18 Psychological Biases That Are Costing You Money

Get smarter on investing, business, and personal finance in 5 minutes.

Warren Buffett is fond of saying that if you have an IQ of 160, give 40 points away because you won’t need it in investing.

So if it isn’t intelligence that sets great investors apart from mediocre ones…

What does?

If you think about the value investing philosophy that Buffett follows, it has nothing to do with buying cheap stocks as it is often misunderstood as.

No, value investing is really a framework of psychology.

It may surprise you to hear this, but think about the key tenet of value investing:

Price is what you pay and value is what you get.

Right there in that simple phrase is the claim that a stock’s price does not provide information on what you are buying.

And it sounds simple, but in practice investors very commonly fumble here.

While they may analyze the business, they can’t but help let their emotions get the better of them when a stock price falls down.

It would be wrong though to say emotions are the issue.

Without emotion, you wouldn’t take any actions ever.

Neuroscientist Antonio Damasio showed this in his research where patients with damage to their ventromedial prefrontal cortex, the part of the brain that helps connect emotions to decision making, would commonly face decision paralysis at even the smallest of decisions.

And we seem to intuitively understand this idea with Star Trek’s Spock—who is very analytical—yet is unable to make decisions from analysis alone. Whereas Kirk’s actions are propelled by “gut feelings”.

The problem in investing though is a lot of these gut feelings misfire.

They were designed to protect a human from physical danger in the primordial world, not find investments and make decisions in an office looking at a stock screen.

So we are in a bit of a Faustian Bargain where we can quell our short term emotions, like our desire to avoid short-term losses or our FOMO, in exchange for what is usually poor long-term decision making.

Most investors will never get passed this for the simple reason that the emotions are always strong and it is hard to engage the logical mind to overcome short-term decision making.

However, with an awareness of how these emotions show up—and the psychological biases they represent—we can train ourselves to make better decisions.

We want our emotions to work with our analysis, but to be able to override them when they lead us astray.

In this week’s Five Minute Money, we will touch on all of the key psychological pit falls an investor should try to avoid.

Argument by Metaphor.

The first one I want to talk about is going to be called argument by metaphor.

This is when an investor who is trying to build an understanding of a company and they shortcut it with a metaphor.

You see a startup pitching a new service, and they call it the “Uber of dog walking.”

And what this is really doing is it is giving someone else a prepackaged understanding that you could then take and apply it to a new scenario.

It allows you to understand something very quickly.

The Uber of dog walking, one can understand what that product is from just one sentence.

The problem is though, when you are accepting this metaphor in full form, you are subverting any sort of critical thinking.

You have now already accepted that this is going to be the Uber of dog walking without thinking about all of the reasons why it may be nothing like Uber at all, why the markets may be very different, the competitive analysis, the management team, etc.

You are taking this metaphor and it is going above any sort of analysis.

Now, I'm guilty of this too. I'll call Coupang “the Amazon of Korea,” but the thing is that's actually backed by a lot of research I've done on Coupang itself.

So very often though, people only do the first part.

They just accept this is going to be the Uber of the next thing, and that will be their investment decision based off of that.

That would be a catastrophe.

And very often it is too, because people are relying on these shortcuts because they themselves don't have a full analysis of the scenario.

So this is someone taking this understanding of a very anomalous situation, translating it to a scenario today and saying they're similar.

Just because you see a similarity in the example though doesn’t’ mean the businesses or industries are actually similar at all.

So be careful of people who try to fool you by giving you metaphors. Metaphors are designed to aid understanding, not argue truth.

Narrative Fallacy.

This is a tendency to create a very clean narrative that fits very messy, real world data.

And if you think about, let's say, the reason why Jeff Bezos was successful with Amazon was because he originally started by selling books.

Because books, of course, as he would say, have a lot of SKUs. And so it's very hard for a bookstore to have everything in stock.

People usually don't mind waiting a little bit of time for a book. It's not that urgent. It's easy to ship because you don't have to worry about damaging it.

And so for all these reasons, books are really just the perfect item. Plus it sits very nicely in a warehouse and you don't have to worry about the inventory going bad.

Now you may take this as a narrative and you'd say that makes sense. And so if you want to build a successful eCommerce company, you have to start with books.

The thing is though, this is just a narrative.

This is not necessarily true.

Forest Li, who started Sea Limited, focused on women's clothing.

Richard Liu, who started JD.com in China started with electronics.

So what we thought maybe initially — that in order for you to have a stellar e-commerce company, you had to start with books — you see that there are these other instances that disconfirm this very clean narrative we have.

And so narrative fallacy is a tendency for us to preference these clean, easy narratives, even if they're not true.

We don't look at what is called “invisible evidence” or evidence that is conflicting. What is the story that we're trying to tell?

Stock market commentators do this all the time.

Why is the stock market going up? “Oh, it's because we think the Fed is going to lower interest rates.”

It's a very clean narrative.

A harder narrative is trying to look at the millions of decisions that individual buyers and sellers have made and all of the data that exists and try to come up with some sort of explanation.

It's impossible, right?

And so that's why we opt for these very clean narratives, but they're not true.

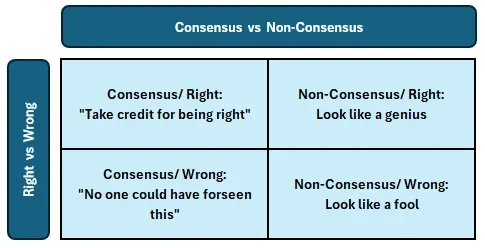

Hindsight Bias.

This is a little similar because we tend to believe things are much more obvious in hindsight than they really are.

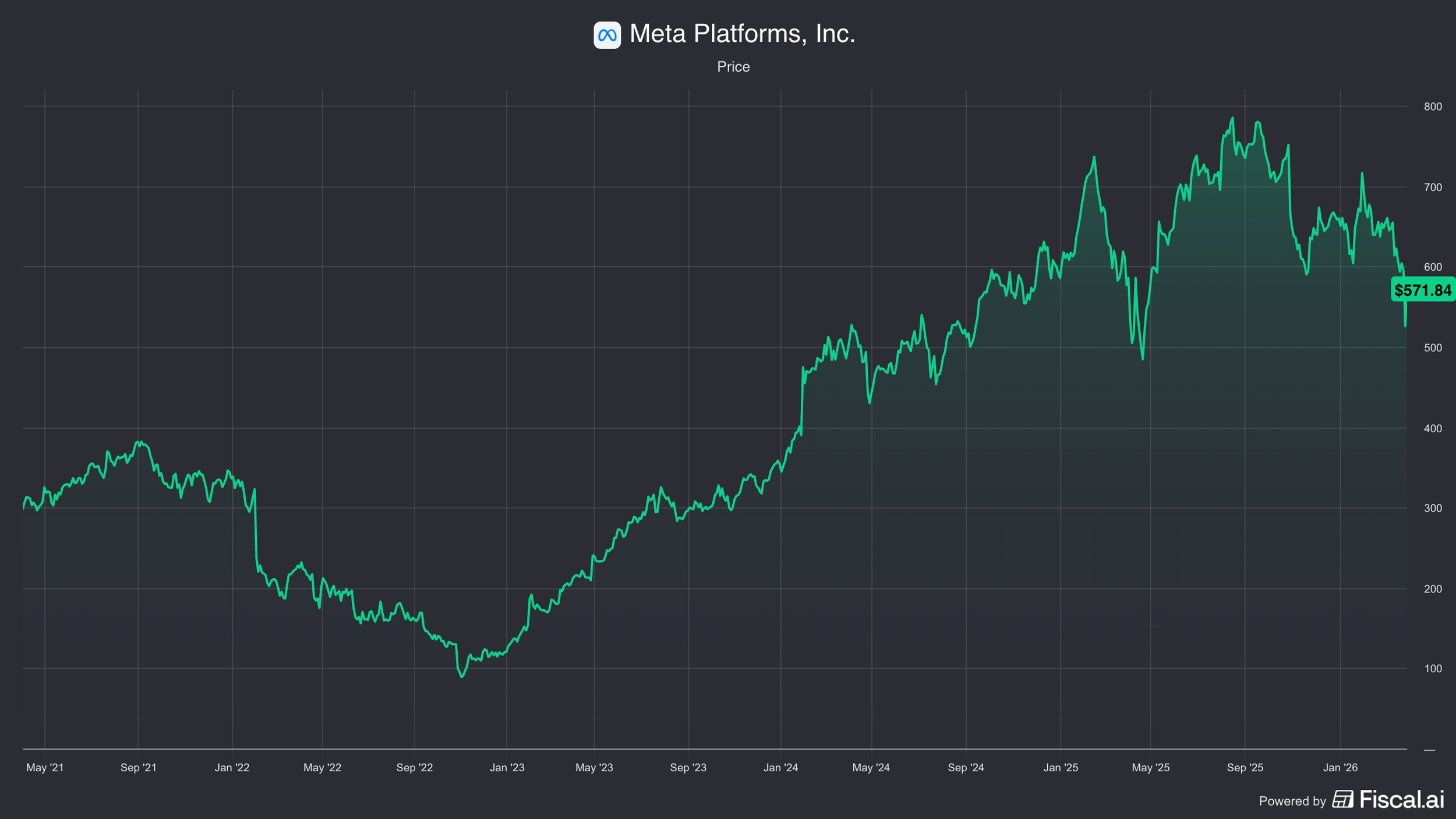

There's a lot of people now that say Meta was a very obvious buy in 2022.

I like to remind them how scary of a time it was.

· App tracking transparency

· Apple’s threat to kick out abusers out of the app store

· FTC potentially trying to split up Meta

· TikTok competition threat

· Would their response with Reels have the same ad monetization success as they had in the feed?

Now I wrote a 160-page report at the time analyzing all of these issues to better understand them, but I know most investors did not do that research.

Instead, they're looking at a stock price that went up and they're saying, “Oh yeah, wasn't that one pretty obvious?”

I saw the same thing with Netflix at that time too, when it was down around 80%.

It seems very obvious in hindsight that these were buying decisions.

And so you've got to guard against hindsight bias because it is going to make you believe that these past decisions were much easier than they really were, which is then going to cause you an issue because you're going to be looking at a stock today and it's going to be confusing, and you're going to expect it to be as easy as it was buying Meta or Netflix in 2022.

Forgetting that those were not easy decisions at the time.

They obviously weren't easy decisions at the time because you would have made them if they were obvious.

And the whole market wouldn't have sold off that much if it was.

Confabulation.

This is basically our tendency to just always create narratives.

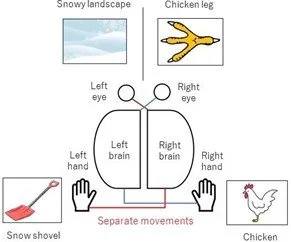

And there is something called split-brain patients, which are people that have their corpus callosum cut.

So this is like a bundle of nerves that connect the left hemisphere to the right hemisphere and it's interesting to do studies on them because we only talk from our left hemisphere, and each eye is actually linked to the opposite hemisphere.

One of my favorite studies of all time was researchers showed someone with this split-brain condition an image in each part of the vision field. So each hemisphere of the brain saw a different image.

One hemisphere saw an image of snow. The other hemisphere saw a chicken claw.

Then they asked them to point to the associated images. So the right hand points to a shovel, the left hand points to a chicken.

Now, since the left hemisphere is the only part of the brain that is able to talk, and that's the part of the hemisphere that saw the chicken claw, it's trying to create an understanding as to why this right hand pointed to a shovel, and it doesn't know why it pointed to a shovel.

Now the researcher knows it probably pointed to a shovel because it was shown a picture of snow, and okay, a shovel — you go ahead and shovel snow.

Now the participant though, who's being asked this question, doesn't have that data because the right hemisphere can't talk to the left hemisphere.

What it does in this case is it tries to explain why its right hand is pointing to a shovel when the left hand is pointing to a chicken, and so it confabulates a narrative.

It says the reason why it pointed to the shovel is because you obviously need to shovel in order to shovel chicken manure — which is what he said.

And so he was able to create this own narrative, even though we know it's not true and the facts were not what he thought them to be.

But it's automatic for us to come up with reasoning.

When you are researching a stock, when you're making a decision on something, you're trying to put together all of these facts, you're going to automatically draw connections that may not be real, that may not actually be there.

Base Rate Fallacy.

This always comes up when a company is making a big acquisition.

This is going to be a transformational acquisition, and investors will buy it.

They'll buy it because of the framing effect in part, or the narrative fallacy.

You're creating a clean, simple narrative.

There are all sorts of reasons why you may go ahead and believe management.

What's happening is you're forgetting the base rate, which is that most big acquisitions fail.

They end up writing off most of it and usually divesting the investment because it's very hard to integrate a very big company together with another very big company.

Very often the strategic rationale is a little tenuous.

You have different cultures, and whatever the reasons are, the base rate is that they're not that successful.

And so what you want to do in all scenarios is think about the base rate?

If a company is trying to go into a new market they've never been in before, well, how successful have other businesses been trying to penetrate India, for example?

That's a market that's actually notoriously been very hard for a lot of western companies.

Same with China.

Survivorship and Selectivity Bias.

Now, when you're looking at your data sample, you have to be careful that you don't have survivorship bias in it or selectivity bias.

This is when you're looking at a pool of data and data is being omitted from it for various reasons.

Let's say you're looking at the most successful entrepreneurs.

Guess what?

You're not looking at a list of all the entrepreneurs who tried very similar things and weren't successful.

This is going to make you believe that certain things are easier to do than maybe they really are.

So this plays into the base rate fallacy as well, because you could have skewed base rates.

Now I mentioned briefly invisible evidence.

This is the evidence that disappears over time.

Let's say if you're looking at what makes a company successful, you're ignoring all of the evidence of businesses that did very similar things and did not end up being successful.

So what you want to do when you're crafting an investment thesis is you want to look for disconfirming evidence, because if you don't, you're going to fall prey to confirmation bias.

Confirmation Bias.

That is a tendency to only want to look at evidence that confirms our thesis.

As an investor, you want to make sure your thesis is as accurate as possible.

One example is, let's say I am looking at the cloud providers.

I want to understand how they're able to charge such high prices that get them such nice margins.

Because usually you're taught that when there's three big players in an industry and they all kind of have a generally similar service, they compete on price, and price gets pushed down.

And so I wanted to understand how sustainable this margin was.

Was it just the fact that there's more demand than supply?

And so once supply increases enough, that is going to lead to pricing pressure.

So I wanted to look at what could disconfirm this.

So I looked to China.

I wanted to understand the cloud environment in China because in China, interestingly enough, all of these players, even the big players like Alibaba Cloud, have always been much, much, much less profitable.

And so I was looking for all of the reasons why they weren't profitable to see if it shed any light on profitability for the Western companies.

Sunk Cost Fallacy.

But I also needed to not fall prey to sunk cost fallacy there and say, just because I did all of this research, I need to get something out of it. And so instead I just moved on and said, that's fine.

I wasted a bunch of time trying to research that and I went nowhere with it.

And sunk cost fallacy is something that's very common in a lot of investing too.

You'll spend time researching something and it may lead to nowhere.

But it's something that you have to guard against, because the stock doesn't care that you did hundreds of hours of research on it.

That's not going to change the return profile of it or the risk involved in it.

And this also feeds into desirability bias.

Desirability Bias.

This is the idea that you want something to happen and so you're just going to believe it's going to happen.

There are all sorts of people that will buy penny stocks, meme stocks, meme coins, whatever it is, and they do this because they want to get rich.

These stocks, these tokens, whatever it is — they don't care about your desire to get rich and your need to do that and your need for quick money.

It doesn't care about that.

And you focusing on these factors is at the cost of the actual elements that you could research and analyze and actually try to take an opinion on, which could lead to better results over time.

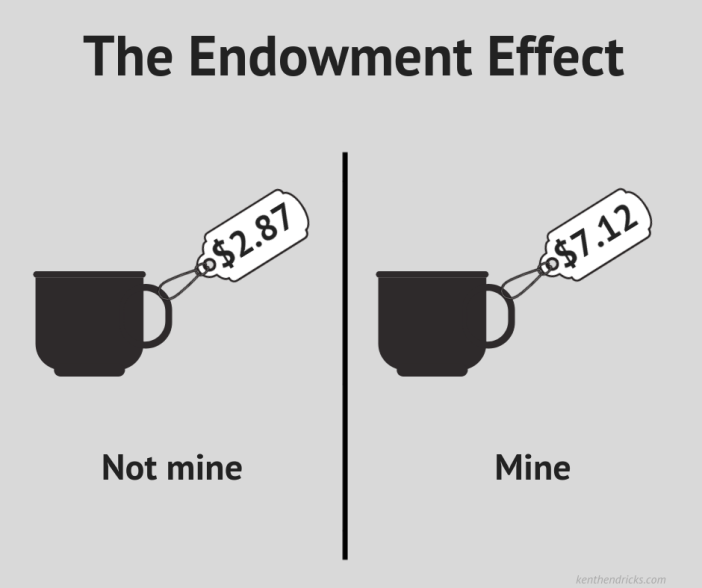

Kind of similar to that is going to be the endowment effect.

Endowment Effect.

This is going to be the belief that things that I own have higher value than things that I don't own.

And it's not like this is a conscious belief — you're just going to do it automatically. They've done studies on this.

They hand out participants random coffee mugs, and if you were the one who was given a random coffee mug, you are going to value that coffee mug at a higher price than if you weren't given the coffee mug.

Just by virtue of the fact that you own something, you are going to value it more.

Now, you can imagine if you're looking at the stocks in your portfolio how that can be an issue.

If you're valuing the stocks in your portfolio more just by virtue of the fact that you own them, then that is going to lead you to not look at opportunities fairly.

And Charlie Munger actually talks about this too, where he's fallen prey to it.

It was with Belridge Oil Ridge stock, where he said a broker gave him 300 shares and he took it because that was all the money he had at the time. And then that broker called up later and offered him 1,500 shares. And he knew that this was a great investment. He called it a total steal, a no-brainer.

And he said it was very, very obvious he should have done it. And ultimately he decided not to do it because he would have had to sell something in his portfolio or take out a loan or something in order to buy these extra 1,500 shares.

And he just didn't do it.

And part of that was because he valued the things in his portfolio more — the endowment effect.

He didn't want to sell the things in his portfolio, even though he knew that this was much, much better.

And so even great investors like Charlie Munger can fall prey to this stuff. I can promise you I do, and I can promise you, you probably do as well.

Not Invented Here Syndrome.

This basically is the fact that you are going to be biased against things that you don't come up with yourself.

Now in investing, this would be you saying, "I am not going to invest in this very obvious idea because it is not my idea. I only invest in ideas that I come up with."

There are a lot of investors that just did not even want to look at FAANG stocks or the Mag Seven just because it was like too obvious.

They would not even look at them — didn't matter if Meta was at a low P/E multiple or Google, whatever it was.

They would just say, “You know, it's too obvious, I can't do that!”

They want to come up with their own ideas.

They don't want to copy other people's ideas.

In some sense, that is the opposite of groupthink.

Institutional Imperative.

This is something that Warren Buffett coined and it is what happens when you get a very big institution, a bureaucracy, and it's a mix of kind of these different psychological biases.

Some of it is going to be groupthink, inaction bias, a desire to not want to change things in the way they're done. There's going to be a lot of authority bias in there too.

All of this kind of comes together in this institutional imperative where these organizations just go about blindly doing things they've always done before, because that is the way we've always done it.

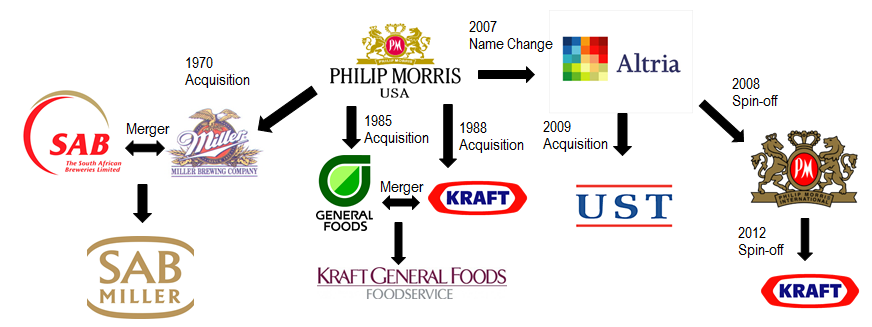

You could see this in capital allocation decisions.

Tobacco companies in the 1980s were very worried about their businesses being legislated basically out of existence.

And so Philip Morris bought General Foods. RJ Reynolds in turn bought Nabisco. Philip Morris then bought another food company, Kraft.

Now, there's no reason why if you had two companies that both had profits to invest somewhere and were both deciding what companies should I reinvest my profits in, you would expect them to come up with very different answers than them both going into the food industry.

RJ Reynolds saw Philip Morris going and buying food companies, and so they went ahead and did the same thing.

That's what this institutional imperative is.

It's kind of this mindless decision-making body that just goes about and does the same thing others do, in the same direction it's been done before, without a lot of rational thought.

An antidote to this is to have a founder-owner in control and to have businesses that are simplified, streamlined, with fewer layers of bureaucracy.

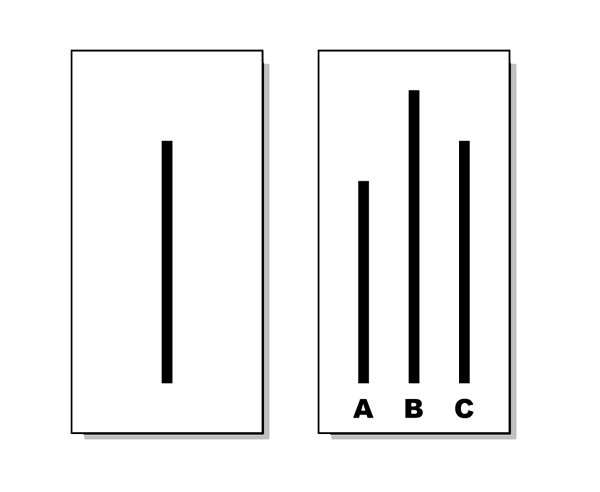

Groupthink.

This is going to be the tendency to conform to what peers are doing.

Now, if you think you are above this, you have to know what the Asch conformity experiment is.

This is a crazy experiment where they'll put people in a room and they'll draw two lines on the board and they'll say, which line is longer than the other line?

And if there are 20 people, only one person is actually the participant in the study.

That'll be like the 20th person. And the other 19 people are all actors, and the actors are told to say that the lines are the same size.

And so this person — the 20th person who's being asked — "Is this really long line longer than this line right there?"

Even though very obviously the lines are not the same length, he very often answers that the lines are the same length.

That is the pressure of conforming to a crowd.

This exists when you're investing.

You want to own things maybe other people are owning — momentum trading, own the hot stock at the time, the AI trade, own AI stocks, own whatever is very hot in the moment.

It exists if you have an investment advisor — you might all of a sudden find that they are tending to buy you the same things that a lot of other investors think are hot at the time or popular at the time.

It's easy for them to conform.

It's harder to go against the crowd.

A lot of times, institutions and bureaucracies are not set up for an individual to go against the crowd because of careerism.

That means that their incentives for their career to do well do not align with your incentives as an investor.

This is very common.

And this is because if you are doing what everyone else is doing and it doesn't go well, you could say, “Whoops, everyone else did it. That's not my fault!”

But if you stand apart from the crowd and then it ends up going poorly, people are going to blame you.

They're going to say, “How could you do something so silly? Everyone else knew to buy the AI stocks. Why couldn't you just do that too!?”

It's a harder thing to stand apart from the crowd.

It's more comfortable owning the thing that everyone else owns.

It's harder owning something that's unloved, that is down a lot, going against the group.

And this also gets even more complicated when you're going against authority.

Arguments From Authority.

These can be arguments from authority or a sort of authority bias, where we have a desire to comply with whatever an authority figure tells us.

It is very hard to disagree with your doctor because he's supposed to be the expert.

And while you shouldn't always disagree with your doctor — in fact, you should usually listen to them — sometimes they tell you things that are wrong, and that is just because that is the best level of medical evidence we have at the time.

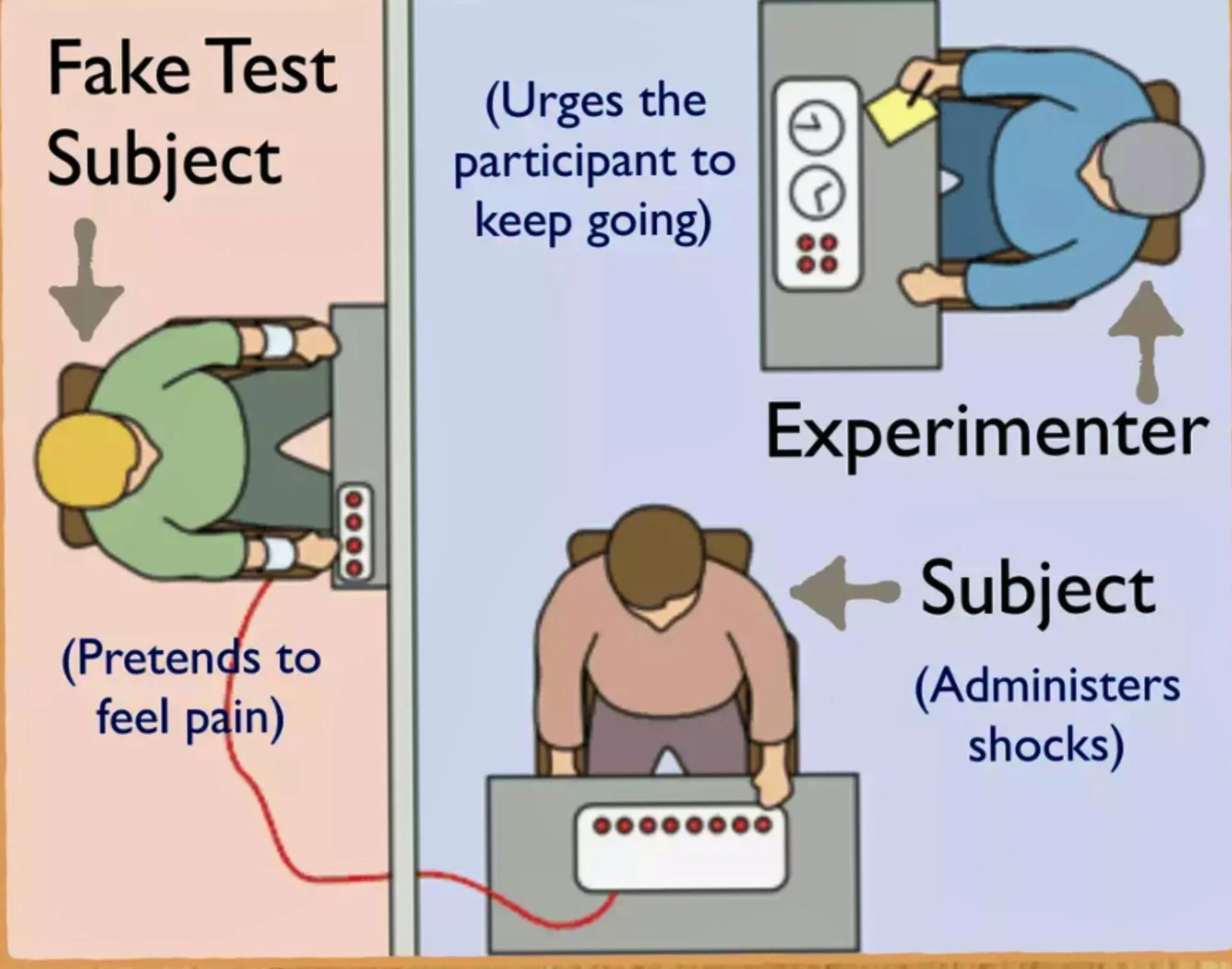

We could look to the Milgram experiment, which is a terrifying experiment, to understand this even better.

In this experiment, the setup is as follows.

There is someone who's sitting in a chair that is hooked up to electricity, and you are then being told by an authority figure to administer a level of electricity to that person.

And the reason why this experiment was originally created was that he wanted to understand, in the aftermath of World War II, why so many people — ostensibly otherwise good people — went along and did such awful, horrible things.

And instead of just saying, well, it's because they must be horrible people, he was looking for a different answer and he got his answer with this authority explanation.

And so in this experiment, the way it works is that there is an authority figure — someone in a lab coat — who is telling someone else to administer shocks to what they don't know is an actor.

But as far as they know, it's a real person in the study.

There's no reason why this person needs to receive shocks or anything like that, but just by virtue of the fact that he's wearing a lab coat and you're in a study and he's telling you to administer shocks to this poor bystander, you're going to do it.

At least a very high portion of people end up doing that.

And that just goes to show our desire to listen to rules, to listen to authority.

Some people are built very differently naturally where they don't want to do this, but that is not most people.

And so when you're dealing with investing money, maybe you hear, “Hey, a Goldman Sachs analyst said this stock was a buy. Morgan Stanley said it was too!”

And that is going to be an authority telling you to do something, and you're more likely to do that just because they told you to.

Whereas if you heard Chad's Stock Picks was telling you it's a buy, you wouldn't care.

But ultimately Chad's analysis might be better than the Goldman Sachs person's analysis.

And so you can't rely fully on these authority figures to actually tell you what to do.

This is why investing is such a tricky thing, because a lot of people are looking for guidance and looking for answers as to what stocks to invest in.

But there's not going to be anyone that can tell you this very often that doesn't have its own perverse incentive attached to it.

Super Response Tendency.

The next one we're going to talk about is the super response tendency, as Charlie Munger calls it. This is going to be incentives — the way outcomes follow incentives.

A lot of investors are more aware of this these days.

They do look at insider ownership. They look at what the targets are in the performance stock units, the RSUs, and all of that's really good because they understand that if a company is being incentivized to hit quarterly numbers instead of a return on invested capital figure, they're going to magically hit those quarterly numbers.

And that's not a good incentive, because that's not a good way to build wealth for longer-term shareholders.

An example of this is where in investment advisory there are some people that are just salesmen and they will sell you a product that they themselves get the highest commission on.

There are all of these structured note products, for instance, where they take a commission off of selling that.

Within the super response tendency, there's this interesting case Charlie Munger talks about where he says, what business can you raise prices on and increase volume?

Very often people list a Veblen good, which is an economic term for basically a good that, as you raise the price — like a Louis Vuitton bag, a Hermès bag — it becomes more desirable and so there's more demand for it. That's not what he's talking about.

He's talking about different industries where the person who is selling a product makes a markup on it or earns a commission based off of that product, and so they're going to opt to sell more of it.

It could be a plumber selling you different plumbing supplies and taking a markup on it. A commission-based arrangement — magically, the more expensive one gets recommended a lot more often.

And so it's interesting to note the way these psychological biases can go into play in the actual businesses themselves, not just on the investment side.

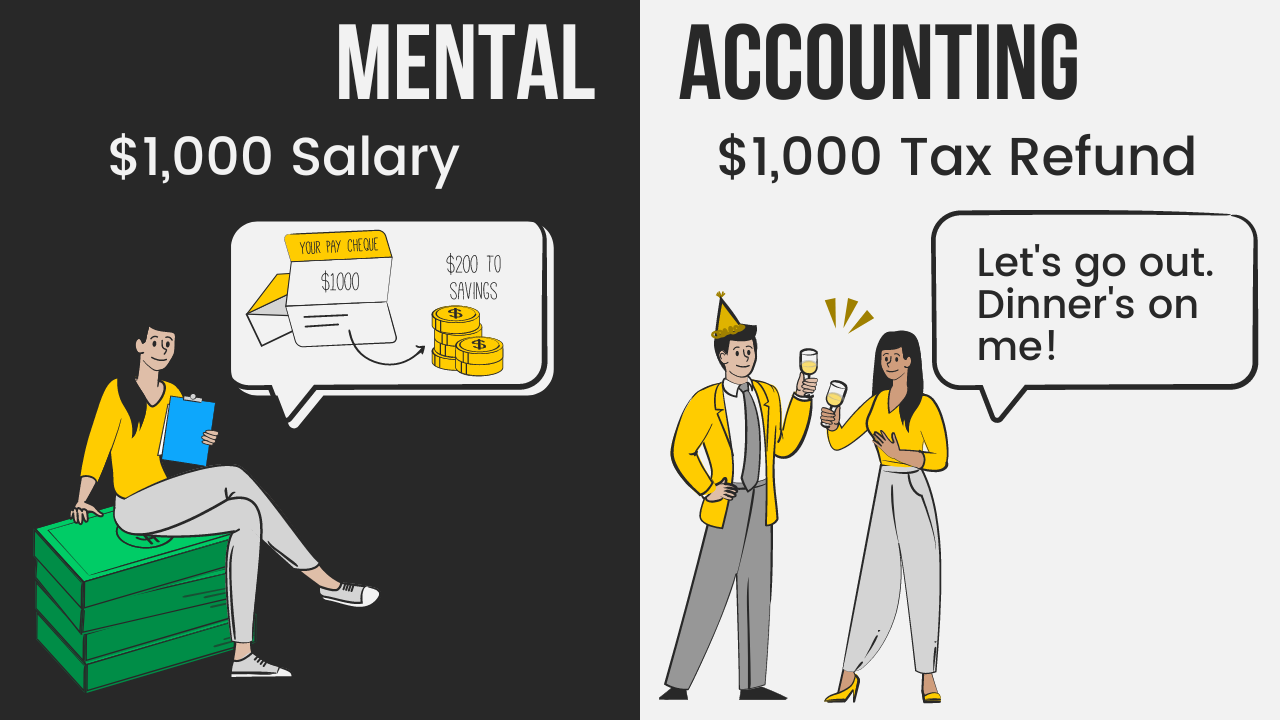

Mental Accounting & House Money Effect.

This is where we treat different dollars in different buckets differently.

So money that you earn very easily — this is also a separate bias called the house money effect.

And so if you just bought a stock and it went up a lot, you just made a 200% gain very quickly.

You're going to treat that money differently than if it was a stock you held onto for 10 years and got that same gain, which you're going to treat differently than if it was a bonus from your employer, which you're going to treat differently from if it was a salary bump.

These are all mental accounting buckets that we treat this money differently.

But it's a bias because it's all our money. We shouldn't treat money that comes from different sources differently.

And I see this very commonly, and this is actually a really sad one, but a lot of times hardworking people — people that have been saving money and then they put that money in an investment account and all signs of caution kind of go out the window and they do all sorts of crazy things with that money once it's in that investment account.

You should absolutely take the same level of care with your investment dollars as if it's the same sort of dollars you've earned from hard labor, from whatever your job is, whatever your wages are.

Don't treat it any differently.

Don't think that just because it's in that investment account, it's okay if you lose it.

Halo Effect.

Now, you also don't want to fall prey to the halo effect.

This is basically whenever there is some sort of positive attribute from a person and then you translate that to meaning there must be this other positive thing about them.

The very classic example is that, unfortunately, it's true too that if someone is tall and good looking, they're more likely to get hired for a job.

They're treating the fact that they're good looking as a sort of halo to mean they must be good at their job.

And so you want to be aware of this.

Affect Heuristic.

This has to do with your first initial emotion characterizing how you feel about an investment.

If you really like eating at Chipotle, you're going to be more likely to want to invest in Chipotle.

Now I think some of this can in a way be like a good tell, because I do think as a retail investor you can have a benefit in that.

If you really like a product a lot, it's probably because there's consumer surplus there, which means that they could theoretically charge more than they really do.

And you should definitely look at that as a potential area to research, but that on its own is not sufficient to make a decision.

Value investing is a framework of psychology.

What separates the best investors from the mediocre ones is not intelligence but rather how one deals with their emotions.

And so there are a lot of different psychological biases that I listed here that interfere with one’s ability to invest rationally, but if you follow this list and you come back to it to continue to be aware of it and continue to remind yourself of these so you actually take these into practice every day, then you're going to become a better investor overtime.

For more on psychological biases, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.