Why This Isn’t an AI Bubble (Yet)

Get smarter on investing, business, and personal finance in 5 minutes.

This week’s newsletter is an adaptation from my recent YouTube video on the AI Bubble.

Are we in an AI bubble?

It's a question that comes up constantly right now, and yet I've never seen anyone actually sit down and break it all the way through: the arguments for, the arguments against, and what any of it means for you as an investor.

So that's exactly what we're going to do today.

This newsletter is broken into three parts.

First, we're going to walk through the five main arguments that strongly point to us being in an AI bubble.

Second, we're going to counter those arguments and talk about why this time could genuinely be different from the tech bubble of the 2000s.

And third, I'm going to share my own conclusion on where I think we actually are in this cycle, and more importantly, what you can do about it.

Let's get into it.

Part 1: Five Reasons We Might Be in a Bubble

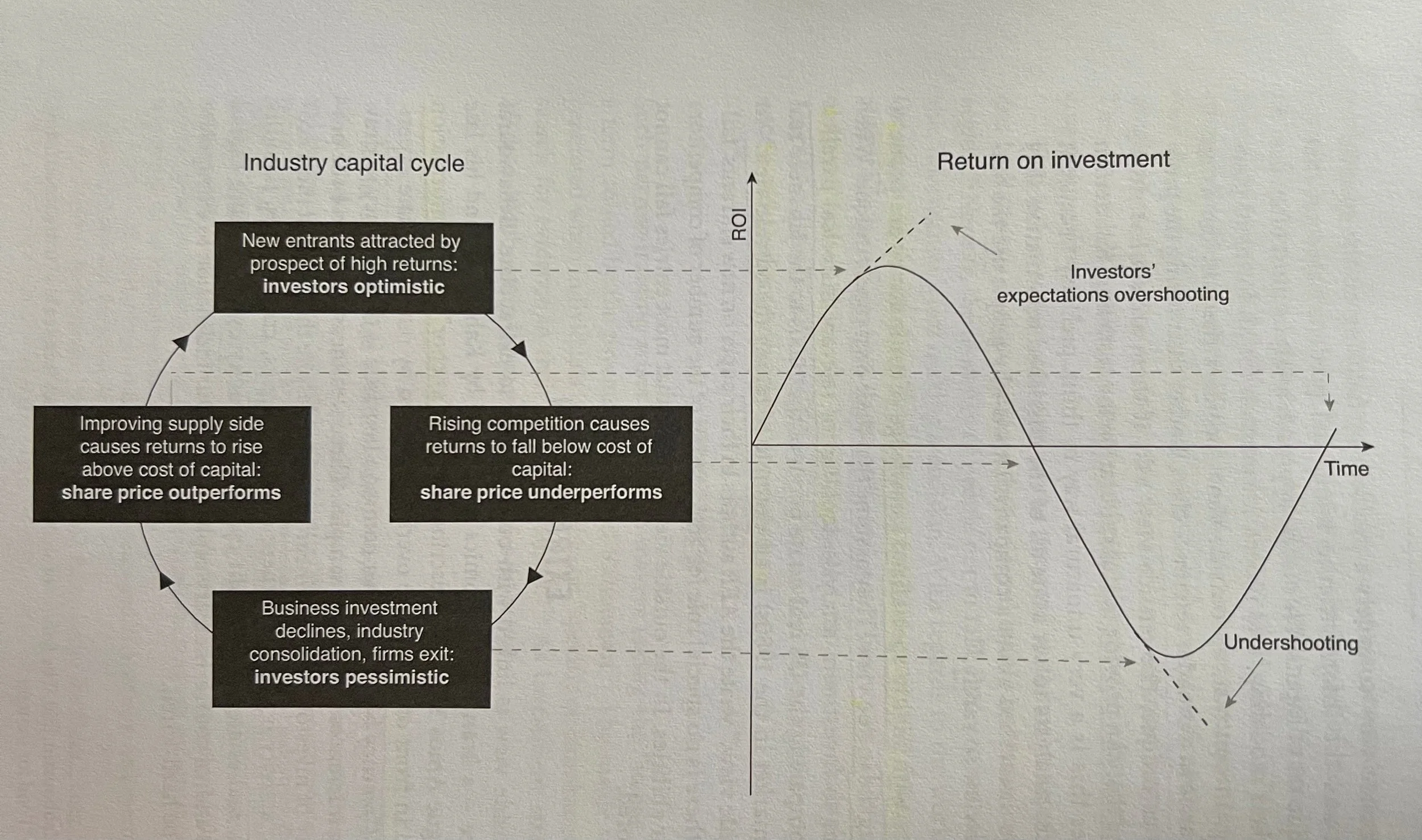

1. The Capital Cycle.

The first argument has to do with capital cycles, and it's a pattern that has played out many times throughout history across many different industries.

The way it works is fairly straightforward.

A new industry, like AI, emerges with genuinely exciting technology, and it draws a massive amount of capital toward it.

Everyone assumes there's going to be a very high return on invested capital, and so more and more money flows in.

As capital flows in, supply increases and capacity expands.

In the case of AI, that means more data centers, more chips being built, and more infrastructure to serve the growing demand.

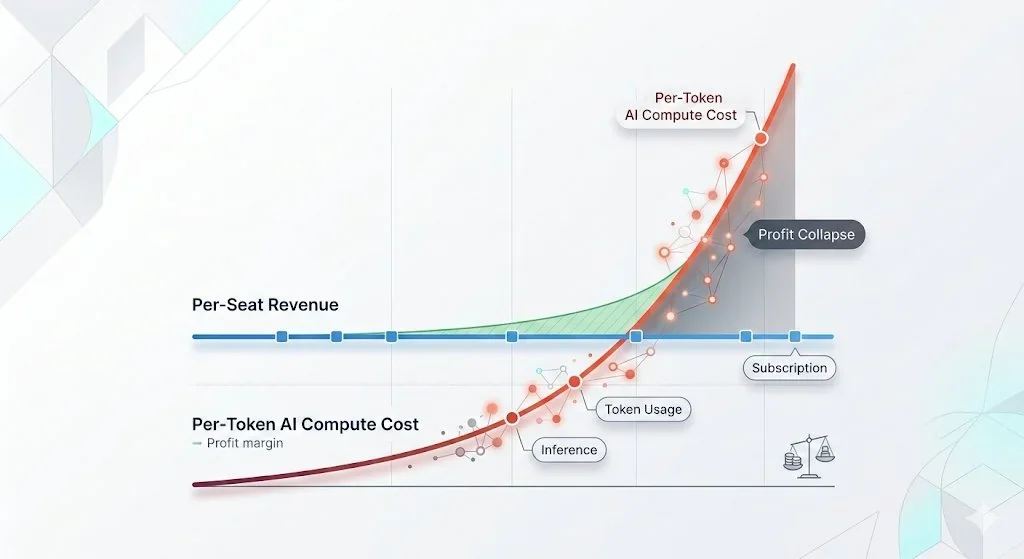

The problem, historically, is that supply eventually overshoots demand.

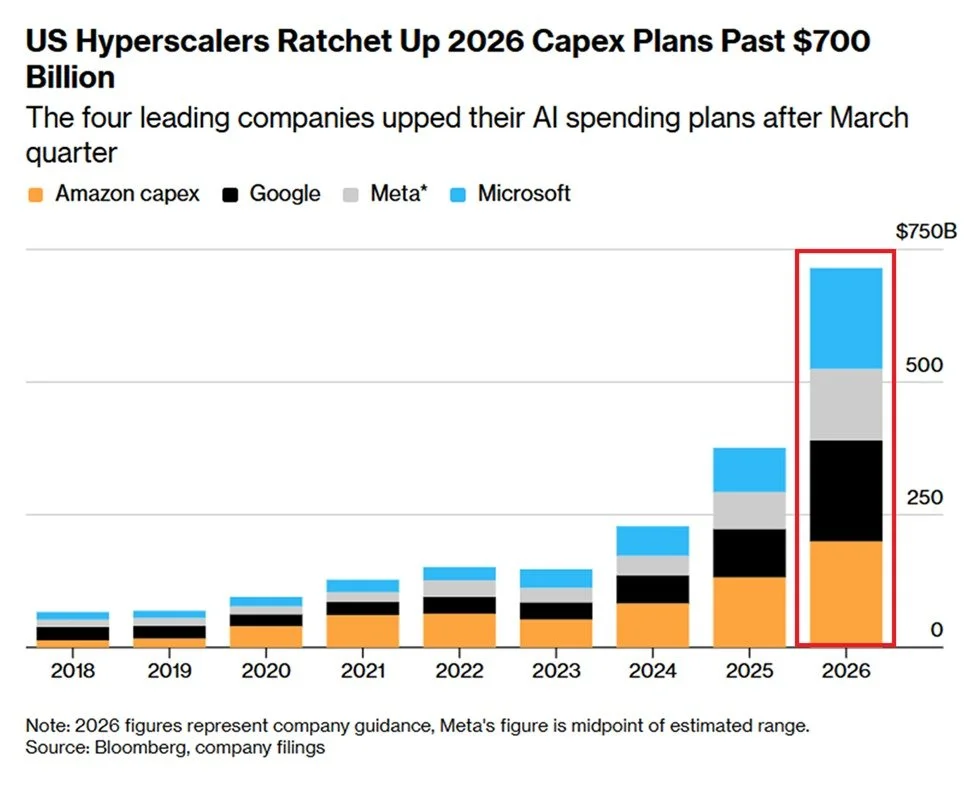

And notably, the big tech companies have almost acknowledged this themselves by publicly stating they'd rather risk overshooting demand than undershooting it.

So they continue to build out — aggressively.

Meta, Google, and Microsoft are each spending over $100bn in capex on data centers alone, and total AI spend right now is roughly double what was spent on the fiber build-out during the tech bubble as a percentage of GDP.

When too much capacity gets built and demand doesn't keep up, prices fall.

And when prices fall, your return on invested capital is lower than expected.

At that point, investors pull back, new money stops flowing in, and the capital cycle begins to unwind.

Now, some people will mention Jevons Paradox here, which is the idea that as prices fall, usage actually increases.

That's a fair point, and it could very much apply to AI.

But timing is everything.

Even if falling prices eventually drive more usage, there can still be a significant air pocket where all of that capacity is sitting there, underutilized, at prices no one expected.

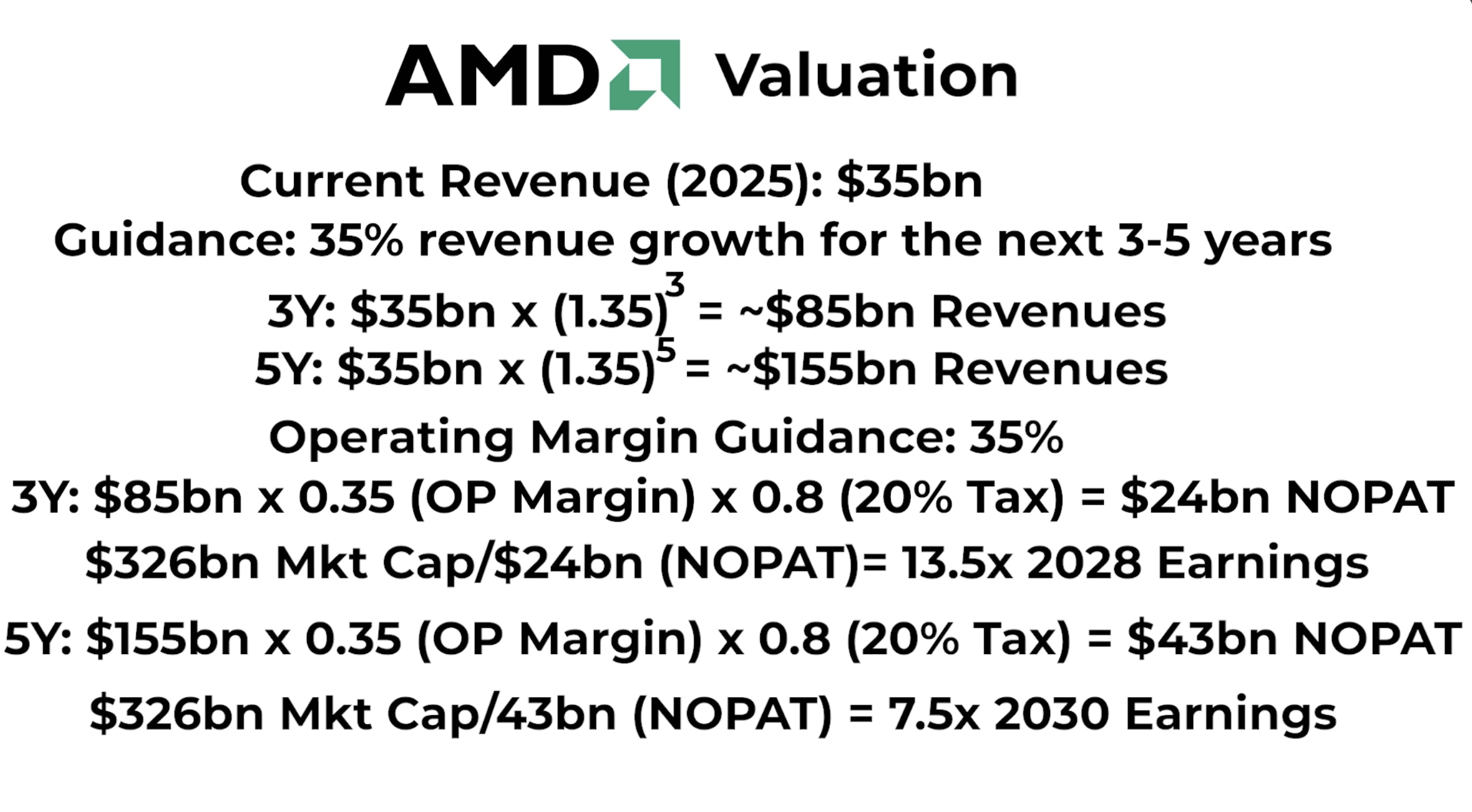

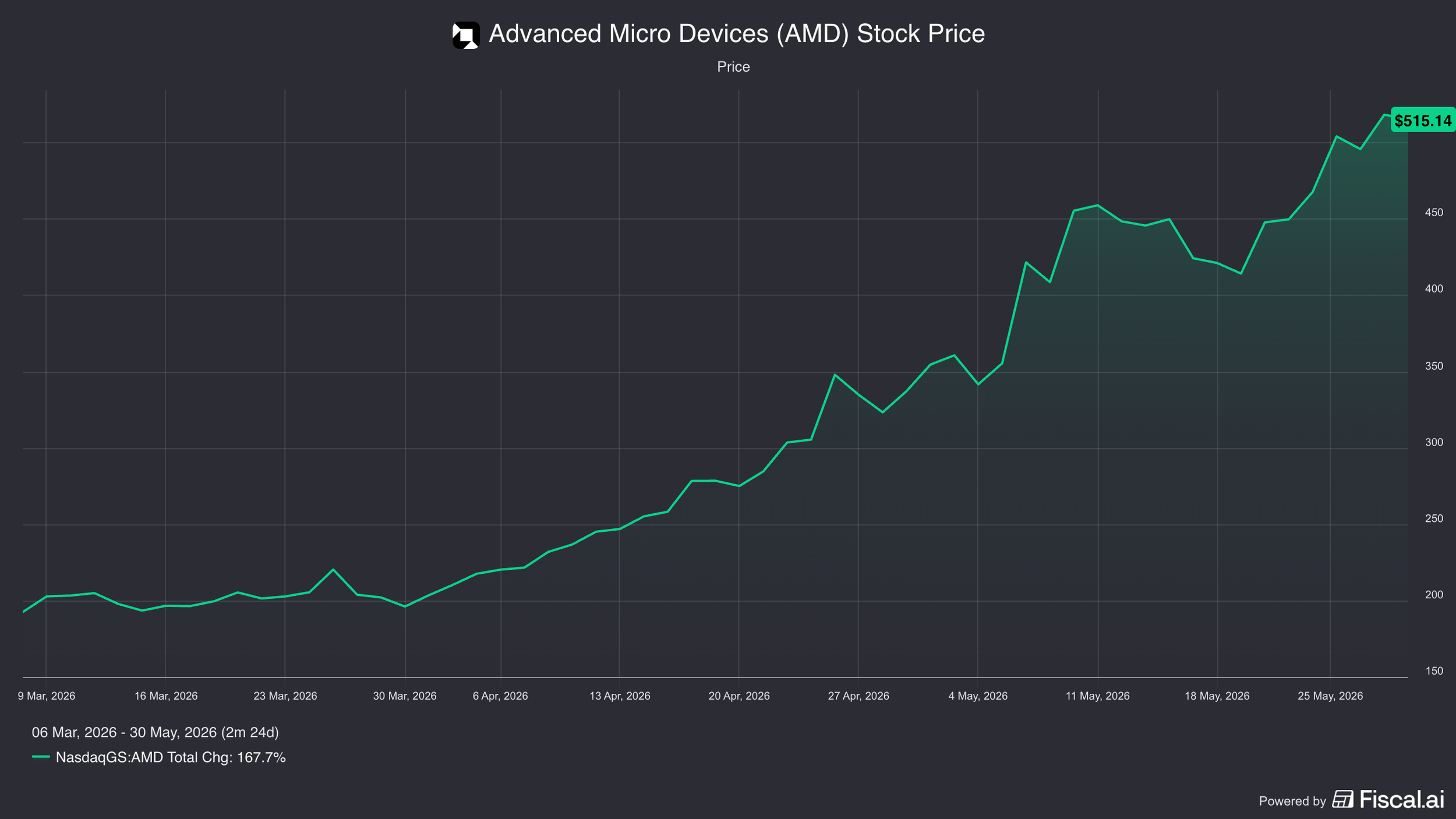

Take AMD as an example.

About three months ago when we did a video on AMD, AMD was trading at $200 a share.

In the valuation section, we assumed 35% annual revenue growth for five years and an operating margin of 35%, well above their current 11%, produced an EPS estimate of roughly $26 per share, putting AMD at 7.5 times 2030 earnings.

Whether that seemed cheap depended entirely on whether you thought AMD was cyclical.

Today, that same stock is at $520 a share, and that 2030 multiple has expanded from 7.5 times to 20 times in three months!

The only way that makes sense is if investors have collectively decided AMD is no longer cyclical, and that earnings will continue compounding well beyond 2030.

Because you simply cannot pay 20 times earnings for a company whose earnings might fall 40% shortly after.

The concern here isn't that AI isn't a great technology.

It's that even if AI fulfills every promise it's made, doing so a couple years later than expected could still be catastrophic for a lot of the businesses currently being priced as if the cycle will never turn.

2. History & Patterns.

The second argument is more of a historical one and it's a simple, uncomfortable observation.

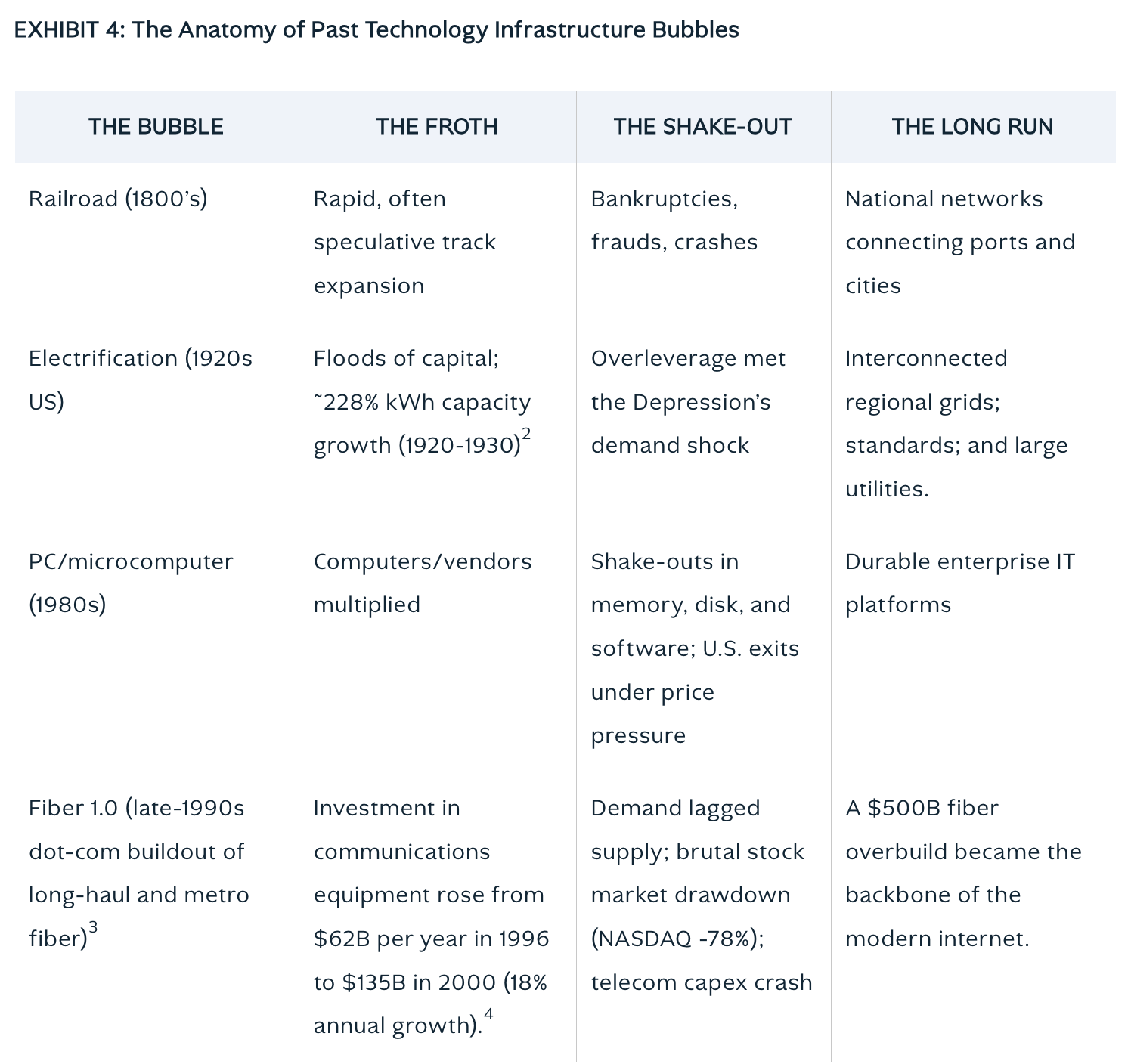

There has never been a major new technology that didn't ultimately result in a bubble.

Go back to canal building in the late 1700s, the railroad bubble in the 1840s, the electricity and radio boom in the early 1900s — bubble, bubble, bubble.

Same with automobiles, where many car companies went bankrupt.

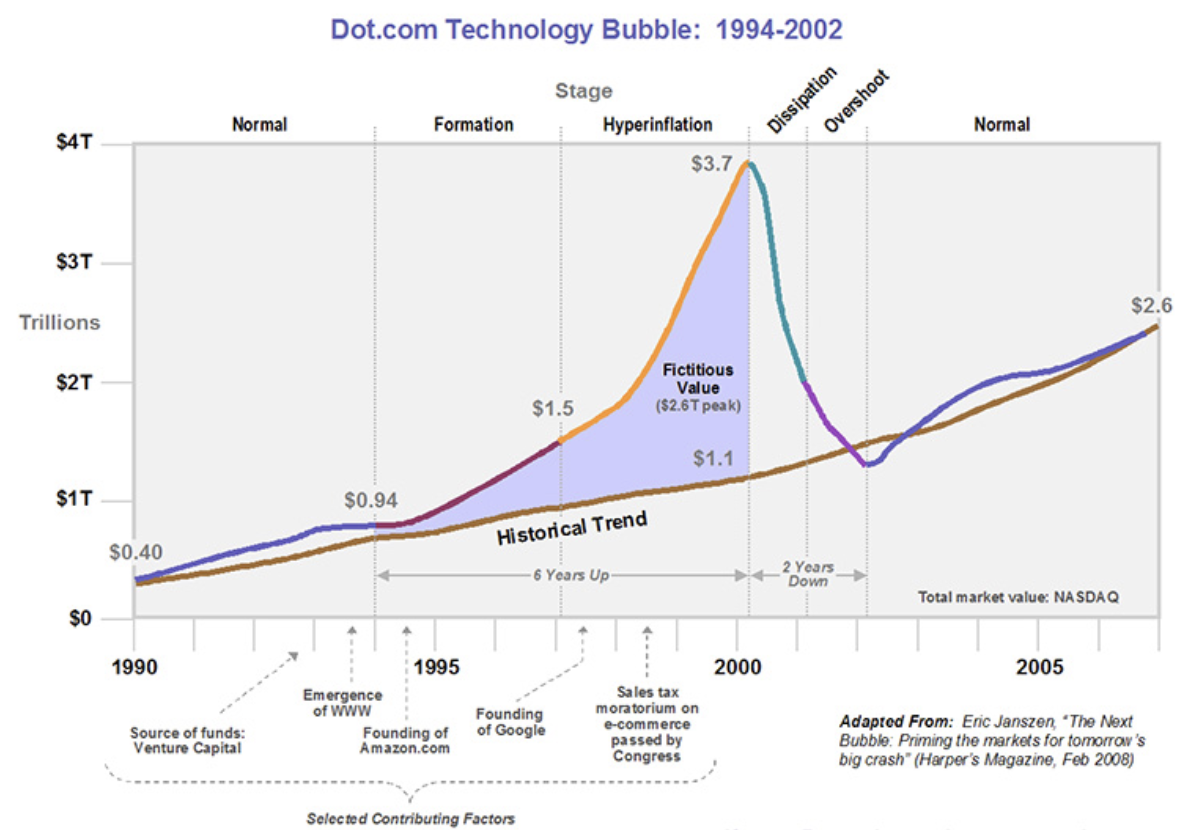

In the 1990s, the fiber optic and telecom build-out was followed closely by the dot-com bubble, where hundreds of internet companies went public, raised massive amounts of money, and almost all of them went out of business.

More recently, if you count crypto as a new technology, Bitcoin fell over 80% from its peak and many crypto businesses collapsed alongside it.

The pattern is consistent: when a new technology arrives, it grips the imagination of millions of people.

The sky becomes the limit.

And because the sky is the limit, it becomes very hard to determine what's actually a reasonable assumption as an investor.

It becomes easy to convince people this is worth far more in the future, because there's no clear historical comparison to anchor you.

What are you going to compare AI demand to?

Without a clear answer, anyone can slip in almost any argument they want.

Tell someone that companies spend trillions on labor and maybe a third of that eventually shifts to AI, it sounds compelling.

And so it goes, for almost every technology, people get overly excited, overly optimistic, and the outcome either doesn't deliver or doesn't deliver on the timelines promised.

AI, as of right now, fits that pattern quite neatly.

3. Investor and Company Behavior.

The third argument is about behavior, both on the investor side and the company side.

And frankly, some of what we're seeing right now is a little difficult to explain with a straight face.

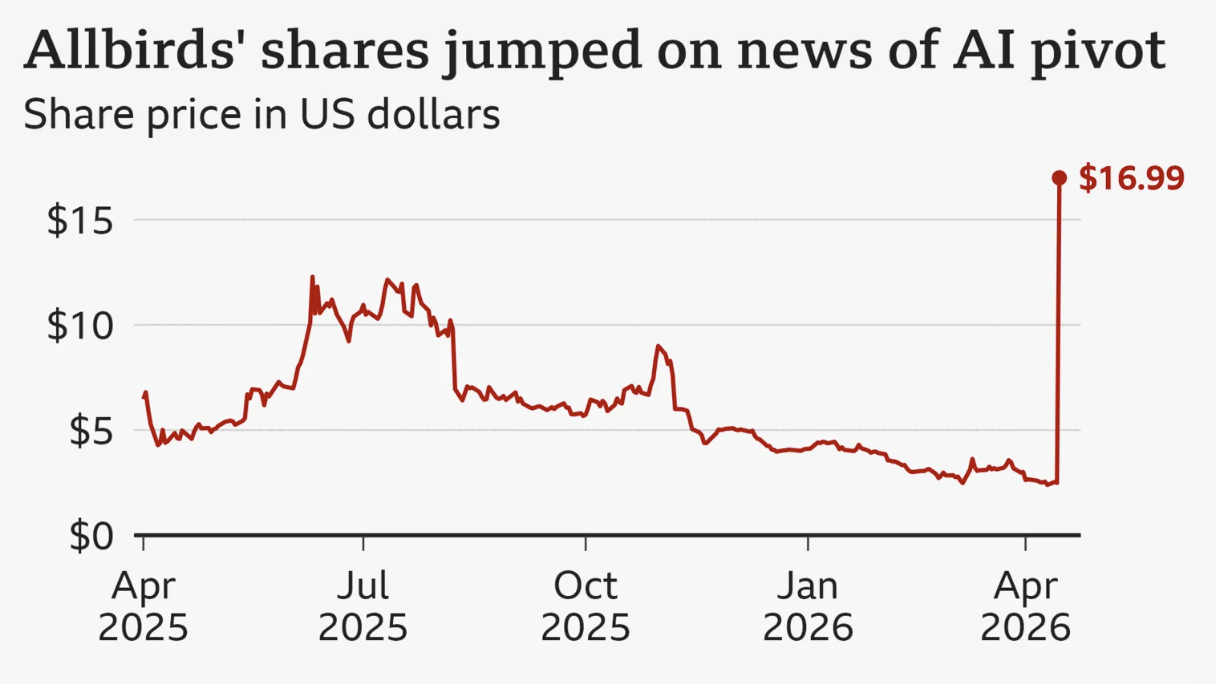

On the investor side, consider Allbirds, a shoe company, announcing it was pivoting to become an AI GPU provider.

The stock shot up 500%.

That's the kind of behavior that tends to show up near the top of markets, not the middle of healthy growth cycles.

Beyond that, we've seen AMD up 150% in three months.

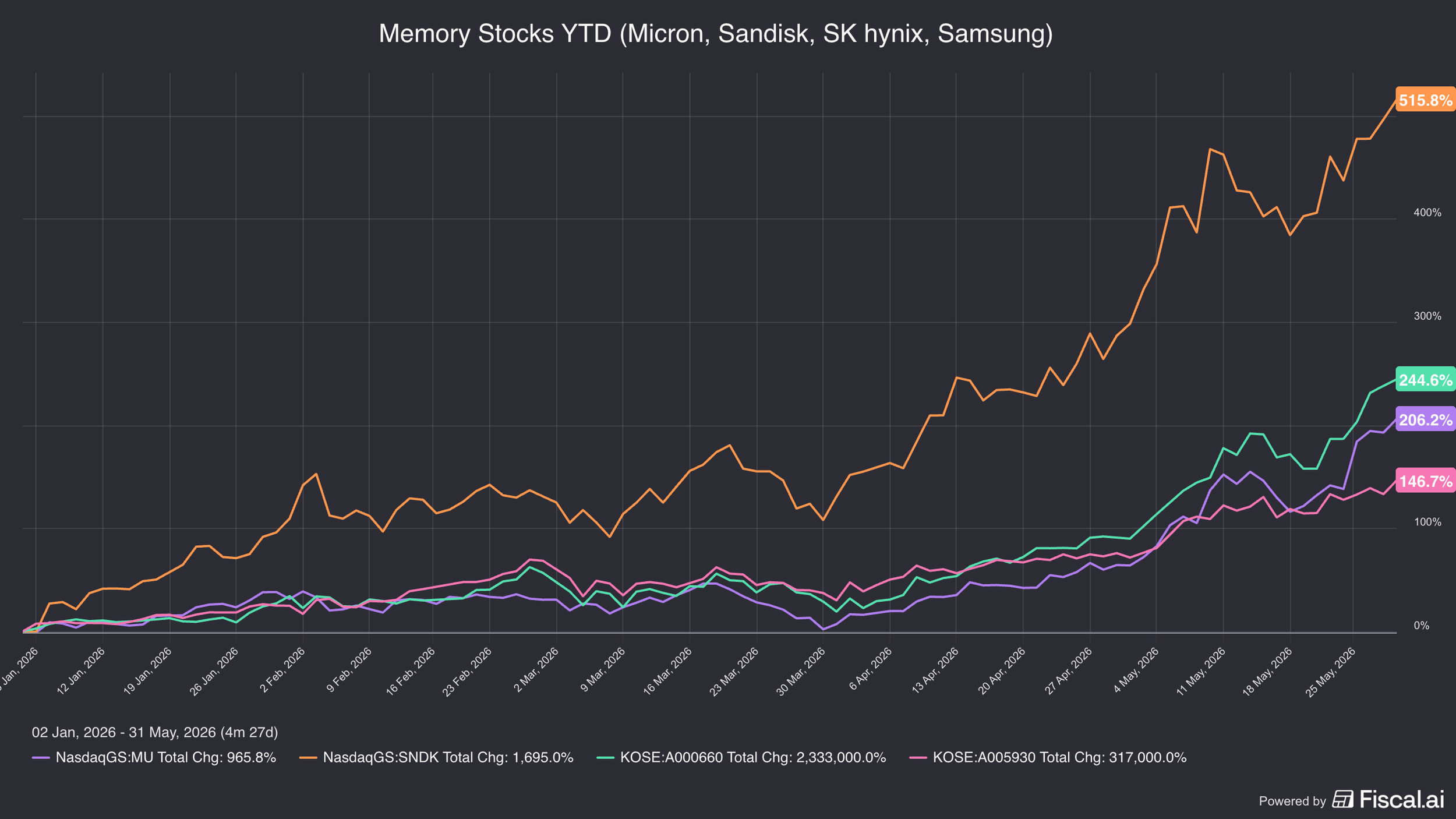

Micron up 200% YTD and 800% over the past 18 months.

SK Hynix up 200% YTD.

SanDisk up 500% YTD and over 4,100% in the past year.

Samsung up 400% in the past year.

Those are not normal stock market moves.

Now, to be fair, earnings at these companies have genuinely gone up.

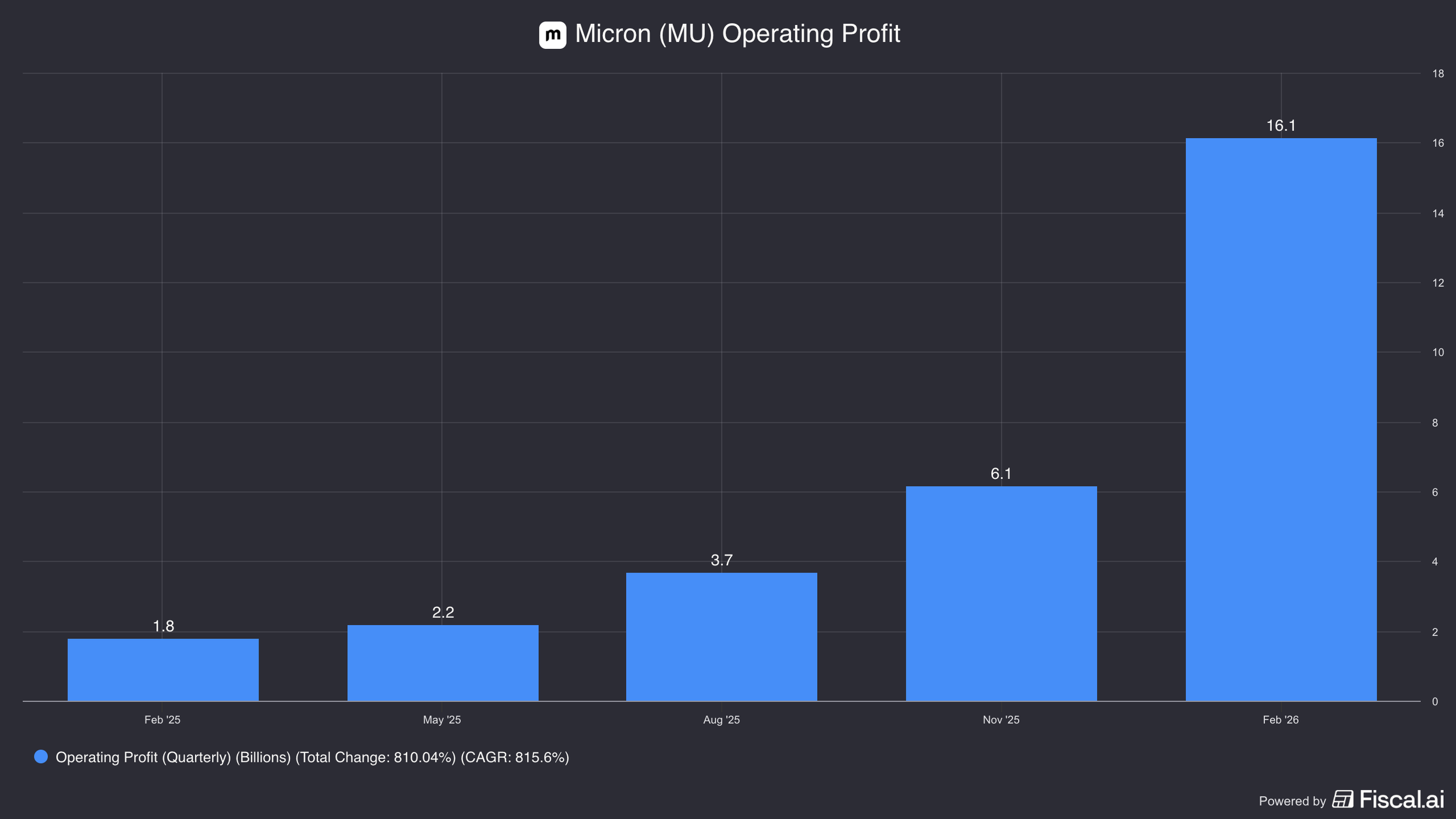

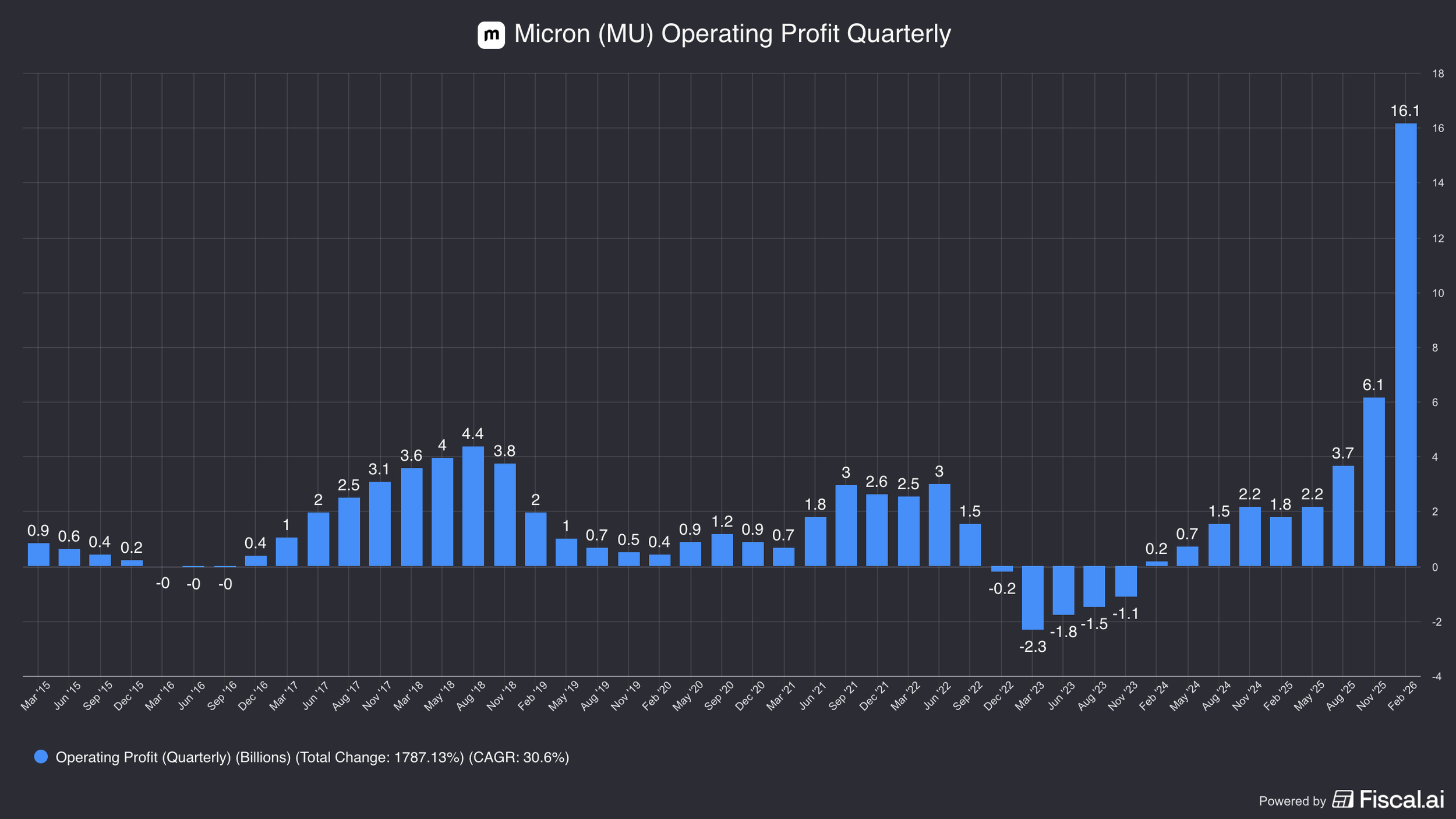

Micron, for instance, posted $16bn in earnings last quarter, compared to just $1.8bn in the same period a year ago.

Analysts are now expecting over $110bn in total earnings from Micron in 2027, which puts the stock at roughly 9.5 times forward earnings.

But here's the concern: the history of this industry is deeply cyclical.

In 2018, Micron had profits of $15bn, which was 88 times higher than just two years prior, when they had only $160mn in profits.

At that 2018 peak, investors put a 3x multiple on the stock because they knew it was cyclical.

Today, investors are paying 9.5 times forward earnings, implying either earnings aren't near the peak or the business won't be cyclical this time.

Historically, that assumption has burned investors.

On the company behavior side, the concerns are equally notable.

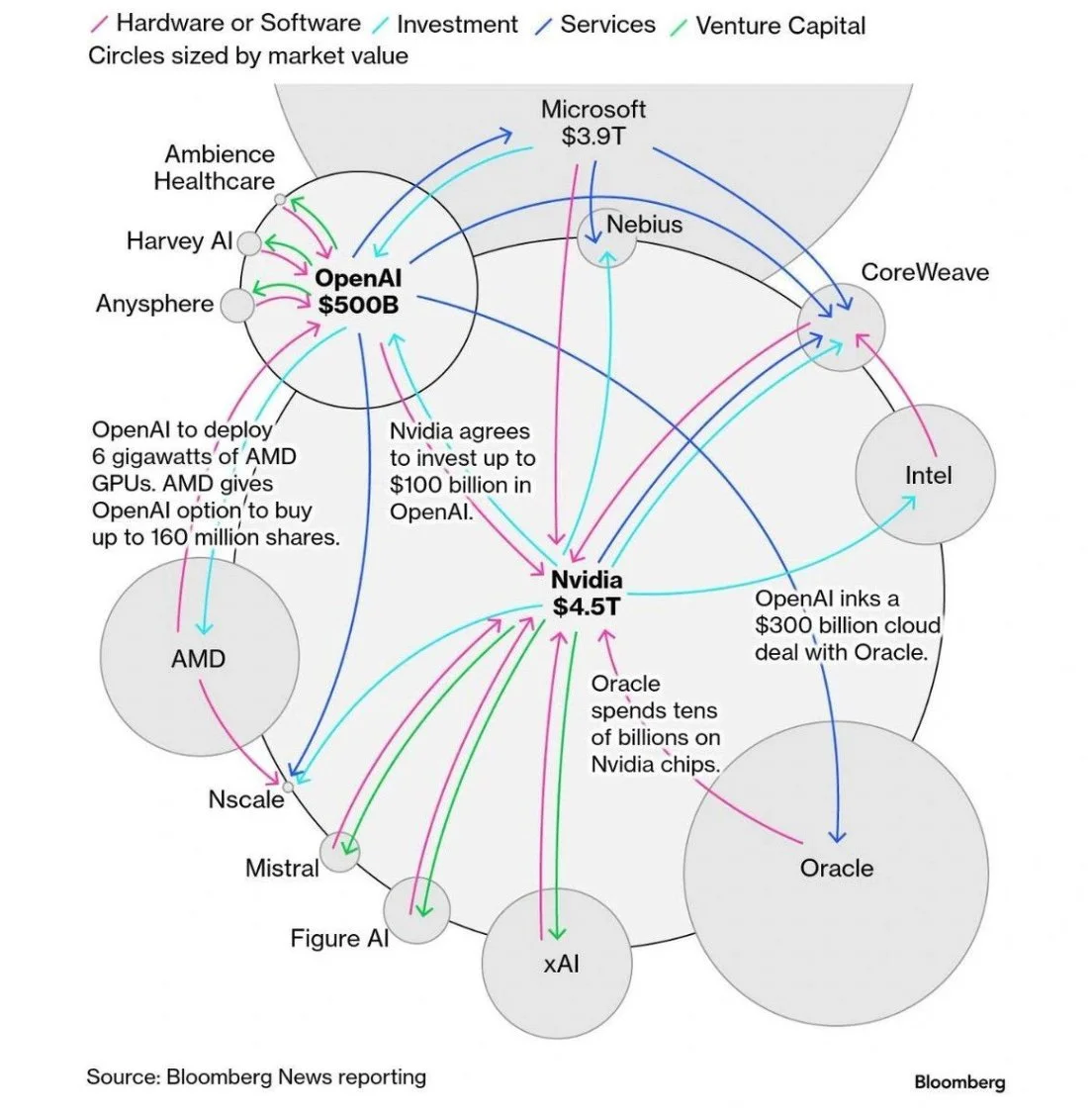

There's a pattern of circular financing happening right now that echoes what we saw in the tech bubble with vendor financing.

NVIDIA had up to $100bn in commitments with OpenAI.

OpenAI in turn signs commitments with companies like Oracle, who then has money to buy more NVIDIA chips.

The money is recycling through the same system, and it doesn't necessarily represent sustainable, organic demand.

Beyond that, there's clear groupthink happening.

Meta ups its Capex, then Google does, then Amazon does.

When large companies make major capital decisions in lockstep with each other, it signals they're more focused on capturing market share than on disciplined return analysis.

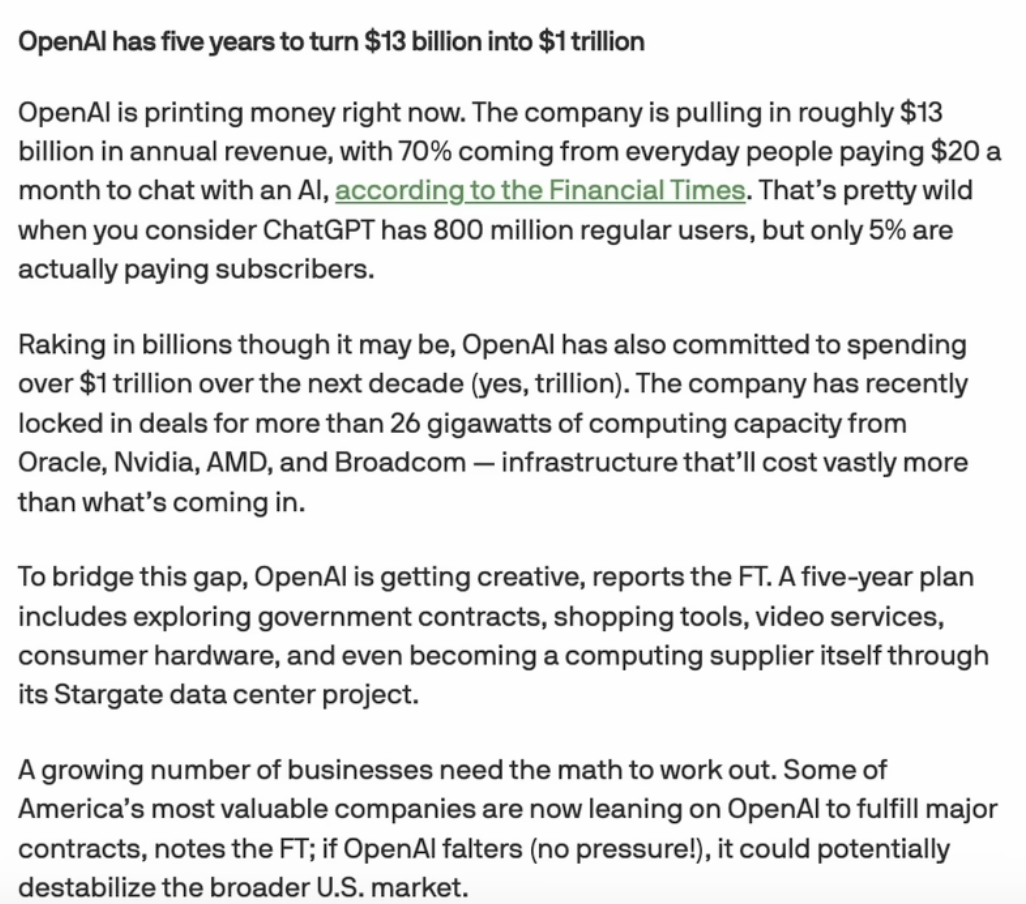

And then there's OpenAI's behavior specifically, which is perhaps the most alarming.

OpenAI currently has over $1 trillion in total commitments.

With Oracle alone, they have a $300bn commitment (roughly $60bn per year over five years).

OpenAI’s current revenue is $20-25bn in ARR.

That gap between commitments and revenue is enormous, and it needs to close very quickly.

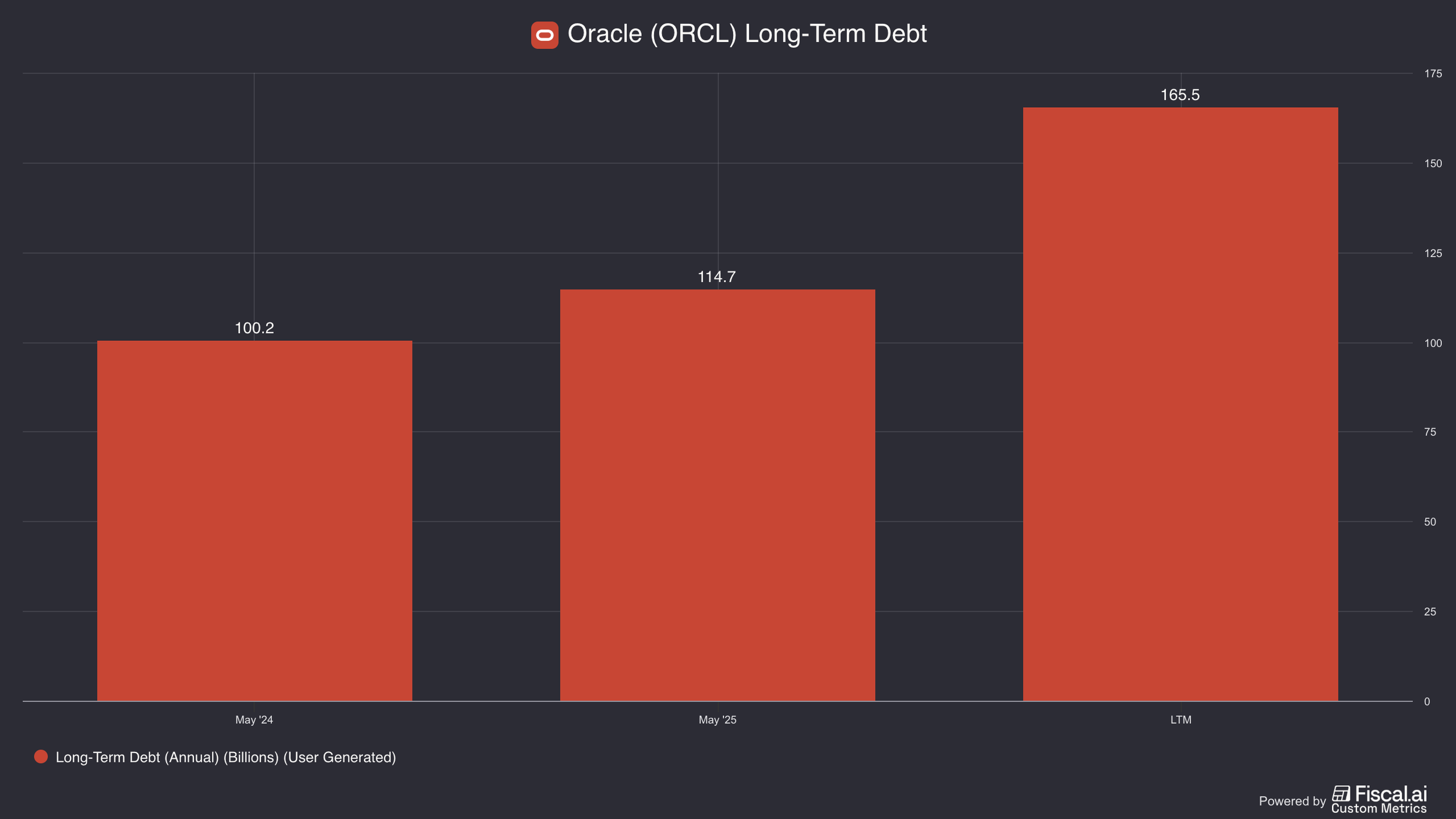

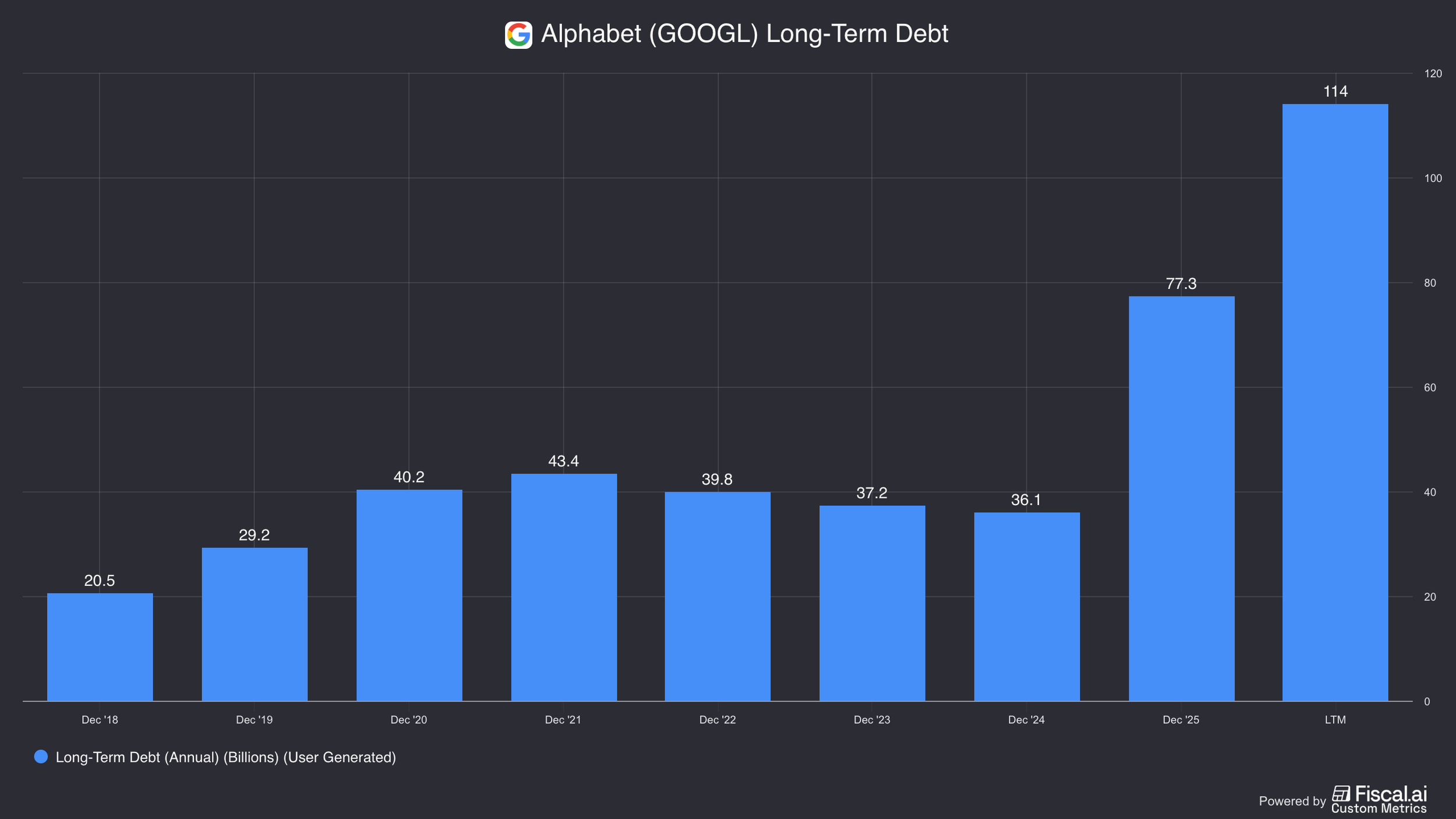

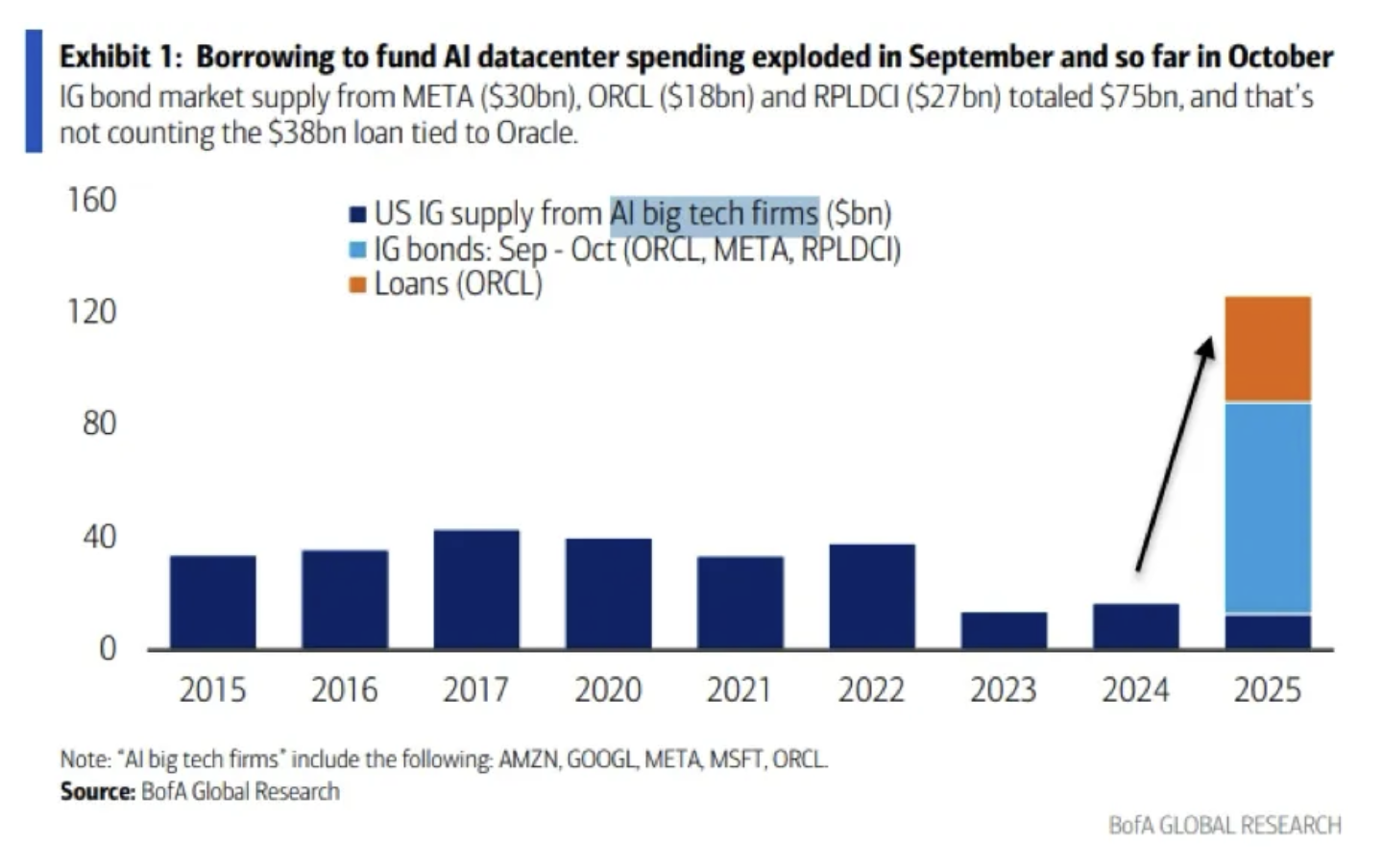

4. Debt Financing.

The fourth argument is about how this build-out is being financed.

Historically, when companies start taking on significant debt to fund expansion in a hot sector, that's a warning sign.

Oracle recently added another $20-30 billion to its debt load and now carries over $150bn in total debt.

Even Google increased its debt load by $50bn.

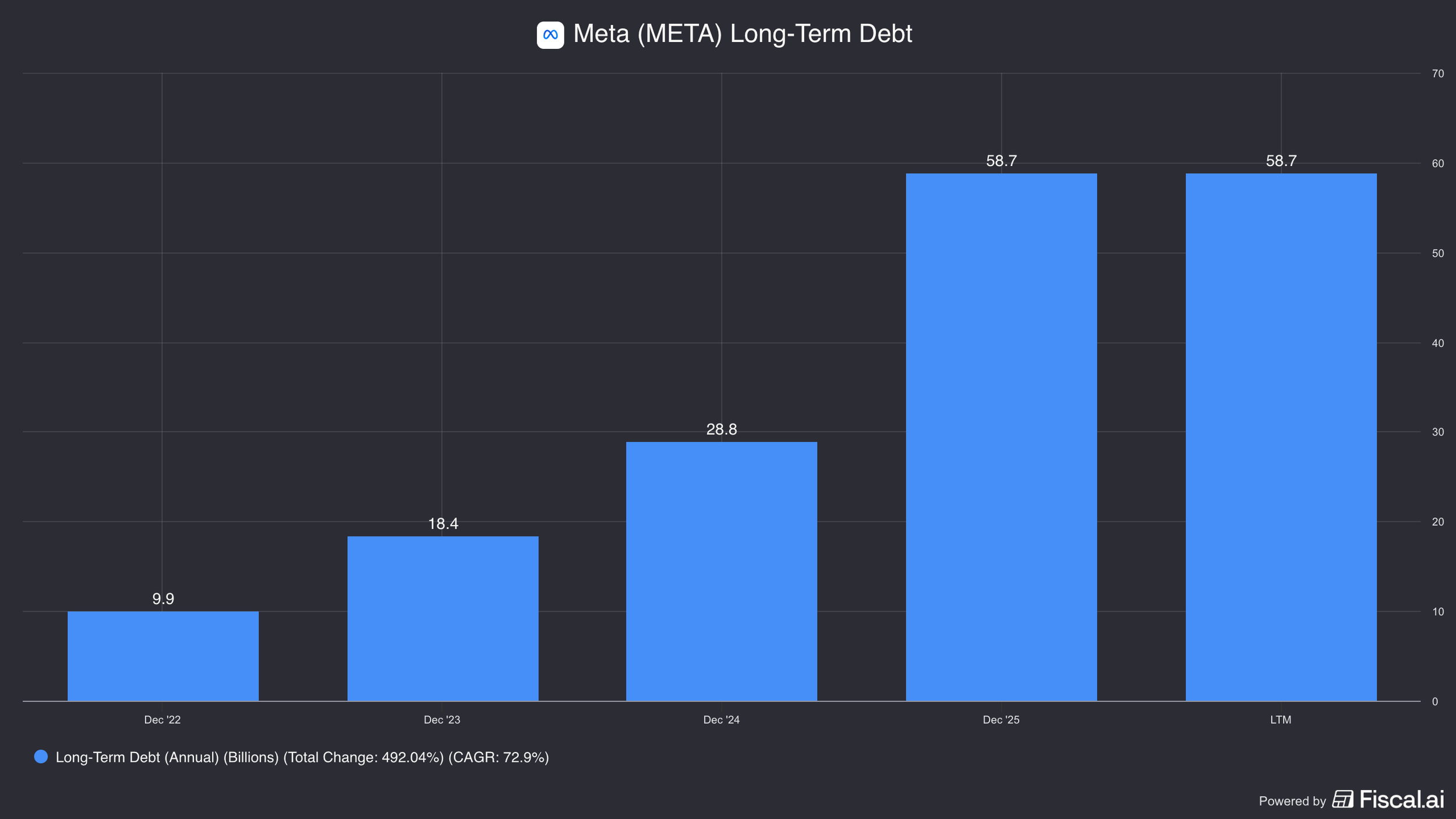

Meta also added $30bn.

Now, these businesses are extremely cash-generative businesses, so the amounts are manageable.

But the fact that even these companies are going to the debt markets to fund incremental expansion is worth noting.

The reason debt matters is that it changes the cost of being wrong.

If you invest operating cash flows into a project that doesn't pan out, you write it down and move on.

If you fund that same project with debt, you're still paying interest, still paying down principal, and your ability to reinvest in the next cycle is meaningfully constrained.

A debt-funded bubble unwinds much more slowly and painfully than one funded with cash.

5. Adoption Isn't Actually There Yet.

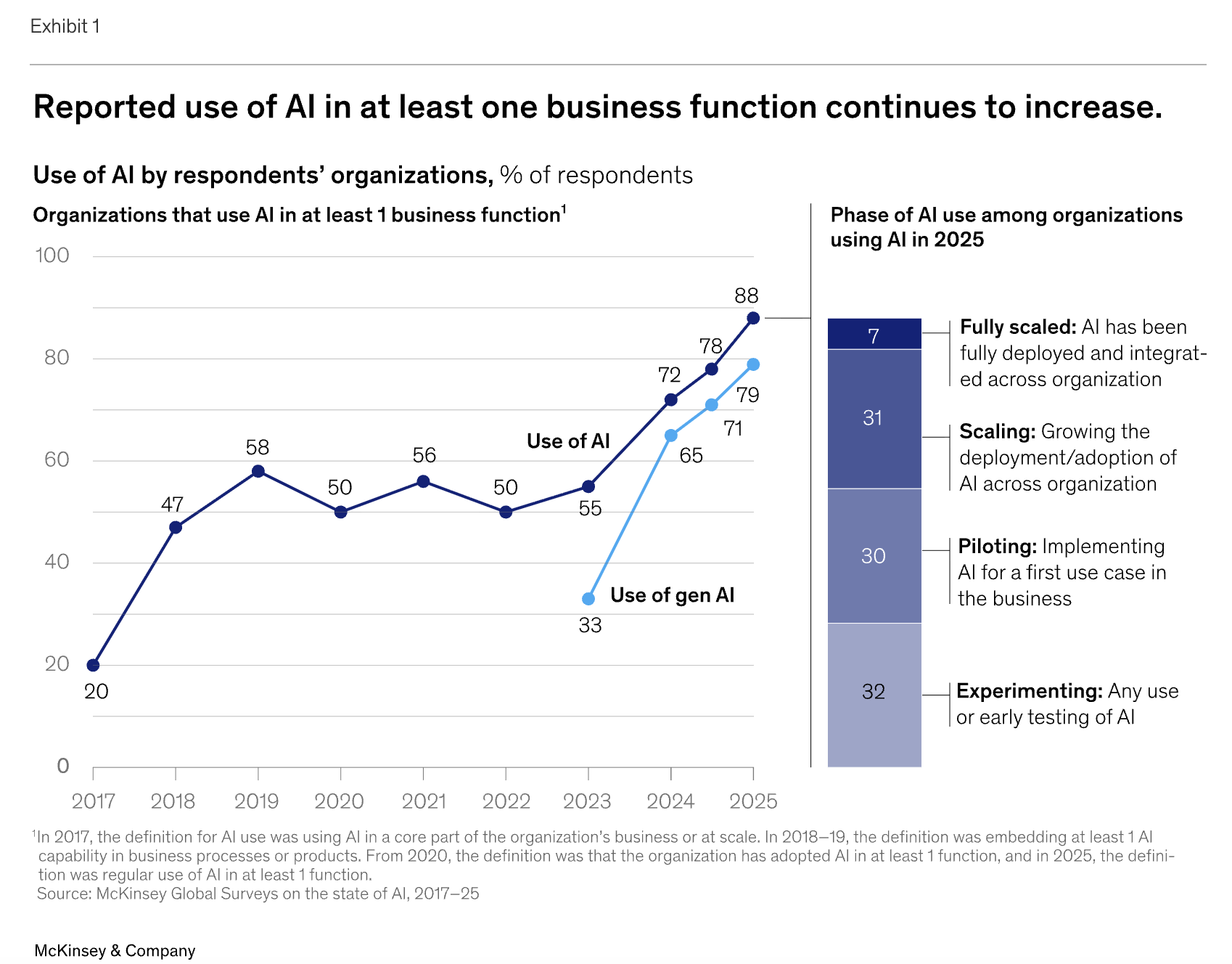

The fifth argument is arguably the most important, and it has to do with how many companies are actually using AI today in a meaningful, profitable way.

Despite the fact that AI gets mentioned constantly — especially on earnings calls — the evidence that it's actually being integrated into business processes at scale is considerably weaker than the headlines suggest.

A McKinsey study from late 2025 found that two-thirds of enterprises were still in pilot phases of AI, meaning they haven't committed to using it in their actual work processes.

Only a third had scaled their projects.

Other research paints an even starker picture.

ISG, a technology research and advisory firm, found that only 31% of AI case studies actually reach production, and only 7% of prioritized use cases reach the productivity goals they set out to achieve.

Gartner says 85% of all AI projects fail.

And perhaps most striking of all, a 2025 MIT study found that 95% of all AI projects failed to show any measurable improvement on the P&L.

Another MIT professor, Daron Acemoglu, found that only about 20% of work can theoretically be replaced by AI, but only 5% of overall work can be replaced by AI profitably.

And then there's what's actually happening in the real world.

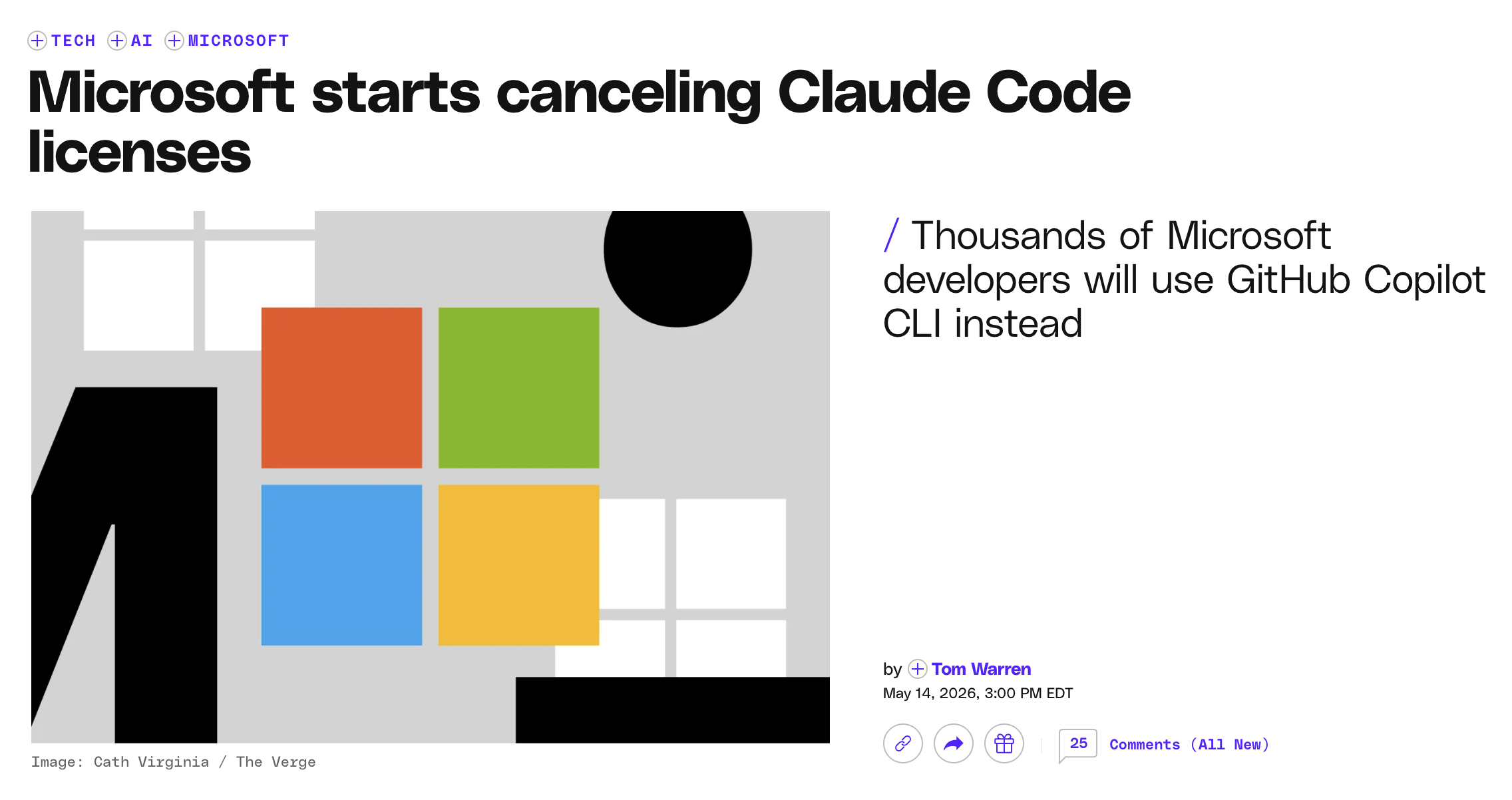

Microsoft recently canceled their Claude subscription for all of their engineers because they hit their maximum AI spend for the year in just a couple of months.

Rather than adding budget, they redirected their engineers to internal tools like GitHub instead.

Uber's CTO said something nearly identical — they maxed out their AI budget for the year within a couple months of the year starting.

The implication is clear: AI is considerably more expensive than companies expected, and they're not seeing returns that justify the cost.

If Microsoft had seen a real, tangible return on that spend after two months, they would have kept paying.

They didn't.

And that's a real problem, not necessarily a permanent one, but a real one right now.

The question is never whether AI will eventually be transformative.

It almost certainly will be.

The question is timing.

If the meaningful ROI shows up in 2032 instead of 2028, that's still a bubble, not because the technology failed, but because the market priced in a timeline that didn't materialize.

Part 2: Why This Time Could Be Different.

Having laid out those five arguments, it's worth being honest about the other side of this.

Because there are genuine reasons to believe the AI build-out is not simply a repeat of the dot-com collapse.

1. Revenue Is Real.

The first and perhaps most important counterpoint is that the revenue is real.

During the dot-com bubble, many of the companies that raised hundreds of millions of dollars were essentially pre-revenue.

Their business models didn't make sense, and almost none of them turned a profit.

AI today is different.

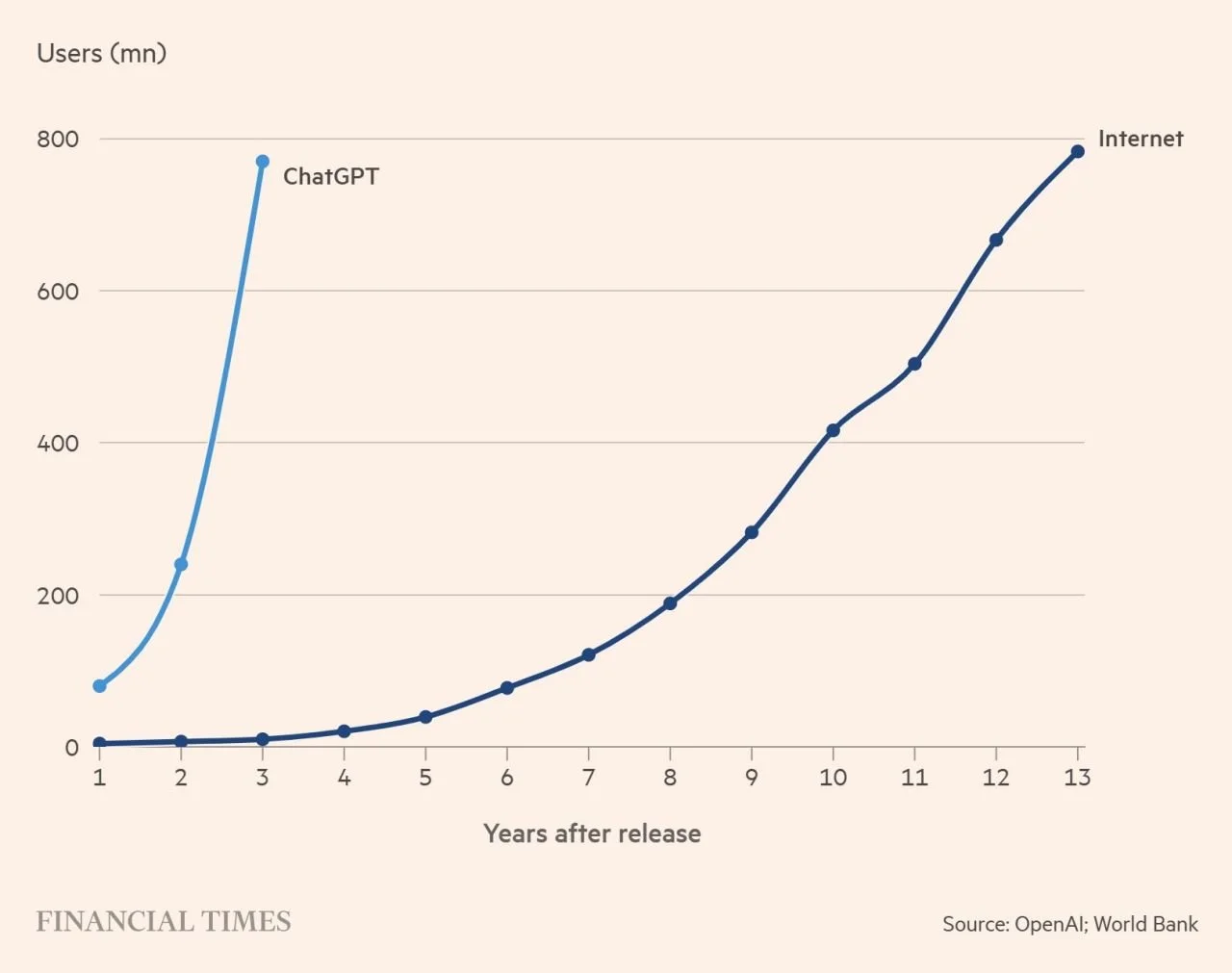

ChatGPT alone has 900 million users.

Compare that to the internet in the early 2000s, which had approximately 360 million users globally.

Google has infused AI into all of its products and has roughly 2 billion AI users.

This isn't speculative future demand and people are paying for this today.

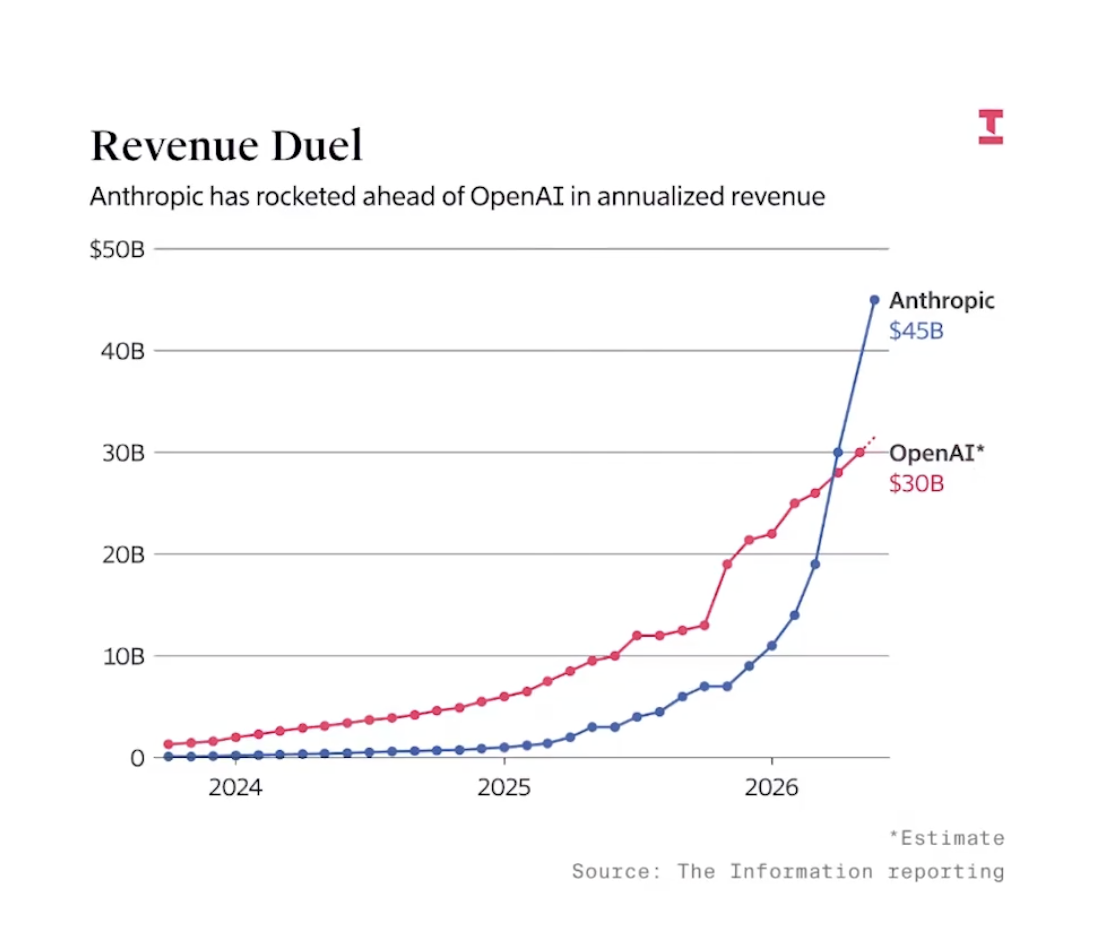

Anthropic, for instance, is estimated to be running at over $30-45bn in annual recurring revenue, up from approximately $80 million just two years ago.

That is the fastest revenue ramp in business history.

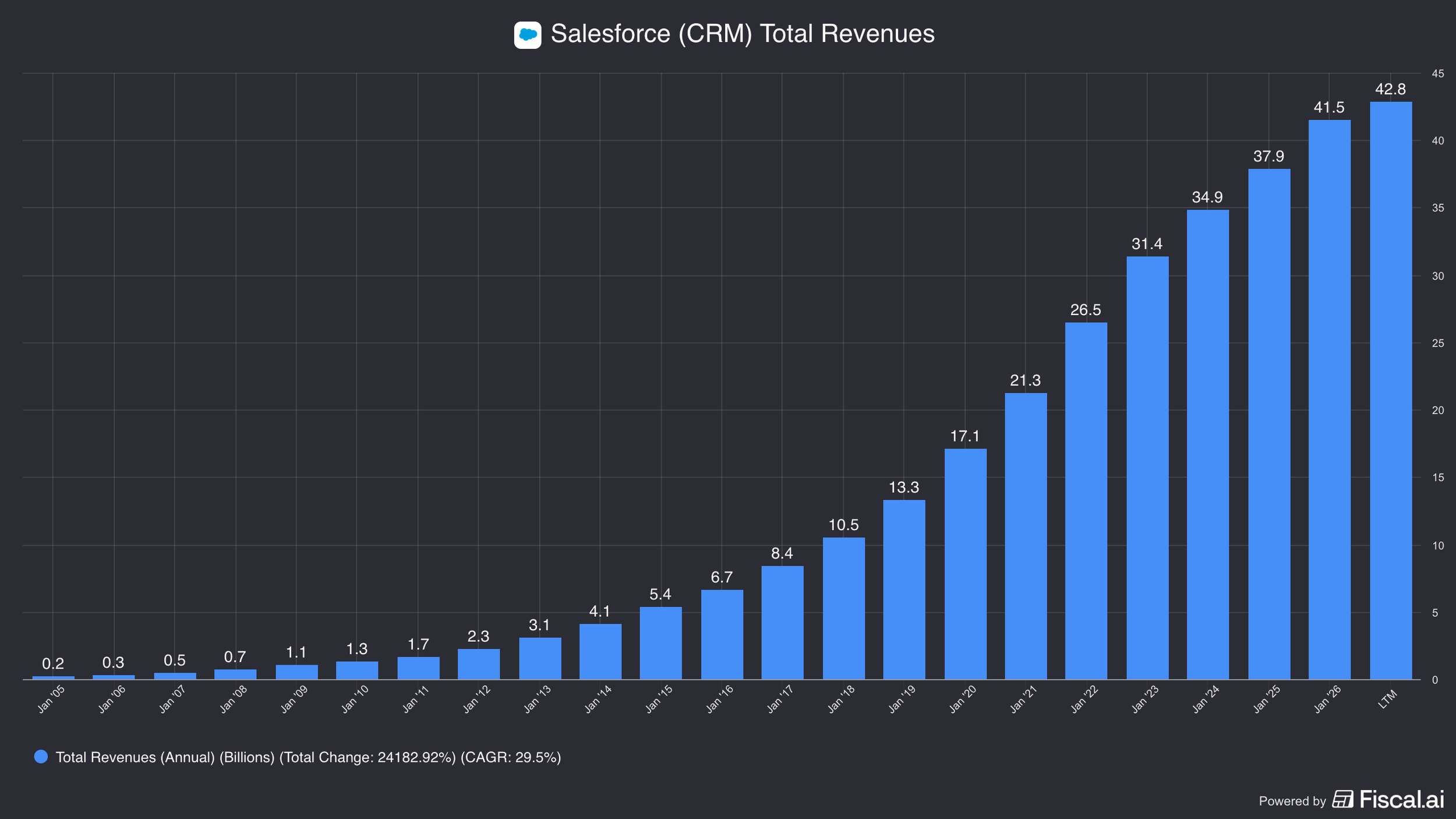

It took Salesforce over 20 years to reach that same figure.

Now, profitability remains an open question.

But what is not in question is whether people are willing to pay.

They clearly are.

And when Microsoft canceled their Claude subscription, it wasn't because nobody wanted Claude, it was partly because Anthropic is running at full capacity and charging accordingly.

That's a sign of constrained supply meeting high demand, not a sign of weak demand.

2. Supply Bottlenecks

The second counterpoint goes back to the capital cycle argument directly.

Yes, capital is flowing in and supply is increasing.

But the rate at which supply can increase is meaningfully constrained.

TSMC has limited fab capacity and is only incrementally expanding its capex, they're aware they could be left holding the bag if the cycle turns.

That's a meaningful cap on high-end chip supply.

Memory companies, while profitable and expanding, are doing so more deliberately than in past cycles.

And the biggest bottleneck of all is energy.

Even if you build the data centers, you can't run them without power.

That constraint may actually be a good thing.

Slower supply growth means supply is more likely to grow in line with demand rather than dramatically overshooting it.

And that's the key difference between this and the fiber optic build-out that occurred during the tech bubble.

During the tech bubble, over $200bn of fiber optic cable was laid and 95% of it went dark.

Nothing ran through it.

Are there dark GPUs today?

Not really.

In fact, GPU capacity is so constrained that used units are trading at a premium on the secondary market.

That's the opposite of what you'd expect to see in a market with oversupply.

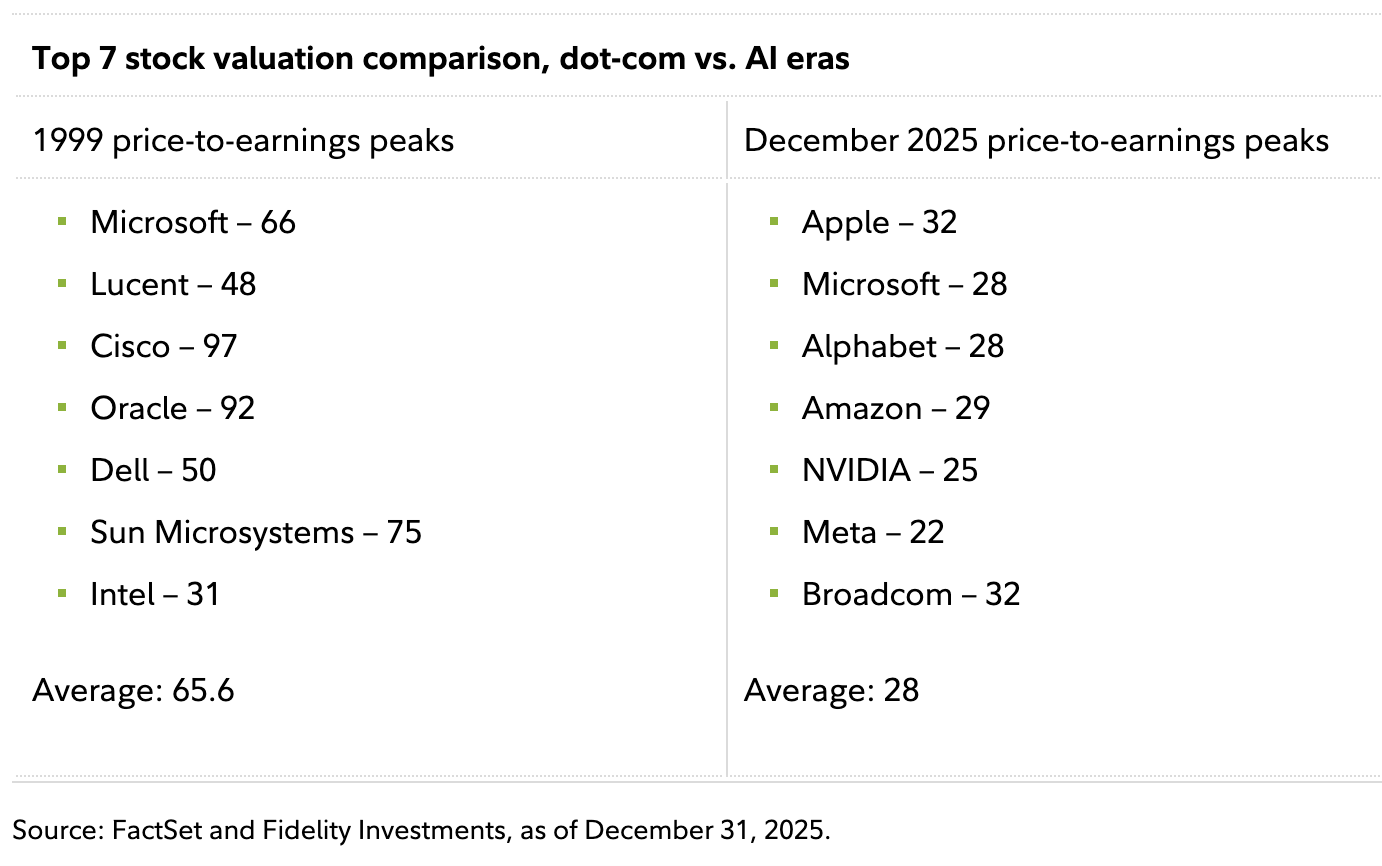

3. Valuations Aren't Nosebleed.

The third counterpoint has to do with valuations.

Yes, some individual stocks look stretched.

But if you zoom out and compare today's market to the tech bubble of 2000, the numbers are not in the same universe.

NVIDIA trades at roughly 24 times forward earnings.

The S&P 500 is at 21 times forward earnings.

At the tech bubble's peak, the S&P was at about 24 times.

The Nasdaq, however, is where the real contrast lives.

In 2000, the Nasdaq was trading at 60 times forward earnings.

Today it's at 24 times.

On a trailing earnings basis, the Nasdaq in March 2000 was trading at 200 times earnings.

Today it's around 30 times.

That's not even close to the same magnitude of valuation excess.

Certain individual names are priced for perfection, and those are worth being cautious about, but the broad market is not exhibiting the kind of extreme multiple expansion that characterized the dot-com era.

4. It's Mostly Cash-Funded.

The fourth counterpoint is that while debt is increasing, the vast majority of this AI build-out is still being funded out of operating cash flows.

Meta, Google, and Microsoft are extraordinarily profitable businesses.

They're generating the cash to fund these investments.

That matters because if the investments don't pan out, the consequence is a write-down, not a debt crisis.

Companies can absorb that and move on relatively quickly.

The systemic risk is significantly lower when capital expenditure is backed by earnings rather than leverage.

5. Higher Quality End Customers.

Finally, the fifth counterpoint is about who's actually buying all of this.

In past semiconductor cycles, the end customers were often PC makers operating on razor-thin, single-digit margins.

When the cycle turned, those customers would go back to their suppliers and say they simply couldn't afford the contracted prices anymore.

And suppliers, not wanting to lose the relationship entirely, would often capitulate.

Today, the end customers are Meta, Google, Amazon, and Microsoft.

These are among the most cash-generative companies on the planet.

They're not going to renegotiate memory contracts because they're struggling to make payroll.

That dynamic fundamentally changes the downside risk profile for the companies supplying AI infrastructure.

My Thoughts and What You Can Do.

So after all of that, where are we?

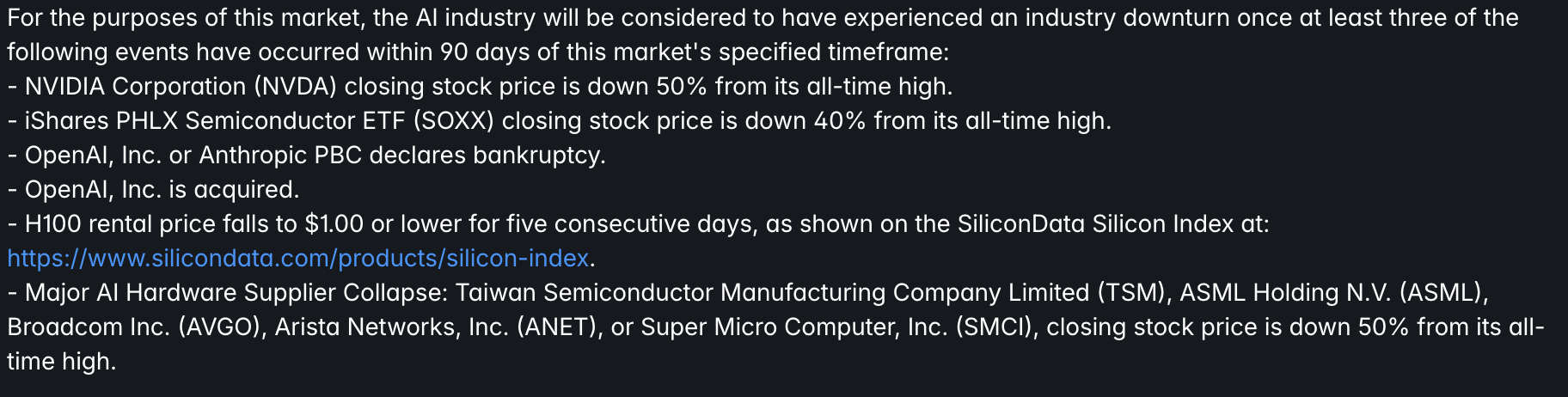

PolyMarket published a definition of a bubble bursting with money behind it: major AI stocks fall 50% from highs, OpenAI or Anthropic goes bankrupt, or NVIDIA's H100 rental rate falls from $7 to $1, with three of those required to trigger.

That's a fair characterization of a real industry downturn.

And I don't think we're there yet.

The S&P 500 at 21 times forward earnings is not bubble-level valuation.

Certain pockets absolutely look extreme, and those are worth avoiding.

But the broad market? Not there yet.

Here's how I'd characterize where we are in the cycle: we're probably in the middle.

For the rest of 2026, capital is going to continue flowing into AI — those budgets are basically already committed.

In 2027, I'd expect the major hyperscalers to put up similar levels of capex again.

By 2028, things get murkier, and the further out you go, the more uncertainty compounds.

The big events to watch are the IPOs of Anthropic, OpenAI, and SpaceX with XAI.

Historically, a wave of large, marquee IPOs tends to signal the later stages of a cycle.

That said, OpenAI and Anthropic are not the low-quality companies that were IPO-ing at the tail end of the dot-com bubble.

When Amazon IPO'd in the late '90s, there were still two or three years of run left.

So the IPOs of these companies may simply signal the next phase of the cycle, funneling fresh capital back into the same system.

Beyond that, we haven't even touched on robotics.

Once physical robots are integrated with AI at scale, that could be an entirely separate leg of this whole thing, potentially dwarfing what we've already seen.

Whether that happens in three years or ten is genuinely unknowable.

Now, what should you actually do with all of this?

Honestly? Not much different from what you should always be doing.

I don't think the market is at a level where pulling money out makes sense.

If you're concerned about concentration in large tech names, which will only grow as Anthropic and OpenAI land in the major indices, you could shift some exposure toward RSP, the equal-weight version of the S&P 500.

If you have a lump sum to invest, dollar-cost averaging is a perfectly reasonable approach right now.

If you're especially concerned, it's okay to hold a small cash position, not as an investment strategy, but as an emotional anchor that helps you stay invested with the rest of your portfolio.

But here's what matters most.

Your investment decisions should be grounded in your actual financial plan, not in bubble predictions.

If you were invested during the dot-com bubble but held through the recovery, you ended up fine.

The people who got hurt were the ones who needed to access their money to pay for a college tuition, a roof repair, or a medical bill right in the middle of the drawdown.

Financial planning helps you understand whether you're actually a long-term investor.

And if you are, then whether or not this is a bubble ultimately matters less than you think.

The goal of investing is to do well across the widest possible range of outcomes, not to bet everything on one prediction, even a well-reasoned one.

Here's my personal gut check.

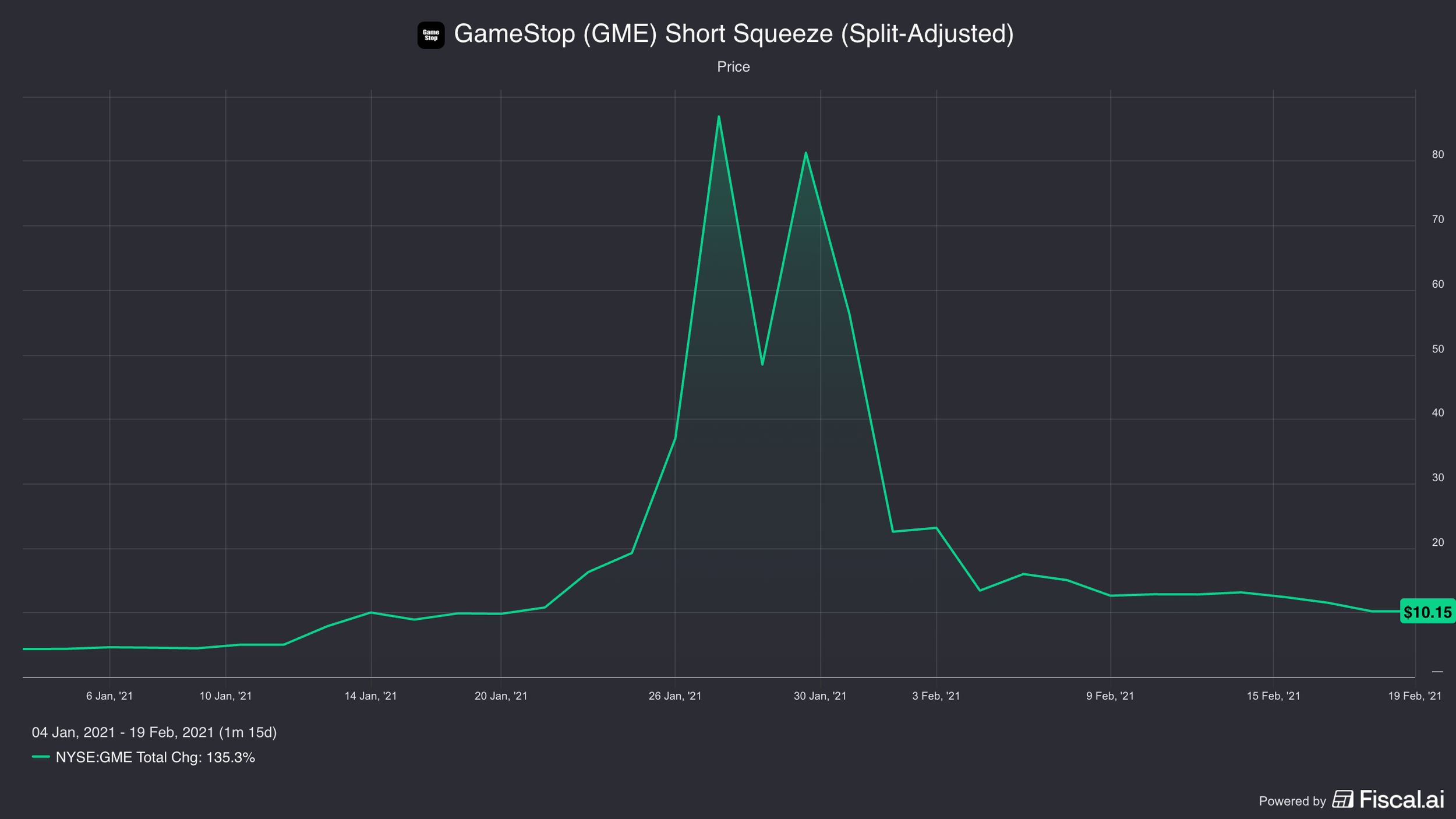

During the GameStop frenzy, three friends texted me asking whether they should buy in when it crossed $200 a share.

I haven't had a single person text me asking whether they should buy AI stocks.

That might just mean I have fewer friends now.

But I think it also speaks volumes to where we actually are in this cycle.

While I can understand fears of investing during a bubble, I also know how hopeless it is to try to time the market.

My suggestion is simply: don’t try to.

If there are areas of the market you find particularly frothy, you can avoid those.

And if you are worried about overall index valuation, you can consider investing in an equal-weight index like RSP.

For more on my analysis of whether or not we’re in an AI bubble, check out the video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.