Intuit Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

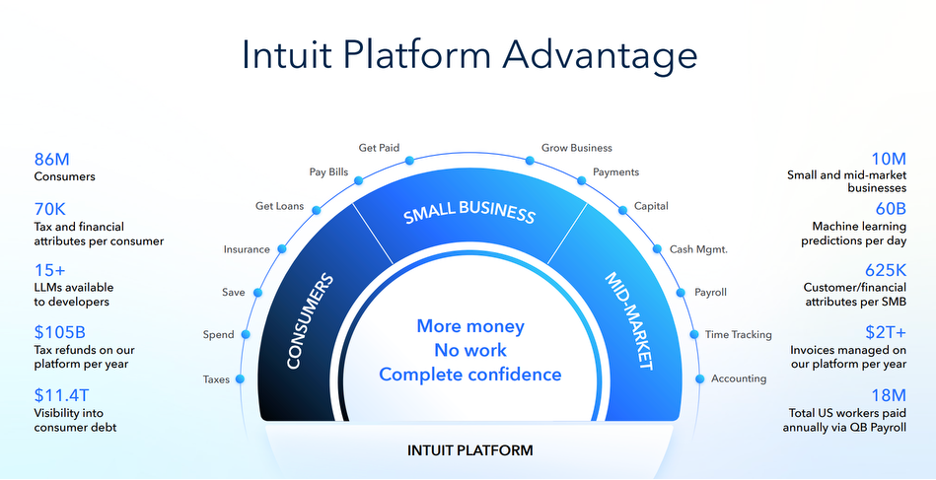

Intuit’s QuickBooks is a staple for over 10 million small businesses.

Their TurboTax and CreditKarma apps have 86 million consumers.

They have grown revenues at a 15% CAGR over the past decade…

And revenue growth has recently reaccelerated

They boost 81% gross profit margins, 27% operating margins, and a 20% ROIC

But their core products are essentially bookkeeping and tax filing…

Use cases AI is particularly good at.

Their stock was down over 50% from peak of $807 to as low as $360 ($480 as of this writing).

Are these stellar financials at risk of disruption?

Or is Intuit’s AI strategy going to actually improve their product and accelerate their growth?

We cover it all in this week’s Five Minute Money, starting with an overview of the business.

Business.

They have two main segments: Global Business Solutions and Consumer.

Global Business Solutions.

The customers here are small businesses, mid-market businesses, and the accountants/bookkeepers who help run them.

This segment is built around:

• QuickBooks

• Intuit Enterprise Suite

• Mailchimp.

QuickBooks

This is Intuit’s core small business operating system.

Businesses rely on them for:

Accounting / General Ledger – QuickBooks helps businesses keep books, categorize transactions, reconcile accounts, and generate financial statements.

Invoicing / Receivables – Businesses can send invoices, track who has paid, and manage cash coming in.

Payroll / Workforce Management – Through QuickBooks Payroll and QuickBooks Time, Intuit helps businesses run payroll, track employee hours, and manage parts of workforce administration.

Payments / Bill Pay / Money Movement – QuickBooks also handles merchant payment processing and bill pay, meaning Intuit is not just recording financial activity but increasingly participating in it.

Financing / Cash Flow Support – Through QuickBooks Capital and related offerings, Intuit helps eligible businesses access financing.

QuickBooks Live – This is Intuit’s bookkeeping-assisted layer on top of software. This adds a human support network to their software.

Live Bookkeeping Help – Businesses can get human help managing and cleaning up books.

Interestingly, they still support QuickBooks Desktop, which is their legacy architecture and despite QuickBooks Online being well over a decade old, still 22% of revenues come from the legacy product.

The desktop version still has more functionality than the online version as the web based app would be too slow to load. That is why they have supported Desktop for so long, but Intuit Enterprise could be the solution to end the Desktop app without losing these users.

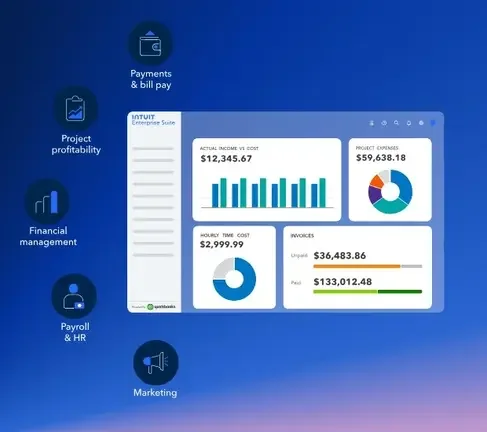

Intuit Enterprise Suite

This is Intuit’s more advanced product for larger and more complex customers. In the past business’s “graduated” out of QuickBooks as they got more complex, so the hope is that this offering can keep those businesses from leaking out of their system.

They have a leg-up in winning those customers too as migrating from QuickBooks Online to Intuit Enterprise Switch is seamless as all of your data and audit trails are already on the platform.

This suite adds:

Multi-Entity Financial Management – It is designed for businesses that are getting too complex for basic SMB tools and need more scale, controls, and visibility.

Integrated Business Operations – It expands beyond simple bookkeeping toward broader business management workflows.

Mailchimp

This product comes from a $12 billion acquisition in 2021.

It is focused on:

Email Marketing – Businesses can create and send campaigns.

Marketing Automation – Mailchimp automates follow-ups, reminders, and customer journeys.

Audience / Customer Engagement Tools – It helps businesses retain customers and drive repeat engagement.

This is a competitive business though and competitors have outpaced them since the acquisition, especially in ecommerce, which is one of the most important verticals. Their focus on SMBs hasn’t been that helpful for Mailchimp as they are more price sensitive and churn has been an issue.

In 4Q25 they reported that revenues in this segment contracted. They are hoping this segment can return to growth after 2026 by integrating it more with QuickBooks and focusing on middle market.

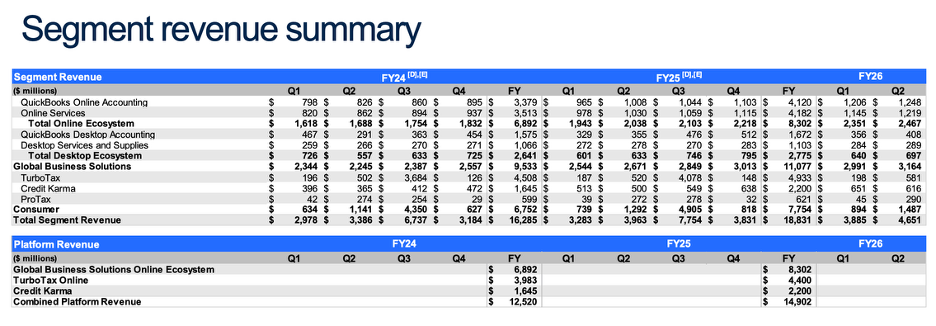

In total this segment is 59% of revenues and grew 18% y/y. They split this segment up further between the online ecosystem, which grew 20% and the desktop ecosystem which grew 10%.

Consumer.

Second segment is Consumer.

This segment includes TurboTax, Credit Karma, and ProTax.

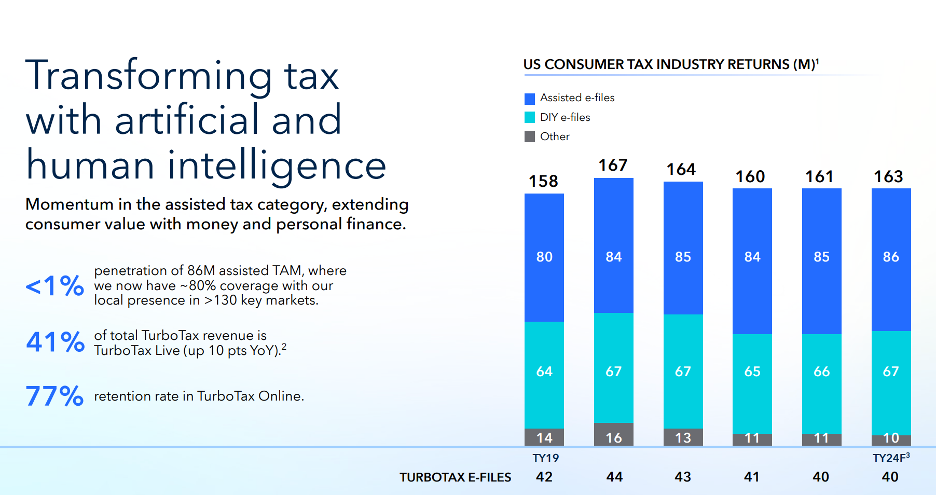

TurboTax.

This is Intuit’s consumer tax filing product.

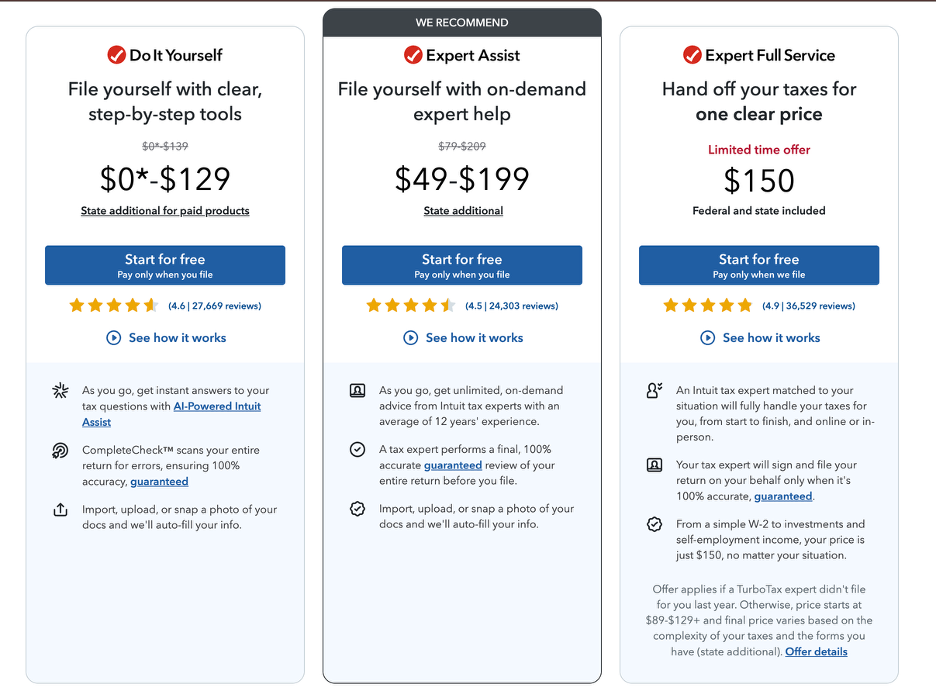

DIY Tax Preparation – Consumers can prepare and file taxes themselves through online and desktop software.

Assisted Tax Filing – TurboTax Expert Assist lets users get help from a human expert while still doing parts of the return themselves.

Full-Service Tax Filing – TurboTax Full Service lets the customer hand off much more of the process.

Electronic Filing / Refund-Related Services – Intuit monetizes e-filing and related services around the return experience, including refund-adjacent products.

Credit Karma.

This is Intuit’s personal finance and financial-product marketplace.

Credit Monitoring / Visibility – Users can check credit scores

Credit Card Marketplace –recommends credit cards (monetizes via affiliate fees)

Personal Loan Marketplace – It also matches users with personal loan offerings

Insurance / Mortgage Lead Generation

Consumer Money Tools

Their leg up here is that they can pull a consumer’s actual credit file to better match them to different financial offerings (and this also be a better quality lead for the financial institutions).

They shut down the popular money management app Mint and rolled that functionality into Credit Karma. Users like to track their credit scores in their too as well as a dashboard that integrates into all of their finances.

Now as they are moving to unifying these three apps more, Credit Karma is becoming lead gen for TurboTax and management noted that it has led to more early season tax growth.

ProTax.

This is Intuit’s tax software for professional accountants and tax preparers.

Professional Tax Prep Software – Intuit’s main offerings here are Lacerte, ProSeries, ProConnect Tax Online, ProFile, and ProTax Online.

Each product is for a different level of complexity.

The accounting industry is not a big growth industry and switching costs are high so market share doesn’t move much.

This is a slower growing business at 7% y/y and expected to slow to 2-3%.

Below you can see the segment breakdown.

They have a lot of seasonality that comes in 3Q because of TurboTax, which generates $4 billion that quarter versus 1/5th of that generated cumulatively the other 3 quarters.

This isn’t exactly an issue though because tax season comes ever year…

Competition.

For Quickbooks competition comes from cloud-based competitor Xero who has a stronger presence internationally, followed by Sage. Freshbooks, and Soho books are competition too, but compete more at the lower end for the simplest of use cases.

QuickBooks market share in the US is estimated to be around 65%.

When moving up market in accounting (Intuit Enterprise) it is Oracle NetSuite and Sage Intacct.

For specific QuickBooks products like Payroll there is another set of competition, including Gusto, ADP, and Paychex.

For QuickBooks Payments and Bill Pay it is Square, Stripe, PayPal and Xero (who acquired Melio).

Mailchimp has many competitors including Klaviyo, HubSpot Marketing, Constant Contact, and Brevo. Then there is also Kit (formerly called ConvertKit), Beehive, Ghost, and Substack for more newsletter type communications.

Mailchimp’s market share was estimated to be as high as 70% at one point, but has slipped to around 50%.

TurboTax’s main competitor is H&R Block, but Cash App Taxes (Square) could also take share at the low end of the market for individual filers. For the simplest filings there is also TaxAct and FreeTaxUSA that compete on cost (FreeTaxUSA doesn’t charge for Federal returns, but will charge for state and both try to upsell with other services).

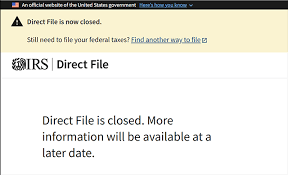

The U.S. Government rolling out a direct, free filing program is also a risk, but after a launching a couple years ago this has been scrapped.

TurboTax is still the giant in the room with an estimated ~60% market share. And while there are cheaper options, it’s not that expensive in absolute.

Credit Karma competes with NerdWallet and Experian, as well as LendingTree and Credit Sesame. SoFI and Chime also offer comprehensive dashboards.

On the ProTax side there is Thomson Reuters UltraTax CS who is a large player, as well as Drake and Walter Kluwer.

All in all, the competitive landscape seems largely set.

Yes, there is always a risk that a competitor can get aggressive with pricing , but it is hard to see it being a meaningful drag to Intuit in the current competitive landscape.

The biggest risk to TurboTax was really the U.S. Government rolling out a free service—and they did—but then discontinued it on low usage (and ample lobbying). The IRS Direct File program will not be available for the 2026 tax season and is unlikely to be restarted again—at least under the current administration.

There is likely more pricing pressure in this business because every time a consumer does their taxes they can compare pricing, but consumers also want to trust their taxes are done right and having the biggest brand here helps convey trust.

The biggest threat to QuickBooks (baring AI which we will touch on next) is really companies graduating from their software. Intuit Enterprise Suite has a good chance of keeping them on their platform.

Credit Karma is a more competitive business to be sure, but their advantage with 140 million registered accounts they have credit info on helps give consumers more accurate options. They still compete on top of funnel with search key words, but the ability to cross-sell TurboTax and have more accurate leads also means their LTVs are higher here. (The AI risk here seems more formidable here, noted below).

But in terms of the existing competition, Intuit seems pretty well insulated. Maybe competitors can weigh on their growth, but it is hard to see anything being too material from existing competitors.

AI Risk.

There are broadly two AI risks here.

1) AI- Native Apps and Pricing pressure

2) AI Agents

The first is the risk that new apps that are AI-Native are able to do a lot of the functionality of QuickBooks and TurboTax and charge less of a premium.

It is key to note that there is already competition in this space that undercuts them, so this new upcomer would have to have a very aggressive go to market strategy and charge much less.

The consumer and SMB markets are different than enterprises where cost cuts are unlikely to sway them.

Consumers don’t have lock in on TurboTax and there is always new SMBs, which creates more of an opportunity to steal share.

While it is unlikely this new AI-native start-up can offer anything materially better product-wise, the competition could weigh on their ability to grow or raise pricing.

The second risk is AI Agents.

There are different versions of this risk because AI agents are already incorporated into Intuit’s products.

The worst case scenario is there is a general AI agent that reached some level of super intelligence and is able to do extremely complex tasks like filling out tax forms and filing them on behalf of the users.

In this scenario the user just tells the AI what to and maybe uploads some documents and it takes care of everything for you. There is no need for software because the AI was smart enough to do it all for you.

A similar thing could happen with a small business. There is no need for a software program that does reconciliation because the AI agent can do it in the background. If you have questions or want a report, you just ask it to reproduce it.

These scenarios assume “AGI” or artificial general intelligence that is able to reason better than a human. There is much debate if we will get there anytime soon. Many scientists do not think AGI is possible using existing LLM technologies.

It is worth noting this is a huge risks for most businesses (and people), so Intuit is not alone here. Now because they focus on the lower end of the market and consumers, that seems to be an area that would be more likely to experiment with technology than enterprises (at least initially).

Absent of that tail risk, most of the AI risks seem pretty manageable for Intuit.

They are focused on making the platform less “DIY” and more “done for you”.

They have AI agents for Payments, Accounting, Customer Service, etc., that are all actively doing the work on behalf of the client.

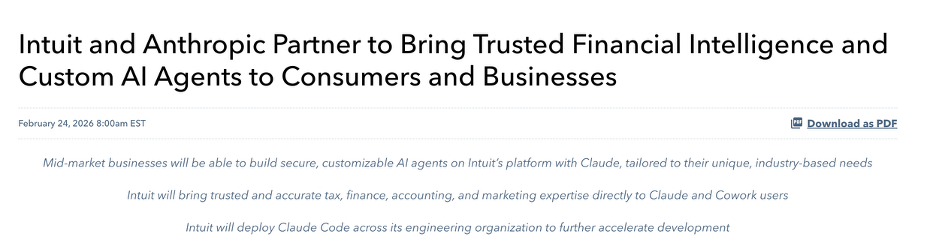

They have AI partnerships with OpenAI and Anthropic whose LLMs they will leverage.

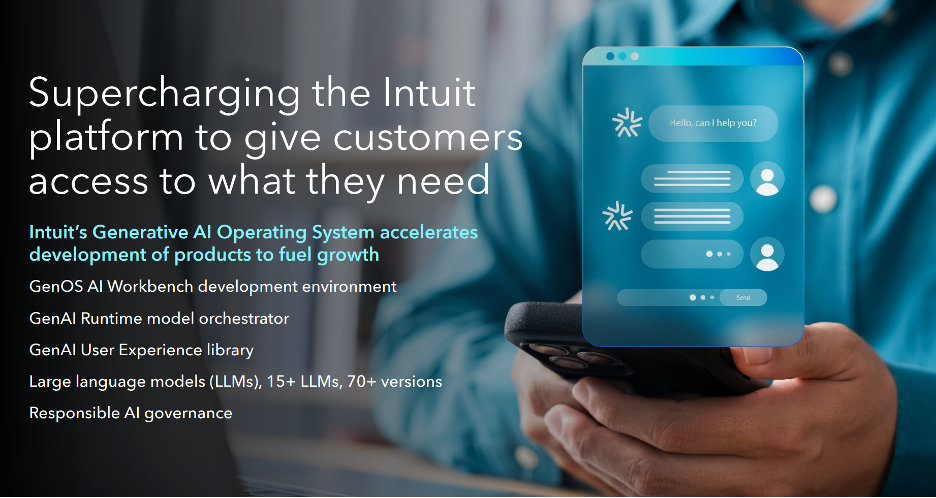

Intuit has GenOS.

This is a proprietary infrastructure layer and development platform that sits on top of the LLMs.

It allows Intuit’s engineers to create AI products much quicker and ties into GenSRF (safety, risk, fraud) to check the outputs are compliance approved and are not hallucinating.

This allows them to bring AI finished products, branded under Intuit Assist, to customer quickly.

Since rolling out AI agents, over 3 million customers have used them with repeat engagement rates of 85%.

And AI is able to automate 93% of the tax process already.

While they lean more into AI, they are simultaneously emphasizing the human element.

Users have the ability to contact humans for live support with “TurboTax Assist”. An on-demand person can video chat with you for help.

Or there is also TurboTax Expert Full Assistant who will do everything for you.

And they are even rolling out their own TurboTax stores.

The idea is that people still feel more comfortable with a human overlooking their taxes, especially if they are complicated.

TurboTax stores allows clients to drop off documents, have the AI do all the hard work, then get a human to sign off on it.

They want to move from just being the “System of Record”, which is a sticky and sought after position in the software stack, to also being a “System of Intelligence”

So far, AI has already allowed them to upsell customers and help them improve margins.

But what does an investor need to assume here for success?

Valuation.

At a stock price of $480, Intuit trades at a market cap of $129 billion and EV of $133 billion.

LTM revenues were $20.1 billion and operating income was $5.4 billion for a 27% operating margin.

This puts them at a 31x EV/ NOPAT multiple.

For 2026 they guided to 12-13% revenue growth and 17-19% operating income growth.

Achieving that would put them at 26x forward earnings.

If they can continue to grow mid-teens for several years, a multiple of 30x+ could be fair.

They have 3 growth engines to continue to support the business:

1) Done for you experiences

Payroll, cash flow management, taxes are all done for you. This makes the product better and gives them pricing power.

2) Money is everything.

Shifting to bring on platform more of the actual movement of money. Starting with instant refunds, but only for customers who set up Credit Karma bank accounts (they are not a bank but partner).

Working capital loans to help factor accounts payable for Quickbooks a customers.

This improves their competitive position and gives them a cross sell opportunity.

However, worth noting banking is a much more competitive space.

3) Mid-market.

Transitioning with customers as they move up market and become bigger businesses. This expands their TAM and winning this business is more valuable than the typical SMB.

They repurchased $2.8 billion of stock in the past 6 months (this is offset by about $1 billion in SBC) and have an authorization to purchase up to $3.5 billion. They also issued a dividend that comes out to a ~1.1% yield.

With good capital allocation and success with their AI efforts, they may be able to continue to grow double digits for a long time with operating margin expansion, a phenomenal outcome for investors.

Or it could end up that new and aggressive AI-start ups weigh on their growth and ability to increase prices.

Or maybe AGI is successful, and the worst existential risk is realized.

It is up to an investor to decide what they are comfortable assuming and whether the rewards they perceive are worth the risks.

For more on Intuit, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.