The Simple Test Every Great Business Passes

Get smarter on investing, business, and personal finance in 5 minutes.

This Five Minute Money was adapted from a recent video Drew Cohen had on the topic.

If only there was a simple formula that can help us figure out which businesses are going to be successful over the long term and give investors outsized returns.

Well… fortunate for us there is.

I notice that all great stocks or great businesses have these three aspects to them, and that is that they

1. Create value

2. Capture a portion of that value and

3. Protect that value

In this week’s Five Minute Money, we are going to break down what that all actually means with examples and case studies, and instances where businesses may have done one of them, but not all three, because even though it sounds simple, of course, we know investing in practice is hard.

Creating Value.

If you think about a business that creates value, there's no better example than the airline industry.

Airlines literally allow us to get to places to see our loved ones or conduct business that we otherwise would not be able to do.

And frankly, at not such an expensive price.

You could go halfway around the world for $500, if you're getting a budget seat.

Whereas before you could have died, making that journey on a ship.

Airlines have provided a tremendous amount of value to everyday life, except… they're awful businesses!

And despite the fact that they've created so much value, they've really failed at capturing any of that value for themselves.

They usually swing between a very small profit margin and a loss, and in addition to that, are almost always at risk of going bankrupt.

In fact, most airlines that have ever existed have already gone bankrupt.

What they really suffer at is capturing a portion of that value they are creating.

Capturing Value.

There are many reasons why a business will not be able to properly capture its value.

But you should note that you should look for businesses that have already proven success or have a plausible way to capture a portion of that value.

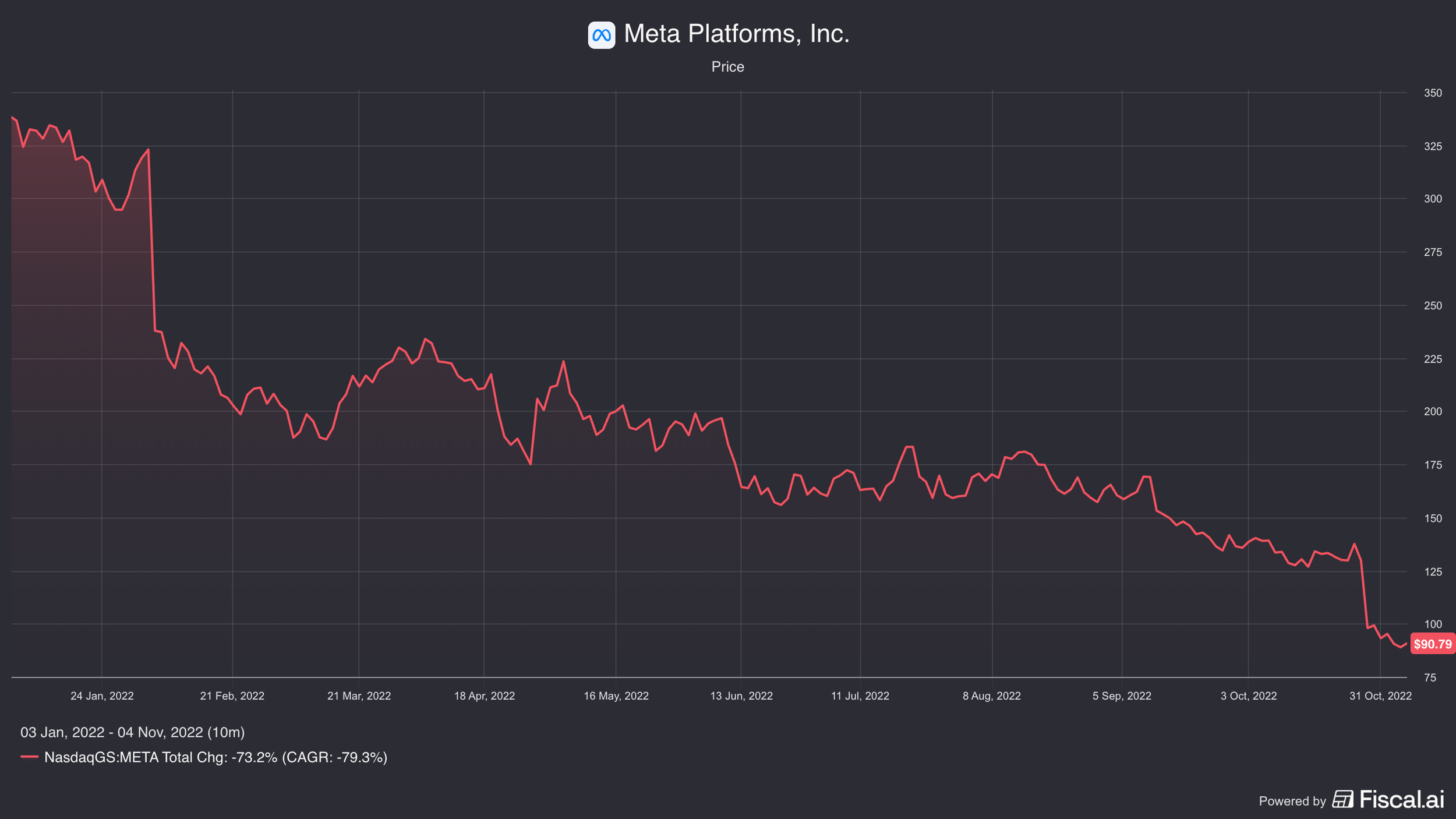

Now, it might surprise you to learn Facebook at one point was in that bucket.

Now people knew Facebook was creating value early on.

It allowed people to keep up with their friends and family and allowed all sorts of socialization over the internet.

Yes, some to the negative, but also a lot to the positive that wouldn't have happened otherwise.

So Facebook was creating value, but investors were really unsure whether or not they'd ever be able to monetize any of that.

Investors thought they'd be able to throw some ads on the side of it, but that was never really going to make it that profitable of a business.

Now, there were some people that were connecting the dots that with all the data they had on individuals that they're collecting, that that would allow for super targeted ads, but that was never done before at the time.

In fact, ads at the time were really bad.

And before they really became personalized, they really weren't worth much.

So, Facebook was capturing a very small portion of the value it was creating.

Whereas today, once they really figured out how to target the ads, they're able to capture a much larger portion of value.

That goes to show that just because you're creating value doesn't mean you're going to capture any.

Remember airlines not capturing much value, LLMs and AI is sort of in this area right now.

AI models are creating a lot of value.

You could use ChatGPT for free, Google Gemini for free, and they create a ton of value.

Are they going to be able to monetize that?

How much value are they going to be able to capture?

That's the question.

Now ChatGPT has premium subscriptions, which you know, some portion of people pay for, but a lot just still use it for free.

We have seen recently that they have introduced ads into ChatGPT, which is a potential way that they can monetize the service.

But then there's also the issue of whether or not users will go to a different sort of chat bot that doesn't have ads.

We’ve seen Claude gain wider adoption since ChatGPT started introducing ads.

There's an issue that maybe people trust the chat bot less once they introduce advertising into it, which could prove to be sort of a product problem down the line.

Especially if a competitor is able to continue to subsidize their growth with profits from a different business like Google is doing currently with Search.

However that develops is not the point.

The point is that they right now are creating a lot more value than they're capturing.

Hence the reason why they barely have $20bn in revenues despite having ~1bn users on ChatGPT.

And that is going to be a question for a lot of different new businesses.

It's clear how they're useful in creating value, but how do you monetize that?

How much are you going to be able to capture?

Protecting Value.

Now, there are businesses that were able to successfully capture a portion of the value they created, but then they weren't able to protect it.

Very common too, if you think of the light bulb, which is very easy to see how that added a lot of value to our life.

The original creator of it, Thomas Edison and General Electric, were able to monetize it.

They sold light bulbs and they had patents on it, so other people weren't able to.

Except over time that manufacturing business eventually felt more and more pressure as other manufacturers entered that business.

And the light bulb, while temporarily having captured a good portion of value, eventually became a very mediocre business.

In fact, General Electric doesn't even own their light bulb business anymore.

They sold it and just licensed the name currently.

What that means is that just because you're able to capture a portion of value is not sufficient to being a great business.

You need to be able to protect it, and capitalism is brutal.

If you think about Pinkberry, which was one of the first frozen yogurt shops in the US, they had lines around the block.

They were doing incredibly well, except many other yogurt shops entered the space and as a result of all of that, their returns went down and it no longer was such a great business that was able to capture a portion of its value reliably that it was creating.

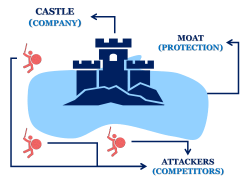

What ends up happening is that even if a business is able to create value and capture a portion of that value, it means nothing unless it can protect it which is usually what the greatest investor of all times, Warren Buffett, calls a competitive moat.

We're looking for these businesses with competitive moats, but of course, in reality it's not so easy because businesses very often lie right in the middle between capturing a portion of value successfully and having a moat that is a little dubious.

Evaluating Competitive Moats.

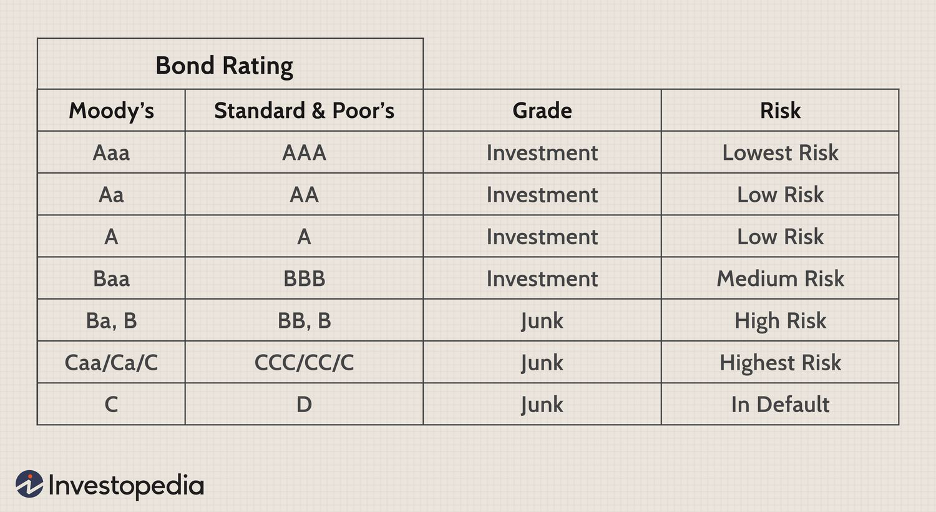

Take Moody’s for example.

Moody's is a credit rating agency, which basically by regulation is only going to be one of the three credit agencies ever (S&P Global and Fitch are the other two).

When you issue a bond, you need a credit rating on it in order to get a lower yield.

It basically pays for itself getting that rating, because it saves the company issuing that bond interest costs.

That is a very hard business to disrupt and has very strong moats.

But what about a business like Duolingo?

Where does that lie on the spectrum?

They're clearly capturing a portion of value right now.

They have over $1bn in revenue, positive free cash flow, but how well are they going to be able to protect their app against incumbents in the future?

Now people may think that Duolingo is sort of this example that's a little bit in the middle and it's kind of hard.

I'm telling you, it's always hard.

Instagram for example, just four years ago, people were worried was going to eventually fall wayside to TikTok and other social media apps.

They said the same thing about Facebook, and in fact, people are still predicting Facebook's demise.

How much of a moat does Facebook really have?

It may seem clear to some investors, but other investors are very much in disagreement about that and think that Facebook is going to eventually hit irrelevancy.

And if they're not saying that today, because the stock price is high, they surely were saying that a couple of years ago when it was trading at a $100 a share.

That goes to show that whether or not a company is able to properly protect the sort of value that it's able to capture is very much up for debate and a key part where you as an investor are able to differentiate yourself.

What you want to be able to do as an investor is see around the corner and understand what is really protecting the returns of a business.

To understand that, you need to know the 6 competitive advantages that protect a business’s return.

The 6 Sources of Competitive Advantages.

1. IP and Brand.

Once a company has a brand that people recognize, that tends to be an advantage in and of itself because it lowers the customer acquisition cost.

People trust it more, so they're more willing to spend money there.

If they see the same brand in multiple places, like a Starbucks all over the place, they have an idea of what they want.

It's been said what a brand is basically a promise.

And once a customer knows what that promise is, they're much more likely to transact.

And so that is what a brand is.

I’m including IP in this advantage too because these are both like intangibles that are hard for someone else to replicate.

IP could be when you have a patent, as General Electric had on the light bulb.

The idea is that if you have a patent, there's usually an amount of time that other competitors aren't allowed to copy you.

Usually, it is around 20 years or so, and sometimes you could get it extended.

You want to be able to build a brand in that amount of time.

General Electric was able to build somewhat of a brand.

It just turned out, people don't care that much about the light bulb brand they're buying their light bulbs from, and manufacturing is hard.

But there's other examples of companies that were in very competitive fields and were able to successfully outcompete with a better brand.

There's a lot of examples in the food industry.

Coca-Cola for example, even though many people actually in blind taste tests prefer other alternative colas better than Coca-Cola, at the end of the day, what they really want is that brand.

They want to buy the real thing.

They want all of that association with happiness and all the billions that Coca-Cola spent on advertising.

That is Coca-Cola using their brand to differentiate themselves even though they don't necessarily have anything within the product someone else couldn't copy.

2. Scale.

Most businesses they have a fixed cost portion and a variable cost portion.

The more that you are able to share that fixed cost portion across more units, the lower the fixed cost is per unit.

That is one source of leverage.

When that happens, we call it operating leverage.

The other thing that happens when you buy at scale is you're able to usually get bulk discounts.

That's another big advantage.

Additionally, you're also able to just kind of streamline the system better.

If you think about Costco for example, they benefit from this in multiple areas.

They have those vendor discounts when they buy in bulk.

In addition to that, because they push so much volume through an individual store, the real estate, the warehouse, all of that, even the employees are amortized across a much larger cost base.

So, their costs per unit or customer are much lower than a competitor who doesn't have that same sort of volume or traffic.

3. Asset / Resource Advantage.

Sometimes when you have a lot of scale, there's a resource you could take advantage of better than someone else.

An example would be a mine or an oil exploration production company.

They need a lot of scale in order to profitably pull out a lot of the resources from the ground.

But an asset advantage doesn't have to be just you exploiting a resource or requiring scale.

It could be a separate advantage from that.

Real estate is a classic example of an asset advantage.

If you're able to have a property somewhere that is very highly trafficked and a competitor doesn't, that is an advantage.

4. Regulation.

Another advantage, and we hit on this with Moody's, is regulation.

If you're regulatorily protected, then that is a huge advantage and that could come from different reasons.

In Moody's case, it has to do with a lot of financial regulation.

But it could also be that you have a plot of land that is licensed to carry salvage vehicles like Copart has, and that is a very hard license for other land to get.

That is an advantage.

Maybe you have a piece of real estate that is zoned for commercial building.

That is a certain sort of advantage.

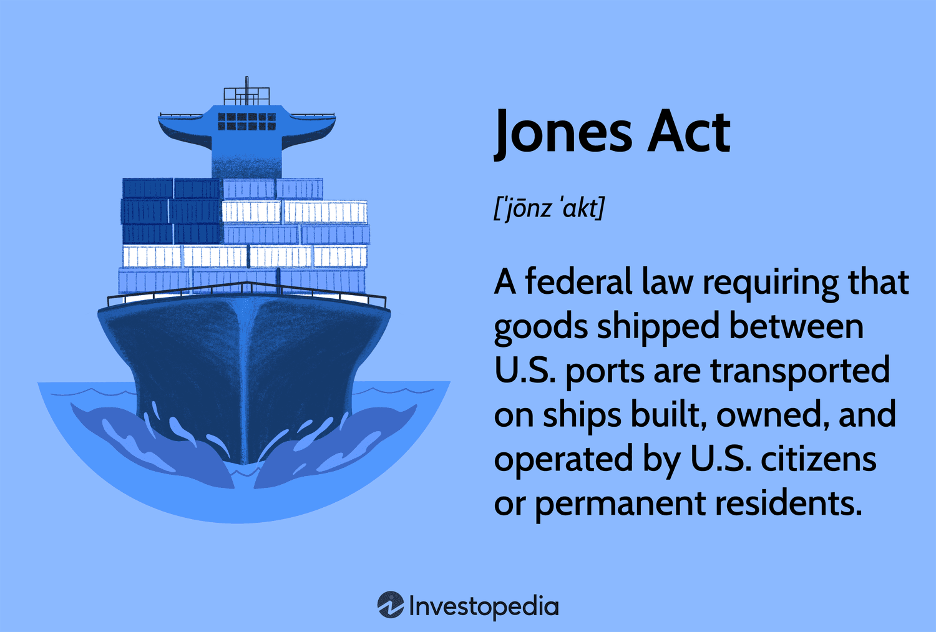

Maybe you're in a business that's protected by actual legislation.

There's a company called Arcosa that would make steel barges.

You may not think much about the steel barge business, but they certainly do and they have basically a monopoly in it because it became Jones Act protected.

What that means is that international competitors are limited or not allowed to basically build that product and send it here.

That is just another example of legislation protecting you.

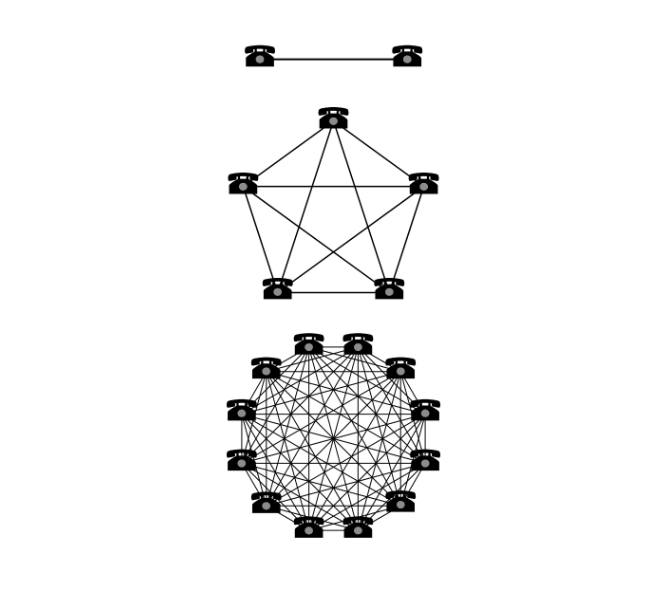

5. Network Effects.

A network effect is that the more people that use a service, the more valuable the service becomes.

Facebook, social media is a classic example of these.

eBay, Amazon, any marketplace, is another example of a network effect.

It doesn't just have to be something on the internet.

Another classic example is telephones.

The more people that get telephone numbers, the more useful the service is because you're able to call more people.

Network effects tend to be very good advantages because there's a big gets bigger effect.

You want to be on the same social network as everyone else is on.

You want to be on the same marketplace selling your product as all the other customers are on.

So, it tends to mean that scale begets even more scale.

6. Execution.

There are a lot of businesses that as they stumble along, they figure stuff out.

They may not patent it, but they're figuring out how to produce something more effectively.

They're building systems internally that allow them to produce something at a much higher level than competitors do.

Tesla, for example, has figured out a lot in the process of building electric cars from scratch that teaches them how to do that better than others.

When Ford tries it or GM tries it, even though they have a big internal combustion engine vehicle business, it didn't help them that much with electric vehicles because there's a totally new “know-how” that you need to know how to do.

The same thing can happen even at a company like Starbucks.

There could be certain ways that you make the drink in a certain order or timing on when to add certain items, so it doesn’t ruin the product.

A lot of restaurants have these little secrets that help make the product better.

But these exist in all sorts of different businesses, things that aren't obvious until you yourself try to go into business and mimic it.

And that is really important.

One of the reasons why there are businesses out there that don't seem to have very strong competitive advantages, but still continue to out execute year after year is because of their execution and internal know-how.

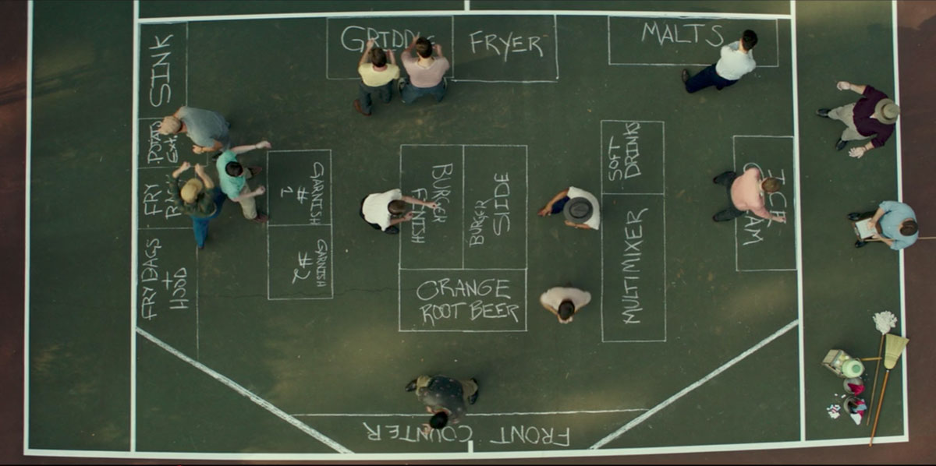

In fact, most businesses actually start in this level where there is no clear winner.

They're just a startup entering the business and they're trying to provide more and more value for their customers and execute, and they're learning more about how to say, make hamburgers more efficiently.

They don't have any brand.

McDonald's didn't have any brand when it started.

It was just really good at executing.

It was learning how do we make hamburgers in 40 seconds, 30 seconds?

And they kept pushing that limit to make the hamburgers quicker and quicker and more effective.

And all of these little things in their operation, from where they store the meat, how they have the production line layout, how they have the store layout, they're learning all of these things and over time, created a very consistent service, which translated to a good brand, which translated to everyone knowing what McDonald's was.

So, a lot of businesses actually start in this area of just execution mattering most, and so don't dismiss a company because it doesn't have all these other competitive advantages figured out.

Now, maybe that is a riskier way to invest before a very clear moat is sort of present, but it also could lead to more outsized returns over time.

Applying This Framework.

At the end of the day, the Create, Capture, Protect framework is not just a checklist, it's a way of thinking about businesses that cuts through the noise and gets to the heart of what makes a great long-term investment.

Every business you evaluate should pass through all three lenses.

Ask yourself, “Is this company genuinely making people's lives better or solving a real problem?”

If so, does it have a proven or plausible way to monetize that value?

And critically, once it's monetizing, what stops a well-funded competitor from walking in and taking that away?

The businesses that we know today (Coca-Cola, Moody’s, Costco, Amazon, McDonald’s) have found a way to create value, capture a portion of the value they created, and protect that value from competitors.

In contrast, the airlines and frozen yogurt chains for example, failed at one of the three.

What makes this framework powerful is that it also sharpens your timing as an investor.

A company in the 'creating value but not yet capturing it' stage ,like early Facebook or today's AI companies, can be an extraordinary opportunity if you have conviction that monetization is coming.

But it can also be a trap if that monetization never materializes.

The investors who win are the ones who can see around that corner.

So the next time you're evaluating a stock, don't just ask 'is this a good company?'

Ask the harder questions: Is it creating real value? Is it capturing a meaningful piece of that value? And does it have a moat to protect that value for years to come?

If the answer to all three is a confident yes, you may just have found the kind of business worth holding onto for a very long time.

For more on the Create, Capture, Protect Framework, check out the video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.