How to Protect Your Portfolio From Inflation (You Can’t)

Get smarter on investing, business, and personal finance in 5 minutes.

This Five Minute Money was adapted from a recent video Drew Cohen had on the topic.

Inflation is very misunderstood by investors.

It’s not just beginning investors, but also prominent hedge fund managers like Ray Dalio, who proclaimed that “cash is trash” because of inflation.

He’s right… except only on a longer-term time horizon.

In the short run, the best asset class to actually own when inflation kicks off is cash.

This may sound paradoxical, except that what we first see happens when inflation kicks off is that central banks usually increase interest rates, and as a result, asset prices fall.

We saw this beautifully in 2022, where the Fed increased rates to 5.25-5.5% at peak, while the tech-focused index, QQQ, fell -35% from peak, and the S&P 500 also fell -25%.

It wasn’t just stocks that fell, even gold was down -14%.

Bitcoin too didn’t fare any better, down over -70%.

Bonds, which are thought to be a safer place to invest, didn’t do well also.

A 10-year bond was down -10-20%, and a 30-year bond was down -30-40%, as interest rates increased.

While investors who fled from their cash in order to avoid the 6.5% inflation rate, thinking that would be weighing on their purchasing power, instead found themselves in assets that fell much more than that.

That is because in market sell-offs, everything that is liquid tends to be correlated.

In this week’s Five Minute Money, we will cover how an investor can position their portfolio for higher inflation as well as potentially higher interest rates.

The Fear of Higher Inflation and Why Cash Isn’t Trash.

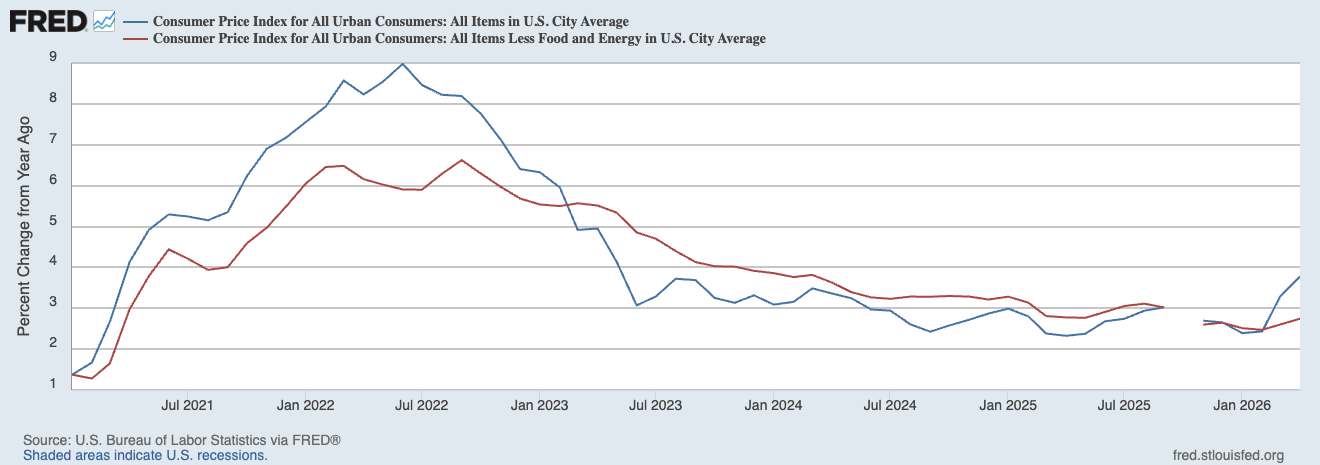

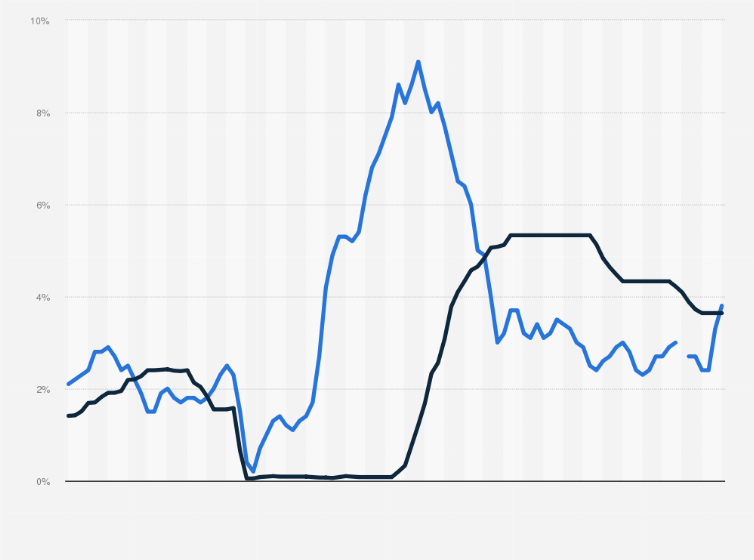

The CPI index recently increased to 3.8% from 3.3%, while Core CPI increased to 2.8% from 2.6%.

The difference between the two, is that Core CPI removes energy and food costs because they are too volatile.

This makes little sense to remove it out to just have a cleaner number because if you are human, food and energy costs are going to be very important expenses in your everyday life.

Energy is an important input cost into all sorts of different things that you will buy too.

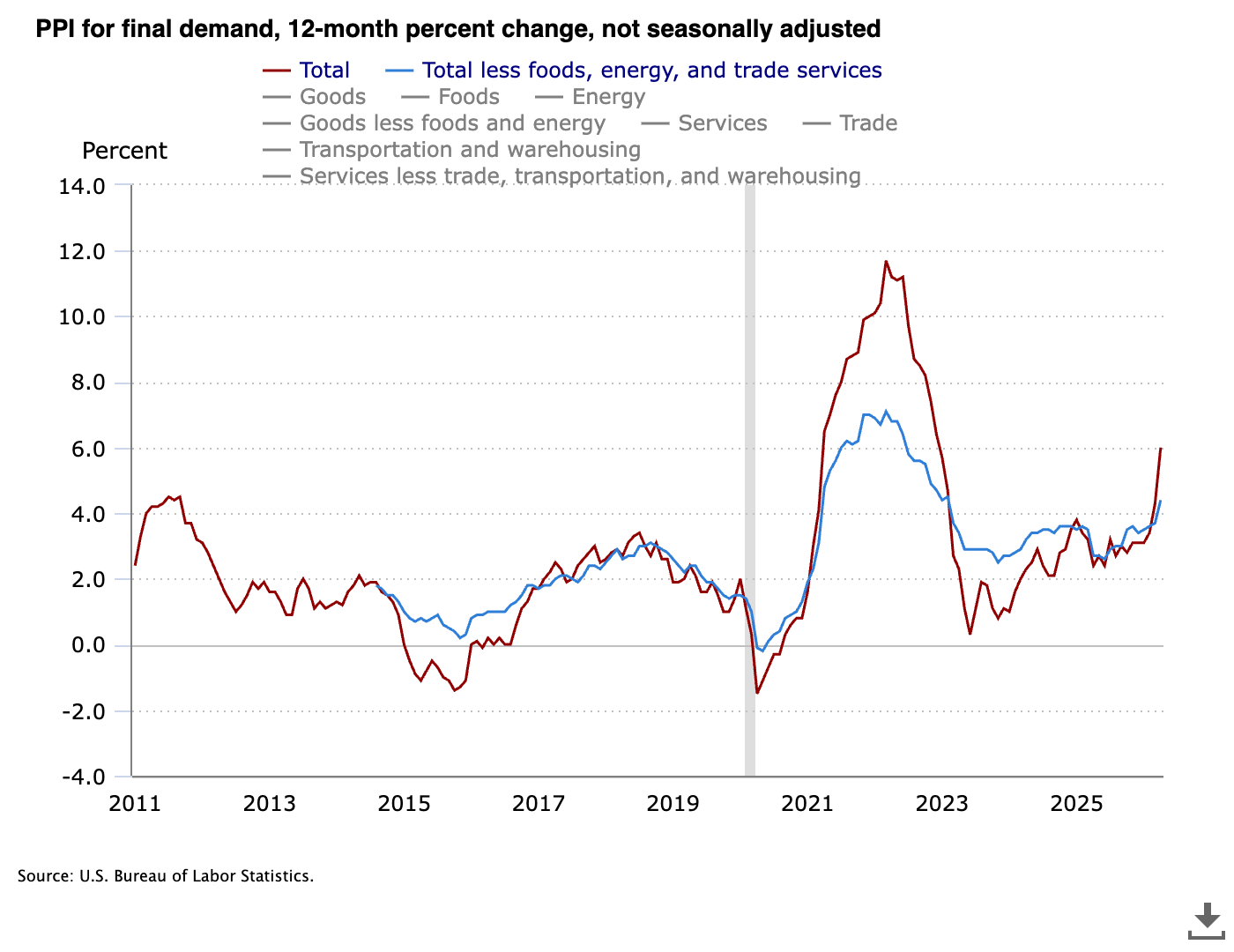

Another important inflation measure that we can look at is called the Producer Price Index (PPI).

This is basically the price that businesses sell stuff at.

PPI is known to be a leading indicator because there tends to be a lag between prices increasing and it showing up in the prices that consumers pay.

Having PPI increasing is actually more concerning than the CPI itself, and recently, it increased from 1.4% from 0.7%, which was the largest gain since March 2022 when inflation just started to pick up.

This increase has sparked new concerns that this could start a new cycle of inflation that the Fed will have to fight with higher interest rates, and with the PPI annualized at 6%, the concern is that it will eventually lead to higher prices for consumers as well.

One point that I want to emphasize is that just because you have a lot of cash, it doesn’t mean you actually experience inflation unless you spend that.

For example, let’s say you have $100,000 sitting in cash and you’re seeing inflation rates are going up to 6%.

You’re hearing people like Ray Dalio say, “Cash is trash and it’s going to eat away at your purchasing power!”

So you are worried about holding cash and as a result you went and bought a bunch of different financial assets that you thought would protect you against inflation.

The actual inflation you experienced may have been relatively minimal because if you were spending $100,000 a year and you experience 10% inflation for example, that’s only a $10,000 increase in your expenses.

If you had this $100,000 in cash and you put it in financial assets and hoped that could make up for that 10% difference, instead what you would experienced was a fall in all of these assets that you bought as we mentioned earlier.

This is because when interest rates increased and repriced, all these financial assets were repriced lower.

So in the short term, the desire to run away from cash actually had the opposite effect of increasing your purchasing power, it actually decreased it.

While it’s generally true that cash over a 10-20 year time horizon, it’s a bad thing for an investor to hold cash, but in the short-term you are going to still have some expenses and having cash as a hedge not really against inflation, but the higher interest rates that could come alongside that is a totally okay thing to do.

Having 9-12 months of fixed expenses in cash is not the worst thing in the world in an inflationary environment, because as we have seen using the prior example, cash might have been actually the best thing to hold on a 1-year timeframe which is paradoxical and not what you would’ve expected.

Now, the scary thing about what is going on today is we are seeing inflation kick off alongside an increase in energy prices.

Since energy is a large input cost in everything, this means an increase in prices across the board.

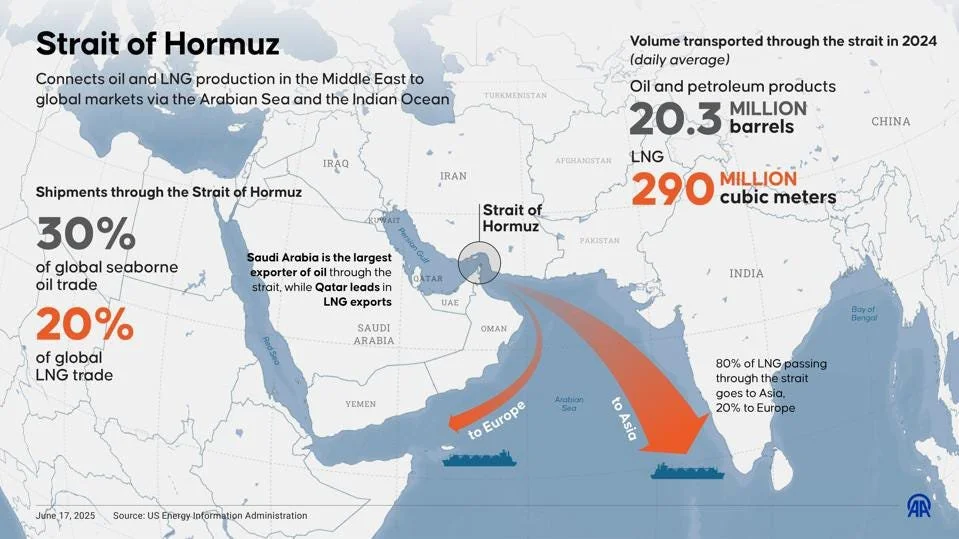

With the Straight of Hormuz closed, about ~20% of the global oil supply is sitting on the sidelines, which has led an increase in oil prices.

The longer this distortion goes on, the more it’s going to impact oil prices and consumer prices in general.

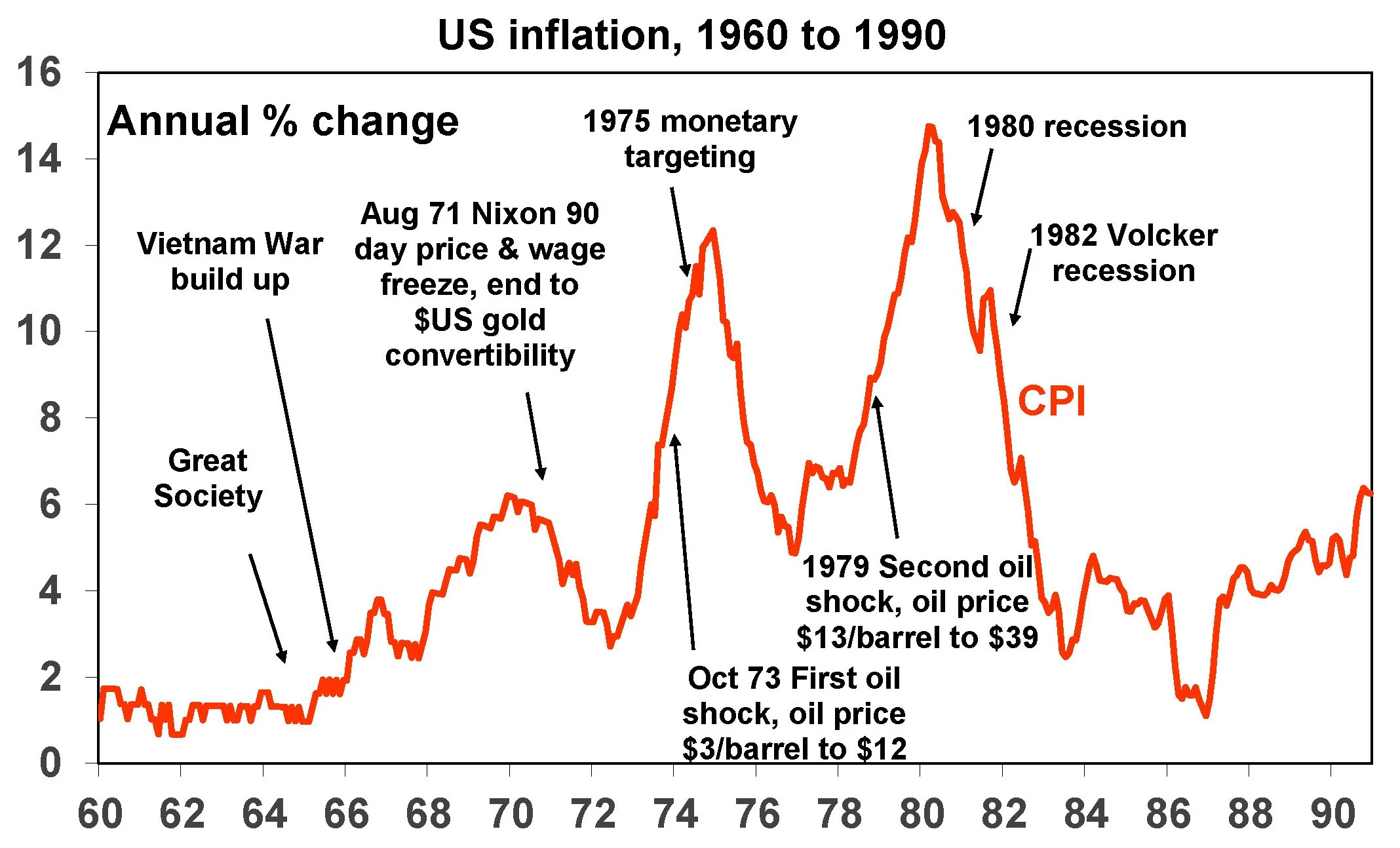

That is concerning because if we look back at the last period where we had very high inflation in the 1970s, there was an energy crisis.

During that time, inflation went up to the high teens alongside oil prices increasing several hundred percent.

The fear for an investor is that there is a 1970s era stagflation, where the stock market is flat for a decade with very violent drawdowns throughout the period.

The more concerning thing for an individual is the decrease in purchasing power as inflation continues to increase.

Now, there are different potential outcomes for an investor that you have to balance, and it’s very hard to predict macroeconomic activity, so how should you structure your portfolio to protect against the risk of inflation?

I’m going to break down each asset class from equities to real estate and explain how each performs during inflationary environments.

How Higher Interest Rates Affect Stock Returns.

When it comes to stocks, the biggest risk is not inflation, it is the higher interest rates that correspond with higher inflation.

This is because when interest rates increase, stocks tend to do worse since an investor is discounting cash flows into the future at higher rates, which decreases valuations.

Stocks with cash flows far out in the future, those that are not profitable today and expect to generate their profits far out into the future, when interest rates increase, the cash flows that are 40 years out are going to get discounted much more than the cash flows that are 5 years out.

In contrast, a profitable company that is generating profits today and is thought to be profitable in 10 years from now, those far-out cash flows are not going to be discounted that much.

So a company that is profitable today is going to have less relative of a valuation change from a higher interest rate compared to an unprofitable company.

Yes, both will still drop in valuation because the discount rate due to higher interest rates has increased, but growth companies that are not currently profitable will go down in value more when interest rates increase.

As we saw in 2022, the companies hurt the most from high interest rates were all of these very high-flying growth stocks that were not yet profitable.

Stock Picking.

So what kind of company does better inflation?

Sorry to disappoint you, but basically none.

No one does better in inflation because inflation is very destructive to a lot of economic activity.

It’s very hard to know whether or not prices are going up because there’s a lot of demand for a product/service or it’s just input costs rising.

And at the same time, you have a lot of consumers that will struggle and so while they may be spending more in absolute, in real terms, they’re spending less.

While no one actually does better in inflation, some businesses can do better in inflation relative to others.

Businesses who do better than others are businesses that have pricing power and are capital-light.

If you have a business that has pricing power, a brand, IP, all of these things that can protect your business and help you raise pricing, that is a positive thing.

What I’m describing here is just a great company.

There’s no reason to actually look for companies that do well in inflationary environments, because it’s the same thing as just looking for what companies you want to own in all competitive environments.

The companies that are great in all competitive environments are going to tend to do better in inflationary environments as well.

So, what is a really bad business to own in an inflationary environment?

This is a business that is 1) a price taker, 2) has a commodity product, 3) doesn’t have control over its costs, 4) doesn’t have a brand name, and/or 5) has a lot of competition.

These are all characteristics of a business you would avoid, even absent of there being inflation.

For example, airlines do pretty badly in a high inflationary environment, especially when energy costs are going up because energy costs increasing means it’s very expensive to fly, which results in fewer people willing to fly.

High inflation weighs on consumer spending, which means fewer people are going to want to travel.

On top of that, when an airline needs to buy new planes, their depreciation costs are very understated because the new planes are going to be much more expensive than the old planes.

Inflation exacerbates a lot of these competitive disadvantages that makes everything look a lot worse.

That’s the reason why you want to own a great company regardless of whether there’s an inflationary environment or not.

With that said, buying a great company is a lot like building a strong ship.

A ship will go through all sorts of storms and you want to build this ship to be strong so it can with last all of these different potential storms.

Inflation is just another one of these storms.

Owning equities in general through inflation still makes the most sense, and it’s unfortunate because your returns are going to be lower.

You’re not going to do well as an investor invested in an inflationary environment compared to one that’s not.

How much lower is your return you may ask?

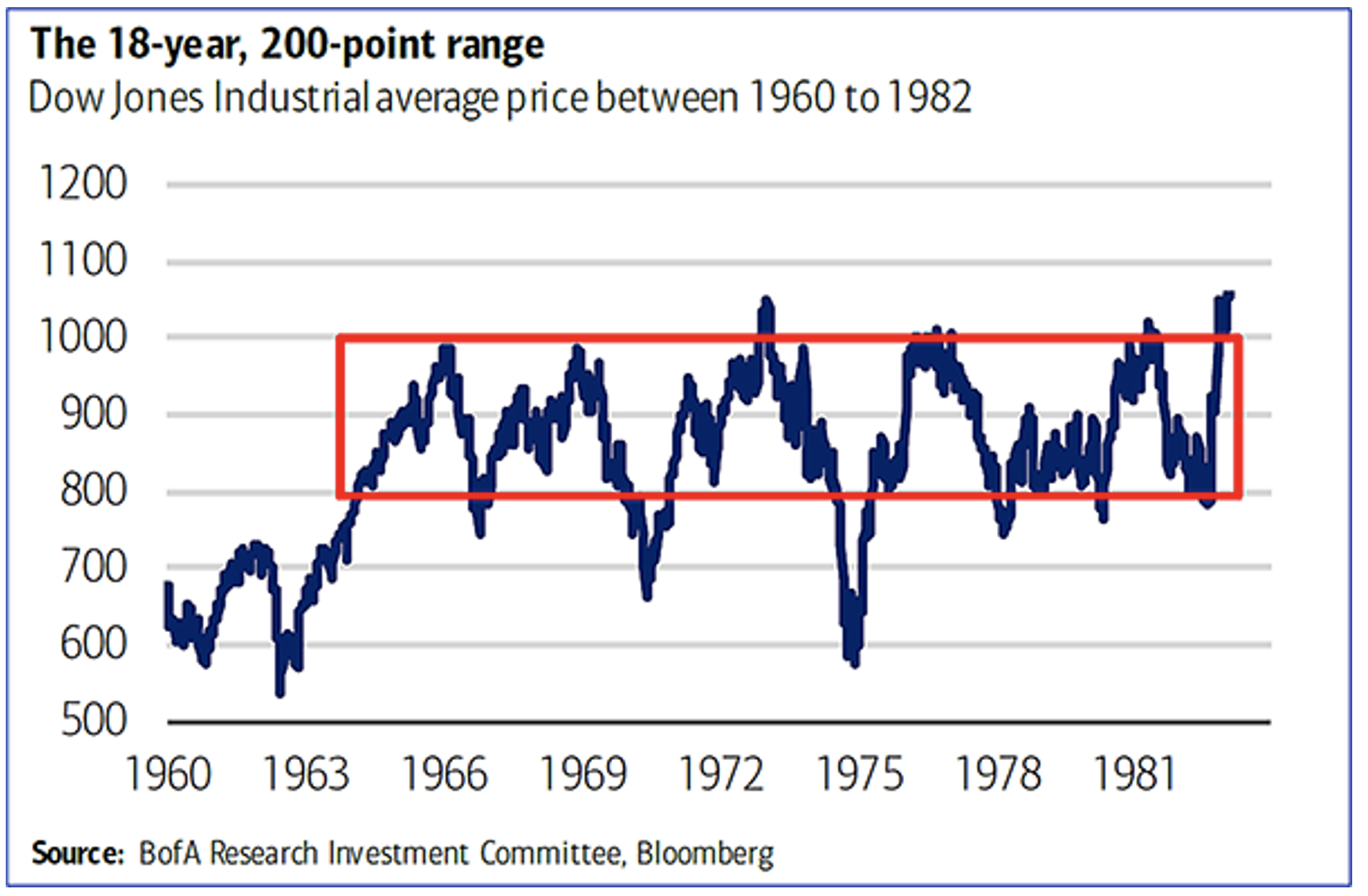

If you are looking at the 1970s, which was one of the worst inflationary periods, your real return after inflation would have been 1.5% annualized from 1970 to 1980.

There are different periods within that where you could have basically had a lost decade, where you didn’t earn anything as an investor.

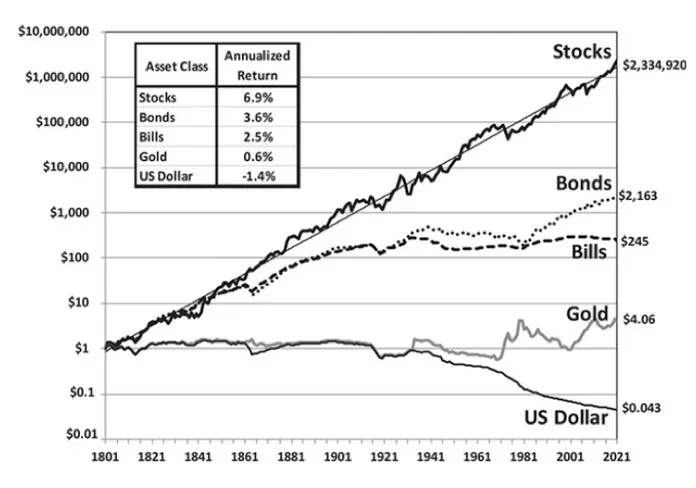

However, if you’re looking at an even longer-term horizon, we see that equities outperform all other asset classes.

What About Owning an Oil Company?

If the primary cause of inflation is going to be energy, isn’t that a good environment to own an oil company?

Yes, with one caveat.

High oil prices means that if you’re pumping up oil already and you have a business that’s existing and the fields are already developed, now you’re just making more money off of them.

The caveat, though, is that what tends to happen and why you have to research the management team is that they will take these extra profits and then go and explore new oil fields or develop new oil fields, which means the incremental money that’s being made is just getting invested back into the business.

When this happens on an industry-wide scale, you’re just increasing supply, and then inevitably it will result in prices falling again.

So that big windfall you got, it was just directed towards pushing out the capacity of the entire industry.

Now, if you looked at the 1970s inflationary period again, yes there is some data where investing in oil companies would have been a good investment over that time period, but there are two caveats to that return you have to be aware of.

The first is that, when gas prices got too expensive, Nixon actually implemented price controls.

The second is that there was a lot of nationalization of oil fields internationally.

These two factors effect those returns you might have seen at that time.

In addition, energy companies have very idiosyncratic returns because a lot of times you could have a great asset, but then the asset is getting depleted as you’re using it.

As that depletion happens, what is management doing with the money?

Are they giving it back to you or are they reinvesting?

We know a good company is one that is able to reinvest profits back into the business at high rates of return.

That is never the case with an energy company because when you’re developing a new field and you’re looking for new oil fields, you almost never know ahead of time whether or not it’s going to be a big success.

So, you could play this macro analysis game when it comes to oil prices, but I personally don’t do that.

I want to own companies that are going to do well in as many different environments, not just for one environment that I don’t know can or cannot happen.

Real Estate.

Real estate would be an ideal asset to own, however, it’s very hard to actually own the right real estate.

If you buy a physical asset and you put long-term fixed rate debt against it, and then you hit an inflationary environment, that seems good because your debt is going to be repaid in nominal dollars, which means that as inflation continues to hit, you could raise rents and the debt your paying off is less.

So if you are able to own the right real estate, have long-term fixed rate debt, and are able to increase the cash flow of that real estate by increasing rent, that is a positive to owning real estate in an inflationary environment.

The problem is that most people are not going to be able to find real estate that is actually attractively valued.

One thing to keep in mind about real estate is that when interest rates increase, the value of real estate can still go down.

If you’re buying the property yourself and are doing the math on the actual cash flows of it, you tend to not care about this as much, but if you’re invested in a REIT (Real Estate Investment Trusts), the value of the REIT drops a lot when interest rates increase.

On the topic of REITs, you have to be careful with the capital structure and how they are financing the real estate.

Do they have enough fixed rate debt?

Are they messing around with floating rate debt, so when interest rates go up it will eat into a lot of the cash flows?

Another downside to REITs is all of the fees layered on top.

And when interest rates increase and the value of the REIT decrease, the yield on a REIT could be the same as a treasury, so why mess about in a REIT that’s doing 5% while treasuries are yielding the same at 5%?

If you can go out and buy an individual property in a great location and find someone to run it for you, that would be ideal, but that is unrealistic for most people and unfortunately not so easy to do either.

Bonds.

Bonds are generally not a great thing to own in inflation but it depends exactly the bonds you’re buying, the interest rates, and what the expected inflation rate is.

If we got a lot of inflation, a bad place to park money would be a long duration bond because when interest rates increase, the longer the duration of the bond, the more the price falls.

That could really decrease your purchasing power very quickly, even if you held it to maturity and were able to get the full coupon back.

If you want to own bonds and are concerned about inflation increasing, shorter term bonds like a 3-month T-bill probably make the most sense because as interest rates increase, you could just roll those into new bonds that have the new higher interest rate.

These are considered like a cash equivalent.

If we do get 6% inflation, the Fed will probably increase interest rates to at least 5%.

In 2022, when we had 6.5% inflation and around 5% interest rates, in real terms, you are losing 1% in purchasing power, so it wasn’t the worst thing in the world especially as other financial assets adjust to the higher interest rates like stocks that fell -20%.

A year later, you could rotate into stocks if you wanted to.

This is why it’s not the worst thing in the world to own some short-term treasuries if you’re concerned about rising inflation.

In addition to short-term treasuries, there is something called TIPS or Treasury Inflation-Protected Securities.

This is a US government product that will adjust the principal for CPI.

If CPI is 3%, the principal gets adjusted upwards of 3%.

Then at maturity, you’re getting that principal back that has now been adjusted for the increase in inflation.

The thing to be aware of in TIPS is that the returns you get can vary a lot because it is based off of investors’ expectations on inflation.

Now if the market is not expecting a lot of inflation, buy you are, this could be interesting product for you because that means it’s not going to be priced like there is a lot of inflation.

But, if the market is expecting a lot of inflation, it could potentially be priced at a negative return, which is what happened a few years ago.

Another thing to be aware of for TIPS is that the returns are not good over a 10-year time horizon.

For example, for a 10-year TIPS, the real return is ~2%.

Compared to stocks, which average a real return of 6-7%, the risk/reward doesn’t seem that great.

Of course, things could be different, and maybe we get a lost decade where returns are zero.

So short-term treasuries and TIPS are fine in the short-term if you are concerned about rising inflation.

Commodities.

If oil is going up and I’m worried about it going up more, why not just own oil?

This makes sense theoretically, but in practice, it doesn’t work out that way.

There are 2 reasons why: 1) your carrying cost, which is the actual cost to implement that trade, is going to be very high, and 2) if you buy a future as a derivative, it’s more of a time-based bet.

It’s not really a long-term hedge anymore and more of a bet on commodity markets.

So, for the average investor who is trying to get inflation protection, trading commodities like oil, corn, copper etc. isn’t really appropriate because you’re buying things that are not cash flow producing.

It’s actually the opposite by costing you money to store it.

In addition, there are many macro factors that can influence the price even beyond inflation that can wash out any potential hedge benefit against inflation.

But what about gold you may ask?

Gold.

A lot of people have comfort in this idea that there’s a limited amount of gold and as a result that means it’s going to always hold its value.

The problem is the correlation between it holding its value and inflation is very tenuous.

In 2021-2023, when inflation started to pick up and at its peak, gold was actually down -14%.

In fact, gold never started going up until the beginning of 2024.

The increase in gold over the past few years didn’t have much to do with inflation we saw in the U.S.

One narrative as to why gold has been on the rise is the de-dollarization by China, India, and other BRICS nations buying more gold and wanting to own less dollars.

Another narrative is new retail enthusiasm to own gold.

Whatever the reason is, it did not correspond to the increase in inflation.

But what owning gold as a long term hedge to inflation?

When doing some research, there was a figure that stated that gold had 7-8% nominal returns since 1971.

That was better than I thought honestly.

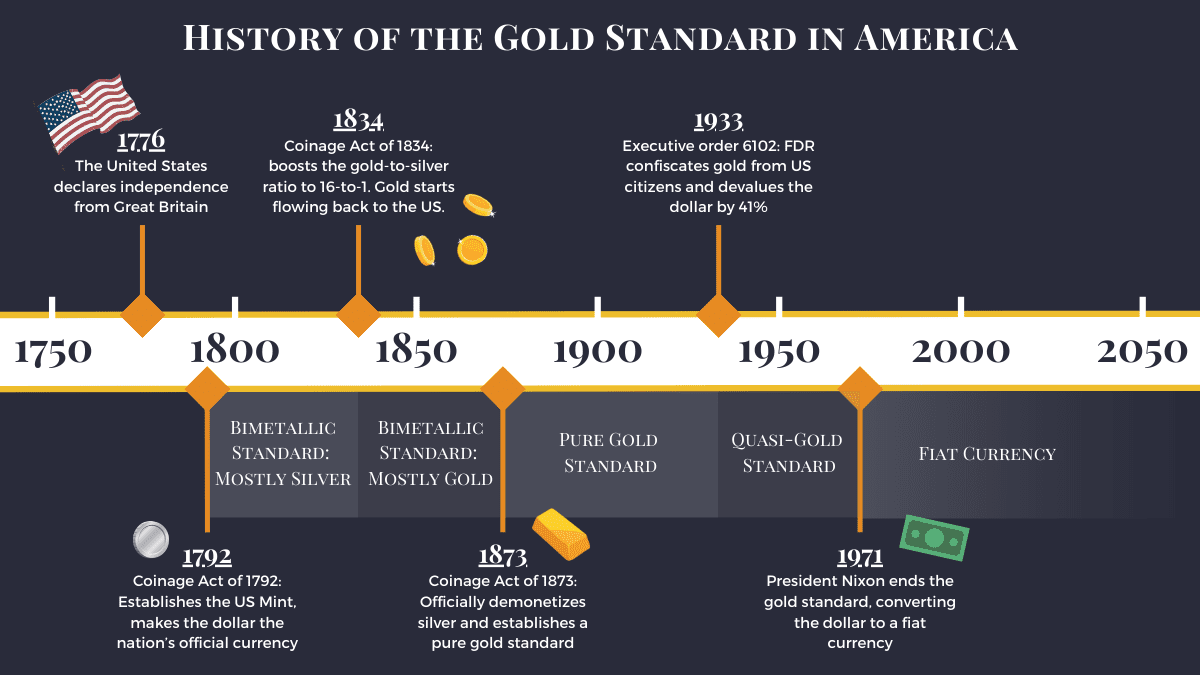

However, that’s an interesting date they chose in 1971 because, the U.S. was on a gold standard prior to that and the price of gold was actually fixed at $35.

After Nixon took the U.S. off the gold standard in 1971, within a couple of years, gold went from $35 to $200 and by the end of the decade it was ~$800.

So a lot of the price appreciation from gold was because it was so artificially depressed for so long as a result of the Bretton Woods systems and the US being on the gold standard.

If you were to back that out, you would be looking at a different return profile.

But over a very long time horizon, stocks tend to be a good investment too and tend to be better than gold.

Plus owning gold seems more speculative because let’s say you buy a bar of gold today, at the end of 40 years, you still own that same bar of gold.

If you buy a business like Apple, well 40 years later, they went from selling a couple million computers to selling a couple billion iPhones and have multiple other business lines.

They were able to create value for consumers and build value in that business over time.

That to me makes more sense to own for something over a very long period of time and what I would want my clients to own is something that’s creating value.

Ultimately, there are two games an investor can play.

You are either 1) trying to buy an asset and make money off of the increase in value and productivity of that asset, or 2) you’re trying to make money by buying an asset and hoping to sell it to someone at a higher price.

When you’re buying gold or silver, and it’s similar with Bitcoin, there’s no way you could really value it.

It’s going to be worth what people are willing to pay for it right?

I think an easier game to play is to buy a business where I know people love the product or service and they are able to charge for it and can reinvest that money back into the business on my behalf and turn it into more money.

Yes, it’s not always easy finding a great company that is able to do that, but you could also just buy the entire index.

You don’t need to pick a specific stock.

Summary.

If inflation kicks off, the first thing we are going to see is very high interest rates and a lot of asset prices are going to go down as a result.

I don’t think it’s a terrible thing to hold some cash on the side in short-term treasuries if you are concerned with inflation.

If you can go out and buy an individual real estate property and you feel qualified to judge all of the aspects of where it’s located and find someone to help run it for you, and the numbers make sense for you, that’s not a terrible way to go. I know that’s not realistic for most people though.

If you want to own bonds, probably stay away from longer duration ones because they could really change in valuation a lot as interest rates increase.

If you are going to live off the cash flows and hold the bond to maturity and are worried about inflation, TIPS aren’t a terrible way to go, it’s probably not going to be necessary for most people, though.

You can own gold if it helps you have peace of mind, but understand it’s speculation of where that price is going to be in the future. The same goes for Bitcoin.

With that said, all of these decisions really should be made in the context of how much money you’re saving, how much money you can actually invest for the long term versus what your shorter term capital needs are, and you should talk to a financial advisor to figure all that out if you’re not sure where to place your dollars to protect against from inflation.

It is important to keep in mind too though that inflation is only one potential market environment that can happen and you want to manage your money for a broad variety of different potential outcomes.

For more on how to protect your portfolio from inflation, check out the video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.