SpaceX $1.75 Trillion IPO: Genius or Delusion?

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

The SpaceX IPO is 3x larger than the next largest IPO ever, and the company is going after very ambitious hundred billion dollar TAMs, including space launch, connectivity, and AI, with initiatives ranging from orbital data centers to a colony on Mars.

Elon Musk may be contentious, but he has consistently made investors money.

The question is whether SpaceX, at $1.75 trillion, will be the exception?

It went public at over 60x revenue, even though growth has slowed: last quarter's revenue growth was only 15%, down from 33% the year before.

And while SpaceX dominates space launch, it's increasingly becoming an AI company, where competition is far steeper.

70% of capex spend is going towards AI, and most of the $75bn being raised will likely follow.

So investors may think they're buying a space company and find out it's mostly an AI company.

In this week’s Five Minute Money, we will break down SpaceX as well as the trading factors to be aware of now that it has IPO’d.

Business Overview.

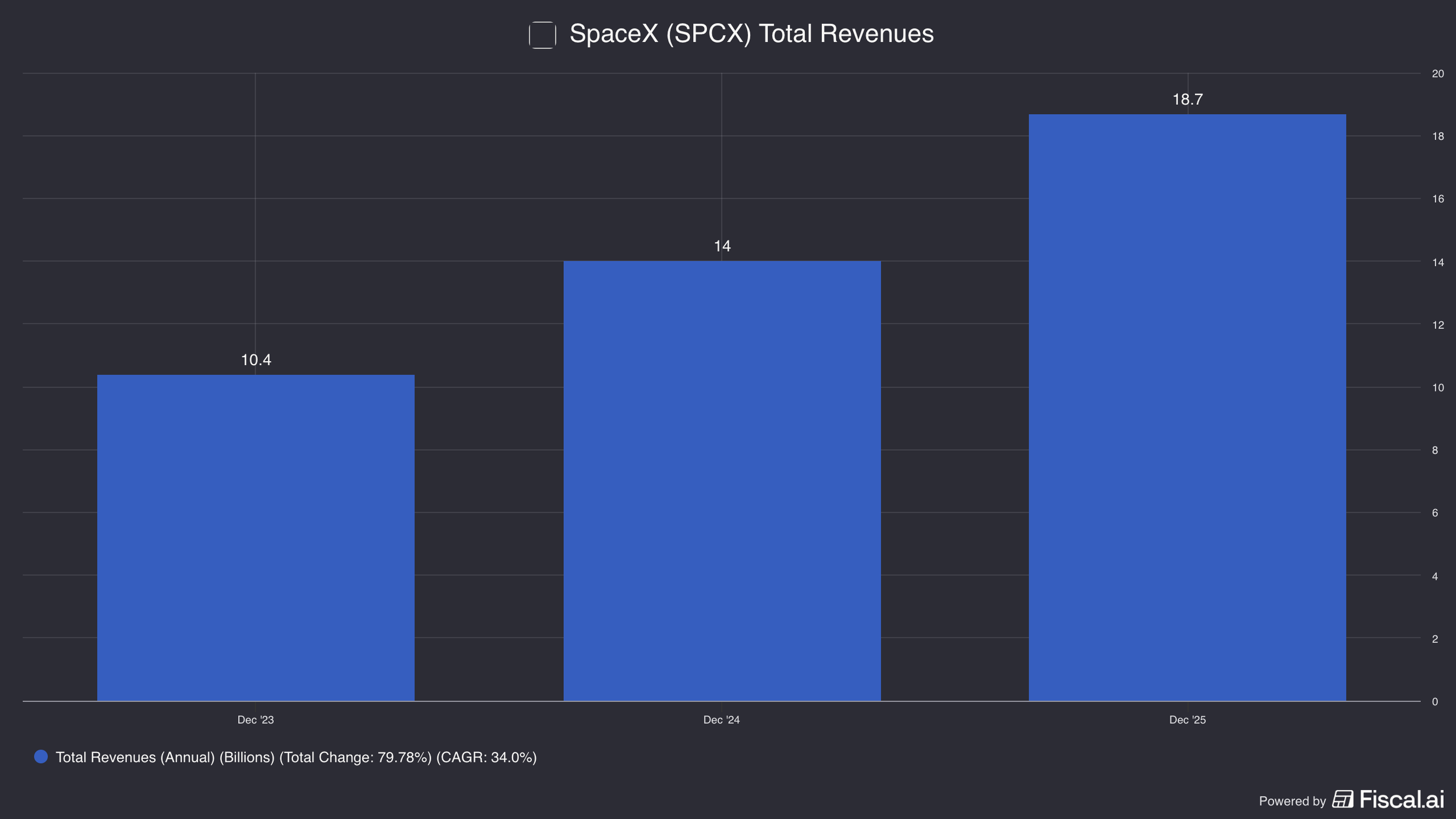

Currently, SpaceX generates about $19bn of revenue and has -$9bn in losses.

A year ago, in 2024, they were EBIT profitable, so it is by choice that they are loss-making instead of showing a profit.

Revenue growth in 2025 was 30%; in the last quarter it fell to 15%.

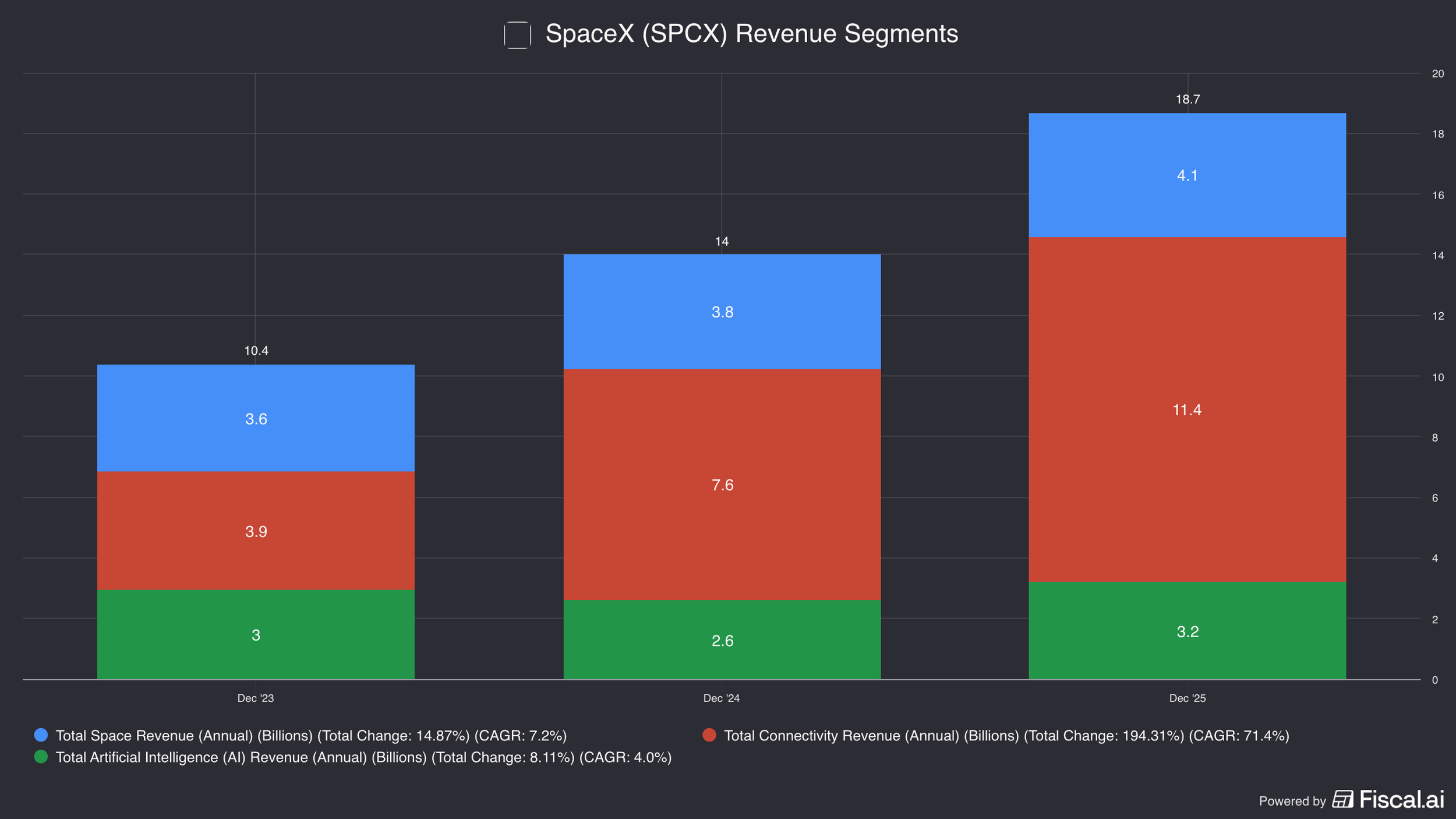

They have three main segments: 1) Space (launch, taking cargo and satellites up into space), 2) Connectivity (mostly Starlink, providing internet through satellites), and 3) AI (infrastructure plus their frontier model, Grok).

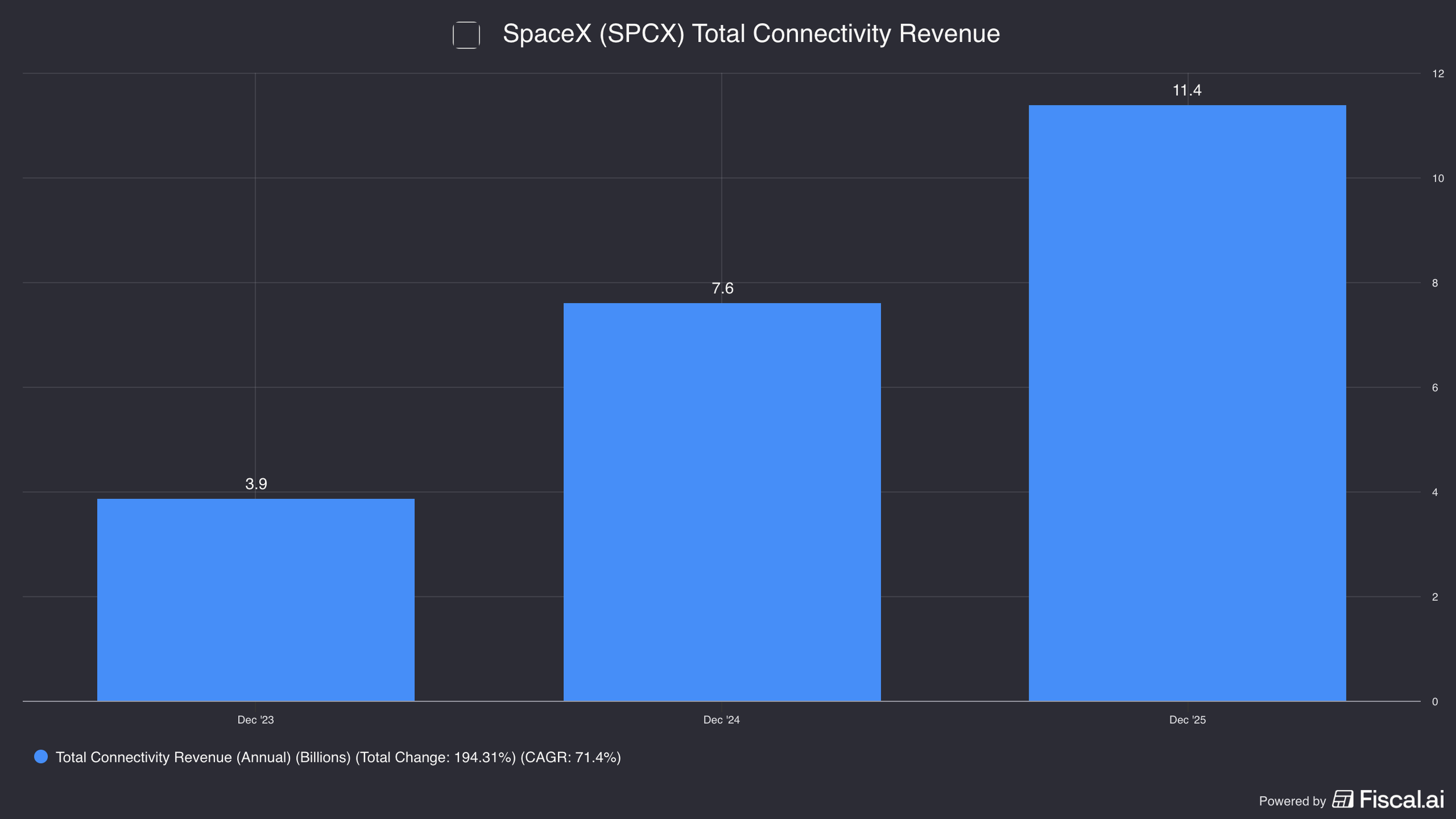

The space business is about $4bn in revenue, connectivity is a little over $11bn, and AI is a little over $3bn.

Most revenue, and basically all of their profits, comes from connectivity.

That's the cash cow funding the cash burn in next-generation rockets and AI infrastructure.

The Space Segment: Launch.

There are two classes of rocket: the Falcon, and the not-yet-launched Starship.

Falcon is the world's first reusable rocket, and that reusability is why launch costs have collapsed: from about $18,500 per kilogram to orbit down to $1,400, a 90%+ reduction, almost entirely driven by reusing the same rocket across many trips.

SpaceX has also been ruthless about driving down part costs, partly because no real supplier base existed when they started.

Elon Musk reportedly tried to buy a rocket from Russia, that fell through, and he built one himself instead, building a scrappy in-house culture (one vendor wanted $100,000 for a space radio; SpaceX built it for $5,000).

Starship, their next-generation rocket, will carry larger loads and push costs down further once it's working.

Right now, 75% of revenues go to R&D, much of it tied to Starship.

Gross margins are 67%, high for a capital-intensive business, reflecting both the favorable economics of reusability and how little competition exists for launch, letting SpaceX command its price while still being the cheapest option for anyone, telecoms or governments, who wants a payload in space.

They're responsible for 80% by volume of all payloads going up.

Growth in this segment was only 8% last year, because launch capacity is increasingly reserved for SpaceX's own Starlink satellites.

Those launches don't register as space-segment revenue, even though the capacity could theoretically have been sold elsewhere.

The Connectivity Segment: Starlink.

Connectivity brings in about $11.4bn in revenue, growing 50% y/y, while subscriber counts are up over 100%.

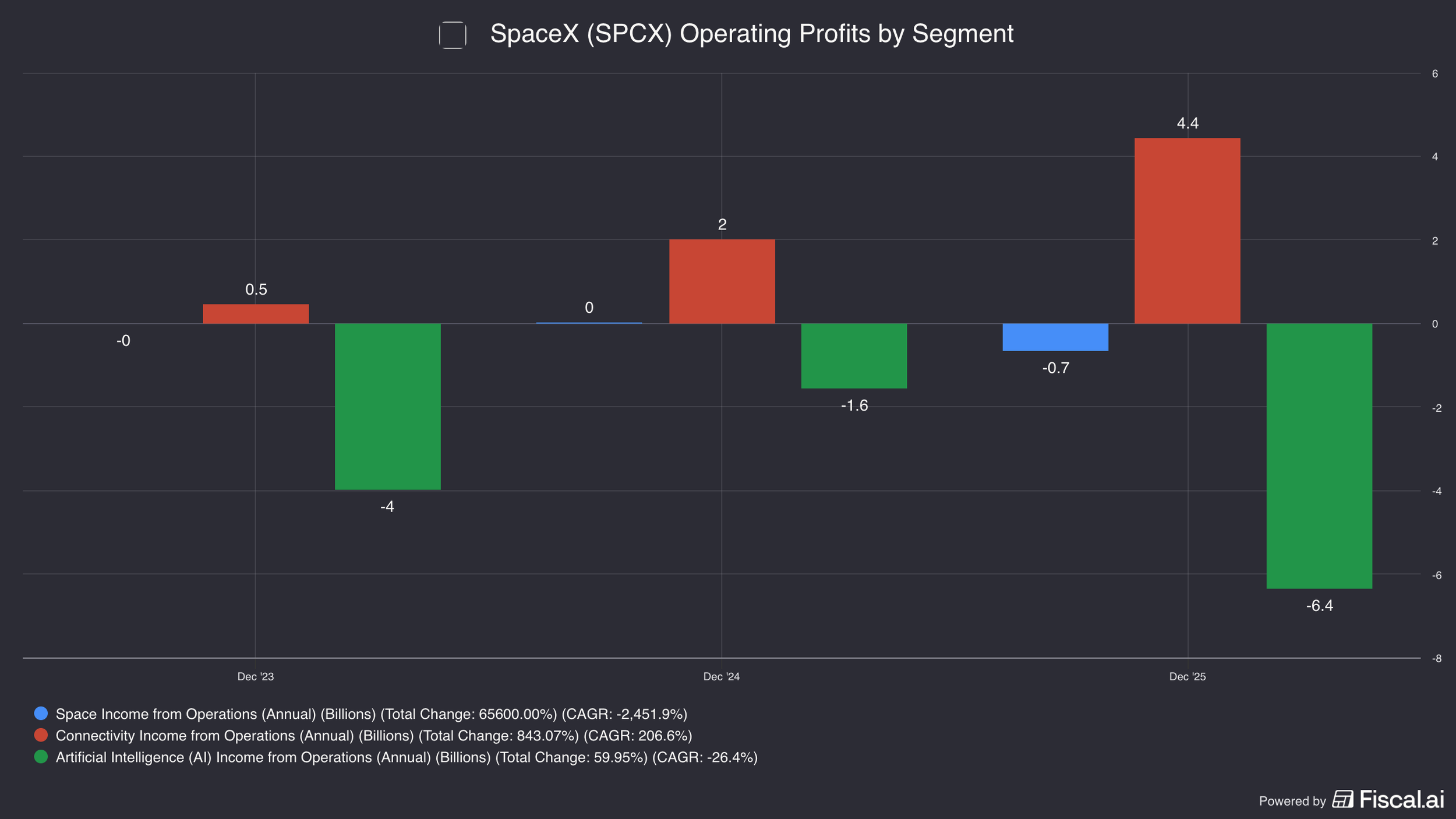

Gross margins are about 52% and EBIT margins are 38%, making this SpaceX's real cash cow, funding most of the capital behind the space business and now also AI growth initiatives, while the space segment itself burns about negative $650mn.

Connectivity has four parts.

Starlink Consumer.

The biggest piece sells internet directly to households: over 10 million subscribers, growing 100% y/y.

Average revenue per user was $66 last quarter, down from $99 in 2023, not necessarily bad, since scale is letting them profitably lower prices and expand the addressable market.

Customers pay an upfront terminal fee plus a monthly subscription, and the service is especially useful where traditional telecom infrastructure doesn't reach.

SpaceX plans for over 42,000 satellites eventually, versus about 9,600 today, which would let Starlink become a real broadband alternative, though today it's used mostly in rural areas without other options.

Enterprise, Government, and Mobile.

Enterprise solutions sell bespoke, bulk-priced internet to airlines, cruises, and industrial customers like John Deere, whose equipment increasingly needs connectivity.

Government contracts carry extra security and sometimes dedicated satellites; the U.S. version is called Starshield.

Starlink Mobile provides stop-gap cellular coverage in dead zones by automatically connecting a phone to satellite internet, priced either as a consumer add-on (like their partnership with T-Mobile) or as a wholesale deal where the carrier pays SpaceX and upcharges customers.

The Importance of Starlink.

This is SpaceX's biggest business and its only profitable segment today, likely for the near term.

Its advantage over rivals like Amazon, which relies on Jeff Bezos's Blue Origin for launch, is a much lower embedded cost structure, since SpaceX owns the cheapest launch capability itself.

The AI Segment.

SpaceX acquired xAI, Elon Musk's AI company, which had already acquired Twitter (renamed X) for $45bn.

A likely reason SpaceX merged with xAI and went public is the enormous capital need of AI infrastructure, which would have been easier to raise against SpaceX's profitable, high-quality launch and Starlink businesses than for xAI alone, where the business remains a question mark.

The AI segment has only $3.2bn in revenue but losses exceeding $6bn, with three sub-segments.

AI Infrastructure.

SpaceX built Colossus I, a massive data center, in 122 days, then Colossus II in 91 days; together these total about one gigawatt, versus an industry benchmark of roughly two years to build 100 megawatts, drawing on the same cheap, fast, iterative execution that made reusable rockets so much cheaper than Boeing's legacy programs.

NVIDIA also prefers more customers over fewer, making it willing to sell GPUs to xAI rather than concentrate sales with Amazon or Google.

SpaceX also touts an integration advantage: data centers, the Grok model trained on them, Twitter's data, and a planned in-house chip fab called TeraFab, all working together, though Twitter's data alone isn't a major edge, since Anthropic has reached a leading AI position without anything like that vertical integration.

Leasing Capacity to Anthropic and Google.

SpaceX is currently leasing data-center capacity to others.

Colossus I ended up with mixed generations of NVIDIA chips, creating lag that hurts training but is fine for inference.

Anthropic pays about $1.25bn a month for access and Google about $920mn, both through 2029; annualized, that's $26bn against roughly $19bn in total company revenue.

This works well now because compute is scarce and commands a premium, but it's not a great long-term model: SpaceX isn't meant to be a data-center landlord, and once industry-wide capacity catches up, that premium should fade toward mature margins of perhaps 20–40%.

Both contracts are cancellable on 90 days' notice, so this isn't guaranteed revenue.

Space Data Centers.

The real rationale for tying AI to SpaceX is space-based data centers: massive satellites with solar panels geo-locked to the sun for power, solving the power, cooling, and siting problems that plague data centers on Earth, while creating new ones, like dissipating heat with no air to carry it.

The plan is to launch many smaller satellites, starting with the first AI1 satellites, eventually aiming for a million of them, with Starship's larger payload letting them launch in bulk and amortize cost across more units.

Grok.

Grok has about 117 million monthly active users, mostly crossover from its embedding in the X app.

As a standalone LLM it trails Gemini, Claude, and ChatGPT, and is undergoing a full rebuild this year amid high researcher turnover, a tough climb, since unlike rockets and EVs, where Musk had an early lead, Grok is coming from behind against far better-resourced rivals.

SpaceX doesn't strictly need Grok to win; it could instead sell space-based AI infrastructure to Anthropic and Google, which it's already doing.

Still, it's investing heavily in both, and success would be good for AI diversity even if the odds look tougher than in SpaceX's other businesses.

Consumer and Enterprise: X, Advertising, and Macro Hard

This bucket includes X's advertising business, a minor contributor: Twitter struggles to attract enough advertisers to match ads well to users, leaving it to compete mainly on low price, a weak position versus Meta.

Musk's political profile has also pushed some advertisers away, though unlike Meta's largely inconsequential 2022 boycott, these advertisers don't see leaving as costly since Twitter ads weren't doing much for them anyway.

Also notable is Macro Hard, an agentic AI enterprise product developed with Tesla, which could work if it proves valuable internally first, though it will need to match offerings from Anthropic, Google, and OpenAI, all of which appear ahead.

TeraFab.

The last piece is TeraFab, a venture with Intel and Tesla to design and manufacture chips for orbital data centers and possibly Tesla vehicles, hard and expensive, but potentially a cheaper chip source if it works.

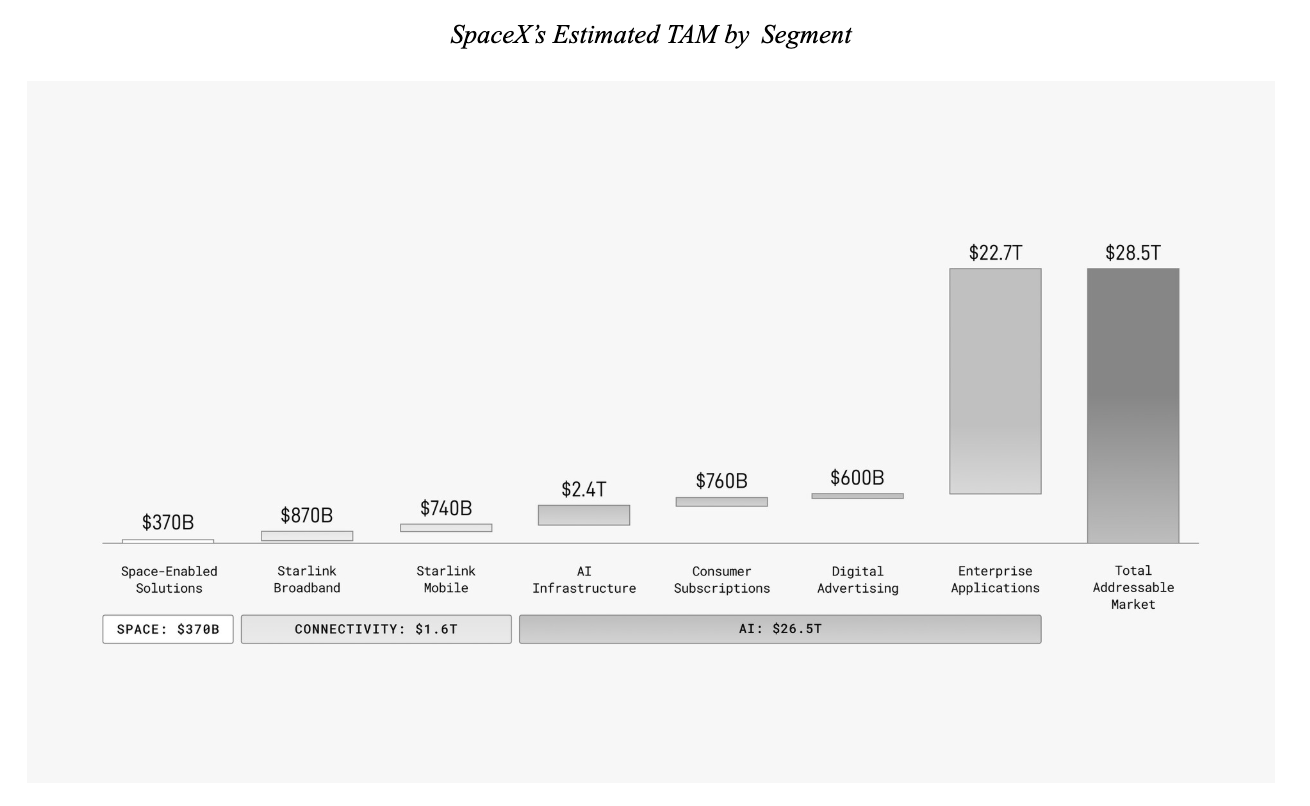

Total Addressable Market.

SpaceX's prospectus cites a $28.5 trillion TAM, a fancifully large number, as bankers tend to produce.

Telling, though: $26.5 trillion of that comes from AI-related markets, and only $370bn from space, underscoring that investors thinking they're buying a space company are mostly buying AI exposure, with some overlap via space data centers.

They also cite $1.6 trillion for connectivity.

70% of capex last quarter went to AI, and a majority of the $75 billion being raised will likely follow.

Since 2002, SpaceX has raised only $9bn in equity total, building the entire launch and Starlink business on it, an extremely high historical return on capital.

The return on this next $75bn looks more dubious, and likely lower than what the existing businesses have generated.

Competition.

One reason AI spending likely earns a lower return than the space and Starlink businesses is simple: competition.

Space Launch Competitors.

The competitive set in launch is thin: Blue Origin, Rocket Lab, a few Chinese startups, and legacy players, and none are close to SpaceX on cost or cadence.

Rocket Lab, a $60 billion company, launches about twice a month; SpaceX launches about twice a week and is accelerating, with no rival response to Starship.

Blue Origin has lagged despite Jeff Bezos's resources, and its Amazon-backed Kuiper network (3,200 planned satellites) pales next to SpaceX's nearly 10,000 today and 40,000 planned.

This thin field is why launch is one of SpaceX's highest-quality businesses, flowing through to Starlink's first-mover advantage.

AI Competitors.

AI is different.

Unlike rockets and EVs, where SpaceX and Tesla were early, AI finds them arriving late against far more formidable rivals: Google, Meta, Amazon, Microsoft, Anthropic, OpenAI, open-source players like DeepSeek, and a wave of neocloud infrastructure providers.

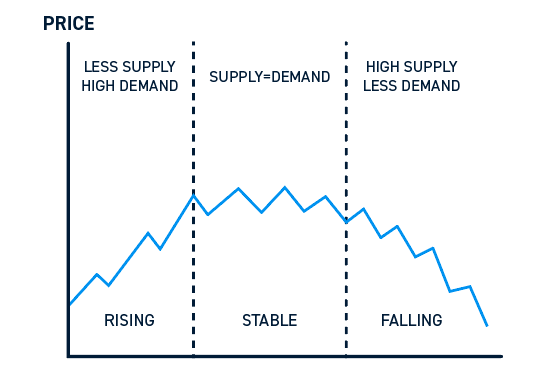

Typical capital cycles see excitement draw in too much capital, leading to overbuild and falling prices, an outcome that may be years away, but makes the space and Starlink businesses the more durable long-term holdings.

Space Data Centers.

Space data centers are a genuinely unique angle: enough of them, built cheaply enough, could flood the market with compute competitors can't match.

But that could take years, and it still competes with Earth-based infrastructure: customers like Anthropic care about cost and access, not location, so space capacity only commands a premium once terrestrial capacity actually runs out.

It's fair to invest partly on belief in Musk and SpaceX's team, but ultimately the economics, not the narrative, will decide the outcome.

Valuation.

At a $1.75 trillion IPO valuation, using the high end of 2026 revenue estimates (~$30bn), SpaceX prices at roughly 58 times sales, despite growth slowing to 15% last quarter from 33% the year before.

For comparison, Palantir trades at 40x sales while profitable and growing 85%.

A 10% Return Scenario.

Assume investors want a 10% annual return over the decade, roughly the stock market's long-run average.

That requires $1.75 trillion to grow to $4.5 trillion.

At a 30 times multiple (appropriate if SpaceX is still growing mid-teens earnings a decade out), that implies $150 billion in profits versus zero today.

That's a large number: Tesla has never exceeded $12 billion in annual profit, and Microsoft is around $120 billion.

Assuming mature margins of 25–40%, SpaceX would need revenues of $470–750 billion, a 33–38% revenue CAGR.

No company has ever sustained 30%+ revenue growth after reaching $10 billion in sales; this would be a first.

A 15% Return Scenario.

A 15% return requires the valuation to grow to $7 trillion in 10 years, needing $235 billion in profits and $735 billion to $1.2 trillion in revenue at the same multiple.

A higher exit multiple is possible, but it should tie back to a DCF: assuming one just means assuming even faster, longer-lasting earnings growth, a less conservative bet rather than a free upgrade.

Growth Opportunities.

So how could SpaceX plausibly generate hundreds of billions in revenue to support those numbers? There are a few ways.

Starlink.

The clearest path is Starlink: 200 million households paying $50 a month, plus a billion smartphones paying $10 a month for stop-gap satellite coverage, would together generate about $240 billion in revenue.

Space Launch and a Broader Space Economy.

A second path is space launch supporting a future space economy: asteroid mining, lunar colonies, off-Earth manufacturing, space-based pharmaceutical research exploiting microgravity, even point-to-point earthbound space travel (New York to Tokyo in 45 minutes).

SpaceX could charge for transport, storage, and fuel, speculative, but real upside if even part of it materializes.

AI Infrastructure and AI.

A third path is AI infrastructure: a million orbital data centers could alone represent a couple hundred billion dollars of revenue.

The fourth is AI itself: a leading frontier model plus consumer and enterprise businesses, though this is the most competitive and uncertain leg, while the space ambitions tend to take longer than expected.

Investors have to decide which assumptions they're comfortable making and whether the implied return is worth the risk.

Many will buy in simply because they believe in Elon Musk, more like venture investing, betting on a person to figure it out.

Notably, Musk's own pay package is tied to lofty goals, including SpaceX reaching $7.5 trillion and hitting 100 terawatts of orbital compute, by some estimates, more than exists on Earth today.

Now, let's turn to the trading factors you should be aware of now that SpaceX has IPO'd.

IPO Trading Factors.

Remember that an IPO price is a pricing, not a valuation.

Bankers set the highest price the market will bear while leaving room for a pop, since that pop creates momentum that draws in buyers and lets insiders exit more easily as shares unlock.

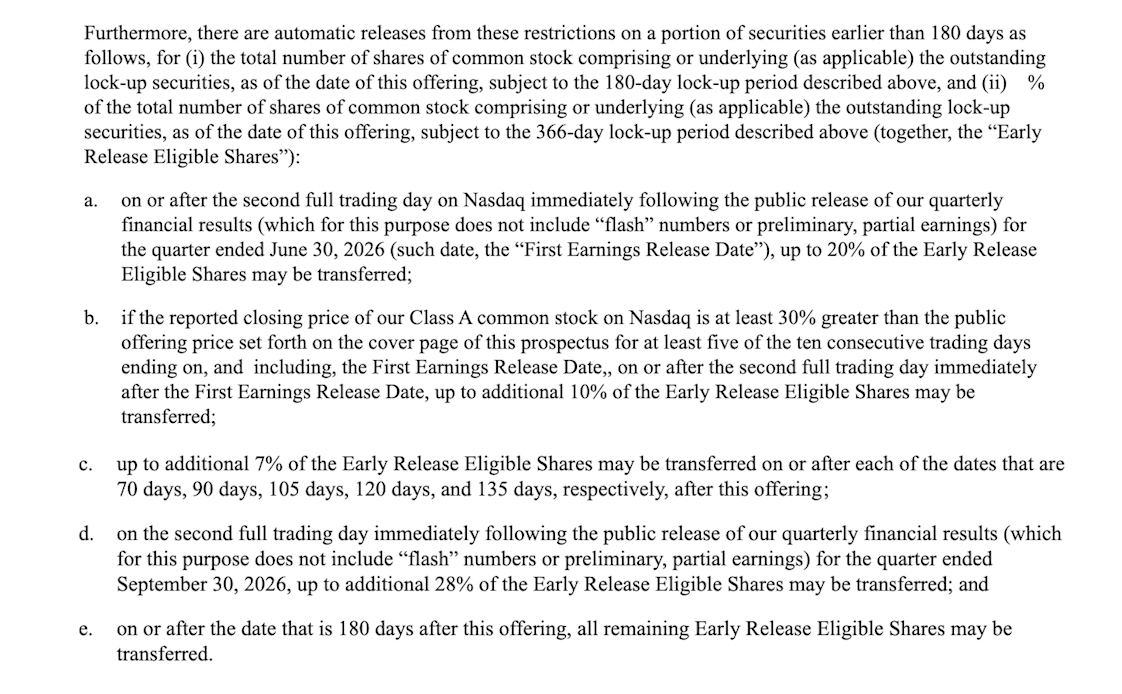

A typical IPO pops on day one, stays strong for months, then often hits a new low around the 180-day lockup expiration, when it's common to trade below the IPO price as insiders sell.

SpaceX's lockup is different in that it unlocks earlier over the course of the 180 days: 20% of employee shares as early as the first earnings report (likely late July or August), another 7% every 15 days after, more around Q3, and the remainder at 180 days.

Demand looks strong: the IPO was already two times oversubscribed, over $150bn in demand against $75bn of shares, though some reflects investors inflating orders to secure a smaller desired allocation.

Banks also typically support the price if it weakens, including by holding shares on their own books.

None of this guarantees a strong debut.

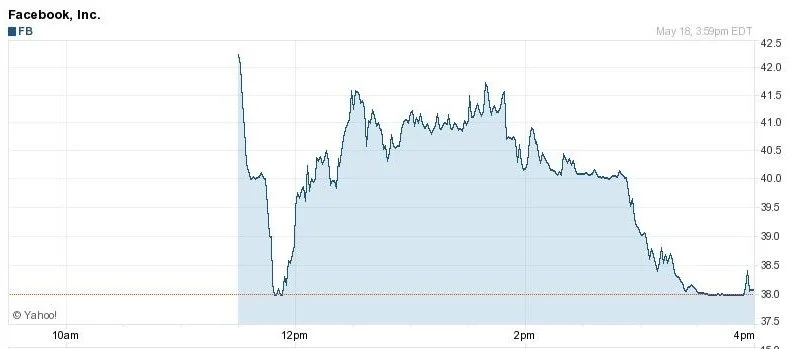

Facebook's IPO is the classic cautionary tale: priced too high at $38, it barely closed up on day one and traded much lower months later.

Buying purely because it's a hot IPO, rather than believing in the long-term revenue story, is trading, not investing, and carries the risk that the typical pop simply doesn't happen this time.

Index Inclusion.

15 days after the IPO, SpaceX joins the Nasdaq index, forcing institutional buying; it won't qualify for the S&P 500 anytime soon given that index's profitability requirement.

Some investors are even selling Nasdaq exposure to avoid involuntary SpaceX exposure, understandable, but not worth restructuring an index position around, since indexing's whole point is letting the market price every holding rather than picking winners yourself.

There's a time when IPOs feel like easy money, but they don't always end well, so know whether you're investing in the business or just trading the pop.

SpaceX's IPO is unlike anything markets have seen.

It's three times larger than the next biggest offering ever, priced at a $1.75 trillion valuation, and built on hundred-billion-dollar ambitions spanning space launch, connectivity, and AI, with even more speculative bets like orbital data centers and a Mars colony layered on top.

Elon Musk's track record of making investors' money is real, but so is the question this IPO ultimately poses....

Will SpaceX be the exception to that track record?

Ultimately, it will be up to an investor to decide if they believe in the story enough to put a lot of faith in Elon Musk to bring SpaceX’s vision to space, and AI around the world…

Or if they want to wait for a better pitch.

For more on SpaceX, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.