How to Invest $1 Million Today

Get smarter on investing, business, and personal finance in 5 minutes.

Congratulations! You just saved up $1mn!

How should you invest it, and where should you begin?

In this week’s Five Minute Money, I’m going to share with you the 3 questions you must ask yourself before you invest a single dollar, the 5 mistakes you need to avoid, and then show you how you should actually allocate that $1mn.

Now, let’s start with the 3 questions you must ask yourself.

The 3 Questions You Must Ask Yourself.

Question 1: When Will You Need This Money?

Sounds like a simple question, but a lot of people don't actually think it through.

Is this money that you need for income in order to live off of?

Or is it money for some sort of future potential purchase like a second house or retirement, or an inheritance to give to the kids?

When you need the money is going to change how you should invest it.

Question 2: What Is the Money For?

If it is for retirement, how far away is retirement?

Is it for a second home or is it for a kid's college tuition?

Now, depending on the purpose of the money, it's going to actually change how you can invest because if it is for a kid's college tuition and you're going to need that money in two years' time, you shouldn't invest it in stocks.

You should put it in treasuries to make sure that the money is there and that there's not a large drawdown and it hasn't recovered, and so then you're dipping into more principal than you would've otherwise.

So depending on whether or not the money is going towards something that must happen at a specific date or if it's more flexible, that's going to change how you invest.

For example, let’s say you want a second home, and you keep saving up towards that, and you're investing towards that.

But it doesn't need to happen in 3 years, it could happen in 5-6 years.

It's not the end of the world, if it gets pushed back.

Depending on whether or not this is money you need or it's more flexible, that's going to also change how you invest.

If it's more flexible, you could keep more money invested in long-term assets like equities, which perform well over the long term but can be volatile in the short term.

Question 3: How Do You Handle Stock Volatility Emotionally?

This is going to be one of the most important questions you ask yourself.

How do you do emotionally with investing?

Are you the kind of person who watches the news and freaks out a little bit and wants to sell all of your stocks every time you hear about something bad happening?

Or do you worry when you see stocks are down 20-30%?

Does that make you want to sell everything?

Does that make you scared?

Does that make you want to exit your portfolio?

If you are someone who does get a little more emotional, that's totally fine.

It's better you recognize that, and we'll invest you a little bit differently, and that'll still lead to better results over the long term than if you try to fool yourself saying that you can handle the volatility and you really can't.

Now that you have answered the three questions, let’s move on to the 5 mistakes you should avoid.

5 Mistakes to Avoid.

1. Avoid Stock Picking.

This one may surprise you coming from someone who researches and actively invest in stocks, but the vast majority of people are going to want to avoid stock picking.

If you do want to pick stocks, you have to understand that is like a mini job in and of itself.

You have to thoroughly research what you're buying.

You have to understand everything about business analysis, valuation.

But again, for the vast majority of people, you should not be picking stocks.

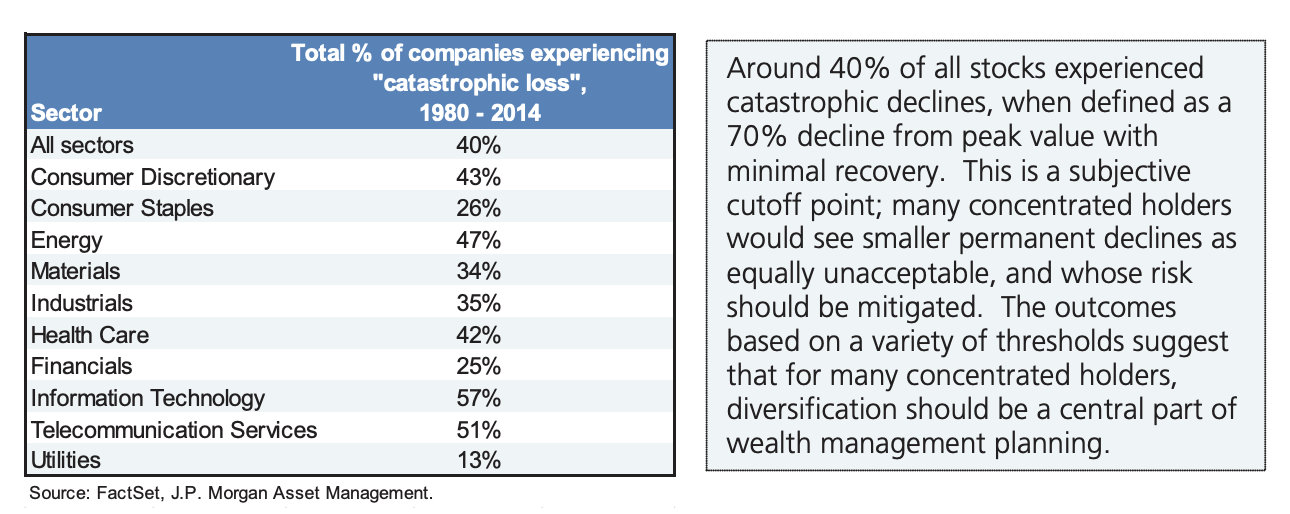

J.P. Morgan did this study where they looked at the Russell 3000 over a 20-year period, and they found that 40% of all stocks suffered a catastrophic loss that they never recovered from.

What is a catastrophic loss?

That is a loss of over 70% and the stock never appreciates.

That's almost half of all stocks suffer this level of impairment and never recover.

And I'm not even talking about stocks that actually make you money.

I'm talking about stocks that just totally destroy your wealth.

This goes to show you that it is much harder to actually pick stocks than it is to beat the market.

We know that almost all active management funds, over 95% of them, underperform over a 5+ year period, and then you keep going out and it's over 99%.

This is to say that it's very hard to pick individual stocks.

Now, the reason why I still like doing it is not just because I have a bias as someone who researches stocks all day, but I do think it allows you to actually own something where you can have confidence in that specific valuation, that business, and the potential future outcomes.

Of course, it's very hard to do, but that is why I still think it's appropriate if you are, you know, having that skill set of researching businesses.

For the vast majority of people and in order to build your wealth, it's not necessary.

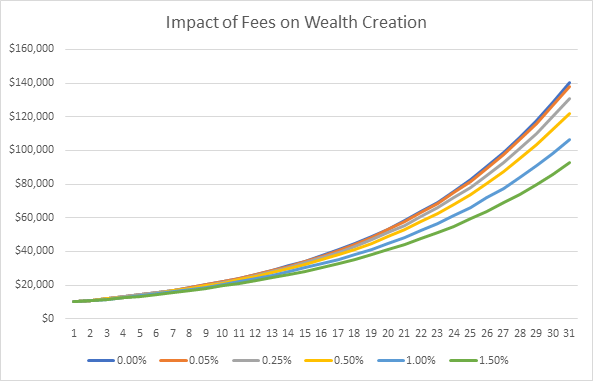

2. Avoid High Fees.

You've probably heard this before, but you might be surprised to learn that it is still very common that mutual funds have loading fees.

This means you buy the mutual fund, and you're literally paying an upfront fee immediately just for the right to get in, and then there's also ongoing fees as well.

You should not be paying any of these fees.

The performance is seldom ever good enough to warrant paying these fees, and there's a lot of great ways you can invest and get broad stock market exposure with a very low-cost ETF.

You really shouldn't be paying more than 30 basis points, which is 0.3%, when you are buying an ETF.

On an ETF, you can find out how much you are paying in fees by looking at the expense ratio.

If it goes a little higher than 0.3%, there might be some specific reason why you want certain factor exposure, something like that.

But for most investors, you should really keep it under 0.3%.

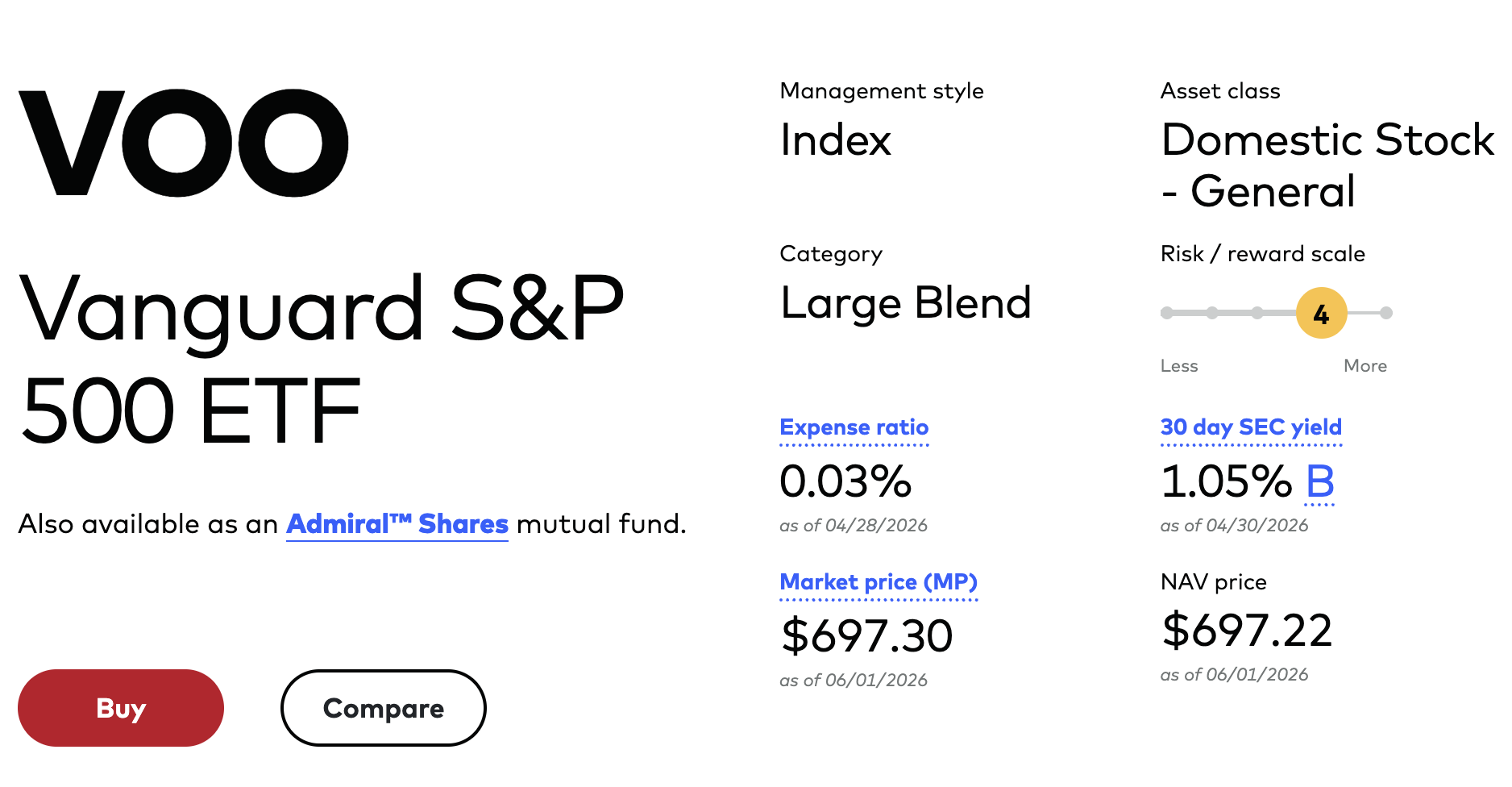

For example, the Vanguard S&P 500, has an expense ratio of 3 basis points, or 0.03% which is almost nothing.

That's another big mistake investors make is not paying enough attention to the fees of their investment products.

3. Avoid Dividend Stocks.

The reason why I'm saying this is that a lot of people will want to generate income in their portfolio, and they will go and buy a dividend stock in order to do that, thinking that this is a good way to generate money.

Here’s a quick explanation of what a dividend is and how it works.

When you are picking a stock or you're invested in a business, it generates cash flows.

Then the business makes a decision of whether or not they want to reinvest those cash flows or give some of those cash flows back to investors.

If they give cash flows back, you get a dividend.

And so, people might think this is a great way to generate income.

The problem with that is it makes an investor focus singularly on one factor of the investment, which is how much cash the business is giving back, rather than looking at the business holistically and how much the total appreciation is of that stock.

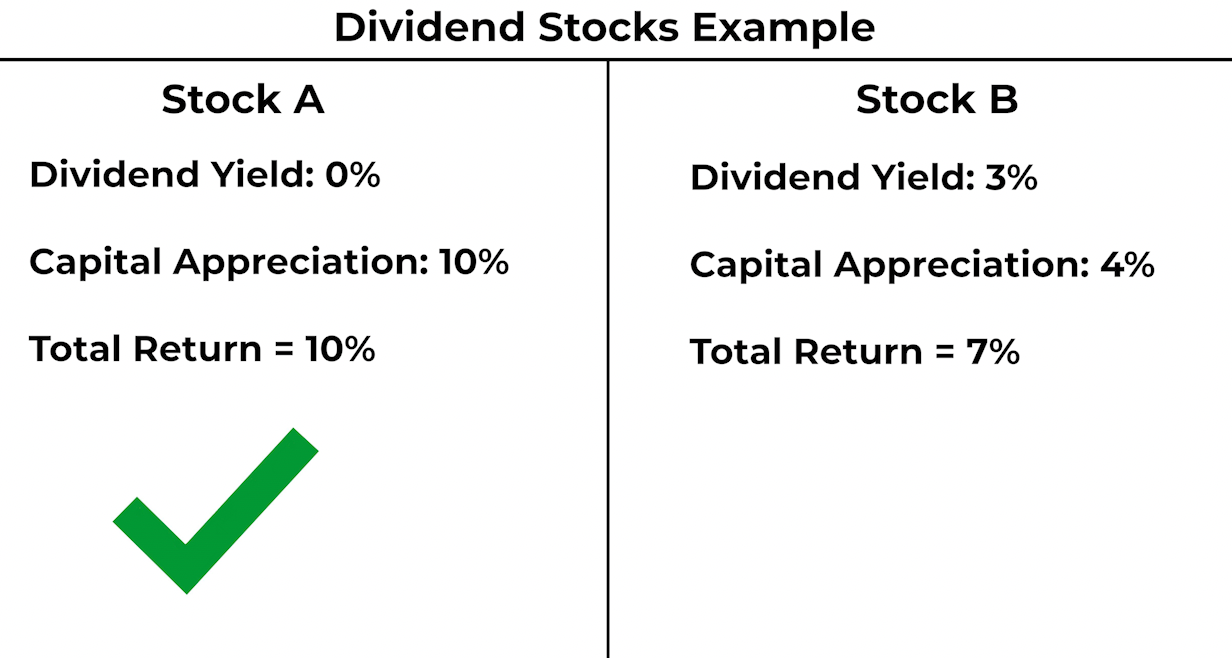

For example, you have 2 stocks to choose from: Stock A that will generate a 10% return from capital appreciation and 0% from dividends, or Stock B that will earn a 3% dividend yield and 4% from capital appreciation for a 7% total return.

You should always go for Stock A earning 10% and if you need the income, you just sell some shares.

This is a more efficient way to invest and also for tax reasons too.

Often, depending on whether or not it's a qualified dividend, you could be paying higher taxes on dividends too, whereas if you're selling a stock you've owned for a while, it usually gets a lower tax rate, the treatment of capital gains.

So do not invest in a stock just because it has a dividend yield.

If you hear people saying you should own some dividend stocks or something 'cause they're safer, that is also not true.

Just because a stock pays a dividend yield does not mean it's safer, and it could actually be at risk of that dividend yield falling or being cut.

Very often it is the case that it's more mature companies that are paying dividends out, which also means they usually have less opportunity to reinvest back into the business.

Now, that's not always true, but I think if you look at most dividend stocks, that's probably true.

With that said, a dividend in and of itself doesn't mean that much.

That's not enough for you to decide to go out and buy it.

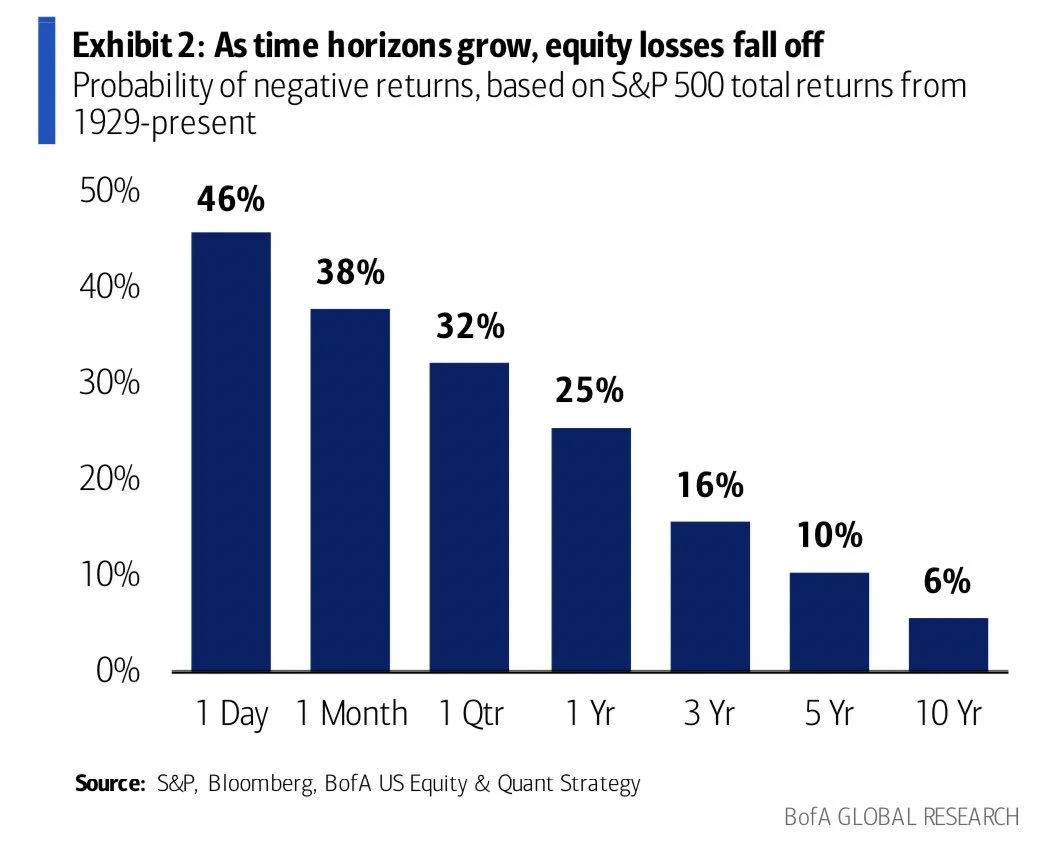

4. Avoid Timing the Market.

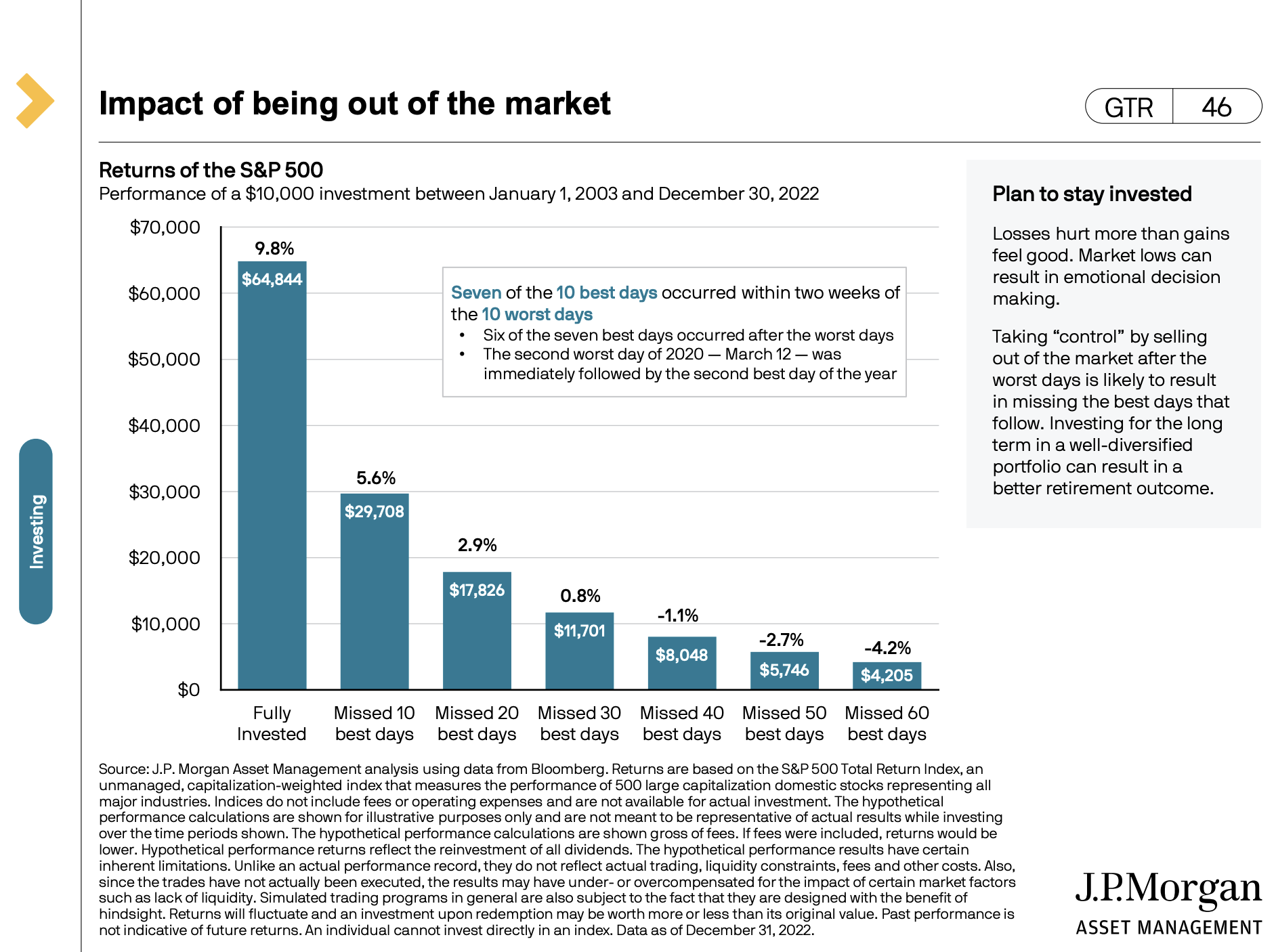

JP Morgan had this study that said, if you look at this 20-year period they were looking at from 2003-2022, and they said the stock market returned 9.8% on average, yearly through that period.

However, if you missed the best 10 days during that period, that return fell from 9.8% to 5.6%.

If you missed the best 20 days, that return drops even more to 2.9%.

You missed the best 30 days, that return falls to 0.8%.

So if you missed the best 30 days in the stock market over 20 years, you make almost nothing invested in the market.

So that is why time in the market matters much more than timing the market.

Furthermore, the best 6 of the 7 days they looked at fell immediately after the worst day in the stock market.

So you have to time it so precisely in order to sell something right before the worst day and then buy it back on the worst day in order to catch that best day.

You can't time the market.

People have tried to do it.

It ends in tears usually, or at least subpar results, and so avoid doing that.

5. Avoid Single-Property Real Estate and Angel Investing.

There are many times, when people get some money, $1mn, and it feels good owning assets, and so they want to own some real estate.

Look, I like real estate. I think it's the best way to generate income and there's also protection against inflation, and it's a good asset class overall.

The problem is when you're buying an individual property, that most people miss, is that you've basically just started a small business.

It may be a relatively easy business, but it is a business no less that will require actual time spent on your part in case things go wrong.

Someone has to manage it. Someone has to deal with maintenance. Someone has to find tenants.

There's a lot of stuff that's actually involved in owning real estate, and so it is not a passive investment.

People think of real estate as passive income.

That's a lie.

That's a lie because there's still active work involved in it, not to mention finding the property and making sure you're invested in the right property.

So if you want to do it, just understand that it's basically like taking on a new hobby, a new small business endeavor, and it will require a lot of research.

And if you are new to it, there's risk that you miss things.

I'll hear all sorts of stories of people that buy properties for the first time, and there's things they didn't know to check in the foundation, and then they get hit with the big maintenance bill.

There are all sorts of different things that you just don't think to think of until you're in that business.

And I have seen people make this mistake firsthand where they will go out and buy a property.

It looks great on paper.

They get sold by the broker, and it just doesn't go as according to plan, and they don't really know how to manage it.

And now they're kind of getting involved more and more in this property, and the return wasn't even that good.

What was the real point of it?

For most people, I think you should avoid doing investing in single-property real estate.

I'm going to extend the same advice to angel investing.

Sometimes people think, 'I'll just throw a couple, $25-50k in a bunch of small investments, and I only need one of them to hit!'

That is a great way to lose all of that money.

Earlier, I gave you the stats that 40% of all stocks suffer a catastrophic loss and never recover.

The stats are much worse for early-stage businesses.

If you want to angel invest and do that, just treat it as a pure speculation and really limit the amount of money you're doing in that.

This should be less than 5-10%.

This is just a great way to burn money because you think it's a small amount, and you place enough of these bets, something will work.

It turns out that most of your bets are unlikely to succeed, and the odds rarely work in your favor.

How to Actually Invest Your Money.

Step 1: Set Aside Emergency Savings.

The first thing you want to do in terms of thinking of this overall portfolio allocation is you want to think about how much you should keep in emergency savings.

As a general rule of thumb, you should keep about 9-12 months of your fixed expenses in emergency savings.

Now, this is going to be conservative.

Some people disagree with me here.

I would rather be conservative here, though.

And so especially if you've got a family and you lose a job and there's a recession.

It makes sense to me that it's just nicer to have a longer runway.

Some people may even want more, and I don't think that that is that bad of a decision.

I think that if that makes you feel good, you can have more in savings.

But general rule of thumb, 9-12 months of fixed expenses in emergency savings.

If you're spending, let's say, $15,000 a month, then save $135,000 in this emergency savings account.

Now, this is money that should either be invested in a savings account, or even better is short-term treasuries.

So do nottake duration on the treasuries.

You're going to want to invest in T-bills with 3 months or less.

And the reason why you don't take duration risk is because if interest rates go up, then the value of the treasuries will fall much more.

For example, if you took put your emergency savings in a 5-year note, and then if you needed that money in an emergency, it's not there, or less of it is there.

You never want to take duration risk with your emergency savings fund.

So, 3 months or less in treasuries, or you could do a high-yield savings account.

Remember, when you own treasuries, you're not paying state tax if you're in the US.

So that's something to keep in mind.

Step 2: Invest the Rest in the Stock Market.

Now, what do you do with the rest of the money that you have?

If you have more than 10 years before you need this money for retirement, it’s very easy to say that we're going to invest it all in the stock market.

Ten years is a very conservative number.

It gives you a lot of time in case that we have a lost decade, which could mean that stocks go down a lot.

It gives them a lot of time to recover.

Some people may want to do more like a 5-year rule of thumb where if I don't need the money for 5 years, I'll invest it in the market.

But I'll also say it depends, going back to question number two, you know, what is this money for and how important is it that you have it on exactly date 5 years?

Because if it is critical that you have that money in 5 years to the date, then you may not want to play these games, and you may want to make sure it's there by putting more in treasuries.

Or if it's fine, you can push this expense out a couple years or worst case scenario, delay retirement a year or two, then that's fine.

You can invest more in the market.

We are going to assume that you have ample time and you're comfortable investing in the stock market.

Here's what you should do.

Of that $1mn you had, we put aside about 13% into treasuries for the emergency savings fund.

The rest of it, $870,000, we’re going to put this all in the stock market.

A lot of people think that stocks are risky, and they are, but the caveat is that they actually become less risky over a longer time horizon.

The more time you have to invest, the less risky it is to invest in the stock market.

Whereas other asset classes like bonds are not becoming less risky the longer you own them.

In fact, they could actually be more risky because inflation can change, interest rates can change, and so that can actually really impact how you could do in bonds.

And so stocks are just going to be the best way to go for your investment allocation.

And there's going to be a desire to make this complex.

Don't do that.

Let's just keep this very simple, and simplicity tends to lead to the best results here.

You don't need private equity.

You don't need fancy hedge funds, a fancy mutual fund manager.

You don't need to pay anyone fees.

You could just invest in low-cost index funds.

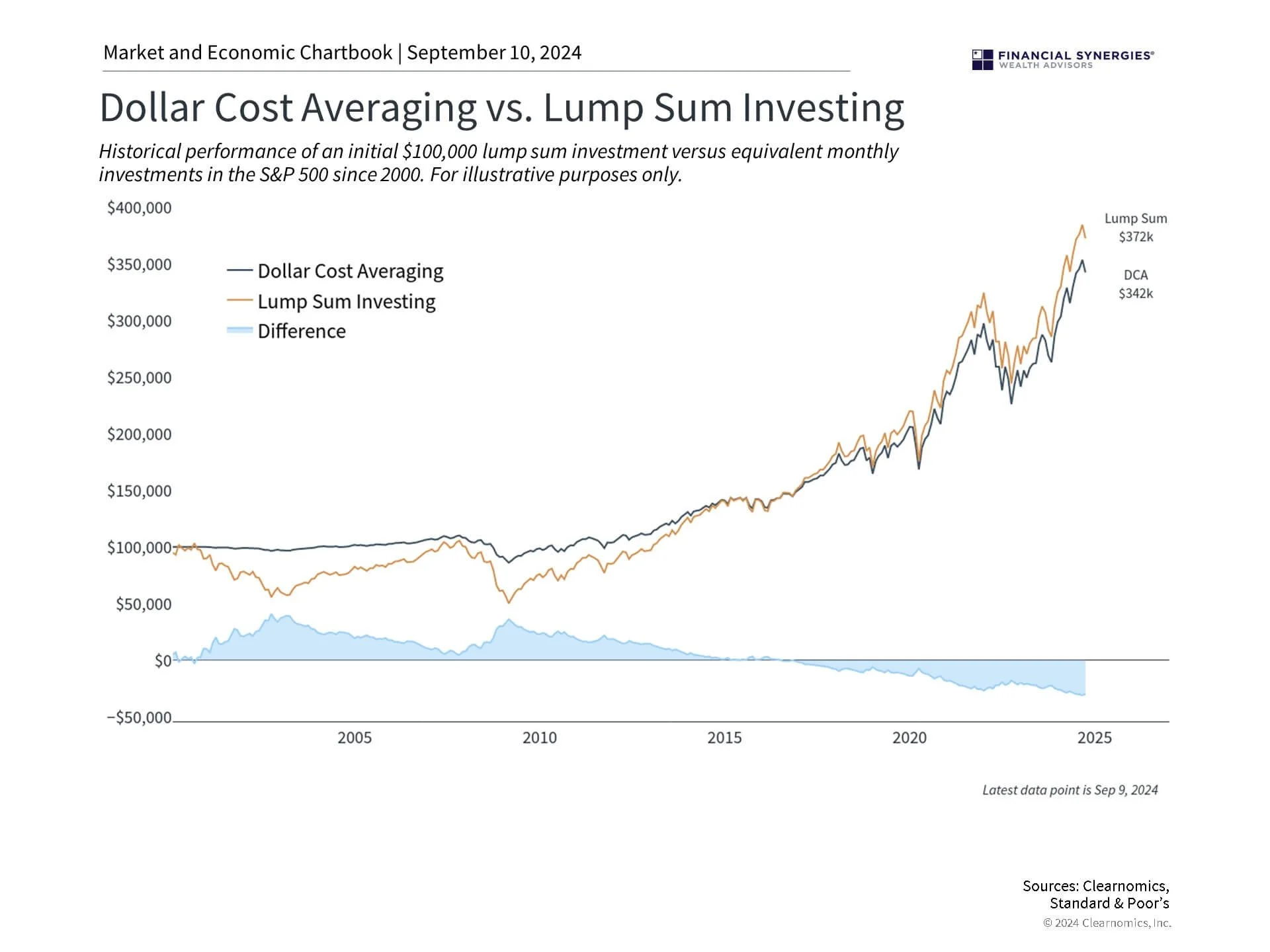

Step 3: Lump Sum vs. Dollar-Cost Averaging.

The next question you might be wondering is: do I just invest all of this money in the stock market right now, or do I dollar-cost average over time?

The answer is, it's going to depend a little bit on your disposition.

Now, if you look at when lump sum tends to outperform dollar-cost averaging, it's in about two-thirds of all instances, it makes more sense to just put all of your money in the market and not dollar-cost average.

And so that means that this $870,000, we'll just invest it today, and we won't add anything else to it unless you have more savings coming in, then we'll continue to add.

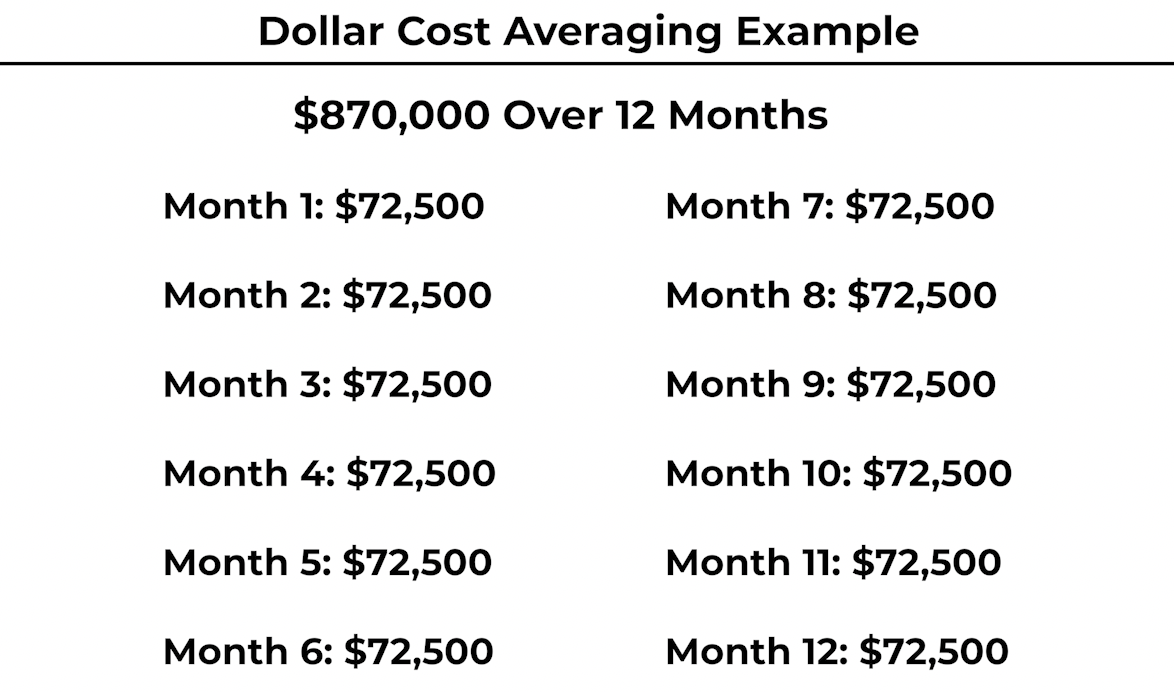

Dollar-cost averaging would mean let's split up this $870,000, into12 equal increments and invest it at the end of each month.

Now, what I will tend to do is a mix of both.

I will usually invest 50-60% immediately on day 1 of fresh client cash, and then the other 40-50% we could dollar-cost average over time.

Now, part of that is because there is a risk that maybe you are investing at a time where valuations are especially high, or there is a bear market or something like that.

But it's also a psychological thing, where people do not like all of their money just invested in one day, and I think this is fine.

Again, this is really about getting your money in the market, and if it takes a little bit more time to get it fully invested, it's not going to be the end of the world compared to if you are so scared to start that you just never do.

I would rather someone dollar cost average, put a little bit in over a longer period of time and get started versus not doing it at all.

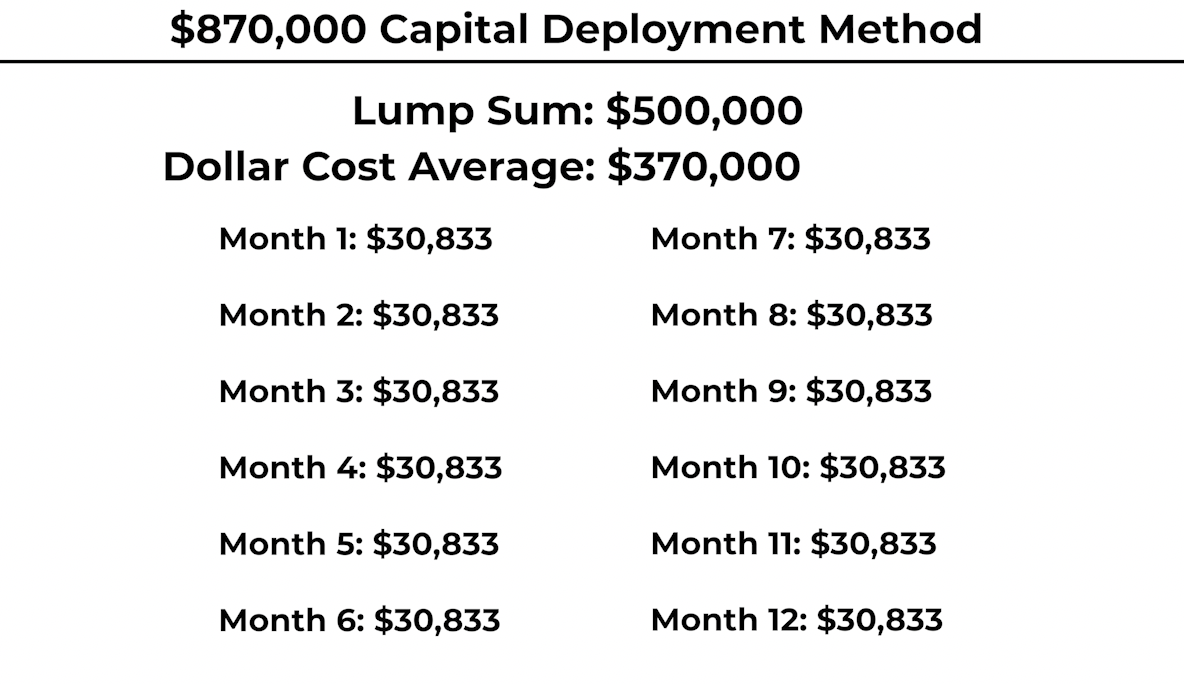

So of this $870,000, we will invest $500,000 in the market immediately and then the rest of the $370,000, we will split it up into 12 payments over the year.

The other thing to keep in mind is that if we do happen to have a correction in your dollar cost averaging, put all of the money back into the market.

Let’s say that we did a couple of these increments, and we have like $250,000 left to invest, and we were continuing to split that up over some period of time, but then the market fell more than 10%, I would just put that full $250,000 into the market because we don't get corrections that often, and when we do, you should just get fully deployed into it.

It's going to be a little scary at that time because something's going to be happening in the world.

And then you're also going to be wondering, 'Oh, maybe it's going to go down more.'

But just get the money in there.

You're not going to get it perfect, but don't let perfection be the enemy of good enough.

Because if the market dropped 30% and you put it all in when it was only down 10%, you're still going to have a pretty good result over time.

In more circumstances than not, the market could be down 10% and then you were waiting, and so you didn't actually put the money in, and then it ripped back up, which is what just happened earlier this year, with the Iran war, and the market went down ~10%, and then it ripped up very quickly in the other direction.

So, if you were waiting for a bigger drawdown, you didn't get it, and you were left holding the bag.

Step 4: Which ETFs to Buy.

Now, in terms of actual ETFs you can own, there's a bunch of them.

I'm just going to give you here very simple ETF selections here, and this is going to be good enough.

You don't need to make things more complicated.

This really could work for even a $5-10mn portfolio.

It doesn't need to be that crazy complex.

The ETFs that you should own are:

1. Vanguard S&P 500 Index (VOO)

2. Invesco Equal-Weighted S&P 500 (RSP)

3. Invesco QQQ (QQQ), which is basically the Nasdaq, a more tech-focused index

4. Vanguard Total Stock Market (VTI), this is inclusive of small and mid caps.

5. Vanguard Total International ETF (VXUS)

There will be a good amount of overlap between VOO and VTI, and so maybe you don't want both or maybe you want to just put more into VTI rather than VOO.

Now, a lot of these ETFs I mentioned, they're pretty US-centric.

Just because it's a US-centric index doesn't mean that these businesses aren't multinational.

If we think of what the largest companies in the S&P 500 are, Apple, Google, Microsoft, Nvidia, these are companies that sell stuff all over the world.

And so just because it is the indexes are US-centric, doesn't mean the businesses necessarily are.

Now, in terms of allocations across these, there's a lot of different back testing you could do, but just to keep things simple, you could just equal weight all of them.

You could put 20% into each of those 5 ETFs and then if you do have more money to add over time, you could see which ones fell in value more, and then just add more to that.

For example, let’s say in a year from now, QQQ is still ripping, and the RSP and international markets are underperforming a little bit, you could add more to RSP and VXUS when you're adding money to that account, and that's kind of rebalancing it a little bit over time.

And that way you're kind of doing a reversion to the mean sort of strategy.

That's just very simple educational advice here.

You should talk to a financial advisor to see exactly what is best for you.

But I think if you're just trying to do things very simple on your own, this is going to be pretty good for just the vast majority of people.

You could just be on your own, and you could enjoy life and don't have to think about investing ever again.

For more on How to Invest $1 Million Today, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.