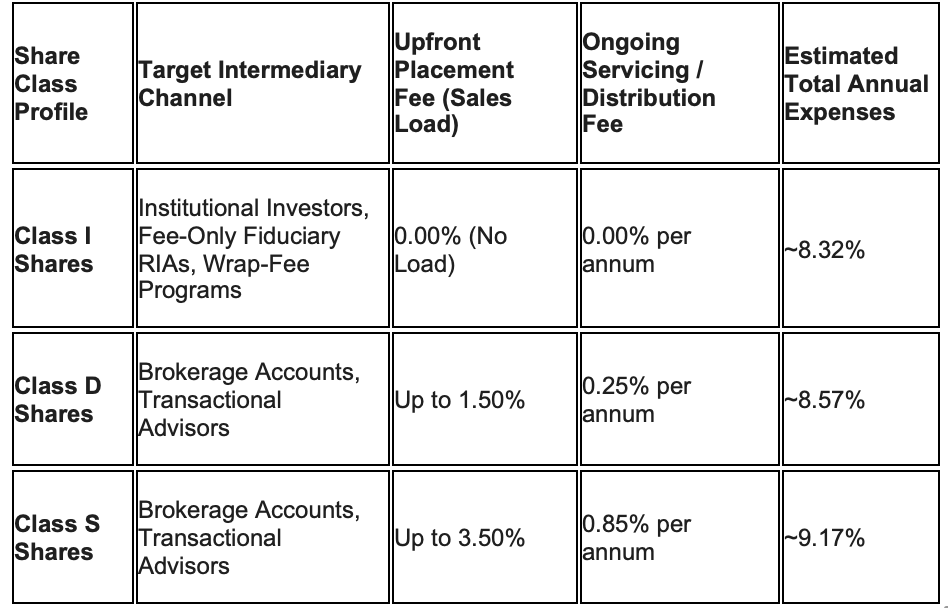

They can charge anywhere from 1 to 1.5% on assets under management. Given the leverage, this could really be increasing fees to 2.5% on the investor's equity investment.

5-6% hurdle rate and a manager often makes 15% carried interest once it is met. That means there is an incentive to earn at least that… and that they might get aggressive with their investments in order to reach it.

Depending on who is selling you the product there can also be an Upfront Placement Fee (Sales Load) of 1.5-3.5% upfront with another 25-85bps in ongoing servicing and distribution fees.

The different class of shares exist to provide a “sales incentive” to get advisors (who do not have a fiduciary duty) to sell their products and make a fee in doing so.

The stress in private credit funds stems from two distinct sources:

1) Liquidity issues

2) Potential Credit Risk issues

The two are related though as any whiff of credit risk can lead to investors running to the door to redeem their money.

As these structures are not built to redeem investors’ money quickly (the money is invested in long duration assets), it can cause a liquidity crisis and fund lock-ups, which in turn causes more investors to want to redeem.

Fire?

There are few private credit funds that have been spared from the increase in retail redemptions, but Blue Owl was a poster child of this phenomenon.

Investors increasingly worried about the risk AI posed to software companies, wondered how “good” the loans to software companies really were.

While the funds show de minimus losses (held loans close to par), the concern was that some these businesses would be wrecked by AI and thus the lenders would not get all of their money back.

This concern was exacerbated by the prices of software businesses (often 20x+ EBITDA) when taken private and the fact that many of these companies borrowed at lower rates than they could get in today’s market.

Since private funds do not value the assets the same way public markets do, and they showed no markdowns. Investors found this to be a bit suspicious.

In response, they ran for exits and tried to get their cash back.

The Blue Owl Technology Income Corp received redemption requests totally 40%. While that was some of the highest seen, other funds saw redemptions far higher than the typical 5% they are suited to serve.

This in turn led to them “gating” funds (limited withdrawals) and selling assets to cover the redemption requests.

Blue Owl sold $1.4 billion of assets to help cover the redemption requestions. Blue Owl noted that the loans were sold at 99.7% of par, trying to quell investors fears that the loans were impaired.

Instead it just made investors wonder if they just sold the high quality portions of the portfolio and now the asset mix was worse.

In turn redemption requests went up even more.

This liquidity crisis could force liquidations of loans at a time where they may not get their full fair value.

However, credit risk is still a concern too.

JP Morgan marked down a portfolio of their software loans, which only made investors question more why these private credit funds haven’t yet either.

Now depending on the fund, software exposure maybe 10 to 20%, so it is not all of a typical private credit’s funds.

And even though software companies were bought out at rich valuations a few years ago, they tend to lend at much more moderate 4-6x Debt to EBITDA ratios, suggesting that they still have cushions to recover even though valuations have dropped in half.

Some businesses are also switching to PIK (payment in kind interest) and having their debt maturities extended, which is typical of a business in stress when the lender doesn’t want to take a loss on the loan.

There is some fear though that the real issue will be when these businesses go to refinance, since they seldom can pay off their debt by maturity, and by then lenders will want more onerous terms, higher interest rates, and potentially an even lower valuation—especially if AI is threatening their businesses (which we haven’t seen yet).

Other public bankruptcies from First Brands and Tricolor also have investors wondering about the due diligence of some of these loans.

While it looks like fraud may have been involved there, it still speaks to lower underwriting standards.

And given that private credit has laxer oversight (it is often called shadow banking), there are growing fears that there is more losses to come.

That is what Jamie Dimon seems to think.

Contagion?

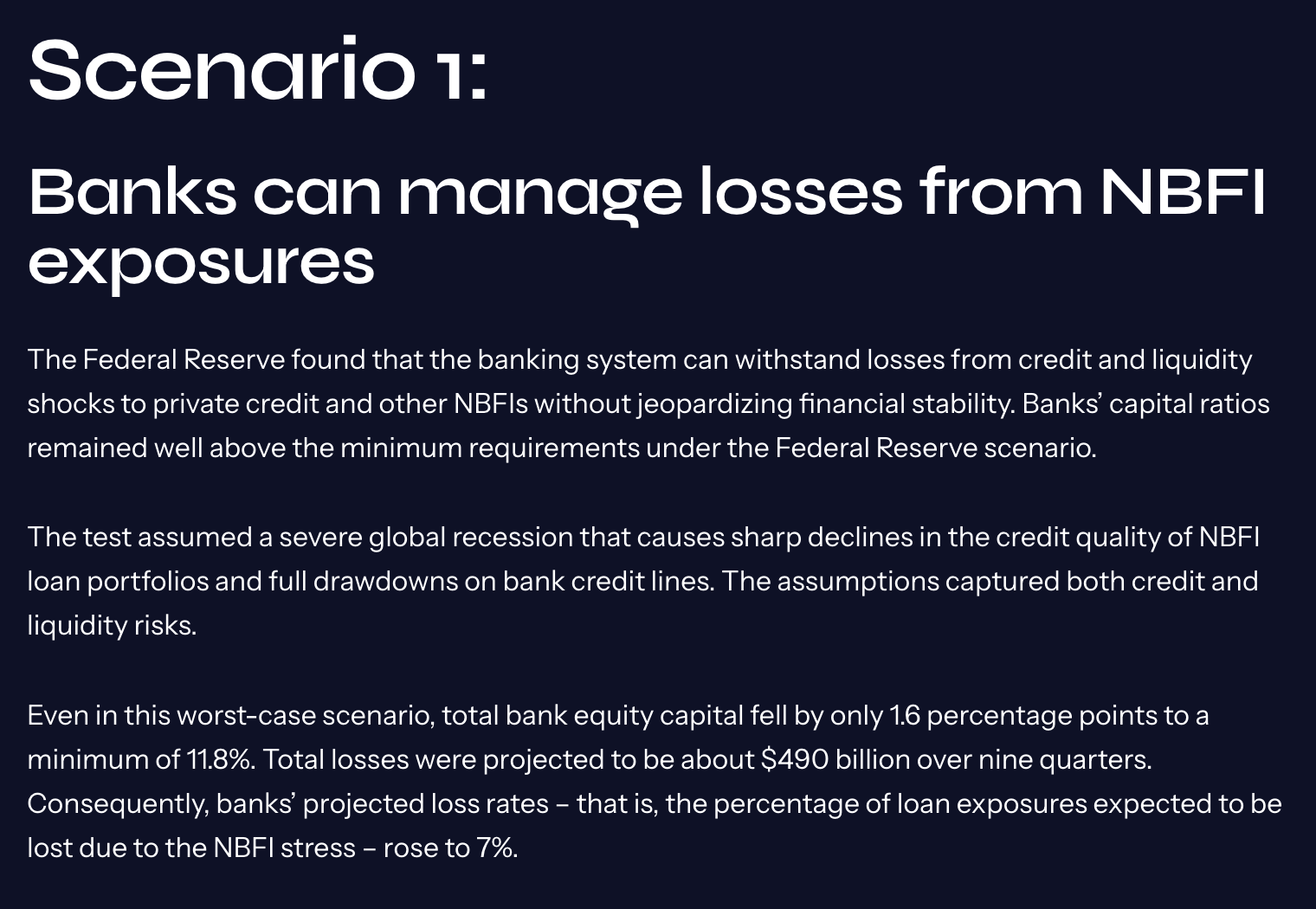

However, it doesn’t seem like the private credit crisis is an immediate threat to the financial system.

The Federal Reserve’s 2025 stress test estimated 7% losses on bank exposure to nonbank financial intermediaries (like private credit funds) in an extreme scenario.

The big banks still had adequate capital ratios in the test.

That doesn’t mean though that investors can’t lose and it also doesn’t mean that a larger contagion is impossible.

Part of the issue with “shadow banking” is it is hard to know just how hard it is interwoven into the financial system because of the laxer standards.

The best thing an individual investor can do though, if they are worried about that, is limit their own personal exposure to it.

And if a high yield seems too good to be true…

It might be.

For more on Private Credit, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.