Booking Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

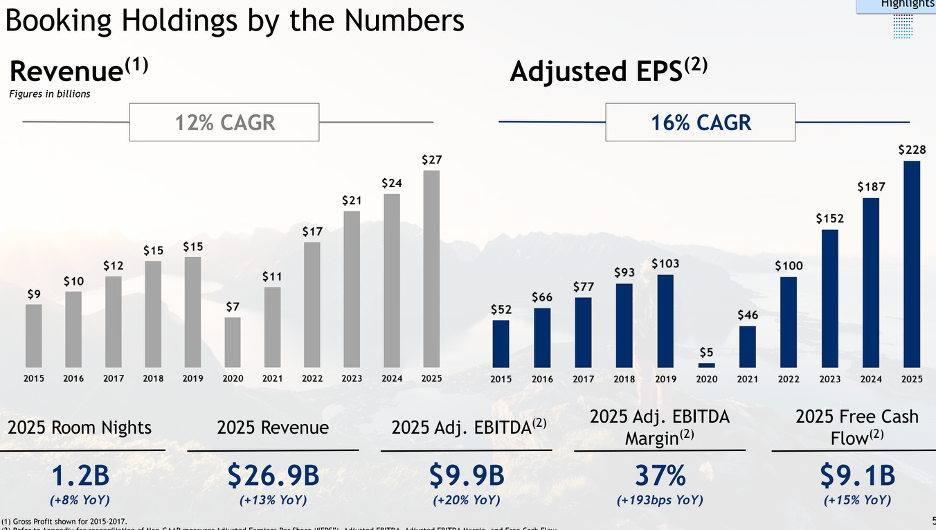

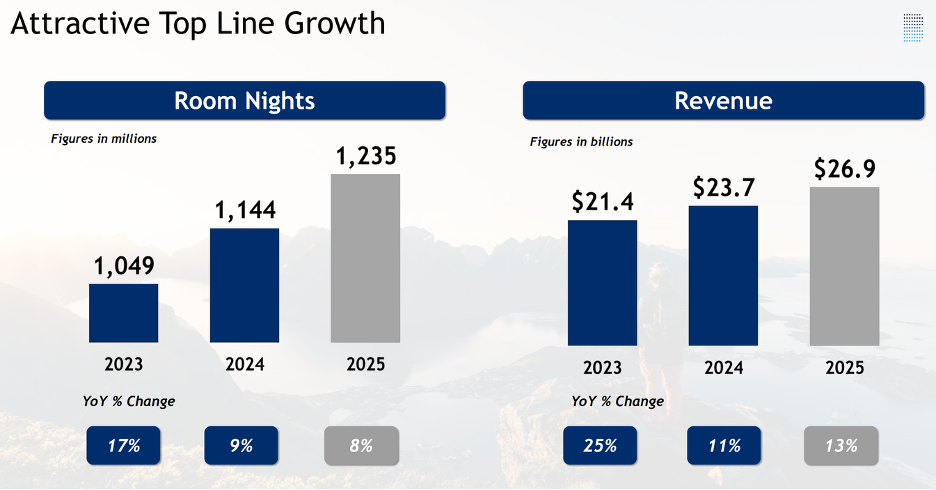

Booking trades at 17x free cash flow and grew revenues 13% y/y.

That is more than Expedia’s 8% y/y and Airbnb’s 10% y/y growth.

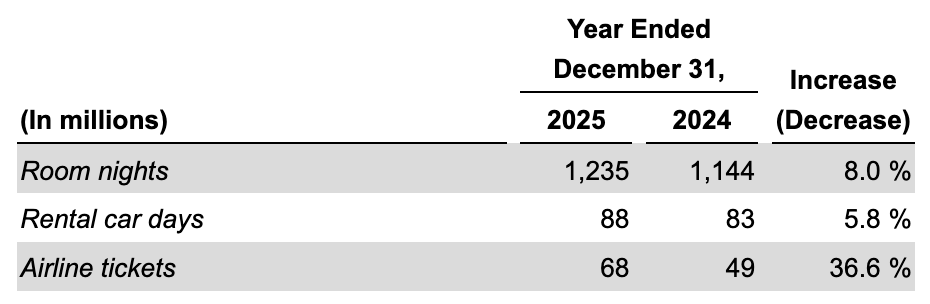

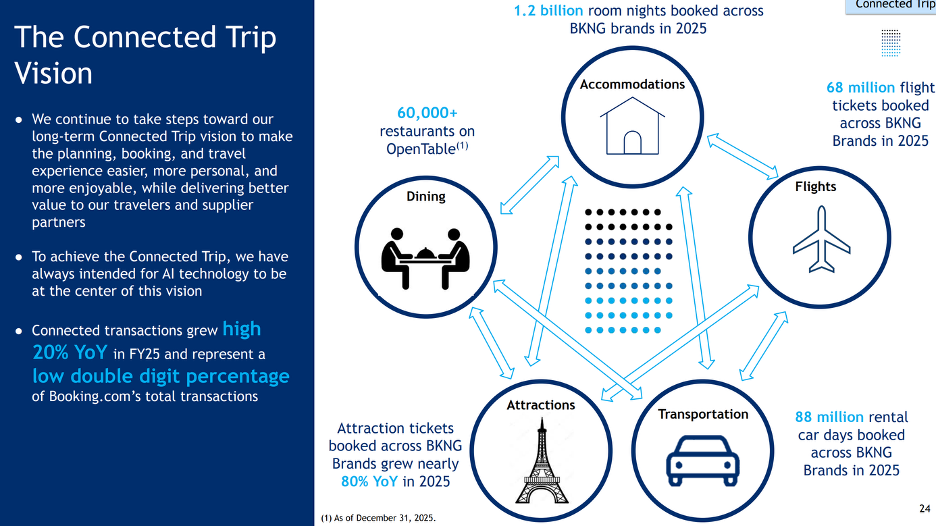

They booked 1.24 billion hotel rooms in 2025.

They have improved the business now over the last several years with 2/3rds of traffic coming direct to them.

Their loyalty program is driving more night bookings on the platform and building customer loyalty.

They have grown their alternative accommodation business to 2/3rds the size of Airbnb’s.

They also sold 68 million airlines tickets and 88 million rental car days in 2025.

CEO Glen Fogel has been at the company since 2000 and running it since 2017.

Over his tenure, the company has consistently grown revenues from $12.6 billion to $27 billion, a respectable 10% CAGR.

EPS though has growth from $47 to $166, a 2.5x increase.

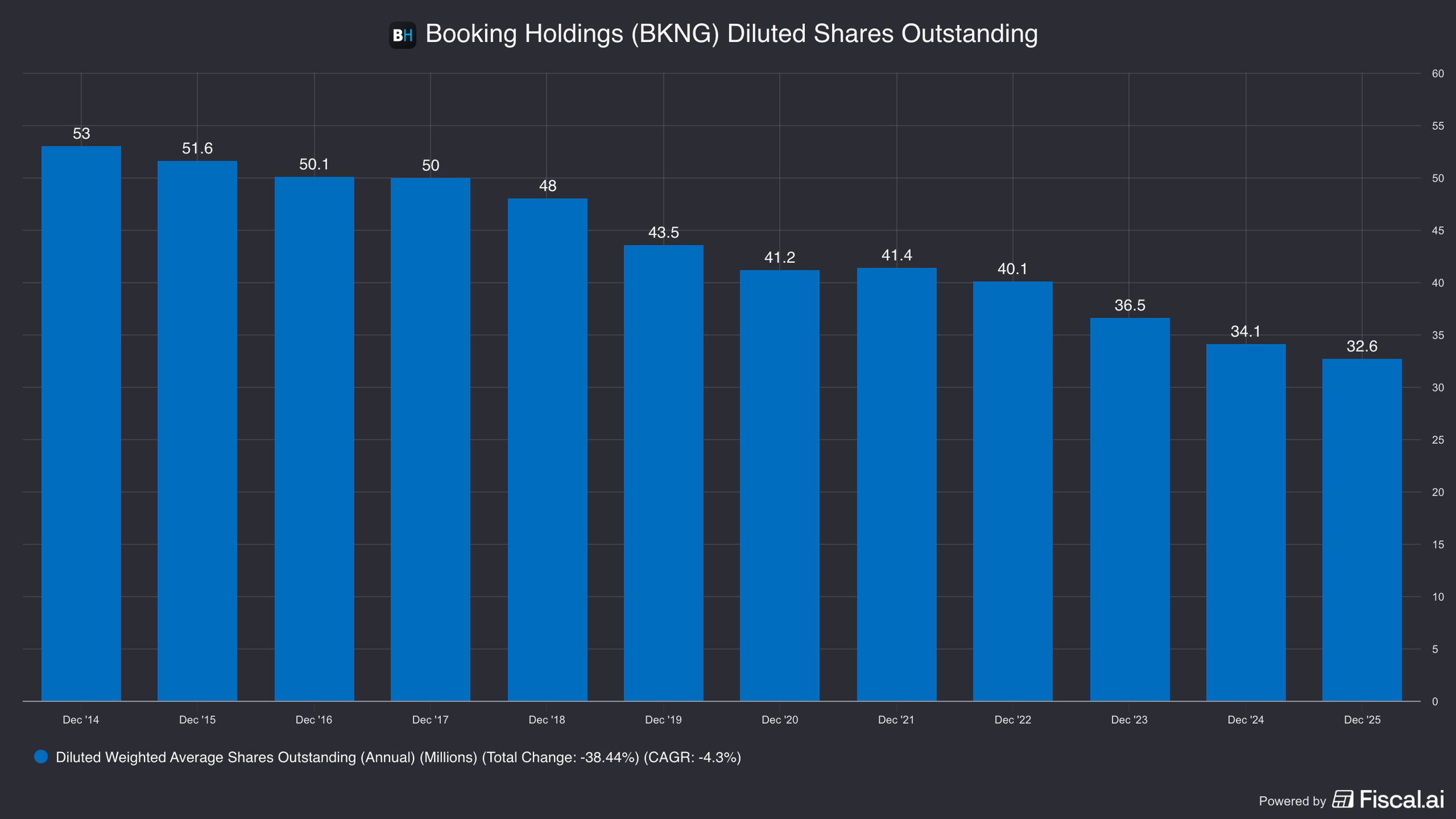

And their share count has dropped 35% from 50 million to 33 million as they aggressively divert cash flows to repurchases.

So why is the market doubting Booking.com, sending shares down 25%?

It’s becoming an old story now…

AI.

The concern?

AI agents can just search the entire web, scrapping each hotels website, comparing rates and booking a hotel for the customer, all without the need of Booking.com.

Sounds scary.

Could that be true?

Well, Bookings main value add is helping connect hotels to customers and customers to hotels, and in theory AI could do that just as well as them, maybe even better.

So perhaps the real question should be, why is Booking.com ONLY down 25%?

As people lean on AI more for everything, isn’t it obvious that they will use AI to book travel too?

What are we missing here?

We cover all of this and more in this week’s Five Minute Money.

Business.

Booking.com’s business is relatively straight forward.

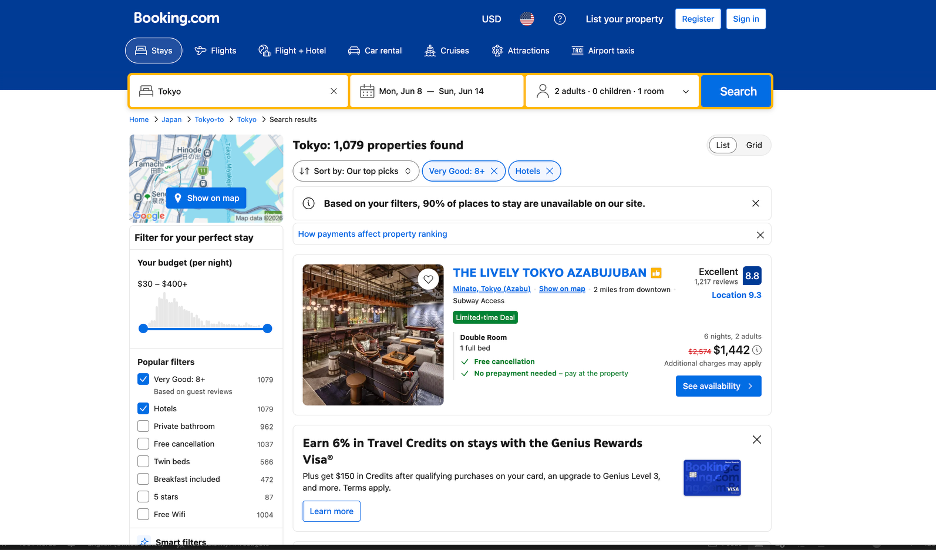

They have a website that customers browse to find hotels and alternative accommodations. After they find the best one at the cheapest price for them, they can make a reservation right there on the site.

This business model is called “OTA” or online travel agency.

Booking.com actually traces their history back to Priceline, who acquired them in 2005.

Booking.com started in the Netherlands and their value prop in Europe is particularly strong.

There are over 100,000 small independent hotels in Europe and aggregating all of them onto the same platform was real value-add as customers could go to one site to search all available hotels and it made it much easier for hotels to find customers.

As a hotel owner, you want your capacity to be as high as possible. And if you have an empty room that goes unrented, you just lost money.

You would be happy to give a platform like Booking 15% of your room price in order to get that sold and keep the other 85%.

This is what Booking does for hotels: they generate them demand that they wouldn’t have had otherwise.

Sure a hotel could run ads on Google and elsewhere, but if you talking about a small hotel, they are not sophisticated enough to do that in the most cost effective manner.

Instead, you sign up for Booking and tell them how many rooms you have and what price you want and Booking will spend money on Google Search ads to find your customer for you. (Hotels can link to Booking directly or through the Extranet)

Since Booking has scale, sophisticated data scientist, and a brand name, they are able to get more clicks on an independent hotel owners’ listings then they could themselves.

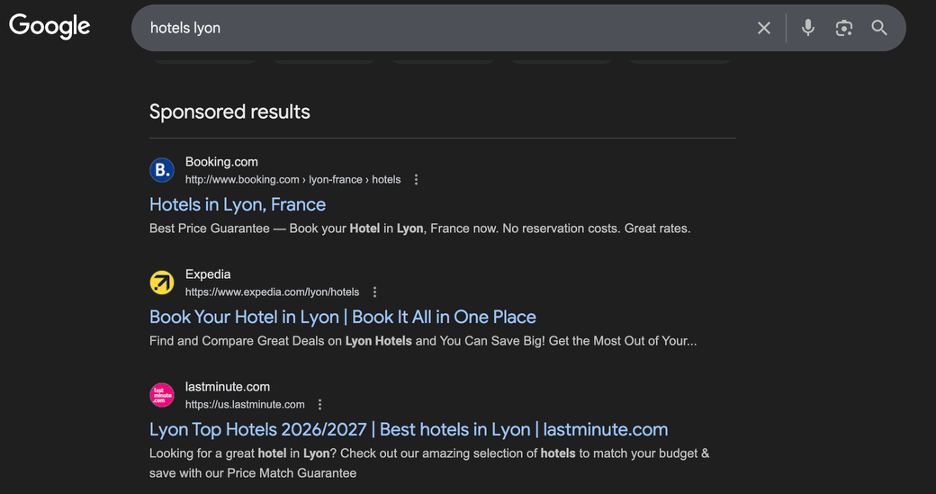

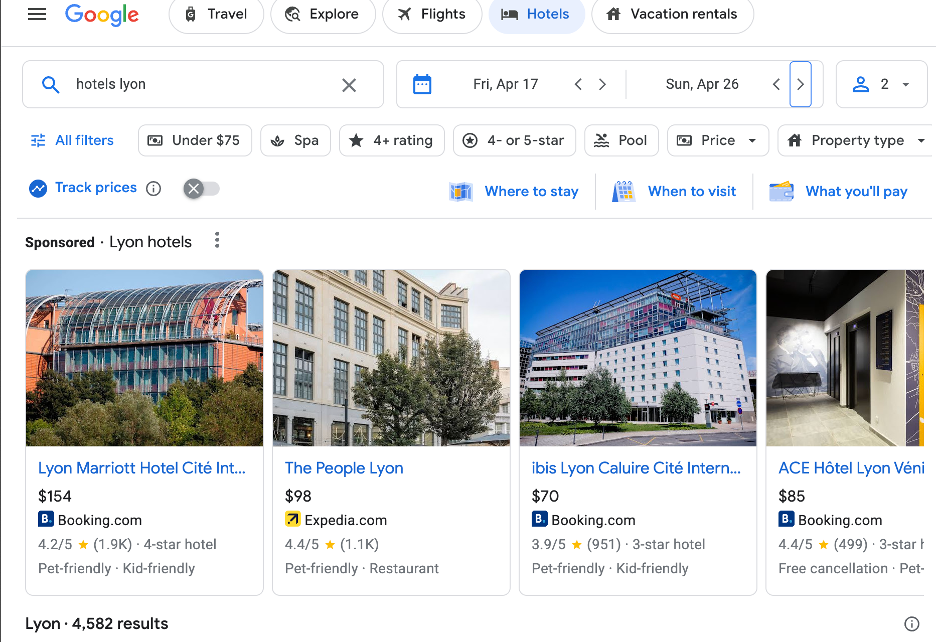

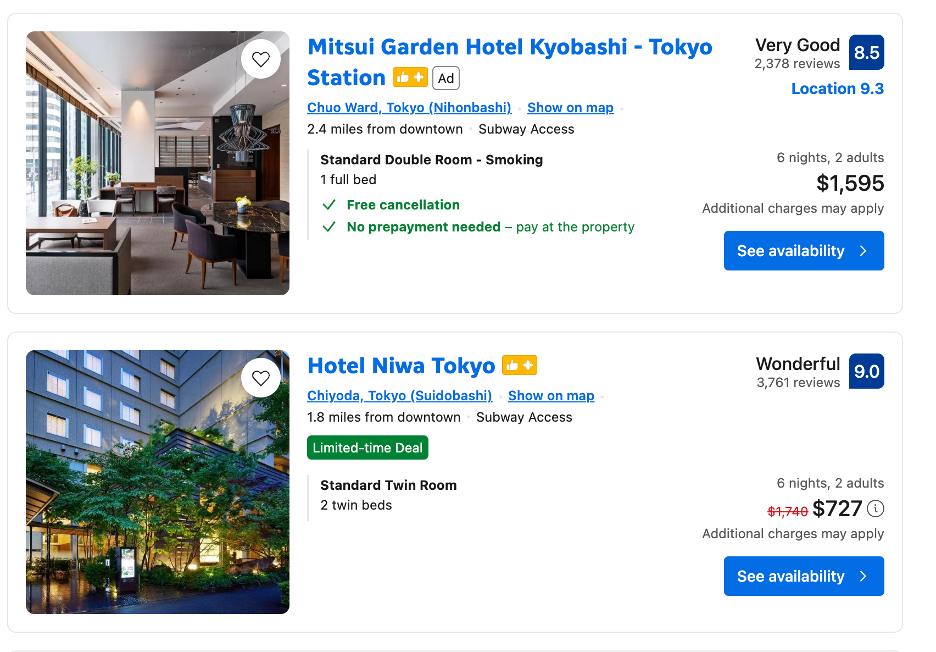

In fact, Booking is one of Google’s biggest customers, spending over $5 billion a year on the site buying words like “hotel Tokyo” or “hotels Lyon”

While many users still start their travel search on Google and use Google Hotels or Flight, Booking pays to make sure their listings are shown there. Below you can see several Booking's listings.

And as they build up their brand it does 2 things for them:

1) It lets them pay less to acquire a click because their more recognized name means people are more likely to click it (so cost per action is less)

2) They can go direct to the customer, with customers starting search on Booking.com or their app.

We will talk more about this, Google competition, and competition from Airbnb and Expedia later on.

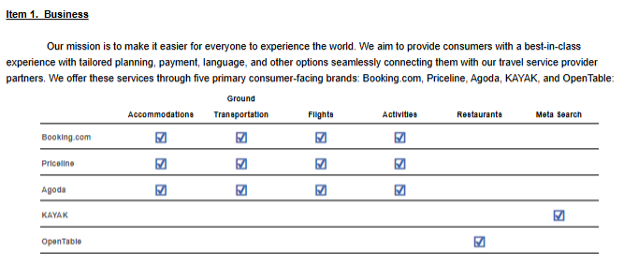

While Booking.com is their main brand and the bast majority of revenues today, they still own 4 other main brands.

Priceline, which is used for the discount market for flights, hotels, and car rentals in North America.

Agoda, which is an OTA similar to Booking, but is very popular in Asia. In fact, the mention this platform as part of their Asia strategy because Agoda does a good job of localizing the platform to each Asian countries home market. They are growing room bookings low double digits in the Asia market, with help from Agoda.

Kayak, which is a meta search engine. This means it will search across all of the OTAs (including competitors like Expedia) for the best price. This business has been under heavy attack from Google, which does the same thing.

OpenTable, which is for restaurant reservations. They restaurant pays them a small fee for each table booked.

In 2020 they took a $1.1 billion impairment charge related to OpenTable and Kayak. They took another $457 million impairment charge on Kayak in 3Q25.

Historically, Booking.com has been strongest in Europe, but has more recently focused on growing the U.S. market.

The U.S. is a bit different than the rest of the world with very large hotel chains though. As a result, many people book direct through Marriott for example and are in Marriot’s Bonvoy program.

The U.S is a low double digit number of global room nights, growing mid single digits, and Asia is about a quarter, growing low double digits.

These are two key growth markets for them.

They are trying a mix of things to grow the U.S. market.

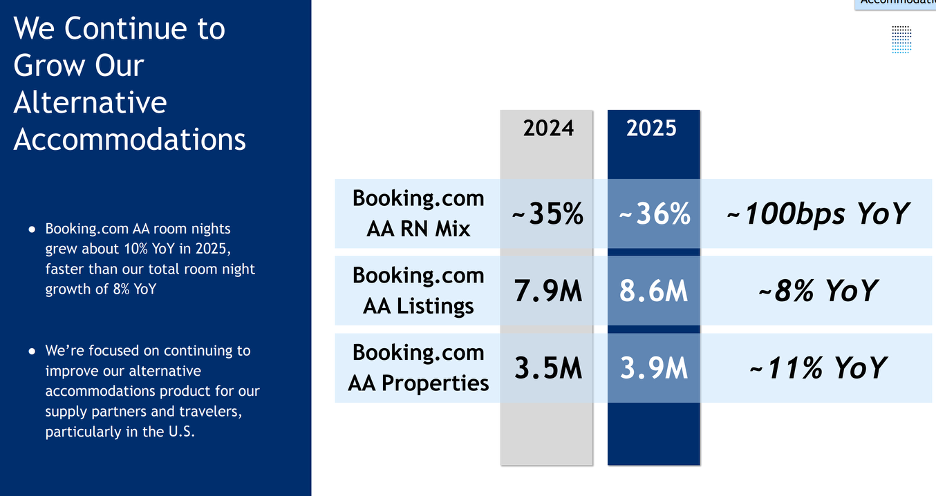

One initiative (and this applies internationally as well) is alternative accommodations.

This is what Airbnb has thrived at.

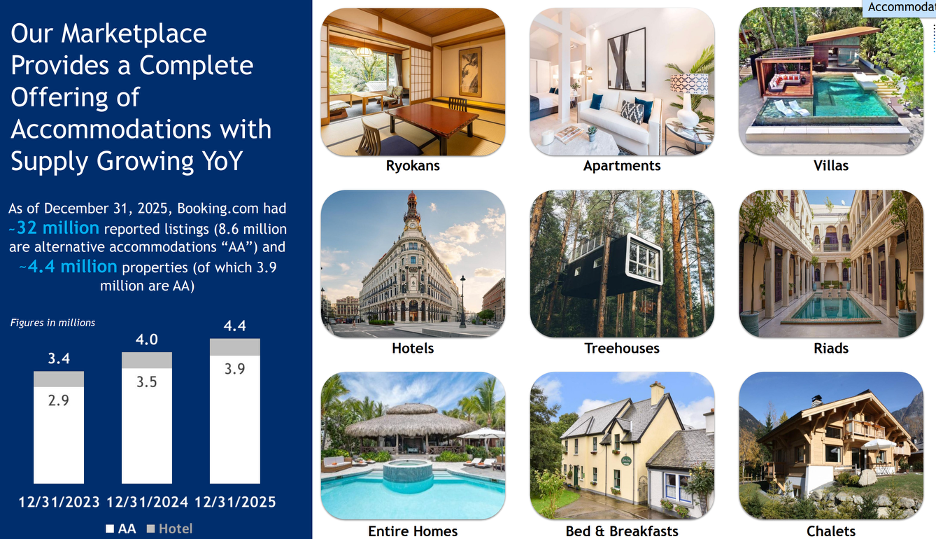

Booking though is already 2/3rds the size of Airbnb in the alternative accommodations market.

Getting more homes and property managers to sign up for the platform is part of their strategy to grow more in the U.S.

They also are leaning into B2B partnerships, where they help power the rewards selection of various credit card companies and airlines loyalty programs.

Lastly, they are doing traditional brand advertising to build up their brand in the U.S.

The hope is consumers start their searches on Booking.com, instead of Google. They also now offers flights on Booking.com so users can book a “connected trip”, where Booking sells them everything.

Historically, this hasn’t worked so well because consumers don’t tend to want to book everything at once. They usually book a flight, and then hotels later, and then attractions last.

The new hope though for the connected trip (and risk to Booking) is AI agents.

Booking is investing heavily into AI agents in order to build the connected trip with better recommendations and personalized travel concierge.

While the connected trip has remained an illusory target for most OTAs, Booking is reporting some success with it. They disclosed that a low double digit of all transactions are now connected trips (trips where the traveler books more than one vertical).

Airline flights booked jumped 37% y/y in 2025, reaching 68 million.

While airlines don’t make them much (if any) money because the economics are much tighter there, they do help build consumer loyalty and habit to Booking.com, which is key.

While flights don’t get discounts, they do count toward a user “leveling up” in their Genius Loyalty program, where a traveler needs 15 bookings year to reach the highest tier with the best discounts on hotels.

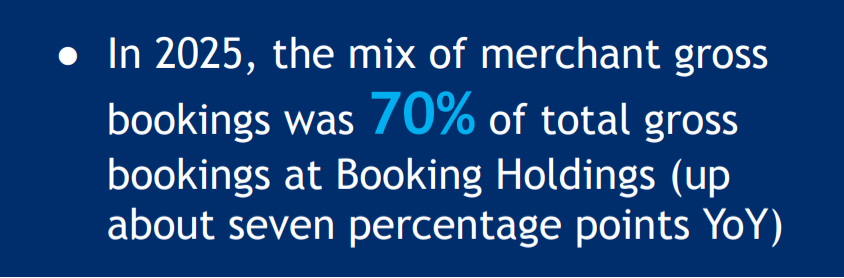

Key though to the connected trip and the improvements in their business has been leaning more on the Merchant model.

Business Model: Agency vs Merchant.

There are two models to this business.

Agency and Merchant.

Under the agency model, Booking.com just connects the customers to the hotel and passes off the payment to the hotel, which usually happens at check out. They then remit the ~15% commission Booking charges back to the hotel.

In the agency model, the hotel is the merchant of record.

In the merchant model, booking is the merchant of record.

This means a few things. First, Booking.com takes the payment (usually upfront) and is responsible for any chargebacks or fraud.

Under the merchant model, Booking generally guarantees a minimum amount for the hotel room, but the hotel doesn’t have say over the final price.

This gives Booking lee way to lower prices if they think it will help boost bookings, or increase prices when demand is high to make a higher margin.

So a hotel room that usually goes for $200, and the hotel usually gets $170 after Booking’s 15% commission, can instead be sold for $185, eating into Booking’s commission, but increasing the hotel nights they book.

Conversely, they maye decide they can get $210 for it, making a little more than usual in commission.

Their pricing algorithm is far better than anything the hotel uses.

Overtime Booking has shifted the majority of their business to the merchant model

They like this because they control the payments, which allows them to offer customers more payment options like AliPay or BNPL.

It also let’s them offer discounts to customers in their Genius Loyalty program.

And is critical to their vision of the connected trip, where they cross sell flights, reservations, transportation, and attractions.

They also have a B2B business were the power the rewards sits for airlines and credit cards companies, and the merchant model makes this run much smoother

It also makes Booking.com responsible for customer service, which can be a good or bad thing.

If they handle issues well for a customer, like rebooking flights after they are canceled, then it can make a customer want to use Booking over going direct to AirFrance for example.

The merchant model also is critical for alternatives accommodations (which is apartments and homes like Airbnb, because there is no check out desk to take payment.

There is also lower cancellation rates when a traveler pays up front and the working capital dynamics are much better for booking (get cash up front).

Lastly, they make a little more margin on the transaction. While they are now paying interchange fees that they didn’t before because they are handling the transaction.

Since they have a lot of volume, they can negotiate this down a lot. Then when Booking pays the merchant, they issue them a virtual credit card (VCC). This VCC has a higher take-rate or 2-3% and since Booking is the issuer, they get rebated back the issuer fee, which can be around 1-2%. Thus payments are either a net neutral or small profit center for them.

Making money on forex is also a component of this. Since they have customers paying in all sorts of different currency, they internalize some of that currency conversion, while still making the typical forex spread (i.e. charging $1.28 for a £1 instead of the market rate of $1.25. A small spread on currency conversion is common).

Monetization.

Booking makes money by charging a standard 15% commission on hotels, but that can range from 10-25% depending on the particulars of the market.

A hotel can enter the preferred partner program, which gives them a badge and a boost in visibility in search results in exchange for an extra 3% fee.

The thumbs up denotes these hotels below are in the program and their listings were top when searching “Tokyo”.

Hotels can also pay more for a visibility bump. There isn’t clear data on this, but commissions can rise as much as 40% or higher if a hotel really wants to be aggressive. They may do this if they are having a really hard time filling rooms at a certain period of the year and only run that temporarily.

Of course though hotels have options in how they can get that booking.

Competition.

There are three main OTA players now: Booking, Expedia, and Airbnb.

We will go into more qualitative competition in a moment, but let’s first see how they rack on fees.

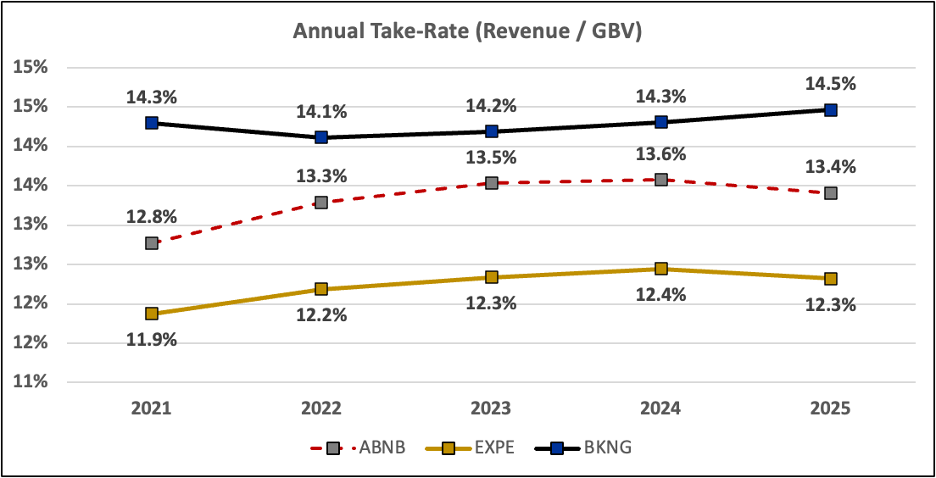

Generally speaking, Booking’s total take-rate (that is what their revenues over Gross Booking Value or GBV is) is higher than peers.

Airbnb’s take-rates is anywhere from 12-20%. They used to charge the host just 3% and then the guest the rest, but are starting to shift that model to just charge the host.

Expedia’s standard rate is 15%, but large hotel chains (which is a lot of their business because they are bigger in the U.S.) can negotiate it lower down to the 10% range.

We can see total take-rate’s for competitors compared below.

Note the take-rates look a little lower because GBV includes taxes and other local fees that they do not charge a commission on.

So booking is a bit more expensive, but for most of the hotels that they book for (Europe-heavily dependent) Expedia is a much weaker player there and Airbnb doesn’t really offer hotel (this is changing a bit).

As mentioned prior, what hotels really care about is getting the room filled, and paying a little bit more to get an occupancy is much preferred to letting it go vacant.

So as long as Booking can deliver a booked room better than competitors, they can maintain that slight premium take-rate. (Generally speaking, though, they are all in the same ballpark).

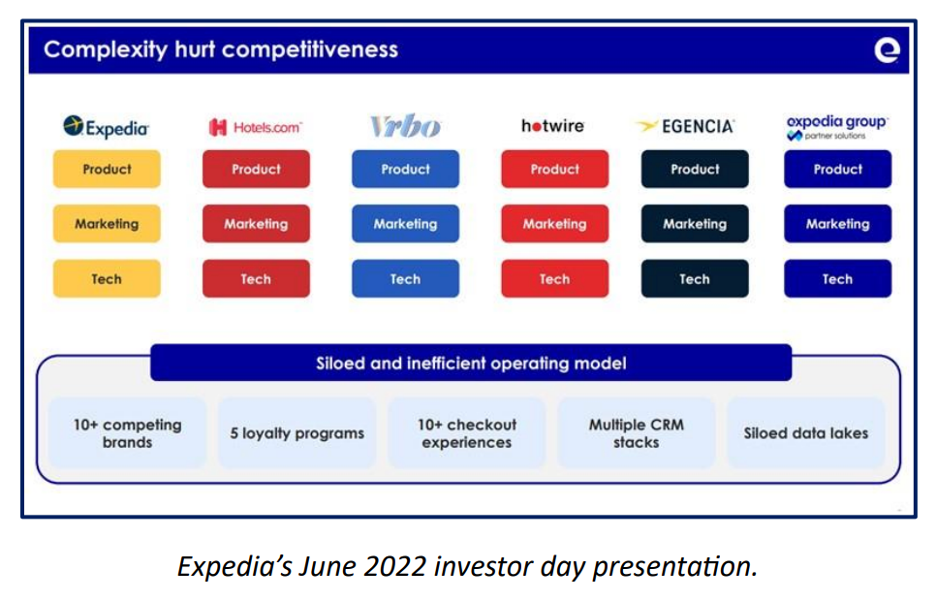

Expedia is their most direct competitor, but they have been mismanaged for years. They had way too many brands: Travelocity, Orbitz, Trivago, Hotels.com, VRBO, HomeAway, and many, many more.

All of this led to very inefficient marketing where one brand was often bidding against another for the same customer.

Efficient marketing is key though to getting the customer to the site.

Supporting too many brands also meant low customer loyalty to all of them.

It also meant supporting different technology back-end for each, which makes it very hard to reiterate on features and improve the platform.

They have since focused on just their Expedia, Hotels.com, and VRBO brands. (VRBO is for alternative accommodations, Expedia is everything).

Booking is still bigger with $186 billion of GBV vs Expedia’s $120bn.

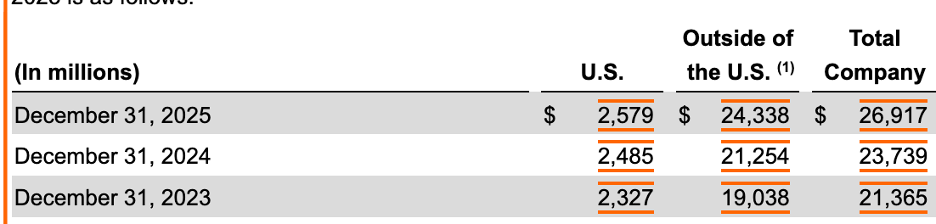

Booking only has about 10% of revenues from the U.S (below) whereas Expedia is around 60%.

Expedia has had a harder time cracking the European market because it took years of boots on the ground to acquire all of those independent small hotels and it doesn’t seem like Expedia has the appetite to try to recreate that, especially given Booking’s existing dominance here.

While it seems like Expedia is becoming a better competitor, Booking has shifted a lot of traffic direct to their app and website, which will make it all the harder for them to gain a strong European business.

Booking and Airbnb compete primarily in alternative accommodations (AA hereafter).

Airbnb has about $91bn of GBV vs Booking’s estimated ~$61bn ($186 billion in total though)

Booking has about 3.9 million AA versus Airbnb’s 8 million.

So if a guest wants an apartment or house, Airbnb is still #1 there.

But Booking still has an AA business that is 3/3rds the size of Airbnb’s.

Airbnb has stellar UI, brand recognition, and the most independent hosts/ listings.

Booking focuses more on professional property managers who may manage 100 units or a dozen homes they rent out as a business. This has been a pretty good area to focus on for them because it is easier to acquire more listing this way and there is less issues with the a property not being what is expected.

Airbnb’s issues is that some host’s properties disappoint and so there is a little bit of a risk in booking an Airbnb. They are trying to address this with guest ratings, preferred hosts, and by pulling bad listings off of their platform.

Airbnb has a particular stronghold in the United States and is growing elsewhere nicely too.

The value props aren’t totally similar, but they do overlap.

And Airbnb is getting more into hotels, starting with boutique hotels.

They acquired a small business called HotelTonight to get them a foothold.

But if they go too mainstream with hotels, they risk losing their identity.

They also have Experiences though, which are individualized travel attractions hosted by an individual that can help them grow, but it is hard to scale.

Other competition comes from users booking directly, but that is more a threat with big chains like Marriot or Hilton, than these tiny 10 bedroom hotels in the South of France.

Their real competitor is other companies—namely Google—that can help connect travelers to the long tail of hotels.

As we already mentioned though, Booking just pays Google a fat fee to stay on top of the search results and win that business.

There used to be a worry that Google would get more into this business and let guest book the hotel directly on Google, but Google has no interest in getting involved in the transaction because then they are respsoible if something goes wrong and needs customer support.

And historically Google has been allergic to things that require a lot of people to scale.

Could AI change this all though?

The AI Risk.

The AI risk is two-fold:

1) Google Search, an important traffic avenue for booking, gets displaced by AI Chat.

This isn’t a big risk though because Booking can simply start paying the chat bots to showcase their listings there.

2) AI Agents do all of the booking on behalf of a guest and are willing to scrap the internet for that random B&B with 8 rooms in Bruges.

This is a more formidable risk because it threatens the heart of the value prop of booking—connecting hundreds of thousands of small hotels to millions of travels.

AI could theoretically recreate that network effect and help surface relevant results for travelers.

That is the first concern. The second is that the AI agent can do the booking of the hotel too, cutting Booking.com out all together.

The AI agent can find small boutique hotel’s website and book directly on it, on behalf of the customer.

Anthropic even has something called MCP or Model Context Protocol and that allows an AI agent to have access to a hotels room booking system and rates.

In theory, this could destroy booking.com and totally eliminate the need for the middle man.

So Booking is toast?

Not exactly.

While it may not be the most impressive rebuttal, the truth simply is business is much harder in practice than people imagine.

These small hotels are not tech savvy enough to host a server side MCP.

And they themselves may only feel comfortable doing so after talking to an actual person and would need help installing it.

In all likelihood the AI companies would need boots on the ground to educate hotels and help them switch.

Which would be a horrendous business proposition for them.

The AI could try to navigate the website’s directly, but that would require constantly scrapping them for new data on pricing and bookings, which is expensive and many websites have protections that make this harder.

Today the failure rate of AI doing this is very high. It could get better in the future, but going through the front end is still a very inefficient model.

Instead, they can just plug into Booking.com.

Booking has their own MCP and already connects to all of the hotels and alternative accommodations.

Plus, and this is big, Booking.com is the merchant of record and can handle the payment.

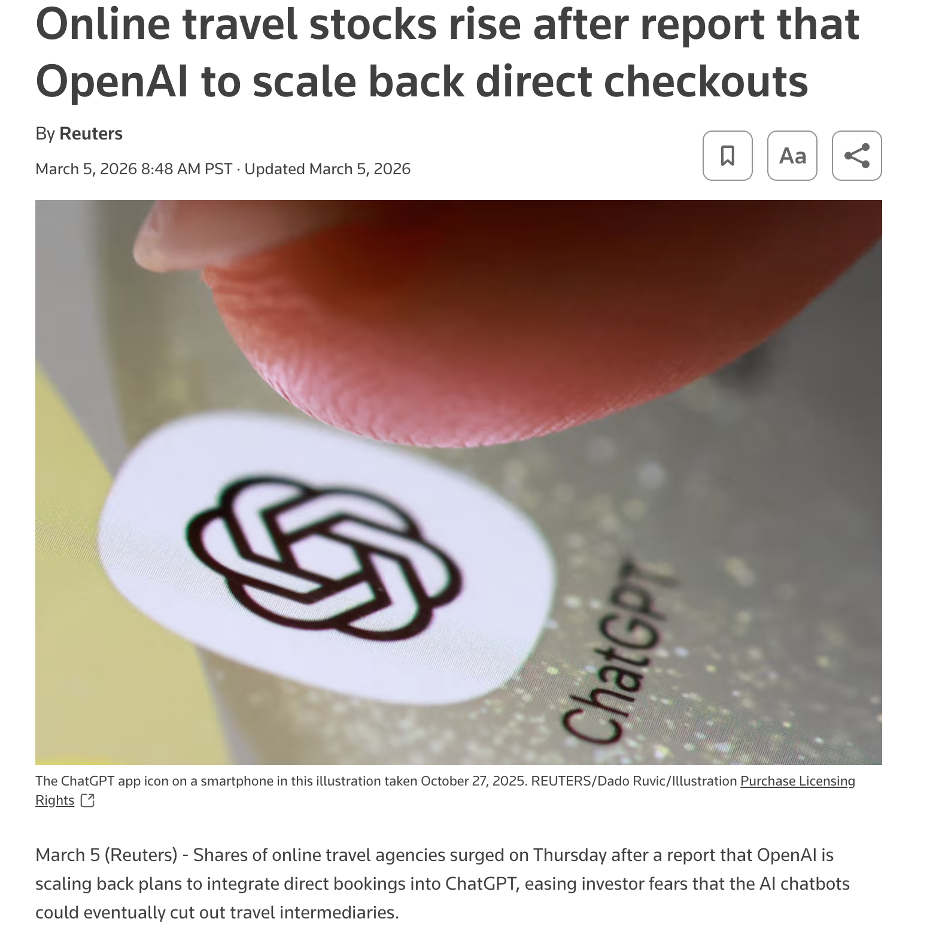

OpenAI has already backed out on the idea of having their own check-out button, realizing it is harder than it sounds.

This is particularly true in travel where you will have to handle cancelations and complaints.

If an AI Agent booked everything on behalf of the customer, the customer would expect the AI agent to be responsible in case something was wrong.

But they wouldn’t be.

There would be no help or customer support to call if they hallucinated the wrong date or if you wanted to cancel because of, say a war in the middle east.

Booking has that customer service that does all of that already.

In OpenAI offered a check-out and didn’t do that, it’s just a worse product.

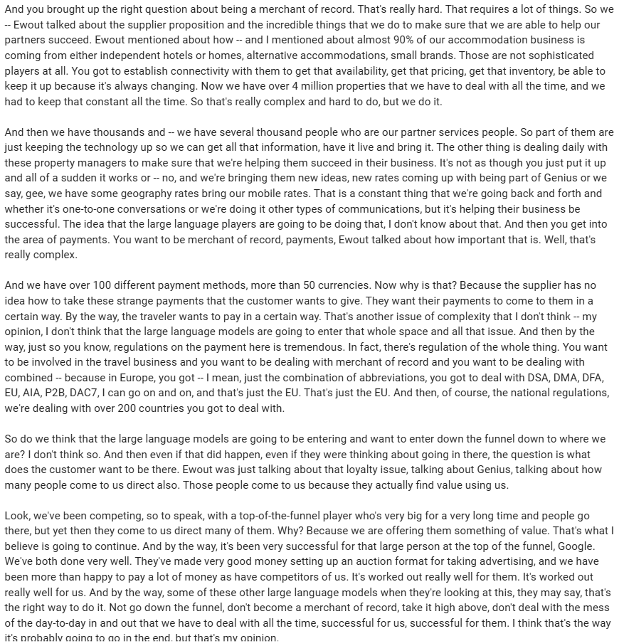

Booking CEO pushed back against the agent model below. Note he says they have thousands of people who just keep the technology working so they can get live rates and rooms from all of their many, many partners.

He also notes that if you process the payment, now you are dealing with forex, 100+ different payment mechanisms, merchant agreements, fraud prevention, and a lot of regulation—especially data privacy regulation in Europe.

It’s not that OpenAI couldn’t theoretically do all of this…

It’s just that why would they want to?

Google was essentially in the same postion for a long time and could have taken the entire OTA market if they really wanted it.

Instead they do the easy thing: sell high margin ads and collect $5 billion+ a year.

Right now Bookings entire earnings are only a little over $5 billion a year, so the upside in entering this business is very limited.

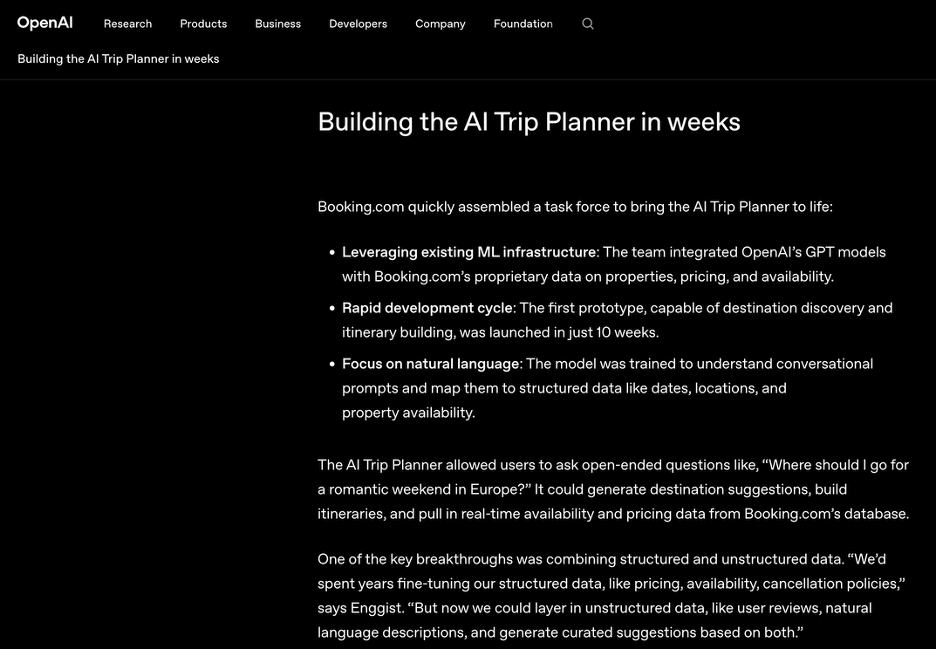

OpenAI is instead partnering with Booking.

The player most focus on building an AI travel agent isn’t OpenAI, but Booking—and they are using OpenAI’s model to do it., but it lives inside of Booking.

While it seems likely that overtime more people will start travel search on chatbots, Booking will simply shift some ad budget from Google Search to chat.

And to the extent they can actually build strong AI agent with more data live on hotels, attractions, flights, etc., then AI could actually be a positive for them.

In fact, they noted that AI already helped reduce customer service costs 10%.

And they are incorporating MCP on their server-side so the AI models work through Booking, not around it.

All in all, it seems like a fair response.

The risk of course, like with most companies, is we get super intelligence and AI can just do everything better with no mistakes, and everyone has their own AI that can cut through all existing infrastructure….

It doesn’t seem so likely to me anytime soon.

Valuation.

At a stock price of $4,240 for a market cap of about $138 billion.

Note that they will split their stock soon 25:1, which will lower their share price to $170.

After backing out stock based comp and amortization of debt discount, you get free cash flow of $8.4 billion.

This puts Booking under 17x free cash flow.

Most of which has been going to buy back shares.

Since 2015 share count has fallen 37%.

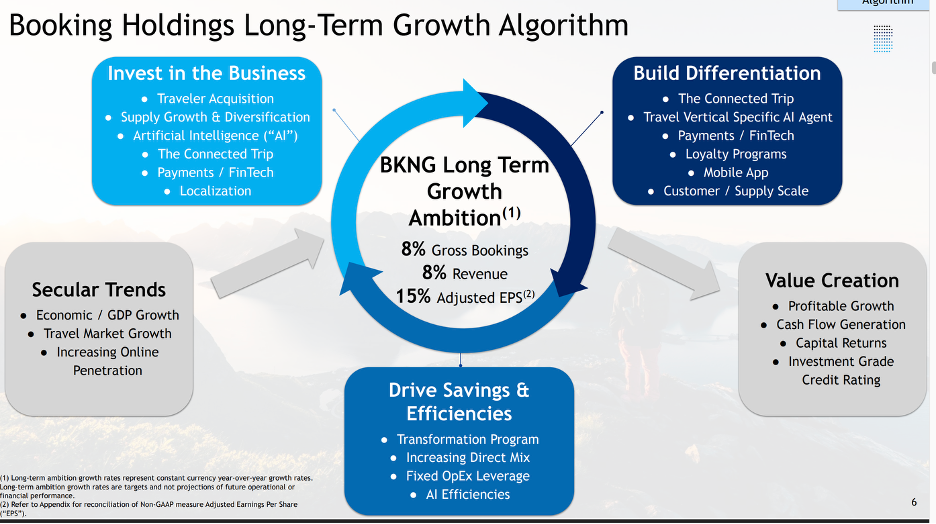

They are guiding mid-term to an “8-8-15” framework.

This means 8% gross bookings growth, 8% revenue growth, and 15% earnings per share growth.

Holding the multiple steady at 17x, which isn’t a demanding multiple at all for the growth, an investors return would be the same as the earnings growth—the 15%.

(The earnings per share growth takes into account buybacks, so we don’t need to account for them by adding the earnings yield to this formula.)

As for what is driving that growth, Booking lists several below.

Including simply booking more rooms with existing hotels.

You could say though that for a high single digit top line and low double digit bottom line grower that a low 20x multiple would be more fair.

If they grew cash flow per share 15% for 3 years and also saw their multiple expand to 20x, that would be a 21% return.

On the other hand, if investors started to get bearish on the terminal value of Booking because it looks like they are getting disintermediate by AI, the multiple could compress much more.

Maybe to even 10x, which would erase any gain.

Of course it is also possible the travel market slows.

Or new ways of booking hotels becomes more popular.

Ultimately, an investor will need to decide for themselves what they are comfortable assuming.

For more on Booking, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.