Is the S&P 500 Too Concentrated to Be Safe?

Get smarter on investing, business, and personal finance in 5 minutes.

This Five Minute Money was adapted from a recent video Drew Cohen had on the topic.

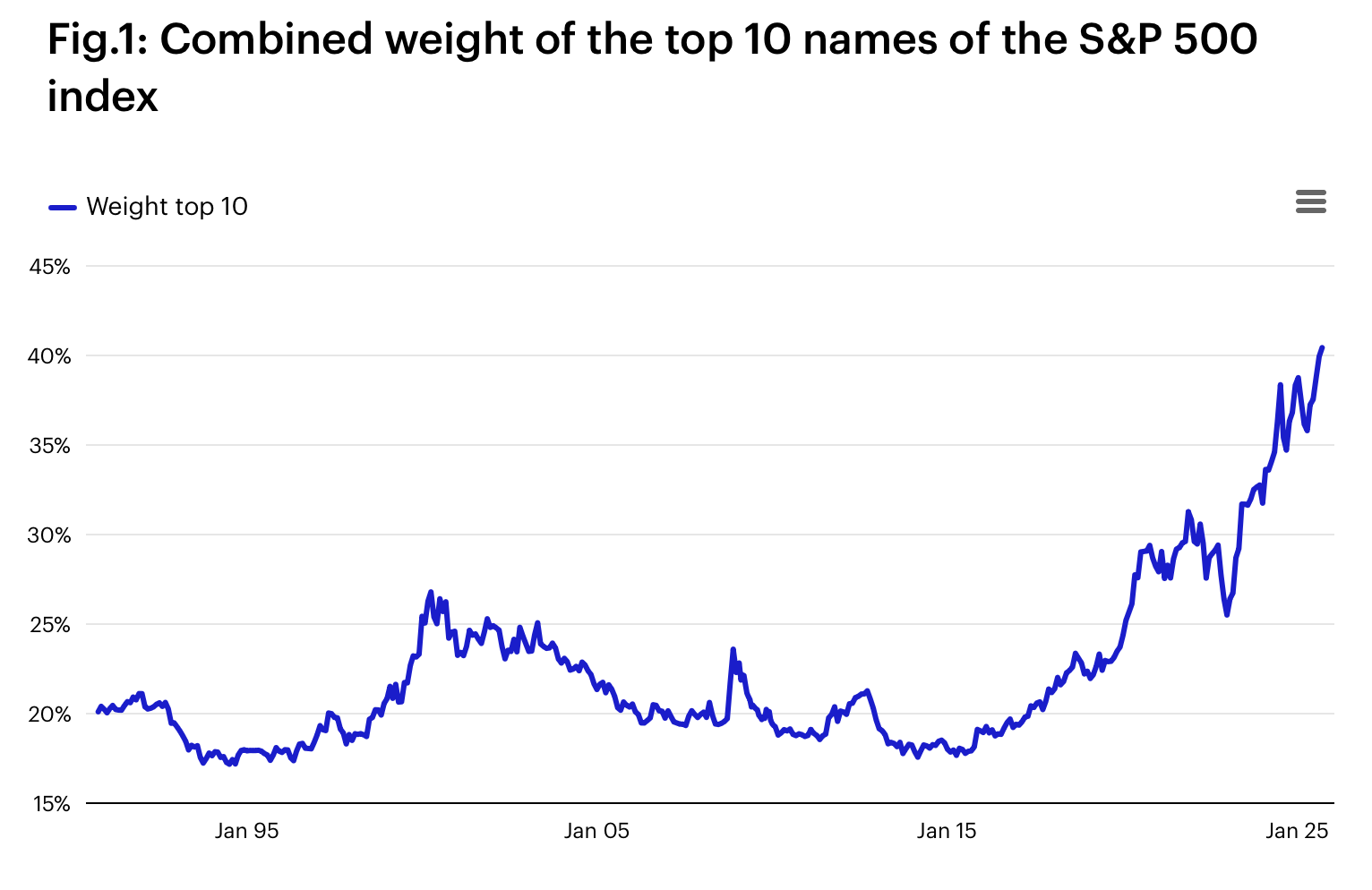

From 1990 to 2015, the average concentration in the S&P 500 for the top 10 stocks was about 20%.

Today, that number is more than double at around 40%.

Increasingly, as an investor buys the S&P 500, instead of getting this broad portfolio of 500 different stocks, what they're really getting is more and more a bet on the technology sector, as well as a certain degree to momentum.

The real problem though is, what does this level of concentration portend for future returns?

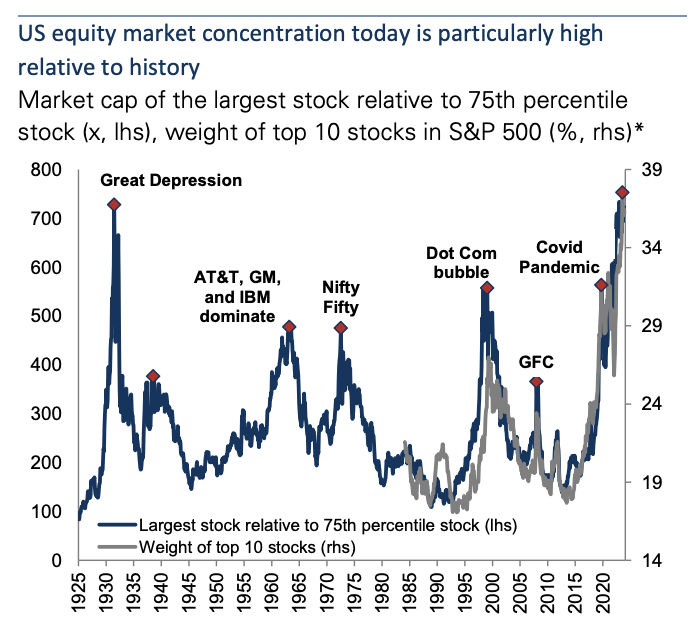

This level of S&P 500 market concentration has not been observed since the 1930s and has already eclipsed the level during the tech bubble.

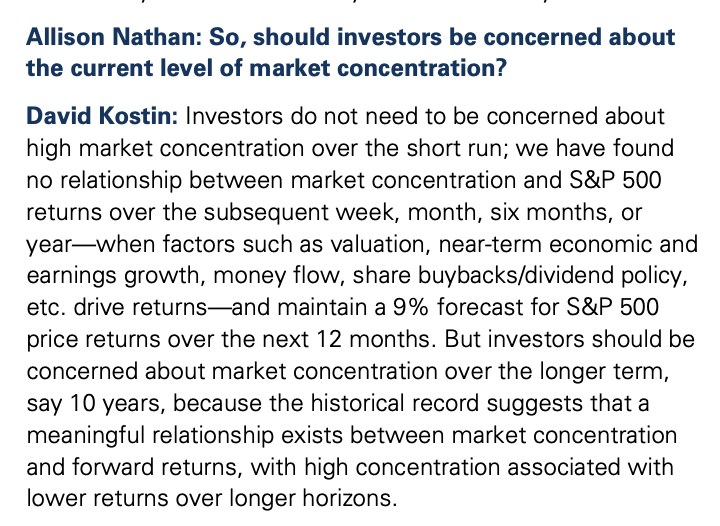

Goldman Sachs chief economist David Costa had this to say about market concentration as it relates to future returns

Now does that mean, though, that we're due for a correction or how worrisome really is this level of concentration?

We break all of this down in this week’s Five Minute Money!

The Real Risk is High Valuations, Not Concentration.

I don't think the real risk is concentration.

I think that concentration is associated with what the real risk is, which is high valuation.

The real concern has more to do with the valuation multiples in buying into an index at elevated valuation multiples, which tends to mean lower expected returns over the long run, more than the concentration risk in and of itself.

That doesn't mean concentration risk doesn't have some risk associated with it.

But the bigger risk is a high valuation multiple.

These two don't have to go together, but they tend to, and part of that is because of how the index is built.

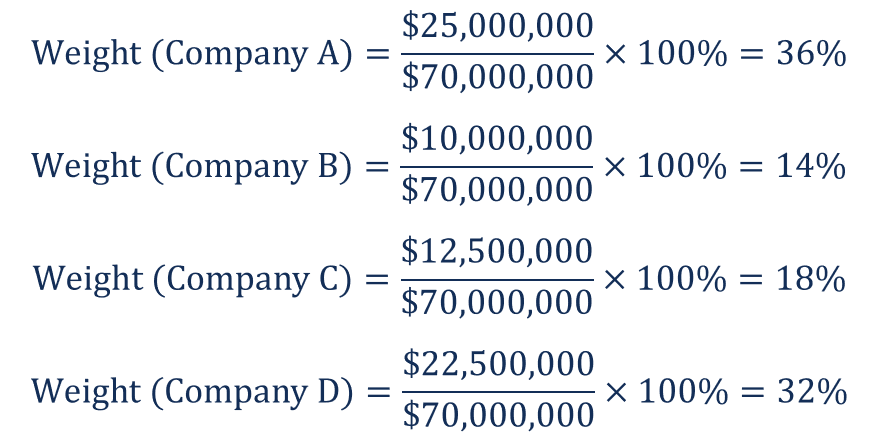

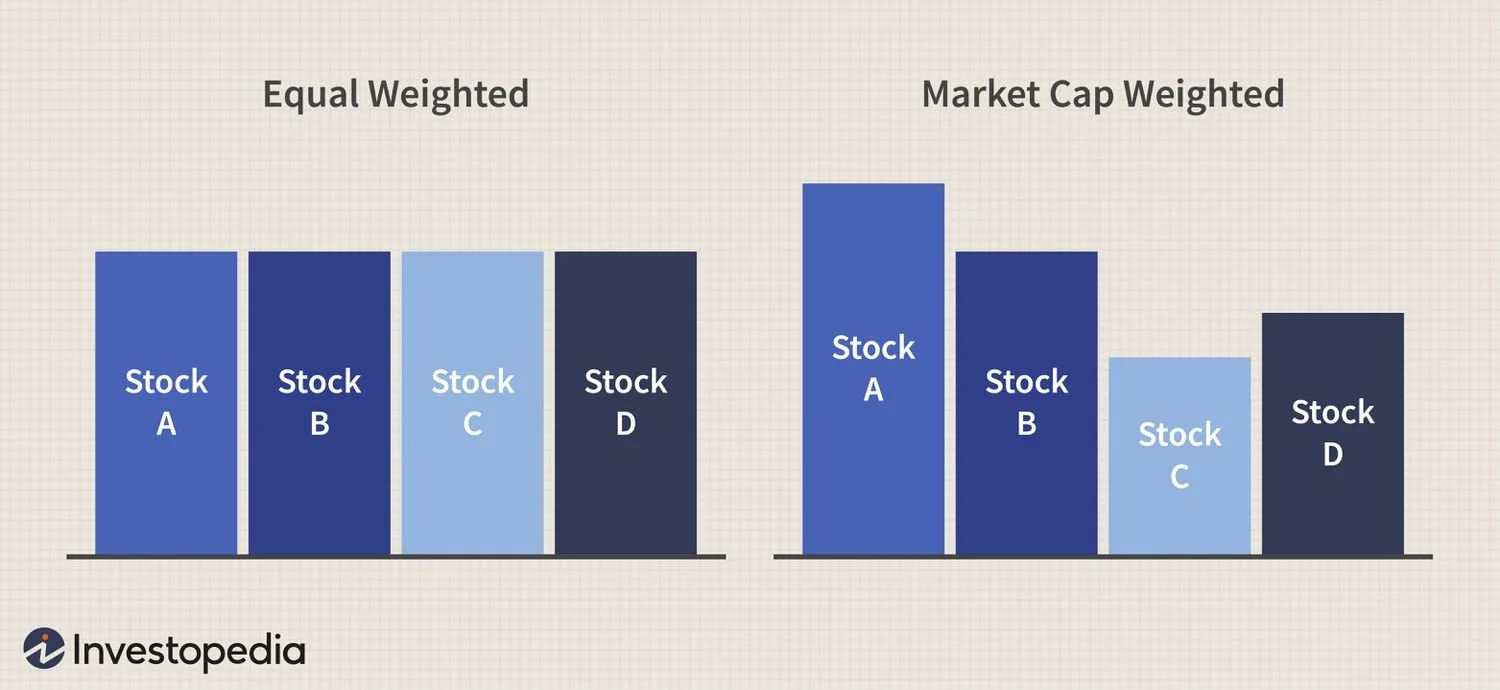

In short, the S&P 500 is a market cap weighted index.

What that means is that the amount of a specific stock's weighting in that index is going to be dictated by its market cap.

The way you calculate that is if you sum up all five hundred companies in the S&P 500, you take their market caps together, that's going to be your denominator, and then your numerator is going to be the market cap of an individual company.

For example, let's say a company had a market cap of a $1bn and the total value of the index was a $100bn it'd be $1bn/$100bn

You get your weighting of 1% ($1bn/$100bn = 1%)

If that market cap doubled though to $2bn, then all of a sudden the entire index is now worth a $101bn.

Now that companies weighting increases to 1.98% ($2bn/$101bn = 1.98%)

As you can see, as a company gets bigger in size, it continues to grow as a portion of the index.

That means as an investor investing in it, you will continue to own more and more of these companies.

Now there's a few things that are worth noting.

Whenever you're buying into an index, it's going to go ahead and buy those underlying securities agnostic of valuation.

This is going to be a big deal for target date funds, retirement funds, people who every couple weeks are invested into the market, or people who are just cost averaging into ETFs over time, which is not a bad strategy at all, but it is going to be valuation agnostic.

As more flows goes into these ETFs, then the ETF providers are going to buy the underlying securities and as these stocks like Nvidia and Google become a bigger and bigger portion of the index, they're going to be buying more and more of these stocks just mechanically.

The reason why I'm pointing this out here is because very often when we talk about market concentration, usually people bring up this idea of passive ETFs and investing and there's a little bit of kind of this skepticism that this is resulting in the market kind of being “stupidly valued," and now there's not actual active investors that are doing price discovery on these companies.

Instead, it's “dumb money” being plowed into the indexes at any valuation. And that's kind of what's propping up a lot of this.

Personally, I don't think that makes a lot of sense to me because if you look at the actual volume and who's doing a lot of the trading on a given day, the majority of it's going to be active investors, right?

Now, passive is about 1/3 of total assets, so it's not a trivial amount, but again, most of the volume is still going to be active and that's where the price discovery is going to happen.

So I don't think that is a reason to not own ETFs or to really be skeptical of evaluations in an index in and of itself, because there is still a lot of active money that is going to put more money to work in lower valuation stocks versus higher valuation stocks.

There's also a lot of ETFs that are quant ETFs that do exactly that sort of factor analysis, et cetera.

Now, as I was saying earlier, the big risk in my opinion is more the high valuations rather than the concentration risk in and of itself.

If we pick what these companies are, NVIDIA, Google, Meta, Apple, Amazon, if I were to tell you you're going to buy all of these at a 15x multiple, you really wouldn't be that worried about it.

If I was going to tell you they're at a 30x multiple, you're going to change your opinion on that.

That is why I think the valuation aspect is the bigger risk here.

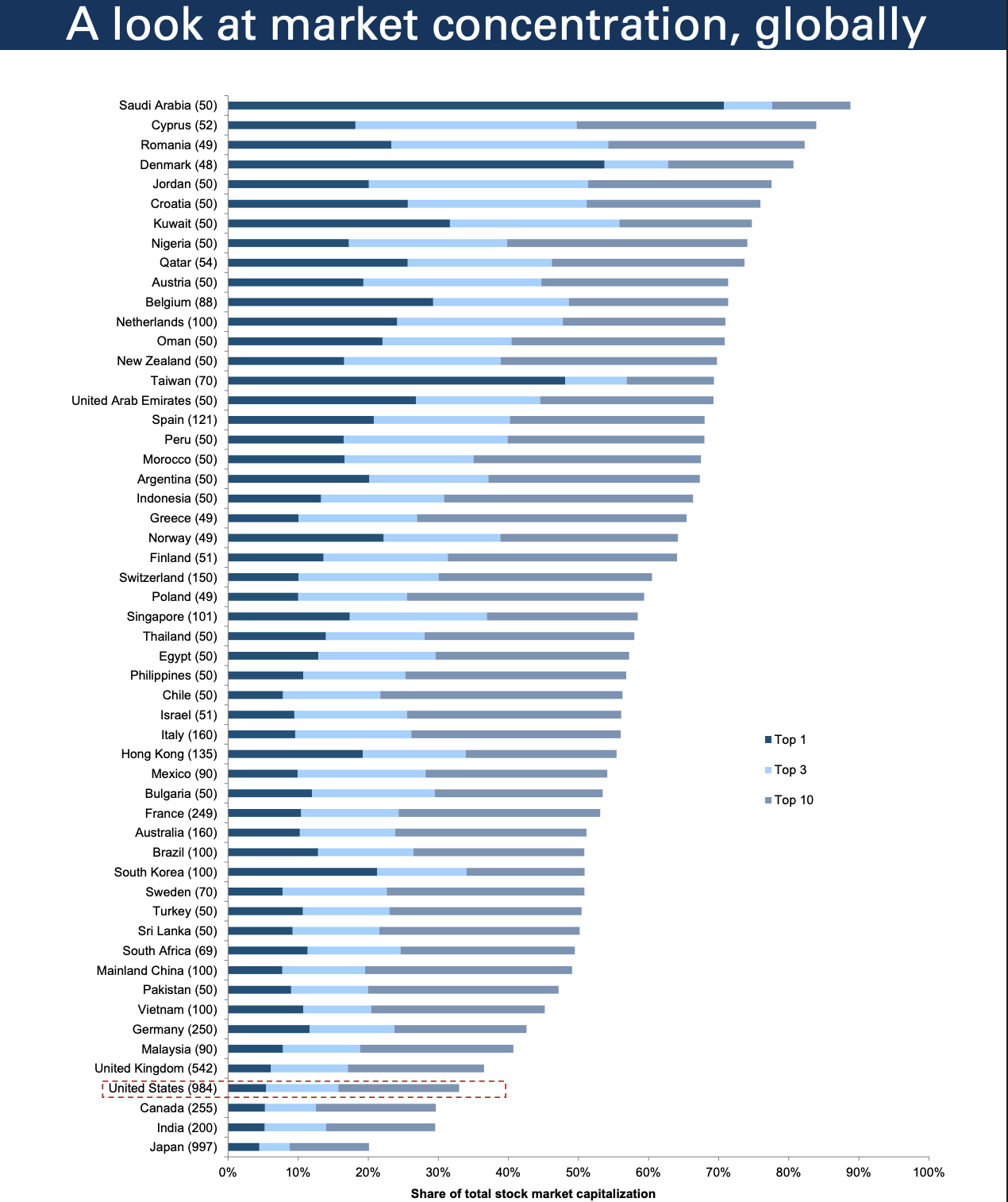

The point is, it's not necessarily the concentration risk in and of itself that is concerning, and if you look at other international markets, like Taiwan, they have over 50% of the index in a single stock (TSMC).

If you look at Sweden, their top three stocks make up also over 50%.

In Canada, the top ten stocks are also around 40%.

No doubt this concentration level is high relative to historic standards for the US, but there's other international indexes that have always kind of had this higher level of concentration and so there's no magic number that says 20% for the top 10 versus 40% is the correct number to have.

Of course, when you are buying into the S&P 500, you kind of have this idea that you're buying five hundred companies, and then maybe you find out you're really buying, 40% of it's going to 10 stocks, and then the remaining 60% is going to the other 490, that might surprise you.

Is that the risk in and of itself? I really don't think so.

But if you are really concerned about that, you can buy an equal weighted index.

Equal Weight Hedge.

The equal weighted index differs from the market cap weighted index because every constituent, every stock in that index, is held in equal amounts.

That has a benefit of you getting a lot more diversification, right?

So if you're concerned about having too much in a few stocks, this diversifies you out a lot more.

It also tends to be a little bit of a reversion to the mean strategy relative to the S&P 500.

This is because, as I mentioned earlier when I wrote that when you buy the S&P 500, it is a little bit of a bet on momentum and that is because as companies get bigger, more money gets directed to these companies.

But there's also the fact that when a stock is doing well, and it could be for fundamental reasons, but then the stock price goes up, that high stock price also tends to bring in more investors that want to buy it up more, and that is another reason that you could get a little bit of feedback loop in there.

When you're invested in an equal weight index, it's kind of the opposite of that because whenever something runs up, they sell it, and then they put more money into the thing that's doing poorly.

So because of that, it acts as kind of this reversion to the mean balancing strategy.

Having said that, the other end of it is that big successful companies they tend to also be big and successful for a longer period of time.

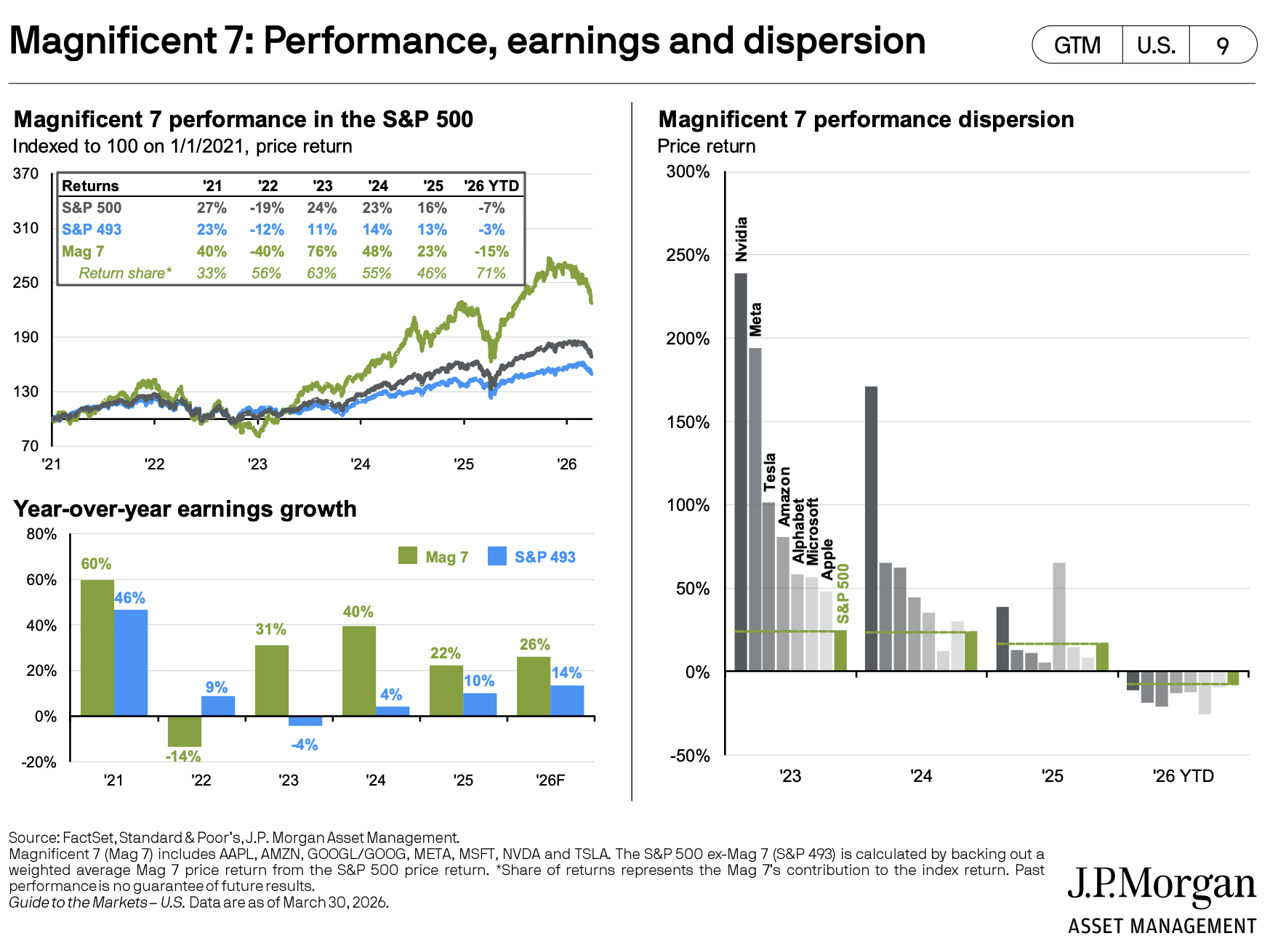

If you're looking at the success run of FAANG and later Magnificent Seven, for how long have people been saying that they can't continue to grow at these high rates of return forever?

But they've been growing a lot faster for a lot longer than many people have expected and they actually accelerated in the last couple years earnings of these companies have actually gone up even more.

Google and Meta for instance have re-accelerated earnings.

Just because a company is big doesn't mean in and of itself it's going to be a bad investment.

Potential Future Returns.

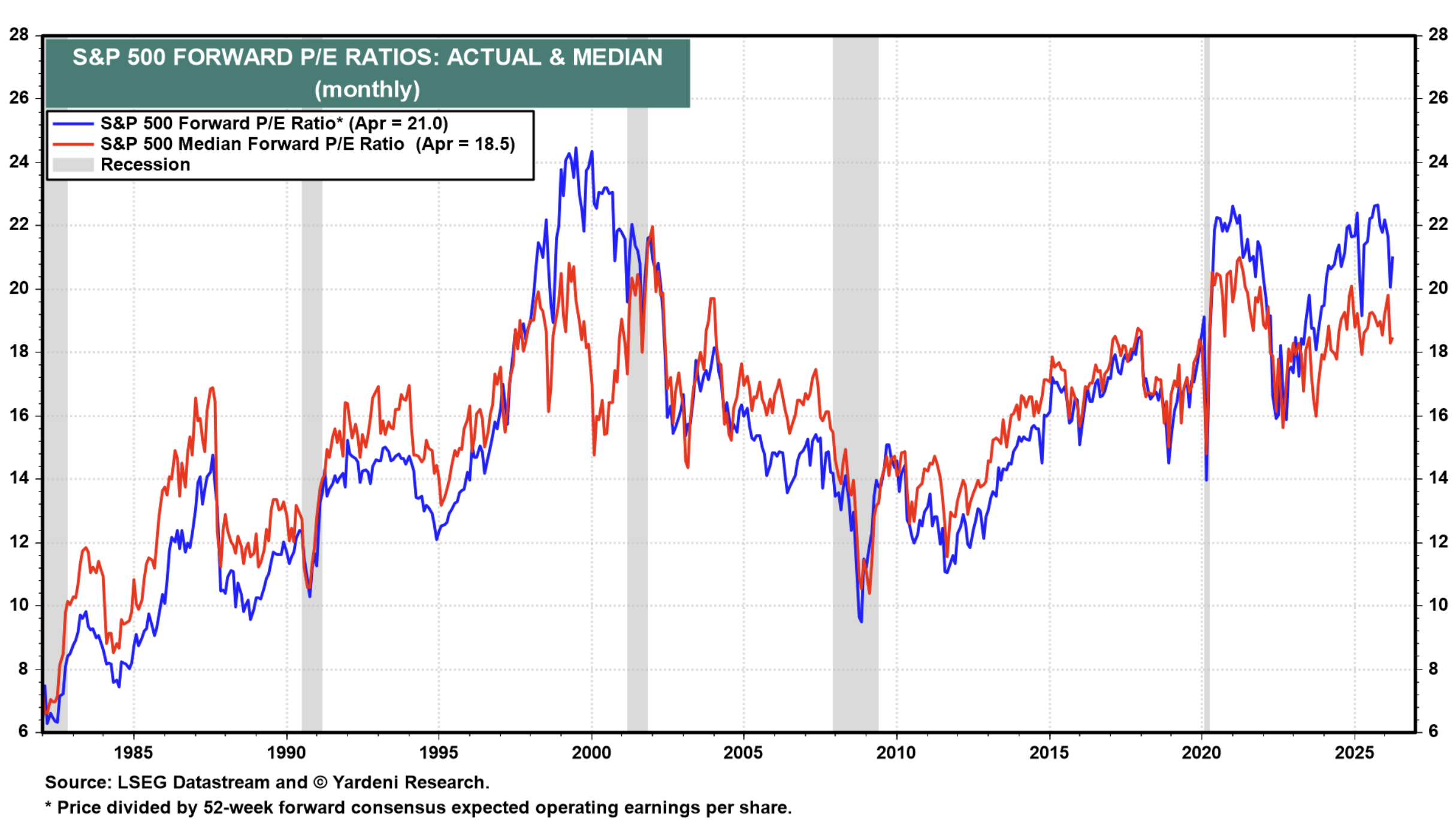

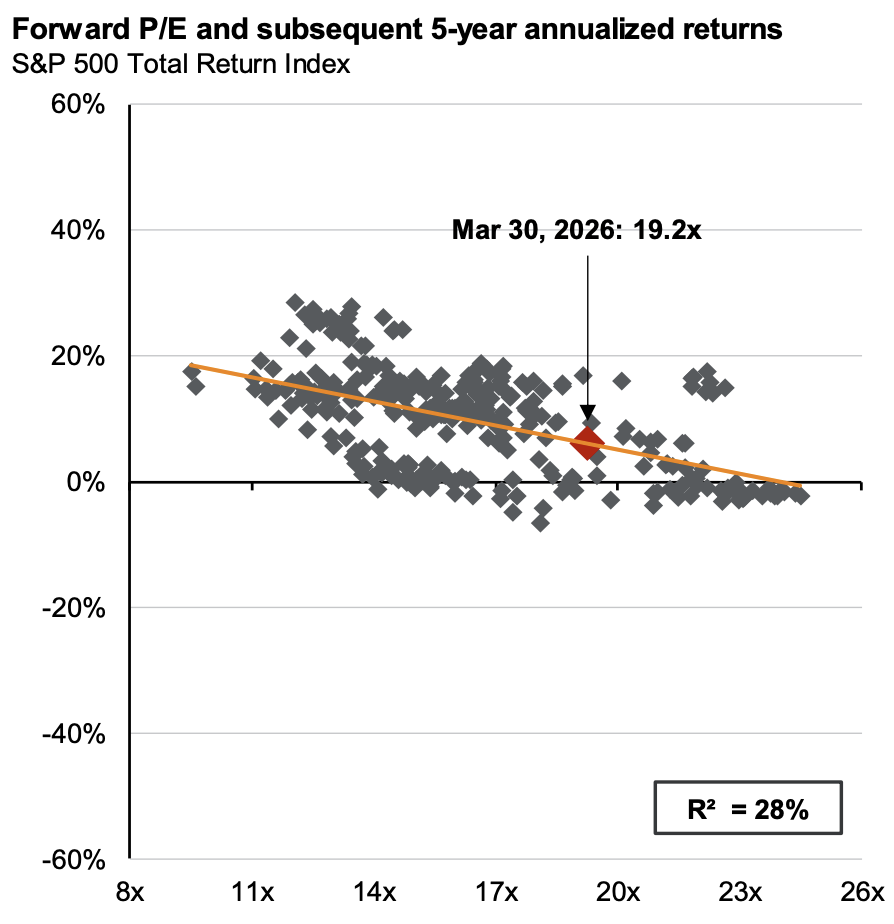

The S&P 500 right now is trading at a forward multiple of about 21x.

This is a multiple that compares to a historic average of about 17x

Whenever you have a higher starting multiple as you probably would expect future returns are estimated to be lower how much lower.

One stat from JP Morgan stated that if you do have a starting multiple of around 21-22x, historically, that has yielded a return of under 5%.

Some periods, you're looking at 0% and sometimes it's going to be a slightly negative, so there is a little bit of a range around that.

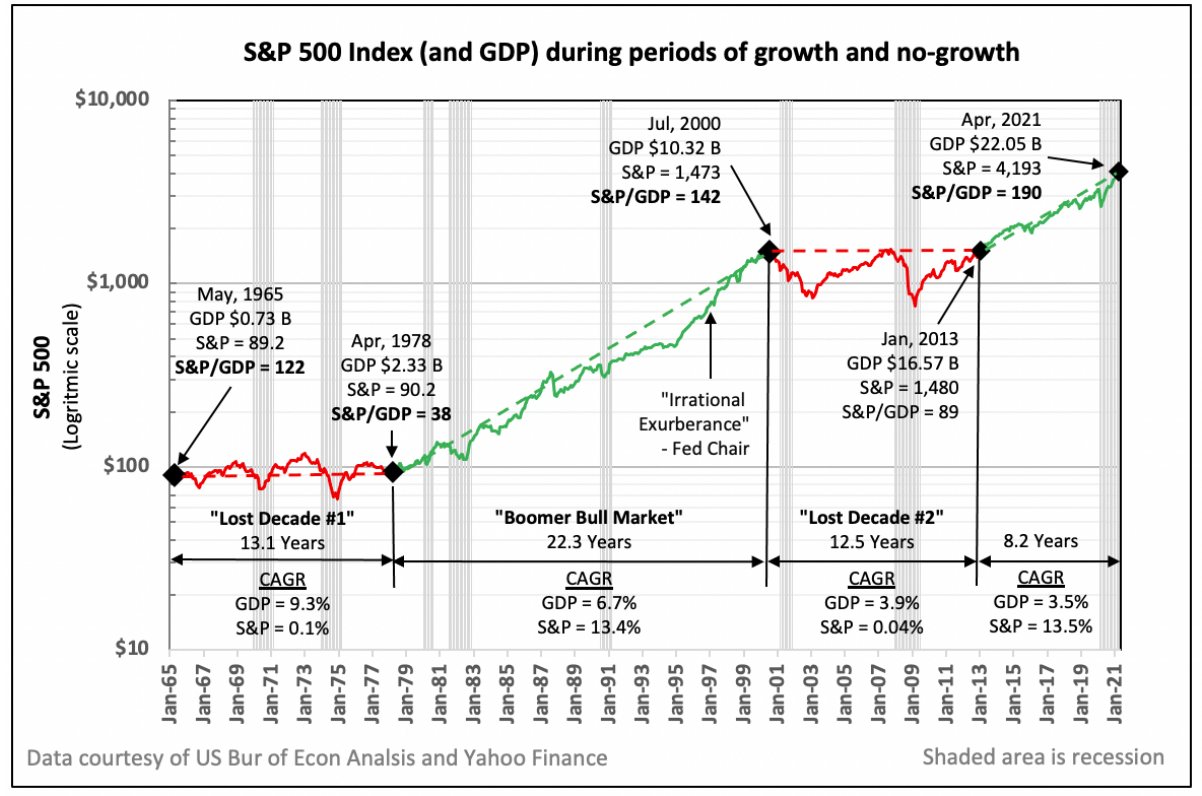

If you're thinking of what the real risk, in my opinion is of high valuation multiples and investing in the S&P 500 today, is potentially the risk of what's called a lost decade.

A lost decade is 10 year period where the stock market goes nowhere.

So it could go down a lot for that, and then ten years later, it's barely recovered.

The last time we had a lost decade really was if you invested at the peak of the tech bubble in January 2000, you would've very briefly been positive in 2006, and then you would've went negative again in the financial crisis and would not have been positive again until 2012.

So for almost a little over a decade stretch, you didn't make any money, which probably doesn't feel that good for most investors, even if you can say, "Well, for the next 13 years, if you held it thereafter, you did pretty well," which is true, and that's an argument to be invested for the long run for sure but if there's something else we could do to avoid a lost decade, minimize the impact of that, then that would be optimal.

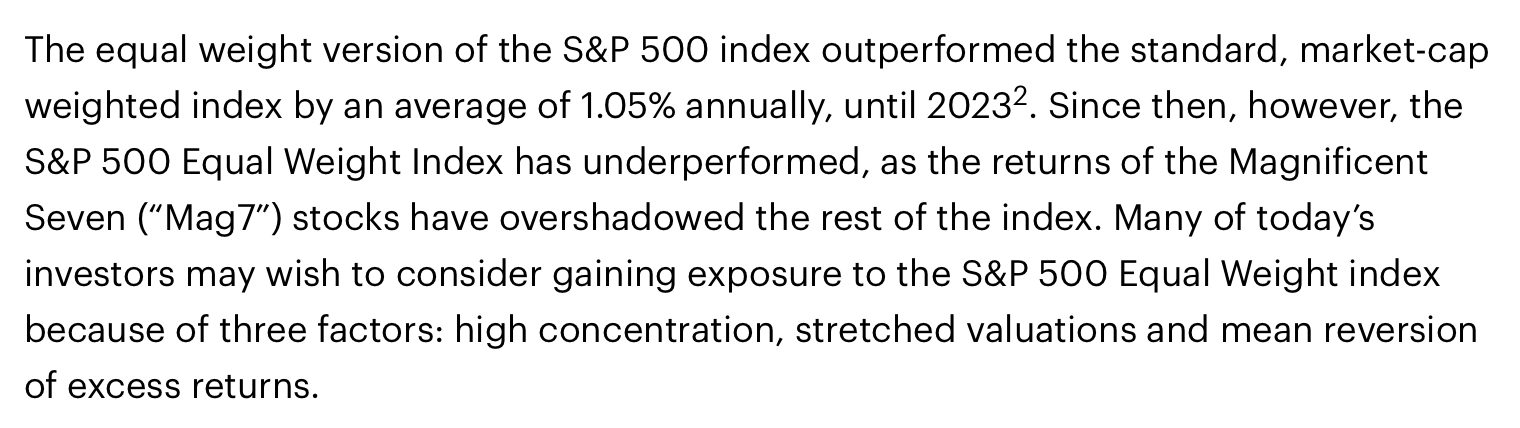

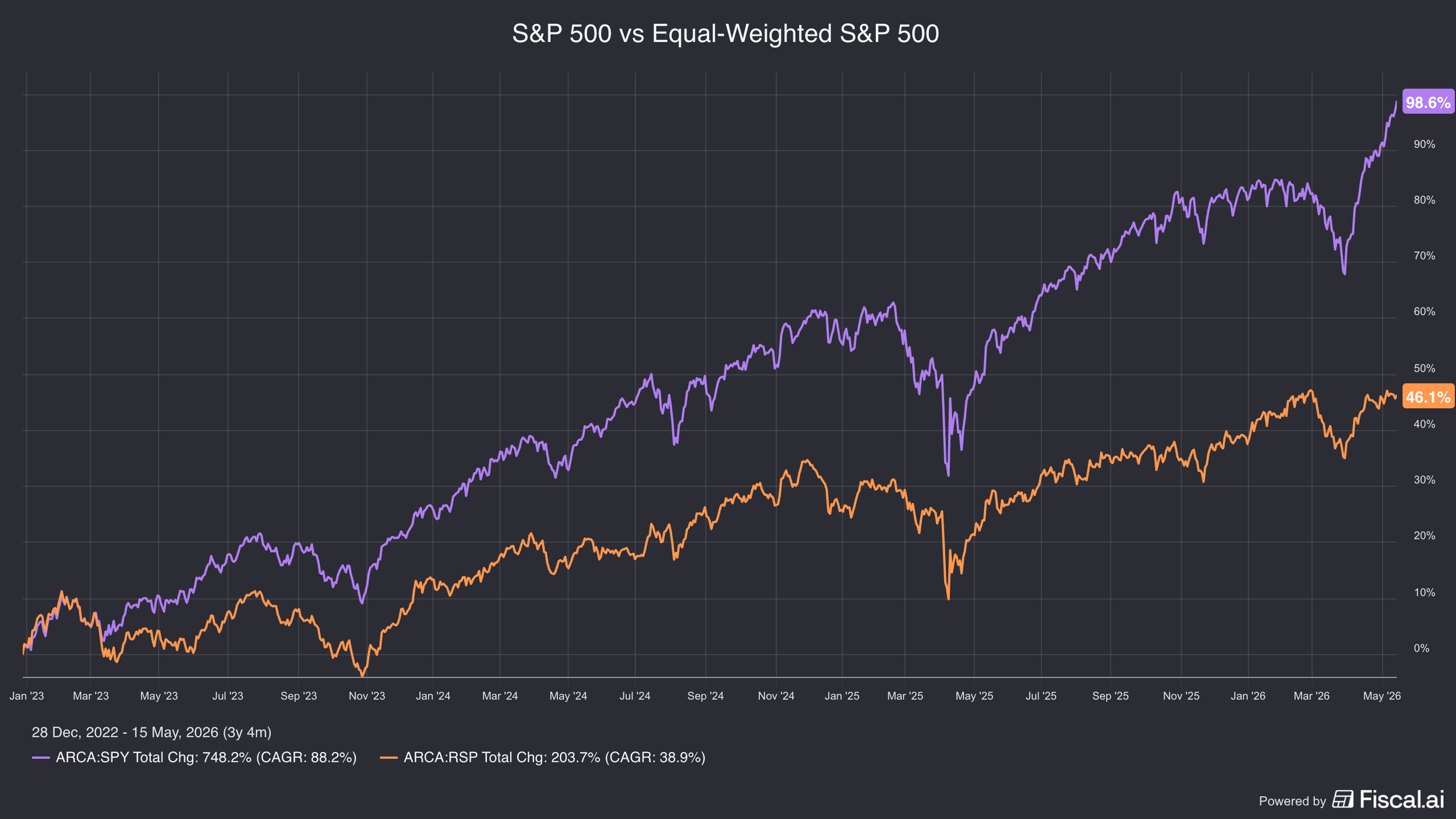

One way to mitigate this and this is an argument for an equal weight index, is if you look at the Invesco data, which is from April 1990 to December 2022, they show that the equal weighted index (RSP) outperformed the S&P 500 by 1.05%.

So a little over one percent annualized for a little over two decades.

What's the catch?

Well, since 2023, it has massively underperformed.

RSP has done about 50% total appreciation versus the S&P 500 having done double that at around a 100%.

That is one of the issues with the equal weighted cap index.

You can miss out on some of these rallies when there are a few really big companies that are making up a disproportionate amount of the overall stock market gains, which is what is happening right now with Magnificent Seven.

If you're invested in the equal weight and you're comparing your performance to the S&P 500, you're going to be massively underweight, Nvidia, Microsoft, Google, Meta, Tesla, all of these companies that have done pretty well over the past several years.

However, and this is now another argument for the equal weight, if you look at that original lost decade I mentioned earlier, let's say that you were invested in the S&P 500 in January 2000, and ten years later, you're looking at what your returns are, it would have been -9%.

If you invested in equal weight, it would have been around 60% (including dividends for both of those figures).

This shows how there's some environments where the equal weight does better and there's other environments where the S&P 500 does better.

I don't think there's any reason to necessarily be so adamant that one is better than the other because as we see, there's certain environments where one of them does better than the other and vice versa.

One of the benefits of the equal weight index today is that it's starting at a lower forward multiple of about 17x versus that the S&P 500’s 21x.

It’s important to note that just because the P/E multiple is high does not necessarily mean it's overvalued.

If you're comparing it to historical levels, yes, that's true, it's higher, but the other elements that aren't taken into account when you're looking at a P/E multiple is:

1) What is the risk-free rate? Because when you're looking at a higher risk-free rate, you would expect a lower multiple.

2) Earnings growth.

S&P 500 Top Holdings and Valuations.

These are the top holdings that make up the 40% weighting of the S&P 500 today

1. Nvidia: 8%

2. Google: 7%

3. Apple: 6.5%

4. Microsoft: 4.5%

5. Amazon: 4.2%

6. Broadcom: ~3%

7. Tesla: 2.4%

8. Meta: 2.4%

9. Berkshire Hathaway: 1.6%

Berkshire Hathaway, as you notice, is probably the only non-real tech company included in there and so when you are invested in the S&P 500, you do have a pretty heavy tilt on a lot of technology names.

In addition to that, these stocks all carry higher than average multiples.

1. Nvidia: 26x

2. Google: 31x

3. Apple: 32x

4. Microsoft: 24x

5. Amazon: 32x

6. Broadcom: 31x

7. Tesla: 180x

8. Meta: 19x

9. Berkshire Hathaway: 20x

With the exception of Meta and Berkshire, these companies are going to be higher than what the market multiple is today.

This is what is lifting up to a large extent, the multiples of the overall stock market.

Now, when I stated earlier that how concentration tends to correlate with higher valuations, can we see why?

All of these stocks carry higher valuations, and they all now have higher weights in the index.

The problem, in my opinion, in and of itself, is not the concentration, it's the high valuations.

However, if you're looking at these companies, you'll notice something else, they're growing faster than the average S&P 500 company.

If you look at what the average growth rates are for an S&P 500company, it's usually around 6-7%.

Right now, the forward earnings estimates for the S&P 500 are around 11-13%.

Could that potentially help rationalize a higher multiple?

Yes, with the caveat that the growth has to actually come.

It's pretty common for people to extrapolate out current growth rates, which are pretty high for a lot of these companies, into the future many years and just assume that's how it goes.

In reality, what ends up happening is when growth stops or slows, it happens very quickly.

Instead of getting 4 years of this above average growth, it turns out you only got half a year and it just ended.

Now that's not a prediction by any means.

That is just me pointing out a potential flaw with you counting on earnings growth saving you from a higher valuation.

It can happen and it also cannot happen.

I personally think when you are invested in an index, this is not really the analysis you should be doing.

I don't think you should be looking at the individual constituents of the index and decide, “Is this a good company? Is this a bad company?” because the whole point of the index is to be agnostic of those decisions and be humble in the fact that you can't always tell.

If you're invested in the S&P 500, I think you just let the do its thing, and you can cost average into that over time, and you also don't have to just invest in the market cap weighted, you could also invest in the equal weighted.

You don't also have to pick between the S&P 500 or the equal weighted. You're allowed to have exposure to both, which may help you mitigate against both risks that are concerning:

1) The risk of potentially missing out on the fact that a lot of these companies that are very big and growing very quickly, maybe deserve to have a little bit more of your money directed towards them.

2) The S&P 500 is at a higher multiple, and it does assume more growth, whereas the equal weighted index does not. And over time, if you are invested in something at a lower multiple and at a time it's less popular, that tends to also do better over time.

Now, personally, I think it's totally fine owning both but, and this is a big exception, you need to understand how much equity exposure you should have and what is appropriate for you.

Because a lost decade may be a bigger risk for some people than other people, depending on how much time horizon you have to actually invest.

Which is why it is very important to do proper financial planning before you're actually invested so you know how long you can actually invest your money for.

If you're invested in an index and know you got 20 years, these decisions matter much less than if you have 5 years.

And maybe you don't need to invest that much in equities at all if your time horizon is that short and you're going to need the cash and can't withstand a drawdown.

Defense of Single Stocks.

When you're invested in the index, you don't really know what the returns are going to be.

I've not found any great way you can actually estimate out what the returns are going to be across time other than to just say, "This is what the index has done historically."

You don't know that the future is going to be the same as the past, because it's very hard to try to estimate out what economic growth is going to be to the future.

Now, that's not me being pessimistic on American capitalism or the world growth or anything like that, it's just the truth that you can't really reliably estimate out these things the same way you can if you're looking at a single stock.

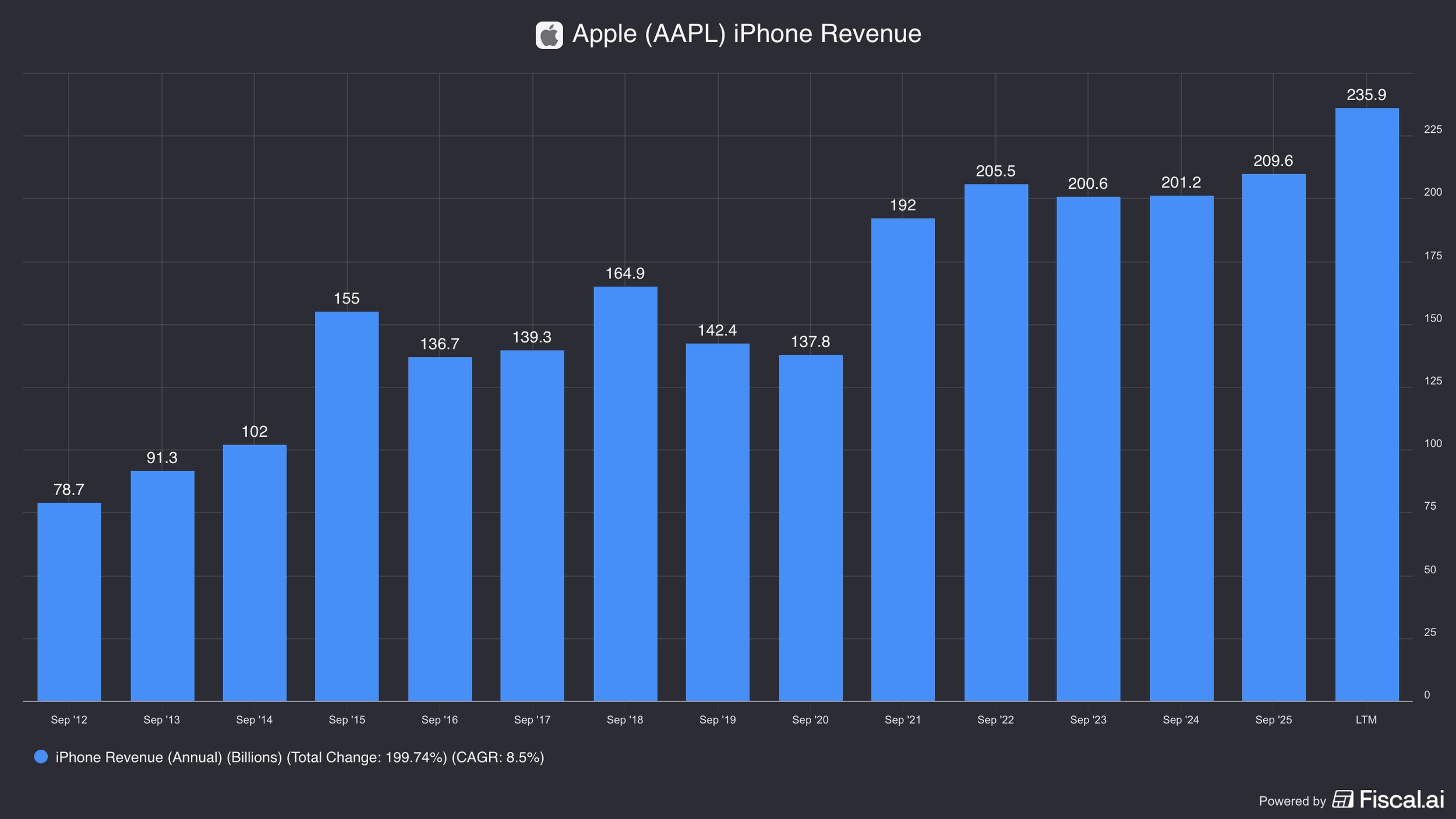

For example you could say, "Well, I'm pretty sure that Apple's going to sell the same amount of iPhones that they sold over the last five years, or if not the same amount, at least 80% as much."

Then you can do the math out as to what that means for cash flows, and then you can pay an appropriate multiple for that.

It's easier to get a sense of what the returns for the stock can be when you're doing that out.

As far as I've found, there's no great equivalent to do that for an index.

Indexes are still great because they do give you a lot more diversification, even in the S&P 500 with having that much concentration, it still gives a lot of investors exposure to companies like Nvidia, Tesla, Broadcom, that they probably wouldn't own otherwise.

What I recommend for you is you first figure out how much money you can truly invest for the long term.

If you can cost average into these, that makes it a lot easier because you can put a little bit of money into the S&P five hundred, a little bit into the equal weight index, and a little bit into your single stock selections too.

Big caveat on the single stock selections that it is very hard to pick stocks.

There’s a stat which says 70% of all stocks, once they hit a big drawdown, never recover.

So you need to be careful when you're picking stocks, and if you're not careful, totally fine to go ahead and just put more into the indexes.

And when you're doing that, you should not be that concerned with what is the best possible return I can get.

Instead, you want to, in my opinion, mitigate against all of these different downsides.

I think it's totally fine to spread your bets across multiple different areas to have some exposure to the market cap weighted, the equal cap weighted, and also single stock selections.

So, while headlines warn of 40% index concentration, just remember that the risk isn’t concentration itself, it is the high valuations associated with it that could potentially result in lower than expected returns or even a lost decade if the growth doesn’t come.

For more on index concentration, check out the video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.