ServiceNow Update: Desperate Pivot or Clear Opportunity?

Get smarter on investing, business, and personal finance in 5 minutes.

Business Update

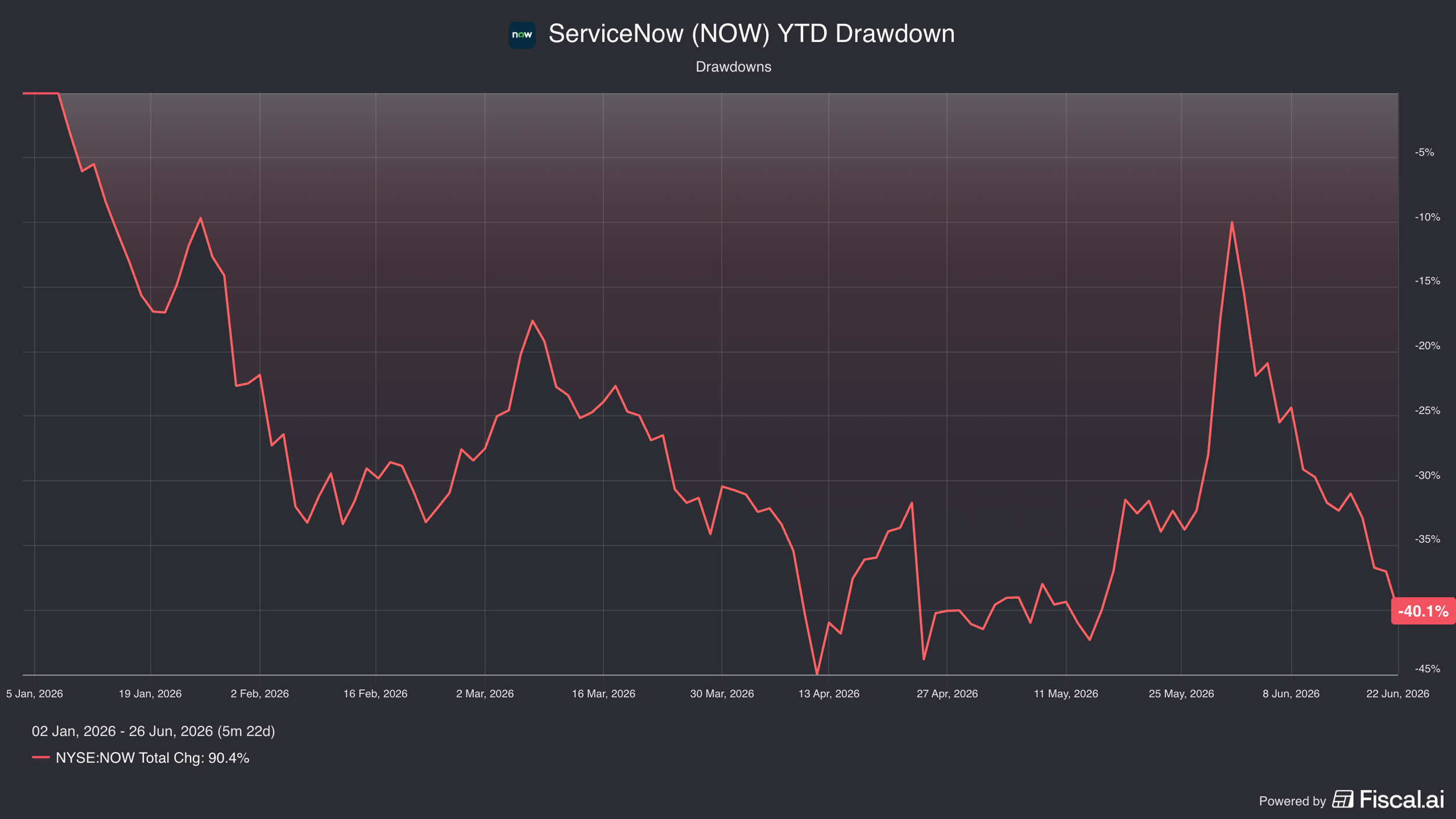

ServiceNow stock is down -60% from its peak.

Year to date, it is down -40%.

In this newsletter, I'm going to provide an update on ServiceNow, talk about what's changed with the business, if anything, and go over the AI fears and everything else that's happened in the past few months.

This newsletter is structured into two parts, 1) the updates, which are five different news items for ServiceNow, and then 2) we're going to move on to the valuation.

5 Updates.

Update One: New Products.

The big thing that's happened is they've had an investor day.

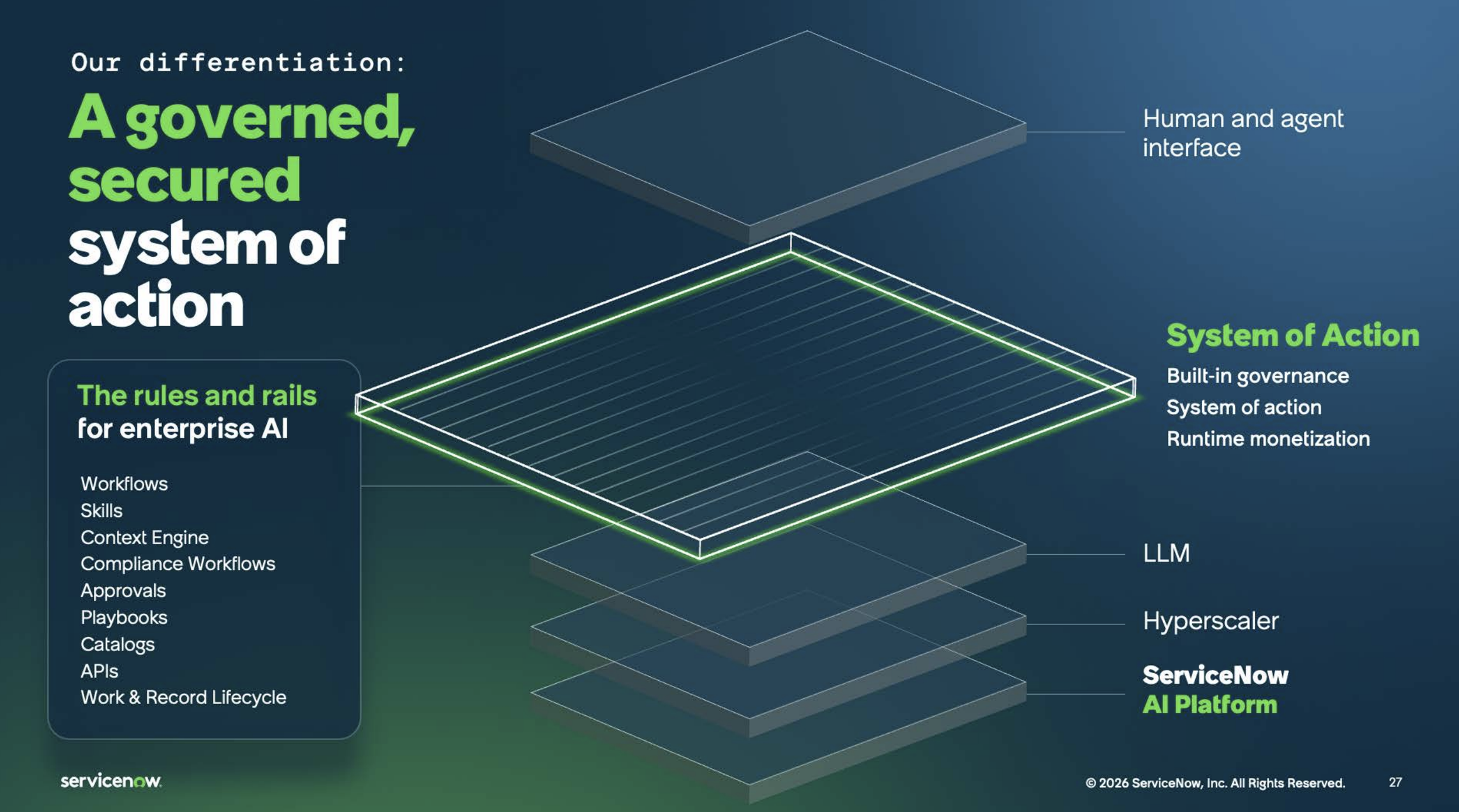

They've been out on a lot of conferences, and the big shift has been, at least in messaging, where they talk about becoming more of a system of action.

If we rewind a few years, everyone would talk about ServiceNow in terms of workflows, ITSM, IT service management, which is where they got started, and this is primarily a ticketing business.

You have an issue with a laptop, a login, a password, it creates a ticket.

Someone looks at that ticket and tries to solve the problem.

Once it's solved, they close the ticket.

Now, though, they're moving beyond that into actually taking action, becoming an operating system for AI agents.

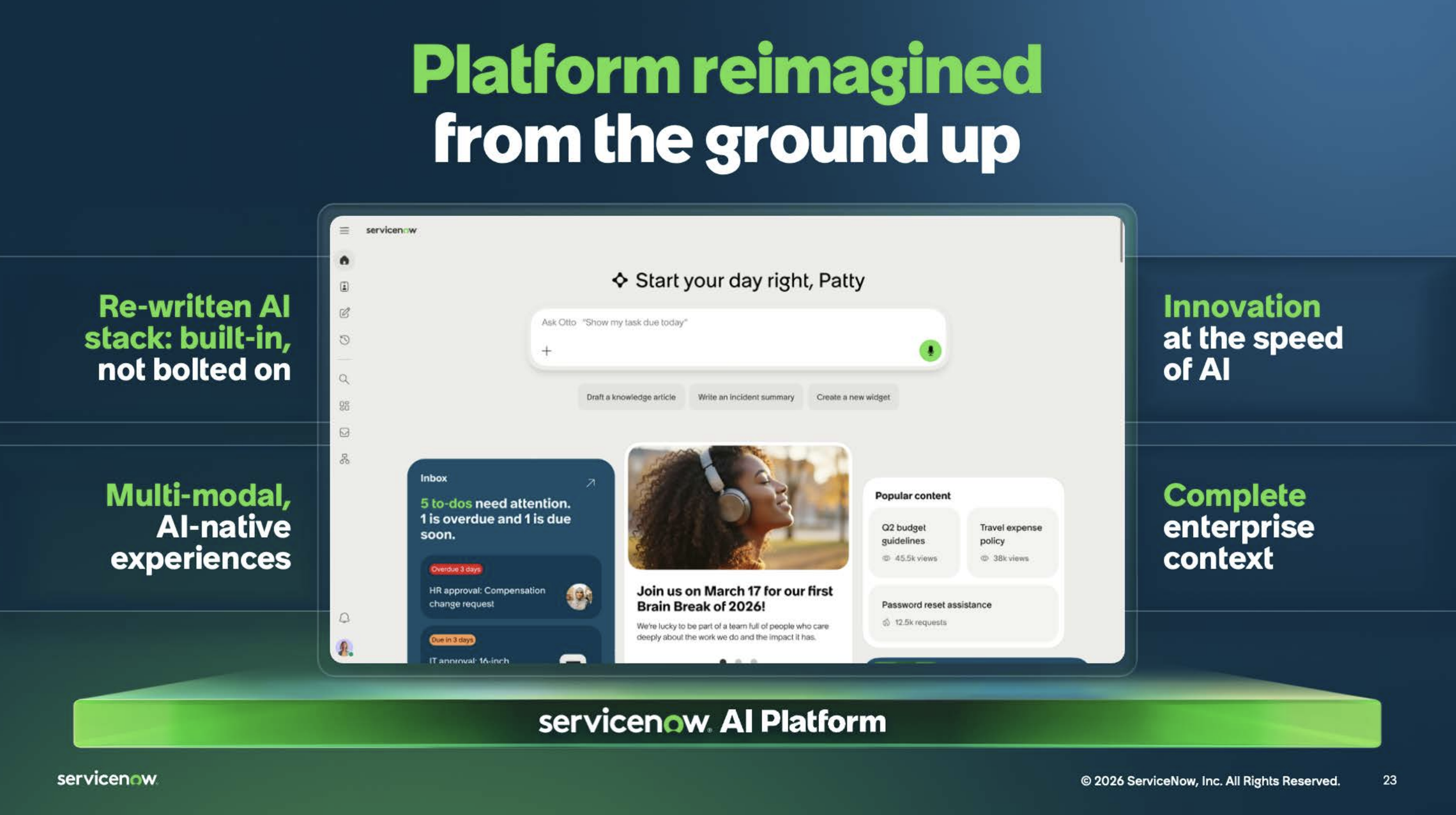

ServiceNow wants to become the AI control tower.

The idea is that ServiceNow is going to be the platform on which all of these different AI agents orchestrate their actual work, and what ServiceNow does is governance, security, and measurement, making sure these things don't go off the wall, which does occasionally happen.

Sometimes you'll tell an AI agent, can you please go ahead and reformat this data, and instead it will go ahead and delete it all and say, “Now you don't need to worry about that formatting, all your data is perfectly gone!”

There are a lot of horror stories about that, and companies don't want these AI agents roaming through all of their data with total autonomy.

Businesses want guardrails on it, and ServiceNow is trying to sell themselves as becoming the guardrails on AI.

They've come out with a few new products.

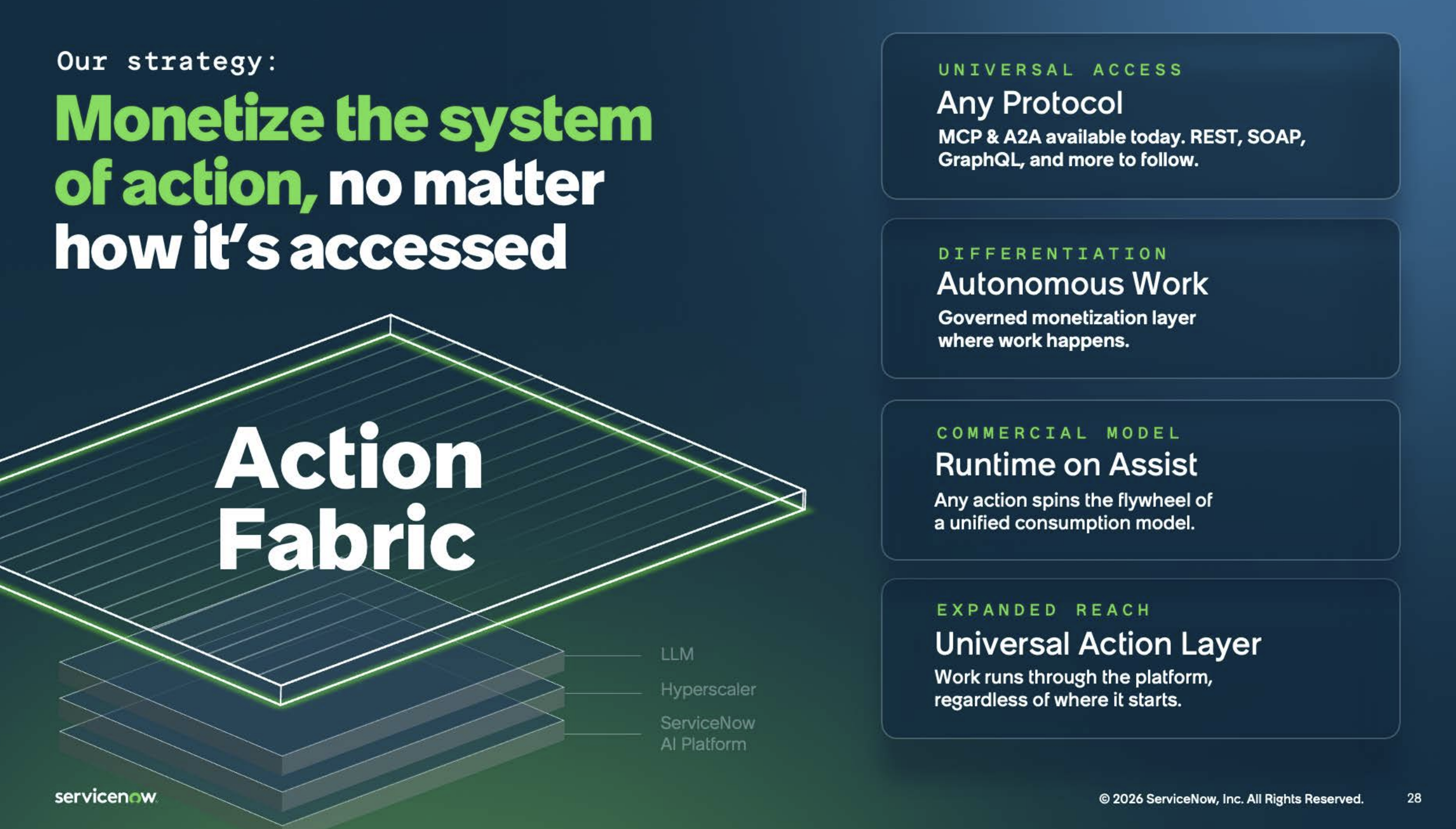

You have ServiceNow Action Fabric, which is a headless MCP server, meaning MCP is model context protocol, basically an API but for frontier models, and it's headless because there's no UI really.

Instead, Anthropic or Copilot directly interact with ServiceNow Action Fabric and take action inside an actual business's software to complete a task with no human in the loop.

This is more and more where the world is going, and ServiceNow is already trying to take their place there to make sure they're involved in this value chain where you have an end product of work, you have the model, and then you have ServiceNow in the middle.

In that way, they're trying to make themselves integral to a company's workflow process.

They also rolled out ServiceNow Otto, which is basically a way to route different requests to different AI agents, so some requests go to an agent in human resources, others in IT, and so on.

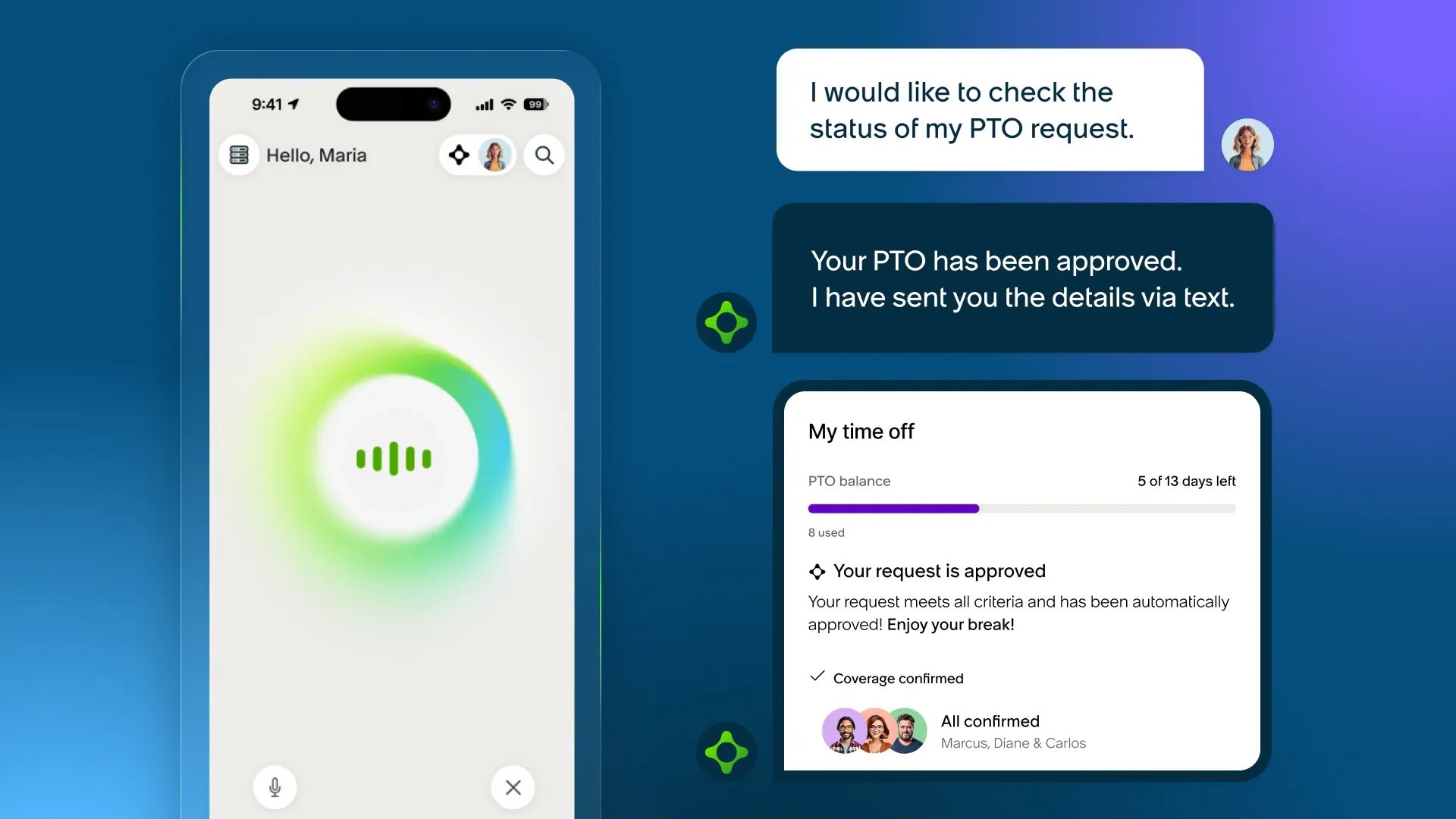

Update Two: A ChatGPT-Style UI Redesign.

The second update is that they changed their UI.

They redesigned their platform to be more AI native, and what that actually means is they basically copied ChatGPT.

ChatGPT has a great UI, and now if you're working in ServiceNow, you'll see it looks very similar.

You get that text box, and even the bar on the left looks pretty similar too, in terms of UI design.

Pretty smart, honestly.

That's all you needed to do.

Update Three: Guaranteeing AI Deployments Under 100 Days.

The third thing they talked about is guaranteeing AI deployments in under 100 days.

Imagine you're working at a company, you know you need to use AI, everyone's talking about it all the time, it seems super impressive, you see all these videos maybe on Twitter, and you're like, how does it know how to do all these crazy things.

And then you go to your business and try to use AI, and it just doesn't work.

No one really knows how to implement it in the actual business.

This is really, really common.

Most businesses that undertake an AI project do not get a positive return on it, and the project actually ends up failing because people don't know how to implement AI in a reliable way that leads to a better outcome for the business.

That is what ServiceNow is trying to do.

They have their own forward-deployed engineers who go into businesses and help them actually get outcomes with AI, because ServiceNow also has a platform on top of it to create custom apps and workflows.

This isn't new, but the new part is the commitment to actual deployments in under 100 days, and in many cases, they say they could get work done in a few days.

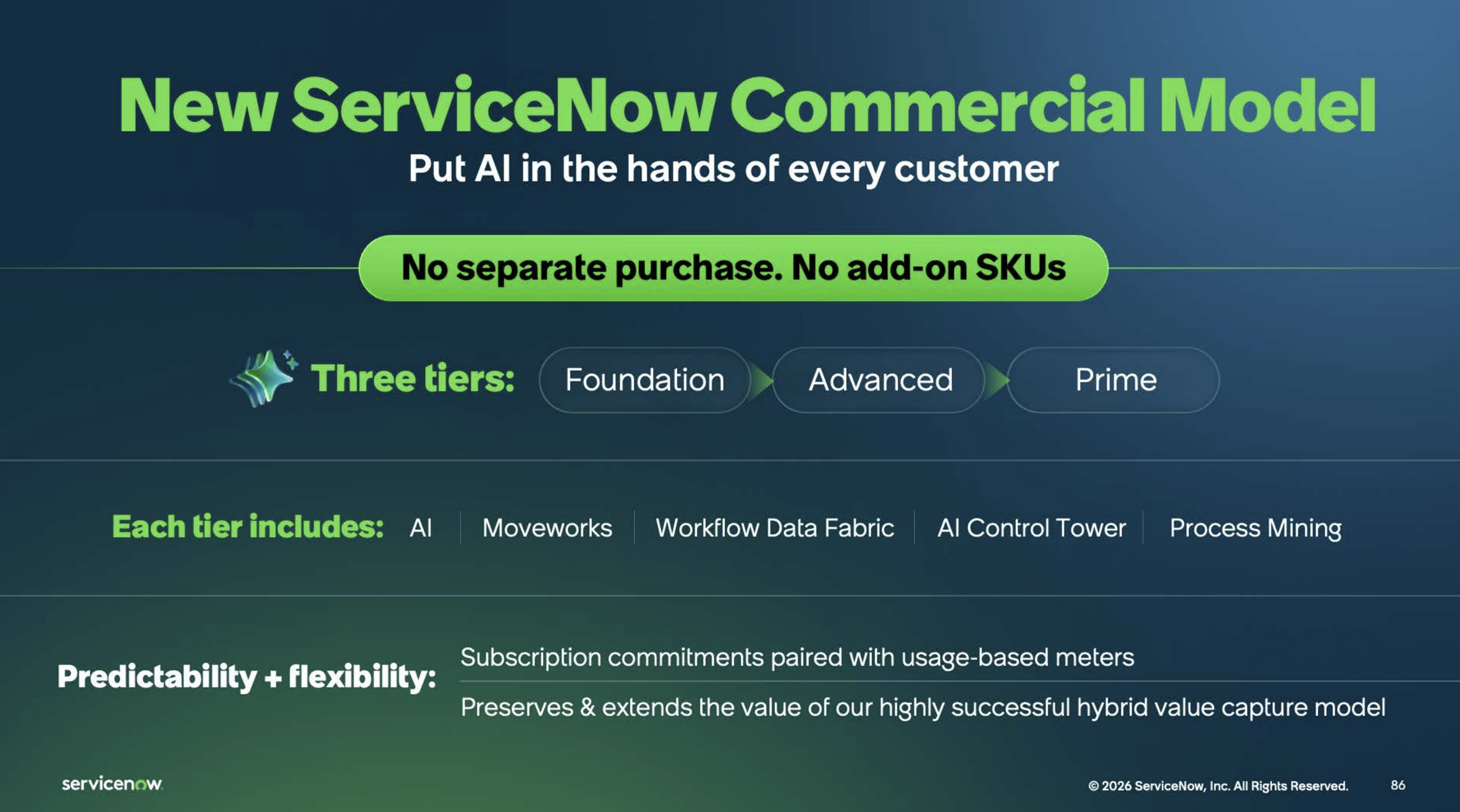

Update Four: AI Included in Pricing, Not an Add-On.

Number four is a change in pricing model.

Before, AI was an add-on to all of these different bundles, with separate pricing.

Now, any package you get at ServiceNow includes all of the AI features.

They have different tiers, but it includes the AI features, and you now pay a premium for an increase in usage.

AI is now standard, and that means they're better reflecting in their pricing what they're saying their strategy is, that AI is going to be critical to everything in the workflow process going forward.

It makes sense that it's not tacked on as an add-on.

Imagine buying software and being asked if you want it connected to the internet, able to get updates and synchronize across your organization, versus living locally on a file on your computer.

Of course you want it connected.

That's why all software is sold that way.

But when people sell AI products now, they're often sold as tack-on things, which is switching a little with this change in pricing model, and I think that makes a lot of sense.

It better reflects where we're going.

Update Five: The Vibe Coding Tailwind.

There's a lot of other things we could pull out from the investor day.

I'm just trying to give you some sense of where the business has been going and what they've been up to.

The last one that I think is kind of a funny one to note is that with all of this vibe coding, you now have a lot of code that you need to manage, and they expect lines of code to increase 20x by 2030.

Do you know who that's pretty good for?

The company that owns IT service management.

What's going to happen when you have all this code is you're going to have a lot more mistakes, a lot more errors, a lot more requests to IT, a lot more IT tickets that need to be created and solved.

That's going to be another big tailwind for the business, because they need to figure out some way to manage this expected incoming deluge of IT tickets.

That's in a nutshell some updates on ServiceNow.

No surprise that the business hasn't changed that much in the past few months, but you could learn more about the business if you check out the original deep dive I did.

Valuation.

Now let's move on to the valuation and some of the new figures they put out.

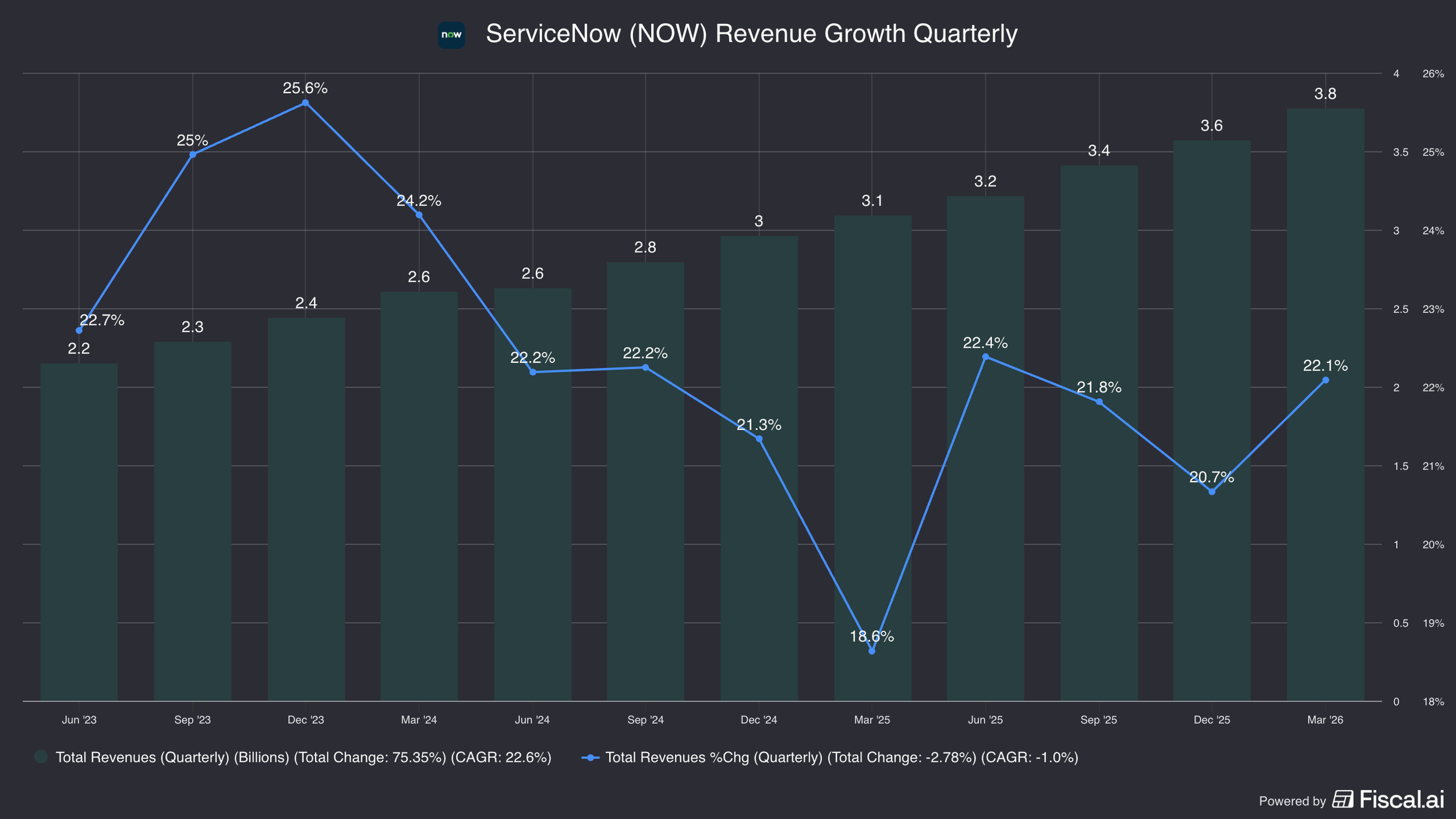

If we're looking at just the last quarter, you saw that revenue reaccelerated growth just a little bit, 22% versus 21%.

I never put too much weight on quarterly numbers, because so much stuff can impact them, especially in this case, it's just contract timing, one contract falling on one date versus another, which could impact the total quarter.

I don't love putting too much weight on single quarters.

For the whole year, though, they're talking about doing $15bn in revenue, and they put out 2030 numbers, wanting to double that by 2030, so that will be $30bn in revenue.

It's a little confusing how they frame this, because they put out a target of $30bn for 2030, but that's not the real target, since they have their own internal target that's higher.

And then people ask what that target is, and they say it's $32bn.

Either way, we're just going to use $30bn in our math, and you could know there's that little bit of upside there.

The other thing they said was that they're going to do the rule of 60 by 2030.

If you're familiar with the rule of 40, it's basically adding operating margins, or cash flow margins, plus revenue growth.

The idea behind it, in short, is that as you're growing faster, your margins are less because you're investing more in R&D and sales and marketing, which compresses margin, but you're making up for it with higher revenue growth.

Whereas when your revenue growth falls, you should be becoming more profitable.

That's the idea behind it in a gist, and they're saying, we're not rule of 40, we're rule of 60.

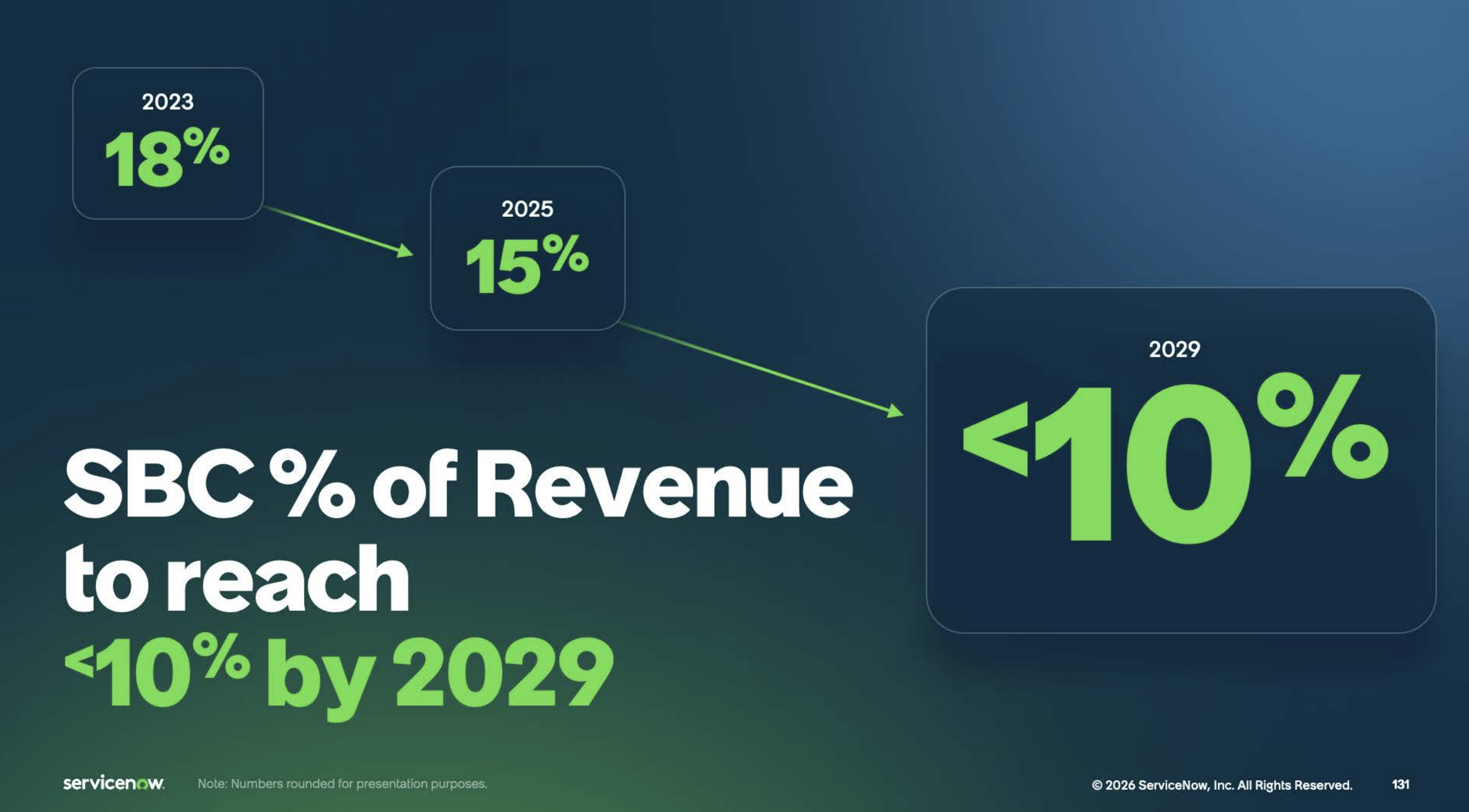

I say you have a lot of stock-based comp in that number.

A large portion of stock-based comp as a percent of revenue is showing up as margin, and that's not real margin to me.

They have been getting better about this, though, and they talked about it in the investor presentation, where they said only 10% of revenue will get directed to stock-based comp, and in the next few years we'll get it down to 15% and then 10%.

Usually for a tech company, you'd see a number maybe like 4-5%, and that would be pretty high, but the funny thing is their aspirational goal is 10%.

Whatever, you could just look at the numbers inclusive of that.

It is high stock-based comp, but that's fine.

I'm going to basically punish them for that, or it's not exactly punishment, but I'm not going to count it as income, and the way we do that is by not including it in the margin when we're doing our math.

Their rule of 60, let's say by then they're still growing revenues at about 20%, that's the CAGR that's implied.

That'll get us to 60 minus the 20% revenue growth is 40, minus 10% for stock-based comp as a percent of revenue.

You pull that out, and that's roughly a target margin of 30% in 2030 (60-20-10= 30% Target Margin).

So they're saying they're going to do $30bn in revenue, and on our math, an implied margin of 30%.

That gets you $7.2bn in NOPAT.

At $89 per share, their enterprise value is $90bn, which gives them an implied multiple of 12.5x for 2030. ($90bn/7.2bn = 12.5x).

So if they're able to achieve these goals, they're trading at 12.5x our estimated earnings of 2030, with some upside that they're doing a little better in revenue.

Then the question is, what multiple do you put on that?

If they're still growing high teens, you could very reasonably put a 25x multiple on that, especially because a 30% margin is not a mature margin for this business.

I would imagine at maturity they could be doing more like 40% or more, though of course they'll be growing a lot less at that point, so you would apply a lower multiple.

But let's say you're doing 30% margins, still growing at a high teens growth rate, once they hit that $30bn revenue number, I think 25x is a pretty arguable multiple for that business.

Some people might want a little higher, but we'll take 25x, so that upside is 100% for a 16% CAGR.

If you want to do a 30x multiple, that's 140% upside or a 21% CAGR.

That's not a crazy multiple if it actually does become that cash flow generative and is growing that quickly and is that entrenched in business process.

Those are pretty strong returns if you believe those assumptions.

Of course, the question is, do you believe them?

If management is so sure of their growth ambitions, how come they haven't been buying stock?

How come they haven't been stepping up their own purchases, putting their money where their mouth is?

If we look at the executive team, they basically haven't bought any stock.

Now, they did cancel their scheduled selling plans, their 10b5-1s, and that does show something, that at least they're not willing to sell stock at current prices, but a buy signal is much stronger.

Bill McDermott, though, the CEO, did buy $3mn of stock back in February, and that was also the first time he's ever purchased stock, so I don't think it means nothing.

It's hard to know exactly how impactful that is to him, but given his cash comp, it seems like it could be relatively impactful, and it makes sense that when the stock's down another -10%, he doesn't necessarily take another swing at it.

That is one positive sign, though, on insider activity.

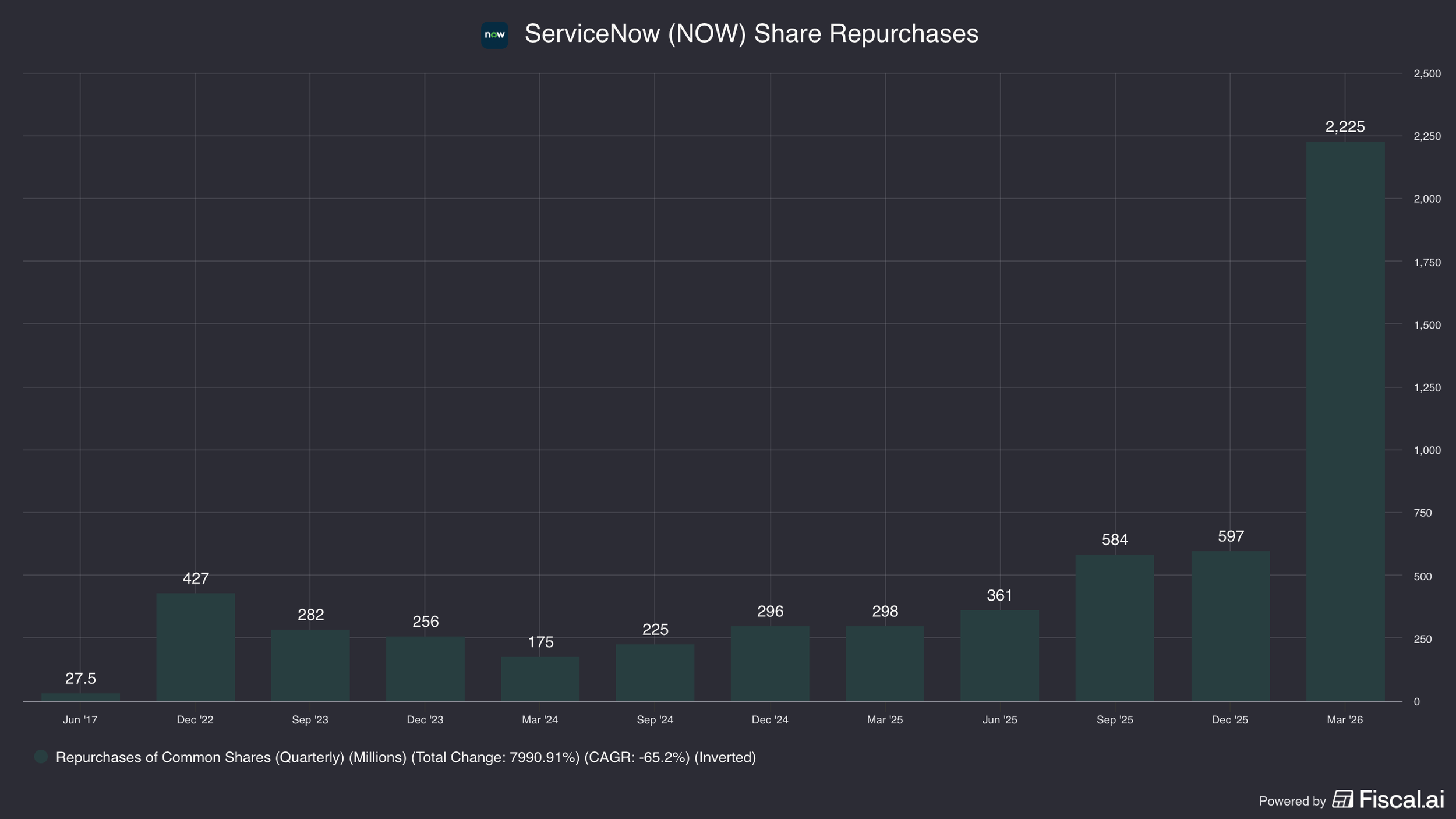

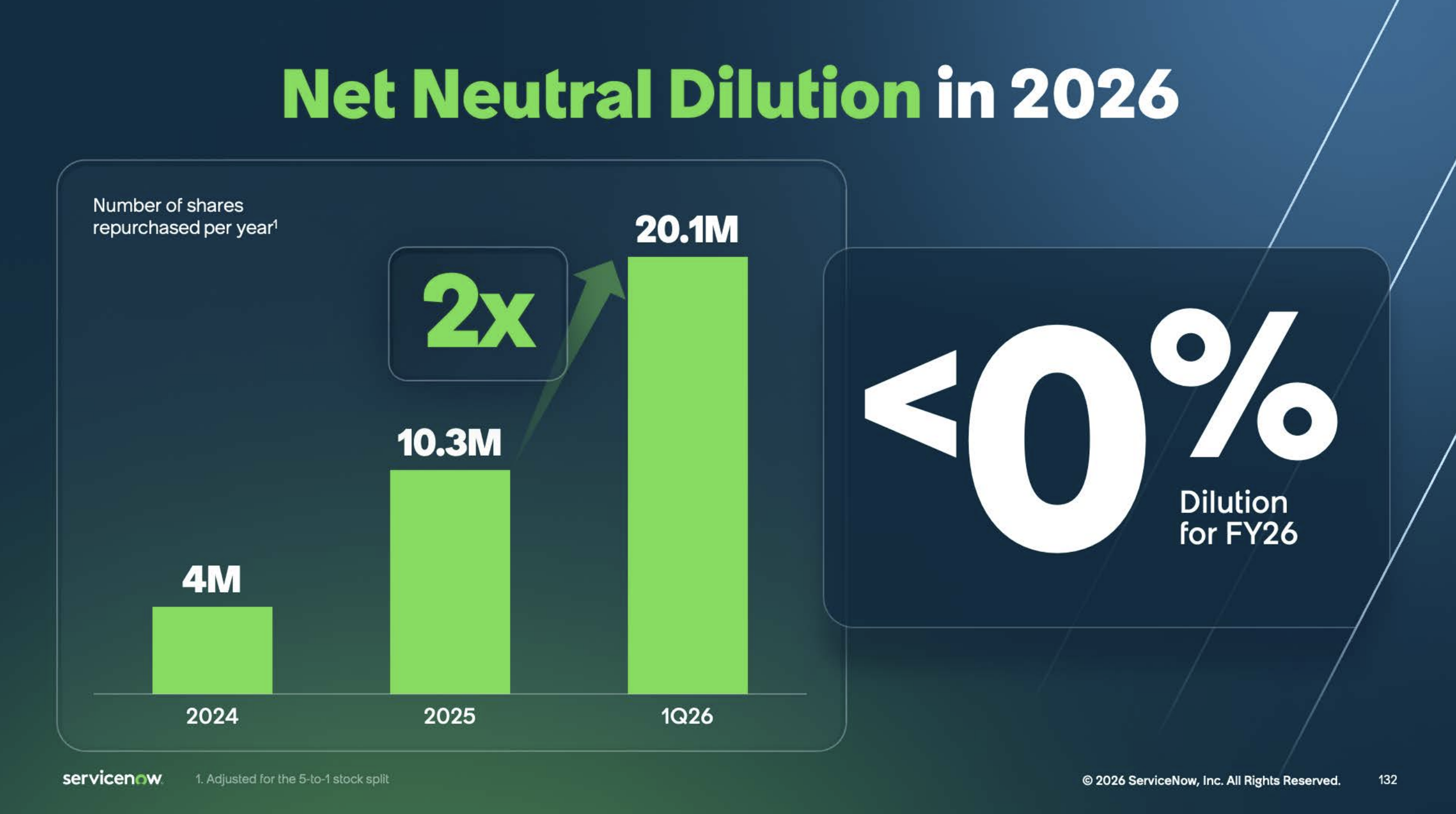

The other thing we'd like to see is more stock repurchases.

They talk about spending so much money on share repurchases, so what's the ending share count going to be?

They said we're going to be dilution neutral, which basically means all the money they spend to buy back stock just offsets the dilution from all the shares they've issued to employees.

They had a slide about this in the investor day where they said, we're going to lean more into agentic AI, that's going to help us maintain our workflow as we continue to grow, that's going to help bring down stock-based comp, and then more cash flows can be directed to buyback.

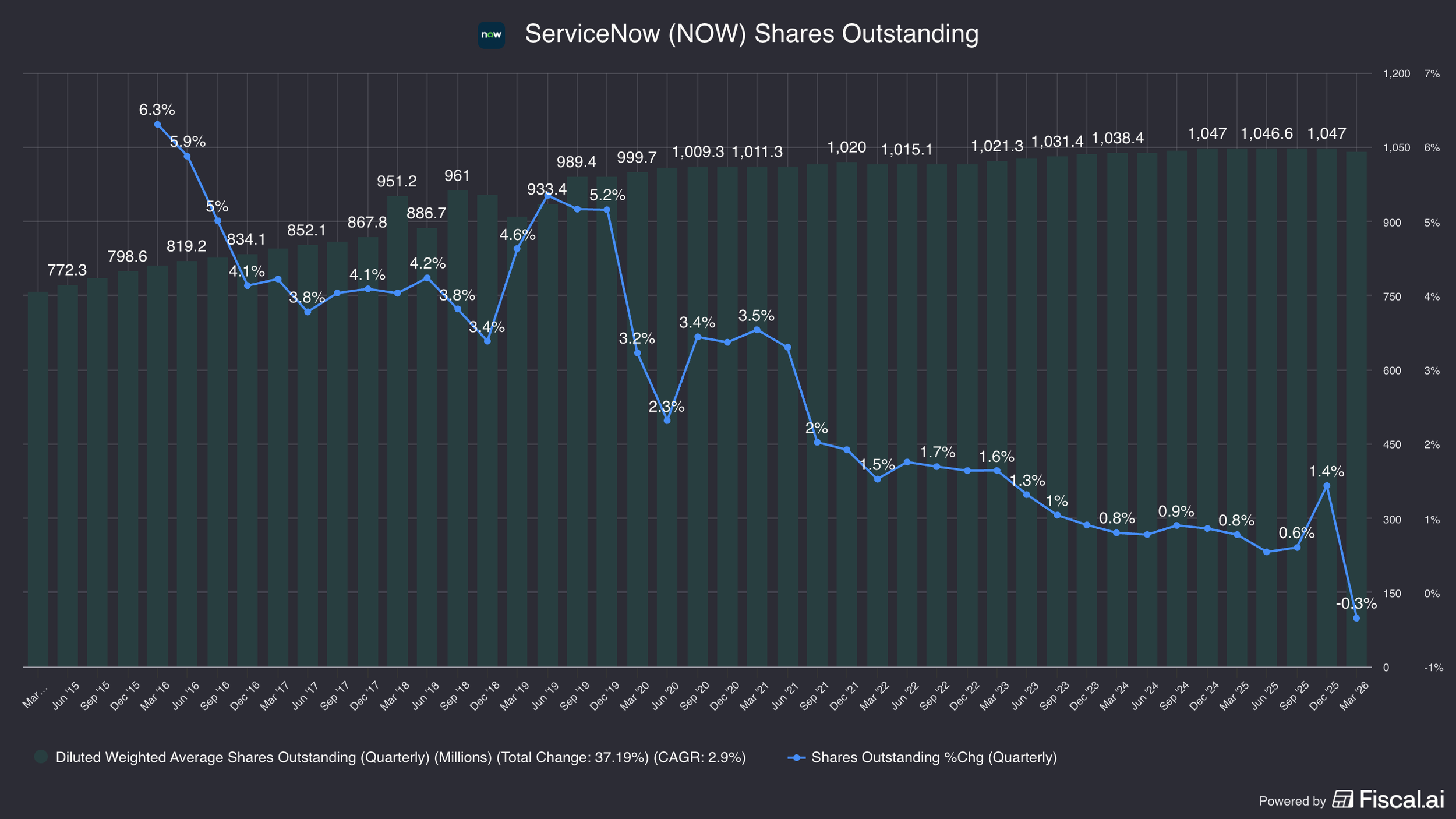

This last quarter actually was the first quarter that quarter-over-quarter diluted share count actually dropped, was actually negative, first time.

Now, they still said for the whole year they're going to be dilution neutral, so this could just be a quarter-to-quarter timing thing, but it does show they're actually very close to the point that they're actually going to be shrinking the share count.

Wild for a company like ServiceNow.

If that happens, though, that's another source of return over these next few years.

It's not going to be a big number, it's not going to really change the valuation that much, maybe a one percent annualized difference, something like that.

But the real question ultimately is, do you believe management?

Do you believe they will be able to hit the targets they put out?

Because if they do, the return is certainly there.

Ultimately, it comes back to how comfortable you are with those assumptions and whether you believe in their ability to execute.

For more on ServiceNow, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.