The Category Killer Copying Costco

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

Charlie Munger praised this company, Floor & Decor for copying Costco.

In fact, it is one of only two businesses he named as properly copying the Costco playbook, the other one being Home Depot.

They have a 3-year payback period on their stores and in year 3 are able to produce 50% cash on cash returns at the store level.

It’s been a category killer in flooring, taking share in one of the worst macro environments for them.

Their largest public competitor, LL Flooring, actually went bankrupt just last year!

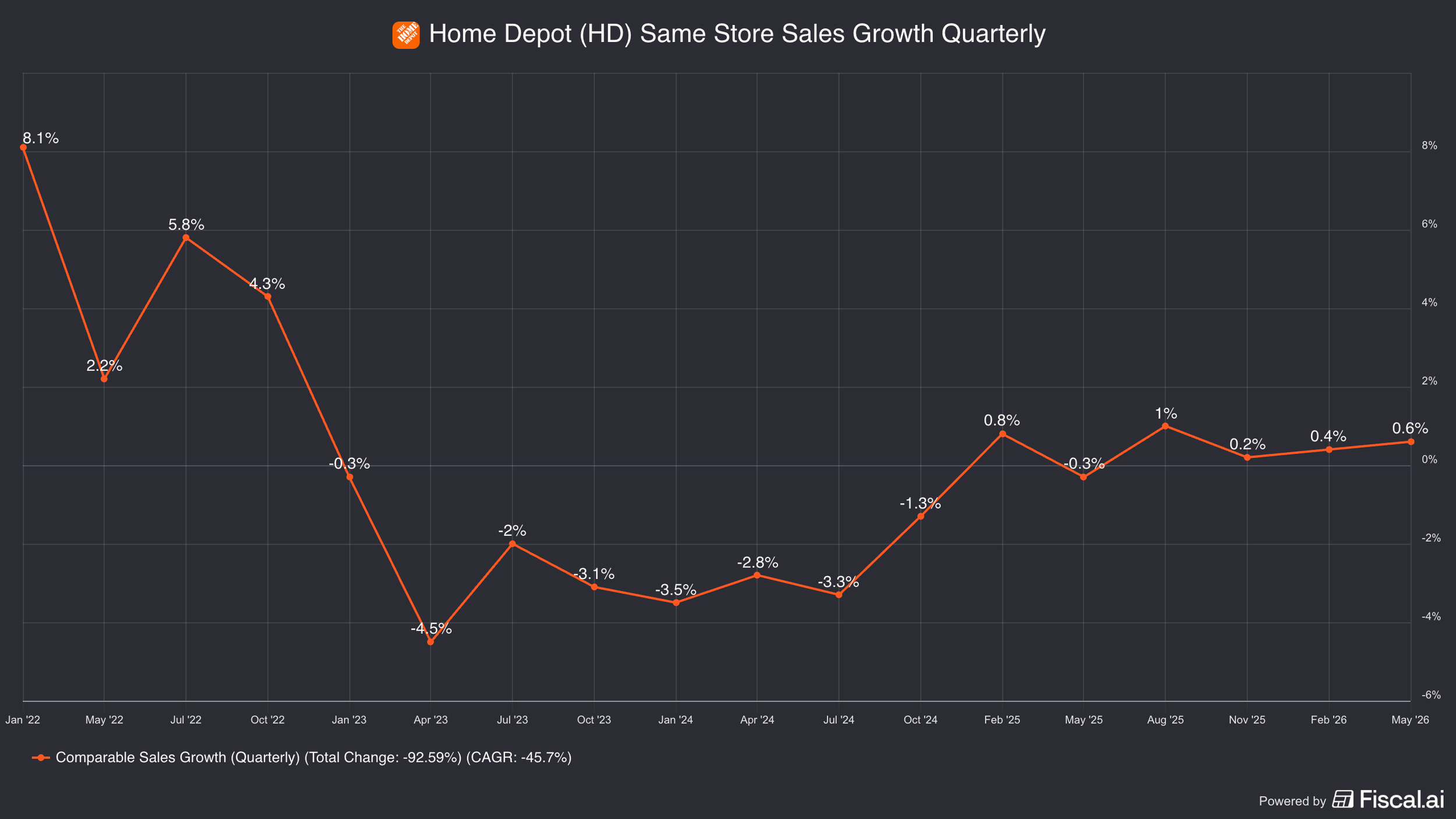

This macro environment is so bad that pre-covid they were doing double-digit same-store-sales growth, but then in covid, they put up 28% same-store-sales growth as everyone rushed to refurbish their homes fresh with more stimulus money, which provided a boom to a lot of demand.

However, since 2023, every year they comped negative same-store-sales growth as demand pullback.

This was in part because in the aftermath with inflation and interest rates rising, this put a damper on existing home sales.

And what is one of the biggest trigger events to replacing your floors?

It’s when you buy or sell a home.

This touch macro environment has punished the stock, falling -66% from its peak in 2021.

They are now trading at a price not seen since the covid March 2020 sell-off.

But despite these tough macro headwinds, what has the company done?

Well, they focused a lot on cost discipline, improving the store level unit economics, improved the business mix to now be over 50% professional geared, and finally they’ve still been opening up new stores, while taking more share in this environment.

So when the tough macro environment turns, they should be a beneficiary.

In this week’s Five Minute Money, we will break down all things Floor & Decor!

Business Model.

Floor & Decor was founded in 2000, by George Vincent West, who realized there wasn’t a specialty store just for flooring that offered a wide selection.

After growing the business to two stores, some private investors got involved and they scaled it up to 25 stores.

Then in 2010, two private equity firms, Ares and Freeman Spogli, got involved and scaled the business even larger.

Eventually, in 2017, Floor & Decor went public.

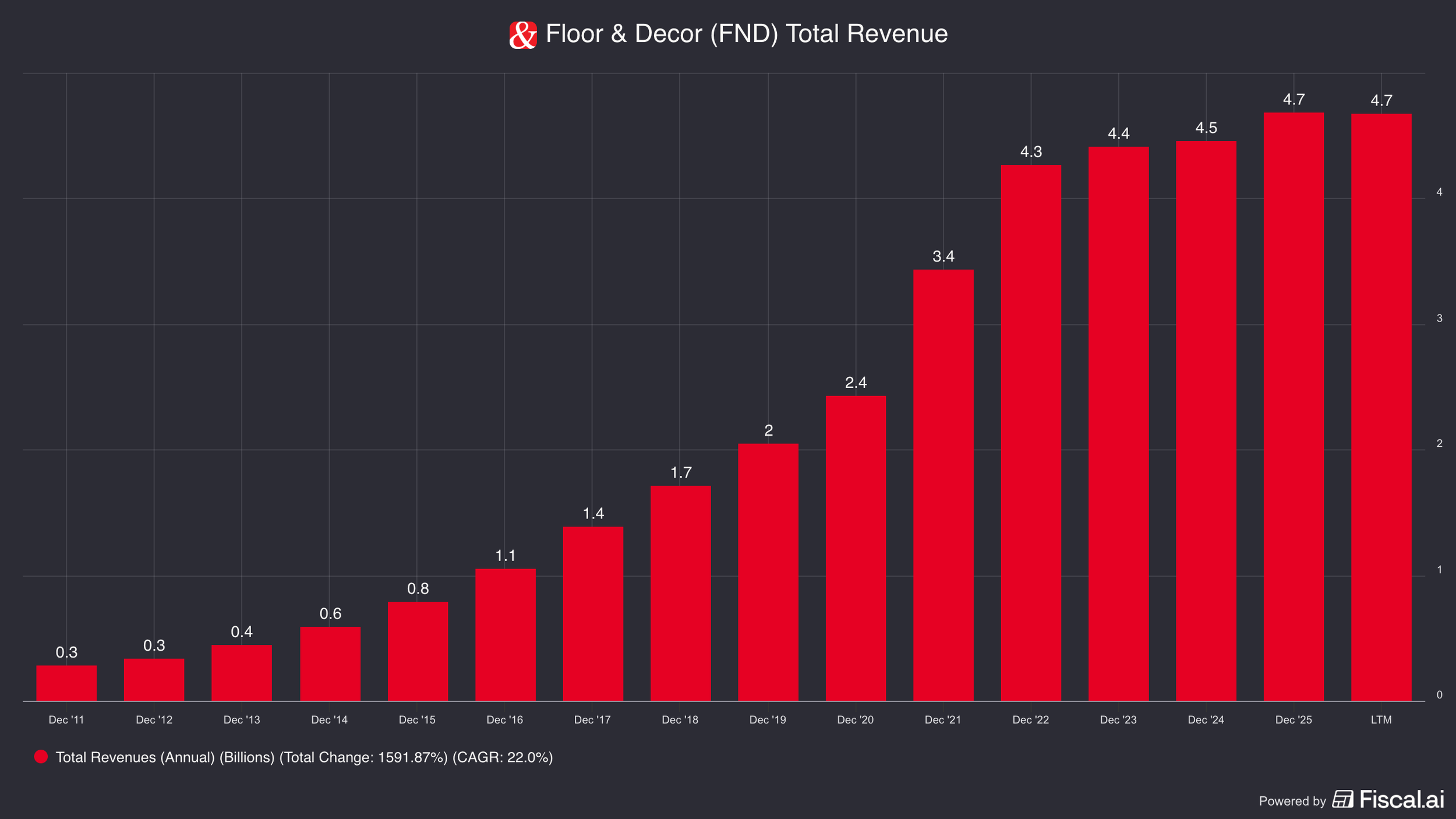

Today, they generate $4.7bn in revenue and operate 276 warehouse stores.

As you probably guessed, Floor & Decor sells flooring.

One of their biggest products is called LVP or “Luxury Vinyl Planks.”

LVP is what is laying the ground of millions of homes and apartments worldwide.

It has been gaining a lot of share against carpet as carpet is going out of style.

They also sell everything else related to flooring; hardwood, stone, tile, as well as wall tile.

Then they do have the decor side of the business which is a small set of accessories like vanities and bathrooms, and recently got into kitchen cabinets.

One risk is they expand too much into this decor side of the business, but as or right now, it’s only a few percentages of overall revenues.

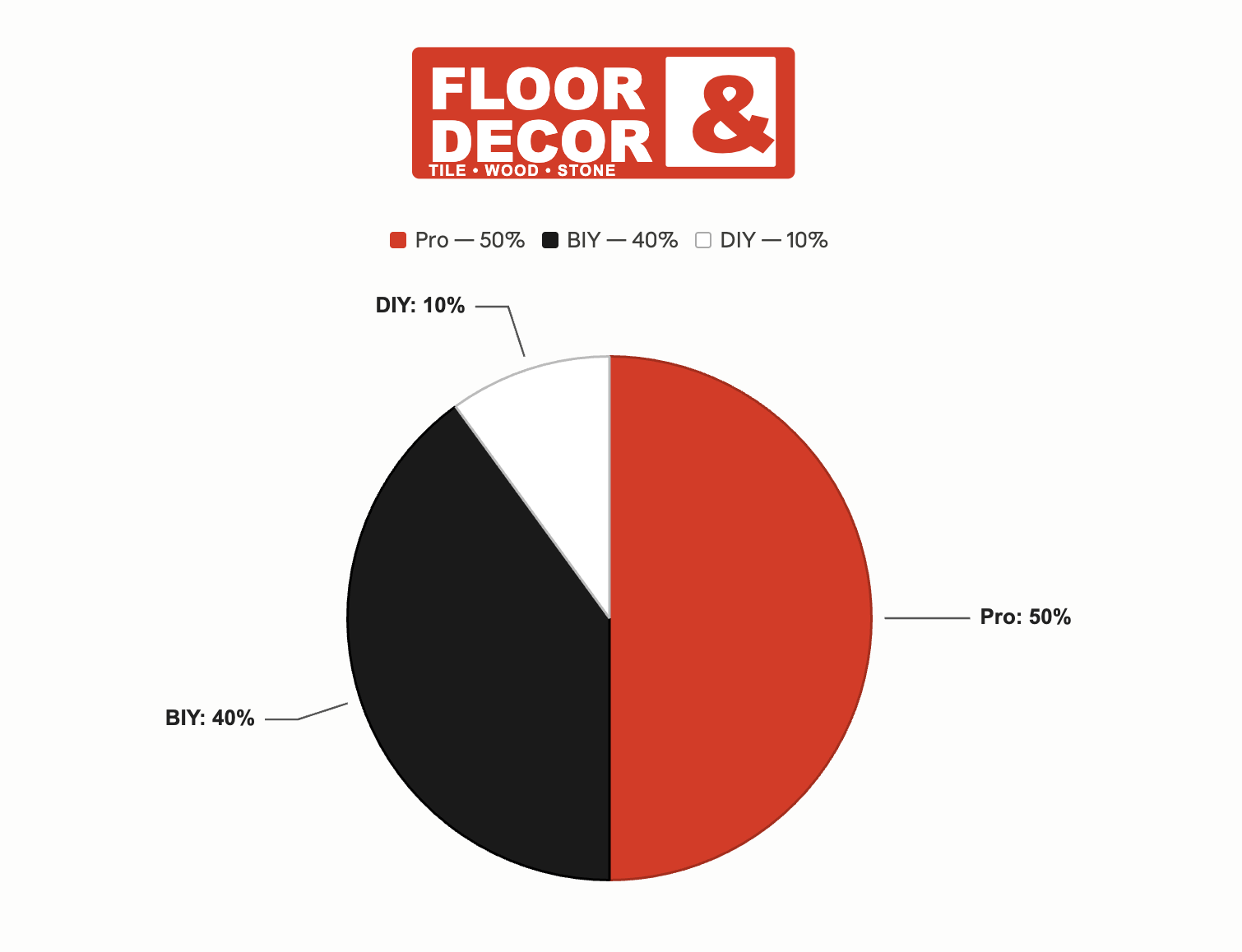

In terms of their business mix, they cater to 3 different consumers:

1. DIY: Do it yourself.

2. BIY: Buy it yourself, then have a pro install it.

3. Pro: Professional flooring installers who are purchasing on behalf of the customer and installing it for the customer.

As you can see in the chart below, DIY is the smallest segment at 10%, then BIY is 40%, and finally Pro is the biggest at 50%.

Now, you maybe thinking, “What’s so special about buying flooring?”

It’s a product that’s kind of a commodity that you could get at a lot of different places?

To understand how they are competitively advantaged versus their competition set, we turn to their value prop.

Value Prop.

Floor & Decor’s value prop centers around 3 key things:

1. The widest selection

2. The lowest prices

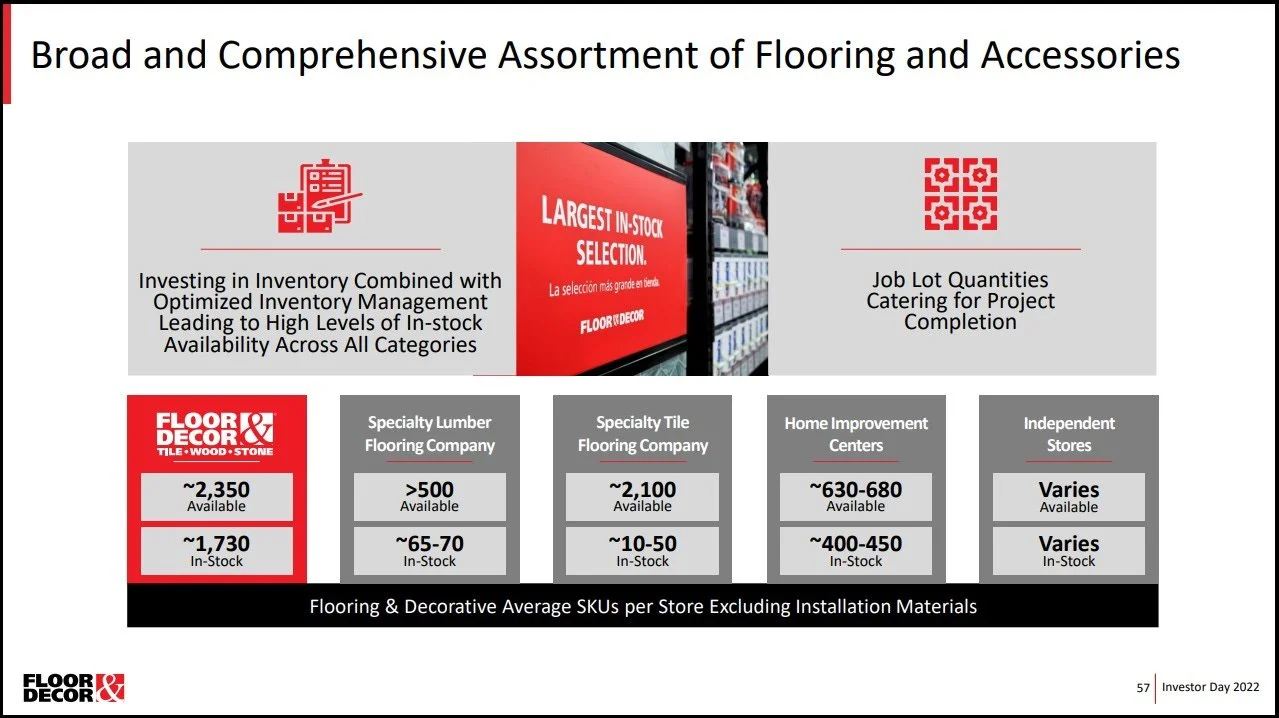

3. In-stock inventory

They have over 2,000 products to choose from compared to 500-600 that other competition offers.

Their pricing model which is called “Good, Better, Best”, offers competitive prices across different quality of goods.

Having in-stock inventory is critical, especially for professionals, because professionals are small businesses who don’t have warehouses to store their flooring.

Very often, a Pro has a job that they need to do that day and they can do to a Floor & Decor to pick up the equipment and go do the job that same day.

If they have to order it and wait for it, they potentially just that job, so having in-stock inventory is very critical need for Pros who again make up 50% of their business.

What allows them to offer this value prop and why competitors have struggled to copy them, ultimately comes down to the way they set up their business model and it all starts with this idea of a warehouse store.

This brings us to why Charlie Munger said Floor & Decor was similar to Costco.

Copying Costco.

What makes Costco so special?

Why are they able to offer the prices they’re able to offer?

If you analyzed Costco, you would quickly find out that a warehouse store is instrumental to their value prop.

It supports the whole thing because you can’t sell at scale unless you have massive amount of store footprint.

Because Costco uses the warehouse model, they have a lot of volume they can push through it, which in turn allows them to get lower prices, and those lower prices can then get passed off to the customers.

If you are a retailer, you can’t sell at scale with a small store. You need a large warehouse.

So similar for Floor & Decor, their competitive advantages stem from the fact that they operate with large warehouses that are 60,000-80,000 sq ft big.

Much larger than any competitor.

For Floor & Decor, having a big warehouse model, that enables you to have a lot of in-stock inventory because the showroom is the warehouse at the same time, which is more cost efficient.

As I mentioned earlier, having more inventory on premise is very important for professionals who want to grab their inventory the same day.

Having a warehouse model also enables more selection.

More selling space, more options.

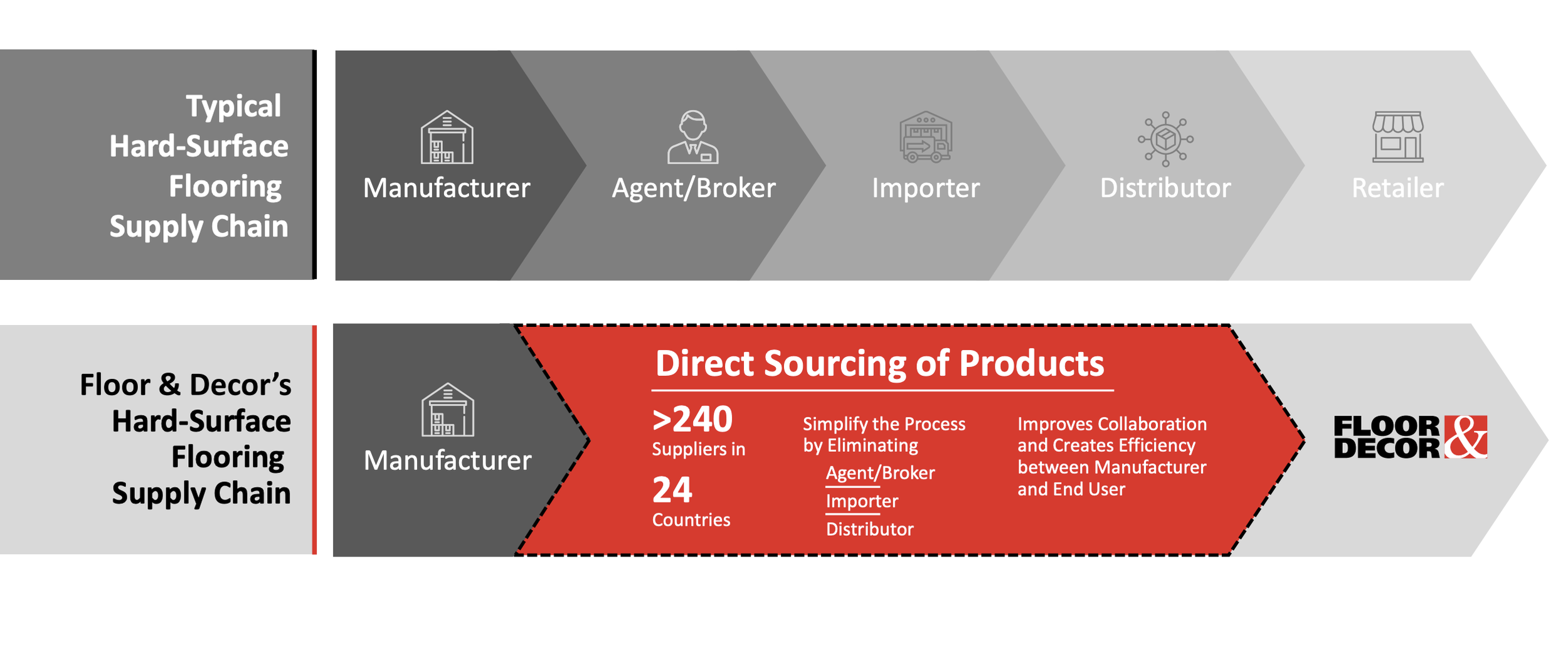

Then the huge amount of volume they have, allows them to go to direct to manufacturers.

Floor & Decor has over 230 direct manufacturer suppliers.

This is very important in managing cost pressures, because as we’ve seen with the China tariffs back in 2018, and global tariffs more recently, they are able to shift supplies to different companies, which minimizes the effects of dramatic price increases on the supply side.

By going direct to manufacturer, it also allows you to eliminate a layer of markup that many other competitors have to pay, which allows them to offer lower prices.

So we can start to see this flywheel that they have going:

A big warehouse allows them to offer the widest selection, which then enables to having the in-stock inventory. Buying in volume allows them to go direct, which then enables them to have lower prices that both consumers and professionals appreciate.

In addition to having such a large warehouse, they can allocate square footage to their decor and design business.

They devote a lot of store space to having vignettes, which are displays to show how different floors can work with different designs so a customer can look at them.

They could also work directly with an in-store designer to help you pick out, measure, and show you different types of flooring for your project.

A disclosure that was given out a few years ago stated that, customers who work with an in-store designer have on average 3-4x higher overall ticket size than those that don’t work with a designer.

On top of that, they practice what is known as micro-merchandising, which allows the store manager to have input in terms of what is actually shown in store.

A lot of times, the store manager will know what sells best in their local market.

This means they not only have more selling space devoted to products, but devoted to the right products localized to the right market.

By having a warehouse model, it enables their whole value prop.

Unless you’re doing all of these things, it’s hard for you to do any of them well.

Let’s compare Floor & Decor’s model to LL Flooring’s to explain why.

The Fall of LL Flooring.

LL Flooring was a competitor who went bankrupt last year.

They operated from storefronts that didn’t have any warehouses attached to them.

That means that you would go into their store, place an order, and they would try their best to deliver it to you.

The problem here is it would take an order to arrive 4-5 days, a week sometimes, which as we mentioned earlier, if you are professional flooring installer you could lose a sale if your supplies are not on time.

Because LL Flooring didn’t have a warehouse, they didn’t have in-stock inventory to offer customers the same day.

So LL Flooring wouldn’t be able to address in-stock inventory without literally ripping apart their whole storefronts, because they needed a warehouse model in order to have inventory across thousands of SKUs.

Having a storefront model wasn’t the correct way to build the business in order to offer the value prop that consumers cared about.

This is where a framework I call the Consumer Hierarchy of Preferences comes in.

The idea behind this is that consumers preference different things and once you fulfill enough of these consumer preferences, you get a sale.

In this case, if we think of what a professional installer cares about, they care about:

1. Making sure there’s enough selection to satisfy the client

2. Low enough prices to satisfy the client

3. In-stock inventory

If a business can’t offer these preferences, it’s not a sufficient value prop.

But in order to offer this value prop that these professionals care about, you have to set up your business a certain way.

Piton Network.

Businesses make strategic decisions every day.

We can think of a decision as a piton.

A piton is a metal stake that a mountain climber hammers into the side of the mountain and then suspends a rope from.

The mountain climber is suspended because of this piton.

While the piton is supporting the mountain climber, it is also constraining where they can go.

They are limited in their future decision space.

So, a strategic decision a business makes, or a piton, enables certain decisions at the cost of other decisions.

For example, you wanted to open up a restaurant and the restaurant lease your purchase is very small with very little in-store dining, but it’s in a great location with a lot of traffic coming through with parking nearby.

What kind of restaurant are you going to build given you made this decision?

Well, you’re not going to have full service in-store dining with a waiter.

You’re probably going to lean more heavily on a takeout business.

If you lean heavily on a takeout business, it can’t be that expensive because people don’t like really expensive takeout food.

You are better off charging something that is mid-price or on the cheaper side.

That means you need to make it up with a lot of volume.

Now, you thought you were just making one decision in terms of what restaurant lease, but it turned out it shaped everything in terms of what your business would be good at.

This goes to show you that how when you make a single decision, a piton, that is now going to enable you to build a business a certain way while at the same time constrain you from building different businesses.

Business makes these decisions all the time.

They are filled with so many different pitons.

When you stack multiple pitons on top of each other, I call it a “piton network,” because when you have multiple decisions that work with each other, that enables you to offer an even stronger value prop, but it constrains you from doing other things.

Floor & Decor’s Piton Network.

If we think about Floor & Decor, the decision to open a warehouse store, that was a piton.

That enabled them to have the widest selection and the in-stock inventory.

That also worked very well with a high-volume business, which allowed them to go direct to suppliers, because you can’t go direct to a manufacturer unless you have a lot of volume to place with them, which meant that in turn, you could get lower prices.

As you can see, these decisions work together.

Now, what business did they maybe lose by making this decision?

Well, Floor & Decor is not going be the highest-end flooring retailer.

If you are looking for very high-end designs, you are not going to a warehouse.

You are going to work with a higher-end designer and have your flooring customed order.

That’s not going to be Floor & Decor’s business

In addition, since they devote their warehouse to just flooring, that’s at the cost of them being able to sell everything else.

By them specializing in just in flooring, they now have a risk that if they add too many other categories, they’re killing their value prop.

If they move too much into other home goods, they risk confusing the customer, which leads the customer to think “Why don’t I just go to Home Depot instead?”

So by focusing just on flooring and making that their specialty, that is an advantage if you are a flooring retailer.

If you want to sell other stuff though, it’s actually a disadvantage.

Someone buying flooring versus buying flooring and then also getting kitchen cabinets are two very different customer journeys.

This all comes down to the decision they made to become a special flooring retailer.

So if we think of this warehouse model as a piton, competitors are not going to be able to copy them unless they also want to build a warehouse out and devote most of the retail space to flooring.

But you maybe thinking, what about Home Depot and Lowe’s? They also use the warehouse model.

Yes, but they made a different decision where they said, “We’re going to cater to everything in regards to home improvement.”

Whereas Floor & Decor is just flooring.

In fact, Lowe’s tried to copy the Floor & Decor model by going direct to manufacturers and having more in-stock flooring, but what they found out was that it didn’t work for their business model.

Lowe’s couldn’t keep enough in-stock inventory because they weren’t willing to devote that much store space to just flooring.

They had all these other categories and prerogatives that they needed to account for.

It’s a lot easier for a company to optimize to be the best flooring retailer or the best home improvement center versus trying to be the best improvement center who is also trying to attract a professional flooring business.

In the end, competitors can’t copy them unless they’re willing to build a warehouse model and devote all of the selling retail space to flooring.

That doesn’t mean though that there’s competition, it’s just competition on a different competitive vector.

Competition.

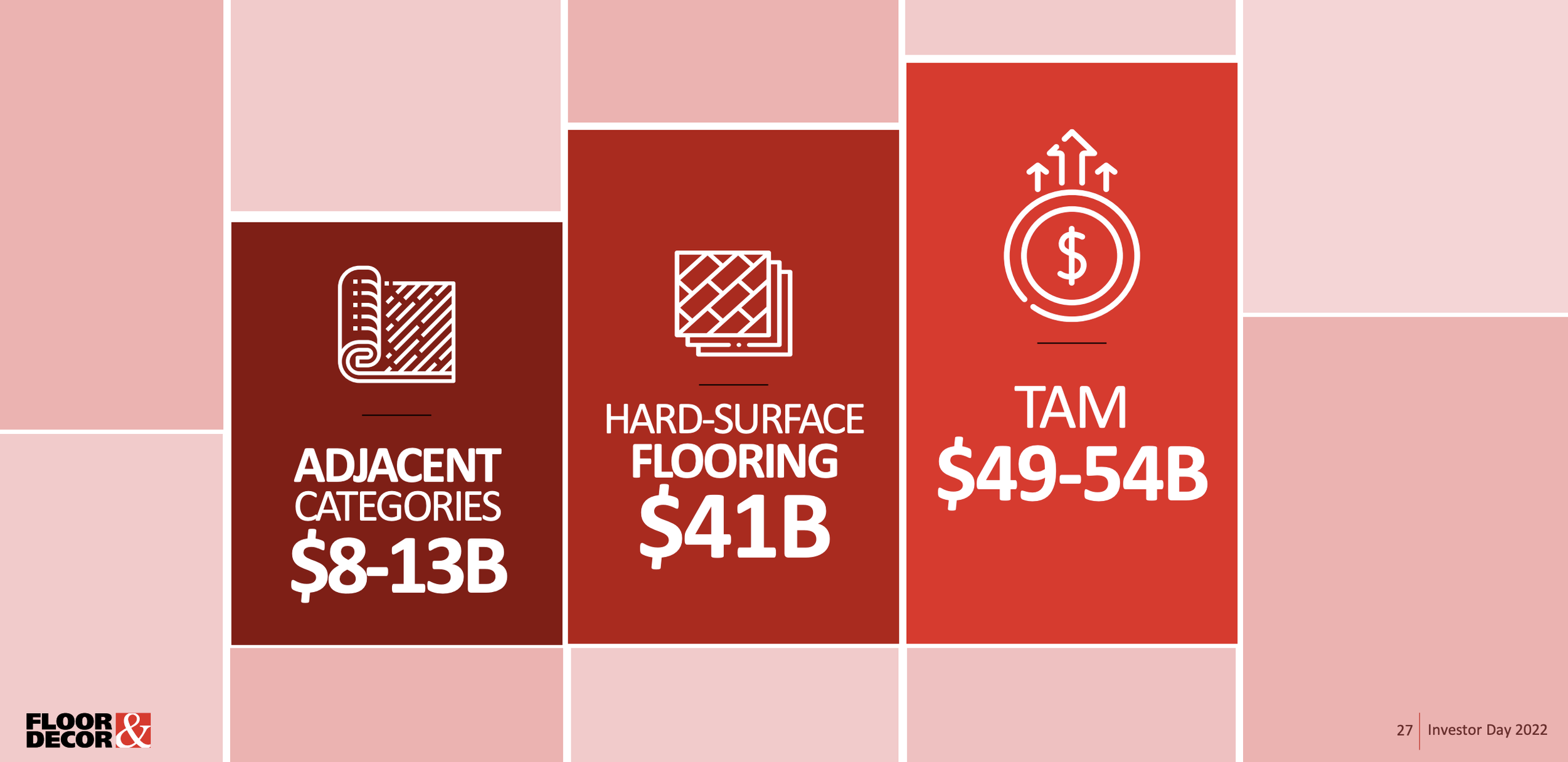

The overall hard surface flooring TAM is ~$40bn.

Floor & Decor is at 10% of that, because right now they have $4.7bn in revenues.

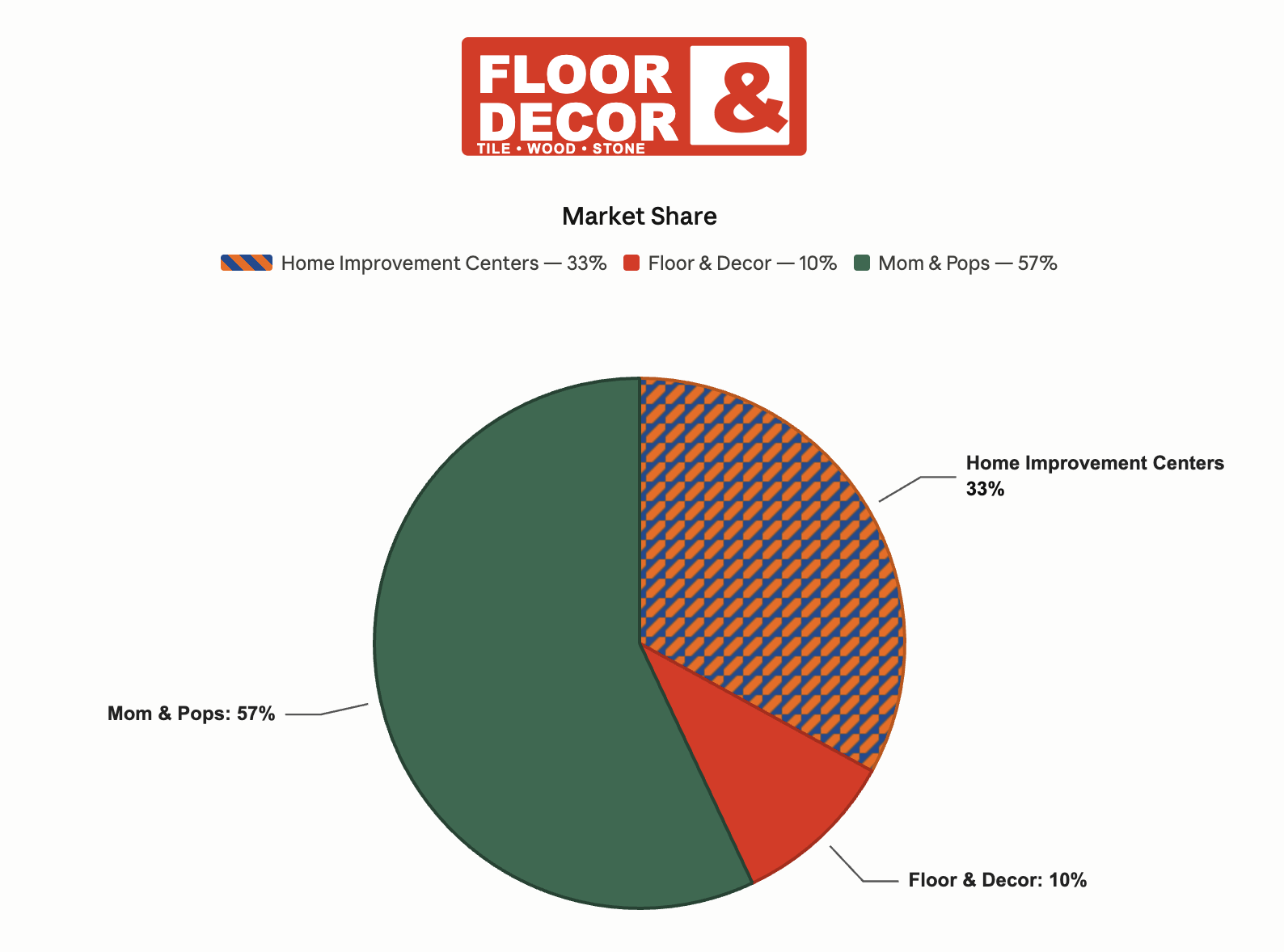

Now, they have two set of competitors: 1) the home improvement centers (ie. Home Depot & Lowe’s) and 2) independent Mom and Pops.

Floor & Decor has been taking a lot of share from these Mom and Pop flooring retailers in the past few years because of this tough macro environment.

As I mentioned earlier, a lot of sales were pushed up during covid, in addition to that, higher interest rates meant that existing home sales fell, which a big trigger event to replacing your flooring is when you buy or sell a home.

Without that trigger event, everyone in flooring has been depressed, not just Floor & Decor.

Home Depot had negative same-store sales.

We talked about LL Flooring going bankrupt.

Another competitor, The Tile Shop, went private last year.

A lot of Mom and Pops went out of business as well.

This has been a tough market for everyone.

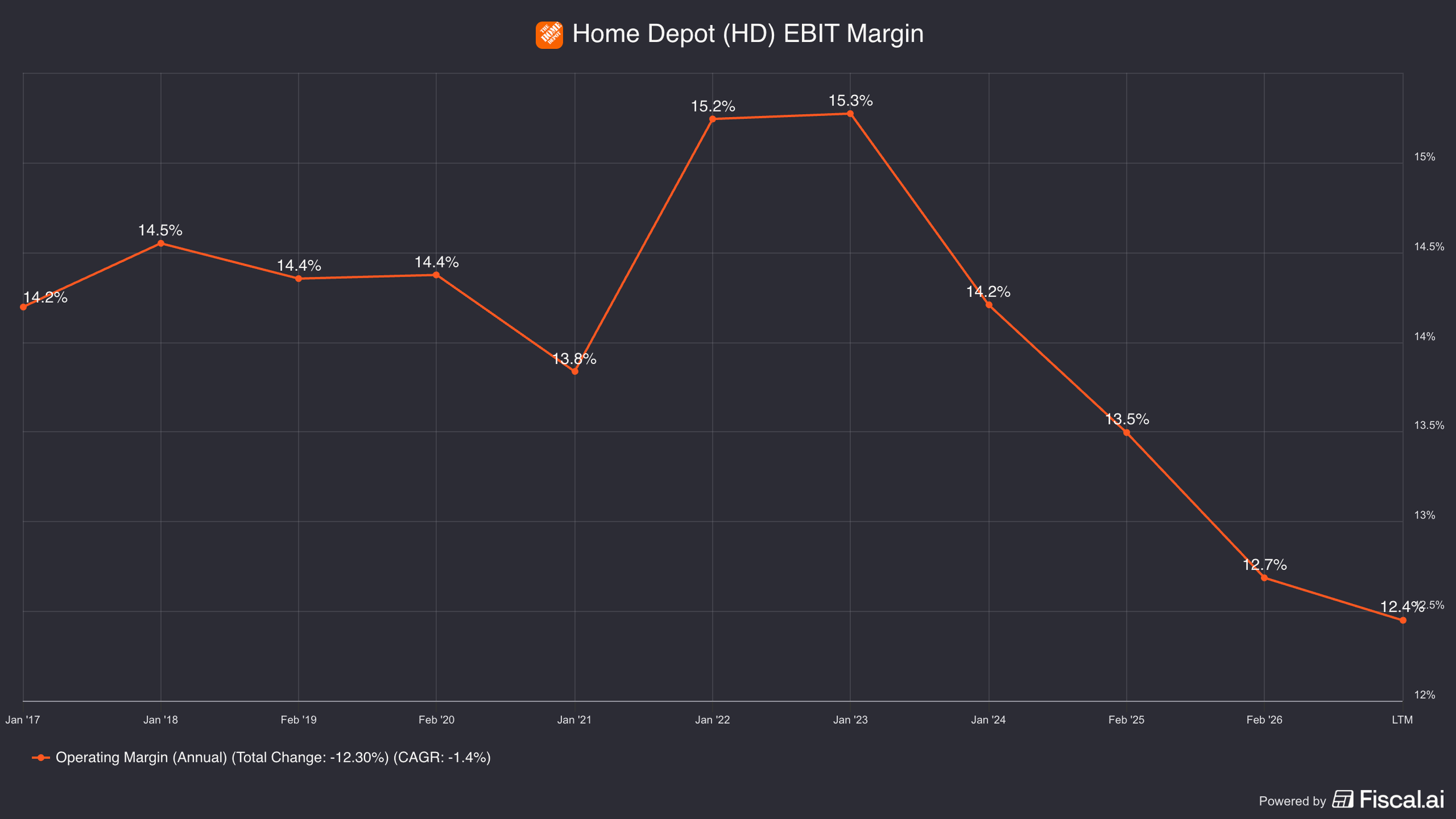

Floor & Decor’s biggest threat right now is the home improvement centers.

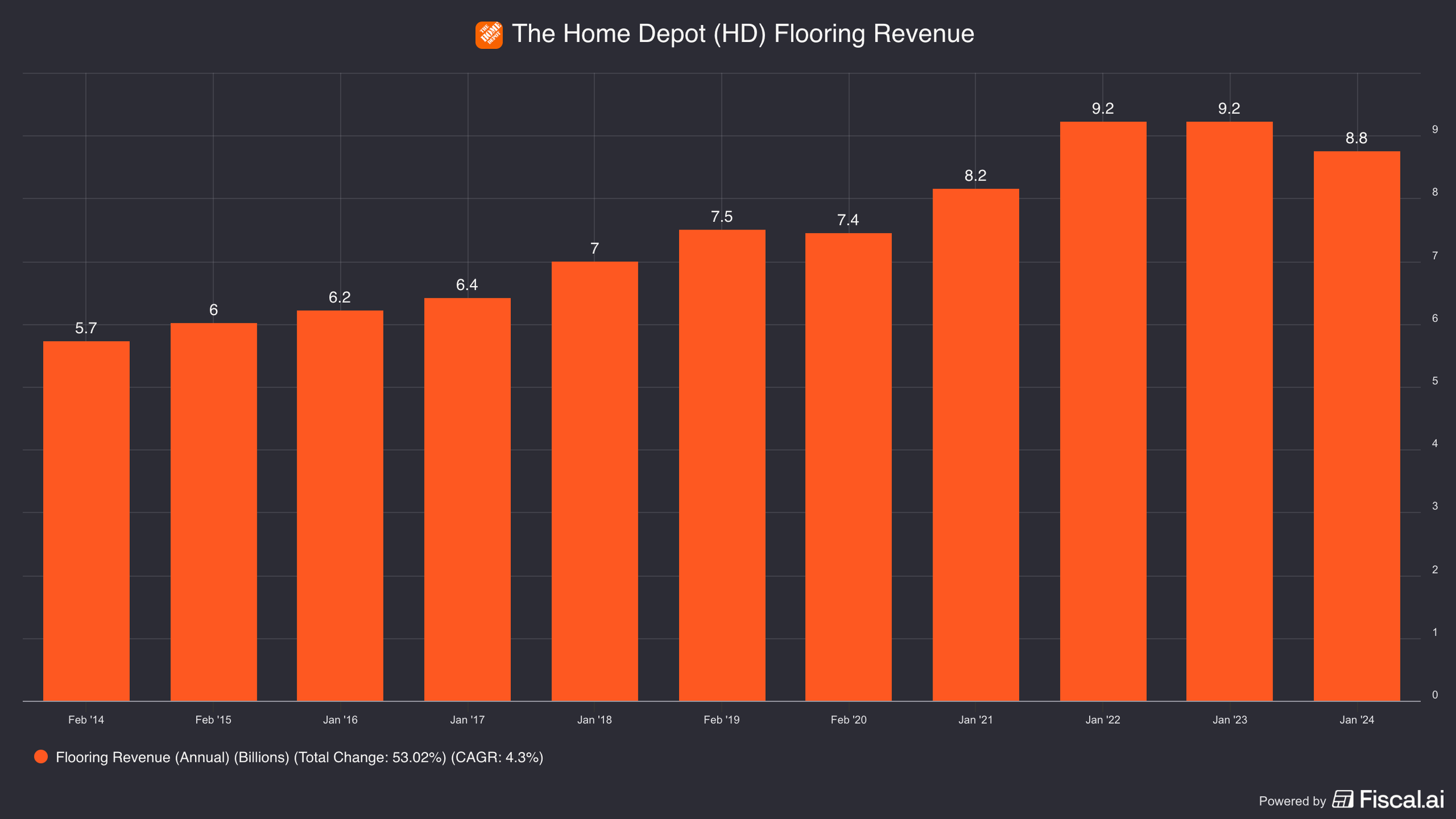

Home Depot and Lowe’s sells more flooring than Floor & Decor at about $8bn and $5bn, respectively.

The customer who goes to Home Depot is going there because they know Home Depot is convenient and it is good enough.

Home Depot has a few hundred SKUs that they can pick from and they are okay at not seeing thousands.

That’s going to work for a lot of people, just not everyone.

And certainly not for the professionals, where you need a lot of different SKUs, and need it all in stock.

Home Depot does do a blend, where they have some in stock and they can also order on your behalf and send it to your home.

For a lot of people that is good enough for them, because they can arrange a professional to install it or they can do it themselves, which is a relatively easy job.

But there is going to be the need of a specialty flooring retailer that caters to those who care about more options and for the professionals, and that is Floor & Decor.

If we think about the market share split, 33% is going to home improvement centers, 10% Floor & Decor, and 57% independent Mom & Pops.

Floor & Decor expects to take share from these Mom & Pops over time because they can provide a much better service, more selection, more in-stock inventory, and better pricing.

The other competitor that is worth mentioning here is Amazon.

You could buy your flooring from Amazon but the problem with that is this is a category people like to be able to see exactly how it looks, because how it looks online can be different than in person.

It’s also a project that you are going to do once a while, so you put more care and time into it, which means you are willing to drive 30 minutes to a Floor & Decor for that project.

For these reasons, flooring has been an insulated category from e-commerce, but there are some people where they are okay with ordering their flooring online.

This isn’t the majority of people and we haven’t seen that to be a real competitive pressure to Floor & Decor.

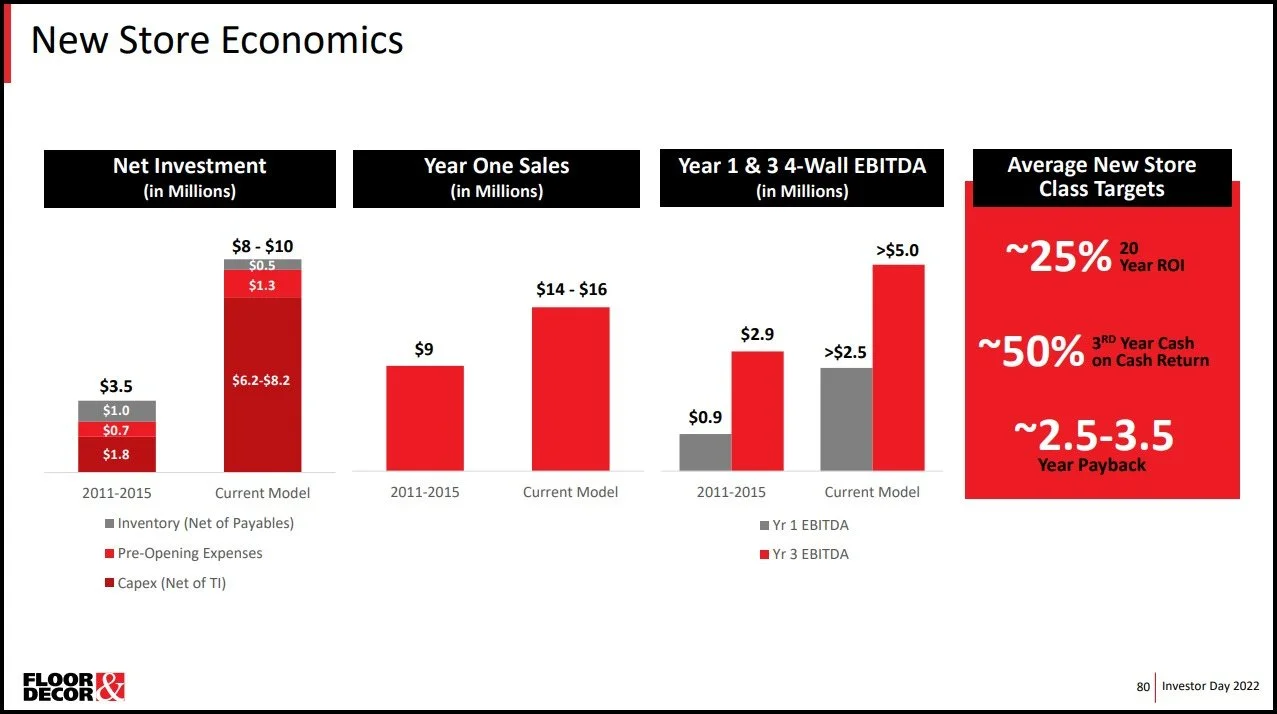

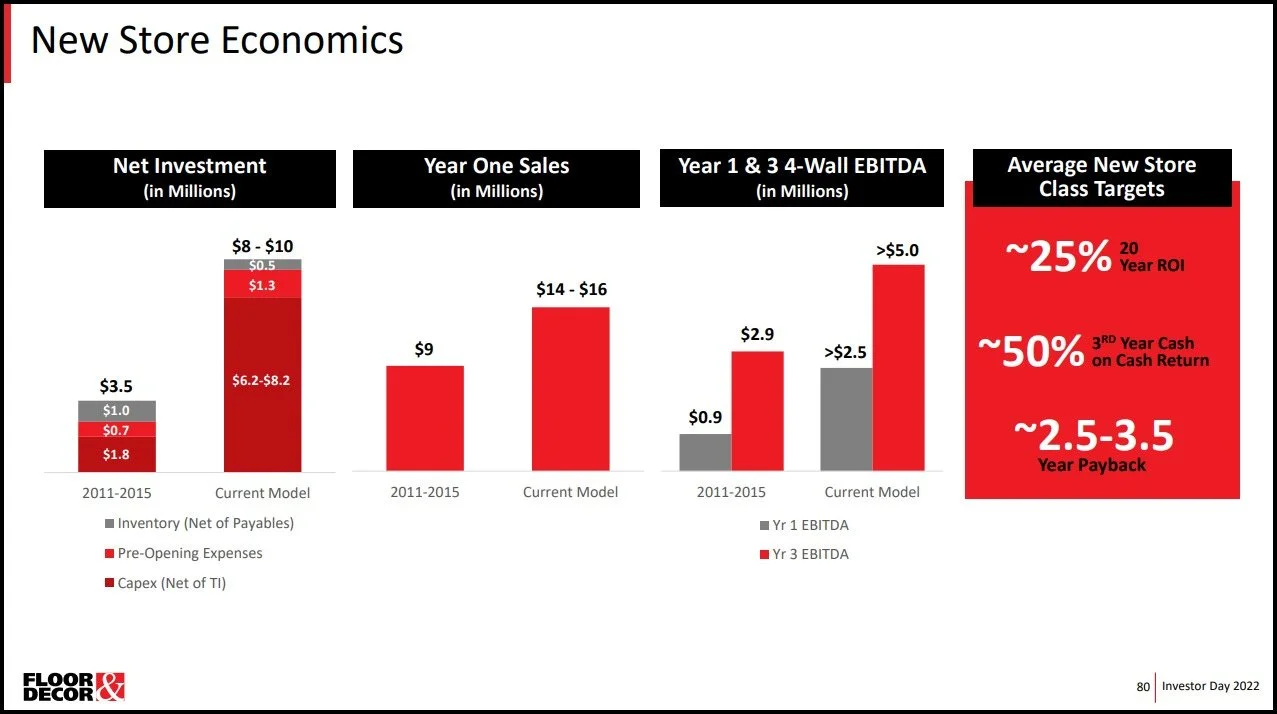

Store Model.

Each store costs $8-10mn to build.

In year 3, they expect to have $5mn in EBITDA.

Giving them a 50% cash on cash return in year 3.

It is important to note that this is on the original store model of 80,000 sq ft, but recently they have been moving more into the East Coast and haven’t found that many 80,000 sq ft warehouses so they’ve been scaling down to 60,000 sq ft, which saves them a couple million on upfront costs.

This is a mix shift that is happening but in terms of the actual return profile it’s pretty similar.

When a new store opens up, it could take as long as 5 years to ramp up.

This is ramp up time is what is plaguing their financials.

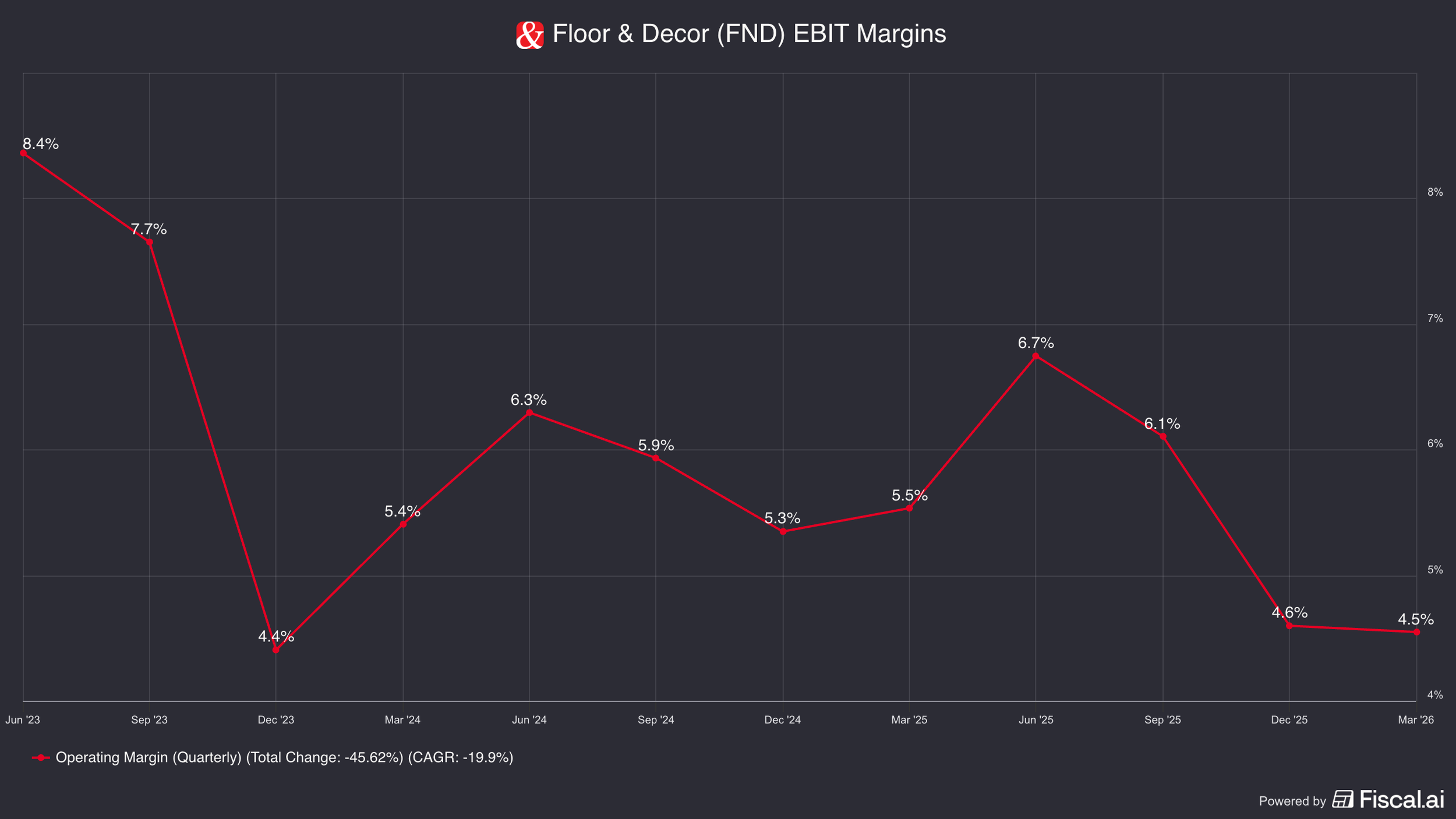

If you look at their financials, you’ll see EBIT margins are ~5%.

Why is that?

It is because it can take up to 5 years for a store to ramp up fully and in addition to that, when a new store opens, it usually cannibalizes other stores initially, but after 3 years both stores end up growing thereafter, because you get more professionals into the ecosystem.

This is a headwind to sales in addition to all of the macro headwinds we have already discussed.

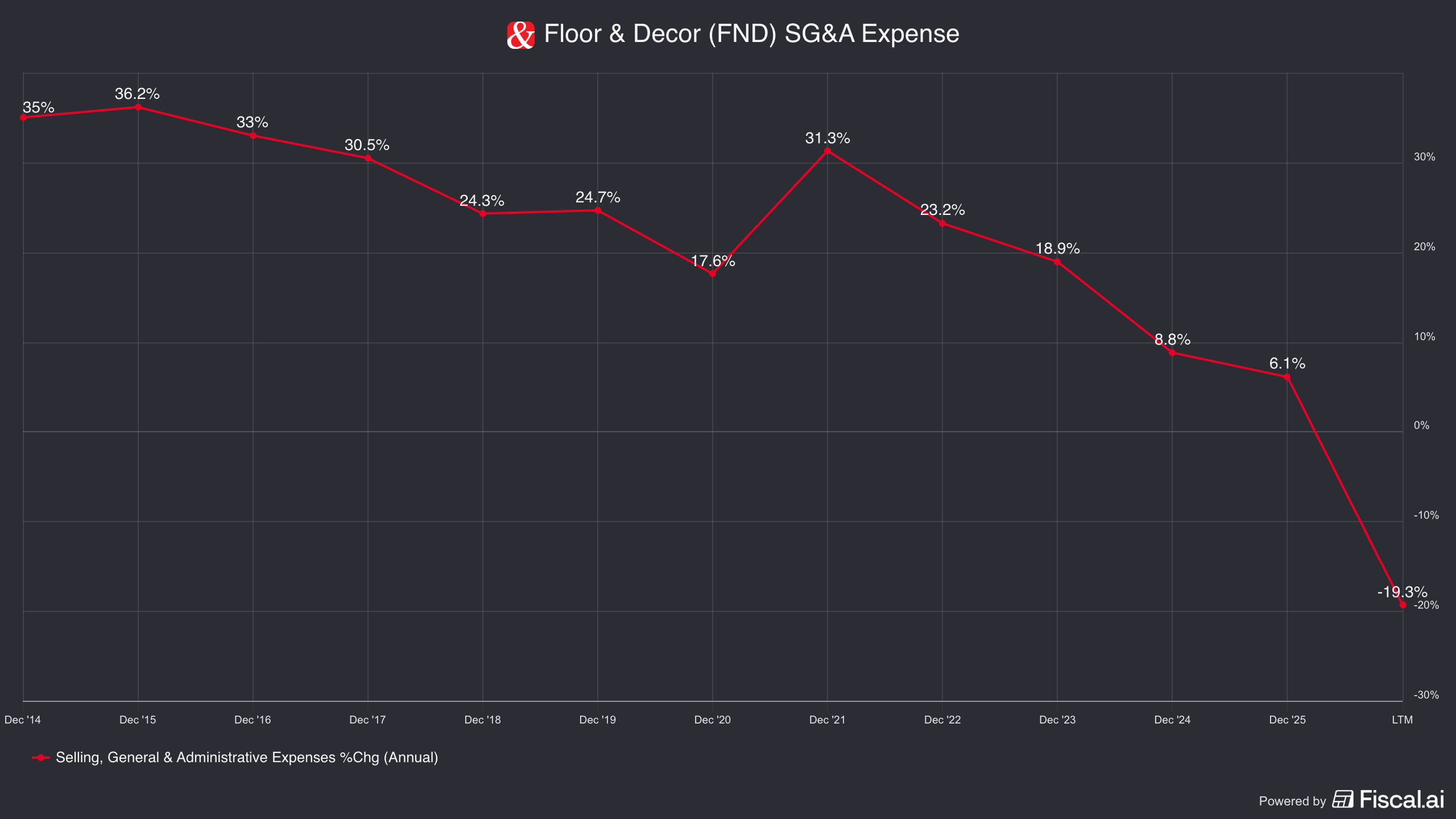

Since they are opening up 20 new warehouse stores a year, pre-store opening expenses are weighing on operating expenses, which is depressing margins to that 5%.

They have done some cost initiatives by reducing SG&A by-19% y/y.

So they are trying to become more cost disciplined to maintain profitability.

Margins were never that high because they were in growth mode by adding ~20 stores a year.

Before it was ~30 stores a year, so they could take that back up when the market turns.

So they have depressed housing market pressuring the top line, while carrying all the expenses for these new stores they are opening, pressuring the bottom line.

If we move past this and look at more mature economics, they have talked about doing high teens EBITDA margins.

If we look at some peers like Home Depot, that seems very plausible that they could reach that.

But what does this mean for valuation?

Valuation.

Let’s say they can achieve 10-15% mature EBIT margins.

If you are taking EBITDA, you could assume a few points from D&A and that would get you to the 10-15% EBIT margin.

So 10% would be conservative and 15% is optimistic.

At IPO, they had a goal of 400 warehouse stores.

They later raised this goal to 500 warehouse stores.

They currently are at 276 warehouse stores.

How much does each store make at maturity?

The most they’ve ever quoted a store actually doing was around $30mn.

Now that was a dominant mature store in an elevated demand environment.

While they could achieve that, we want a more normalize number, so we will haircut that to $20-25mn per store.

So what is priced in today?

If we look at what the company will do in 2026, they guided to $4.8-5bn in sales.

Let’s say the hit the low end ($4.8bn) and can do 10% margins at maturity, and apply a 20% tax, that’s about $380mn in NOPAT.

Their market cap right now is $4.8bn, which puts them at 13x mature earnings ($4.8bn/$380mn = ~13x).

Let’s now value them over the long term.

We will do two scenarios:

1. Conservative Scenario: They reach 400 stores at $20mn/store with 10% EBIT margins over 6 years

2. Optimistic Scenario: They reach 500 stores at $25mn/store with 15% EBIT margins over 11 years

Conservative Scenario.

In the conservative scenario, they will generate $8bn in revenue (400 stores x $20mn/store).

After applying the 10% EBIT margin and tax, that is $640mn in NOPAT.

Let’s assume a conservative but fair multiple at 15-20x.

Applying this multiple range, that would give them an enterprise value of $9.6-12.8bn.

Now this is over 6 years, so if we take their current market at $4.8bn, this would be a 12-18% annualized return.

Optimistic Scenario.

In the optimistic scenario, they will generate $12.5bn in revenue (500 stores x $25mn/store).

After applying the 15% EBIT margin and tax, that is $1.5bn in NOPAT in 11 years.

Let’s apply that same earnings multiple range of 15-20x.

This would give them an enterprise value of $22.5-30bn.

Again, if we think they can achieve this in 11 years, that would be a 15-18% annualized return at today’s market cap of $4.8bn.

Now, what are some risks to the business?

Risks.

There are 4 risks that I see plaguing Floor & Decor.

Risk #1: Non-Essential Durable Good

The first is that flooring is a non-essential durable good, that is easy to defer and is infrequently purchased.

Within a given year, you don’t need to replace your flooring, but eventually after 10-20 years you will have to.

But you can continue to defer purchasing flooring for a long time.

Now, on the other side of that is when you do replace your flooring, do you want to go to the place that has the most selection, the lowest prices, the most in-stock inventory?

But at the end of the day, a consumer doesn’t care about that that often.

They only care about it when they’re in the market for flooring, which doesn’t happen, especially when you’re not buying or selling a home because that is a big trigger event.

This is what creates the cyclicality in the business.

Risk #2: Tom Taylor Leaving

Tom Taylor was the former CEO who was a big part of growing the business.

He was there since 2012 and just left last year.

He helped them navigate a pretty tumultuous time from the original China tariffs in 2018 to the shipping issues during covid, to the more recent Liberation Day tariffs.

He’s staying on as chairman of the board, but the CEO who replaced him was someone from the outside.

Risk #3: Category Expansion.

As I mentioned earlier, they have experimented with selling kitchen cabinets and the risk here is they expand into more categories and clutter their value prop.

The more categories they add, the less space there is for their flooring inventory.

No one is thinking of getting this kitchen cabinets at Floor & Decor.

While yes, they could cross sell a customer on kitchen cabinets once they get flooring, the sale is not going to go the other way.

Someone buying flooring versus buying flooring and then also getting kitchen cabinets are two very different customer journeys.

As we talked about in the piton network section, a clutter value prop gives a customer becomes distracted and gives more reason to look at a home improvement center rather than Floor & Decor.

But this is something where you have to trust management is doing the analysis and doing these trade offs.

Risk #4: Weak Housing Market.

The housing market hasn’t improved since 2022.

There have been multiple false starts where existing home sales look liked they were starting to comp positive but something happened in the world and they went back down.

More recently, we are seeing inflation picking back up a little bit and that comes with the potential of a Fed rate increase.

When interest rates are high, that means mortgage rates are high, which translates to a damping in existing home sales.

If you have a low interest mortgage locked in, you are less likely to sell your home.

So there is no telling when this market will turn.

But it is possible as soon as there is a sign, the stock could run up very quickly ahead of that.

We’ve seen that happen in 2024, when the stock rallied to $130/share, before falling back down to $45/share.

But predicting the macro environment is a hard game to play.

The way I like to think about this though is a great company is like buying a very strong ship.

You want to make sure the ship is well-built to last any potential storms, but you’re not necessarily be able to predict all the storms or how bad they’re going to be.

So instead of trying to predict the weather, you want to find a ship that is well-built that will withstand the toughest storms.

But it is up to you as an investor to decide whether you want to take a journey with the Floor & Decor ship or not.

For more on Floor & Decor, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.