Salesforce Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

In 1999, Marc Benioff left Oracle with a mission:

The End of Software.

What he meant was no more huge upfront licensing fees, no on-premise servers required, and no more physical disks.

Salesforce would deliver their software over the internet.

Now today, the “End of Software” has a very different meaning.

Investors are worried that software is literally going to disappear…

Or at the very least become much less important in a world of “AI Agents”.

While no software stock has been unscathed by this fear…

Salesforce isn’t just any software stock.

They are THE posterchild of Software, having completed over 70 large software acquisitions and boasting among most software revenue among any of the pure-play SaaS players at ~$40 billion annually.

They are highly embedded in organizations workflows process, offering the highly important and sticky CRM system, as well as a slew of other tools from sales to marketing and commerce.

If Salesforce is at risk than what hopes to other SaaS players have?

With the stock down ~50% from all-time highs...

Could this be an opportunity to own one of the most prominent software companies….

Or a trap?

We explore all of this in this week’s Five Minute Money!

Business.

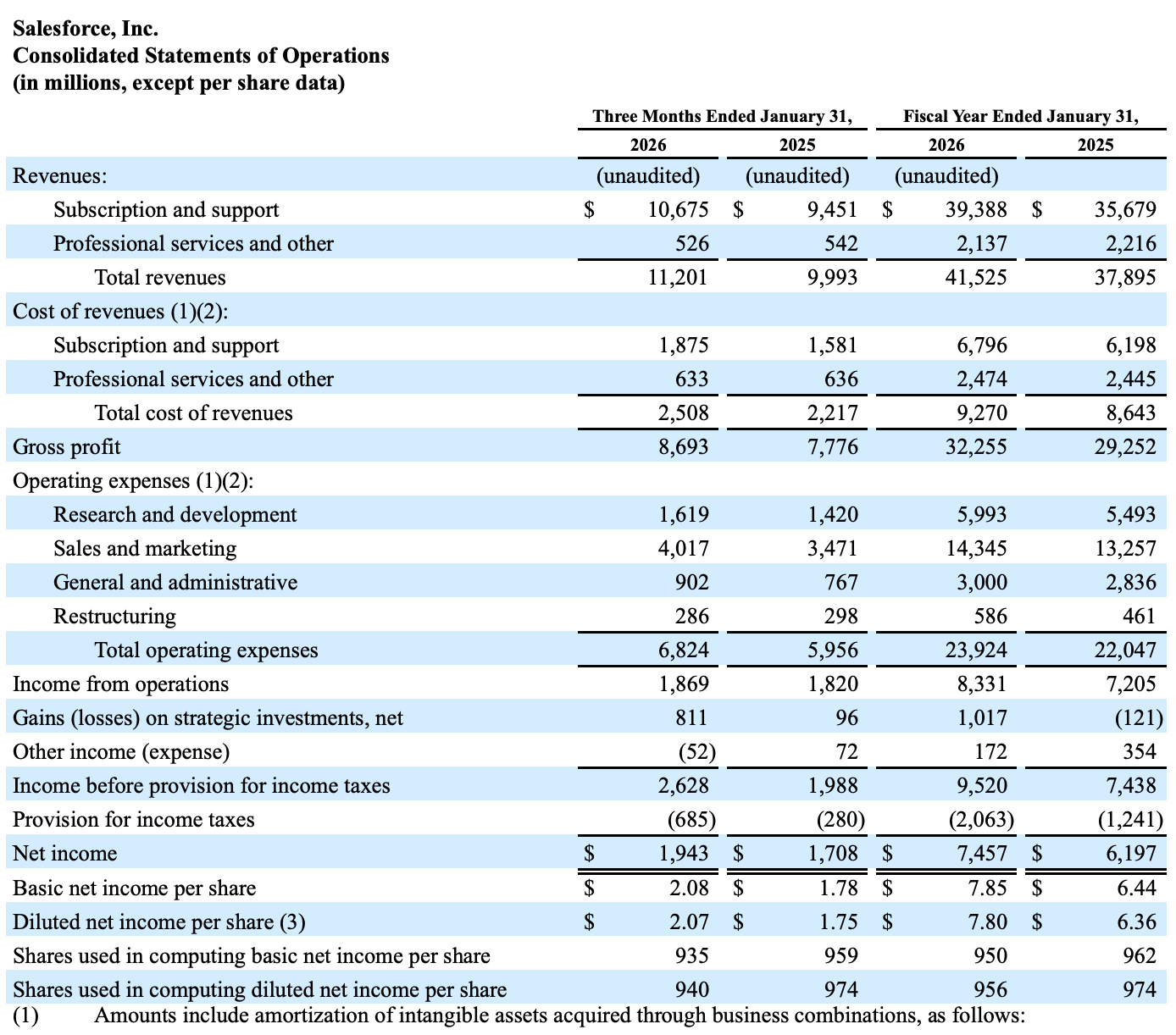

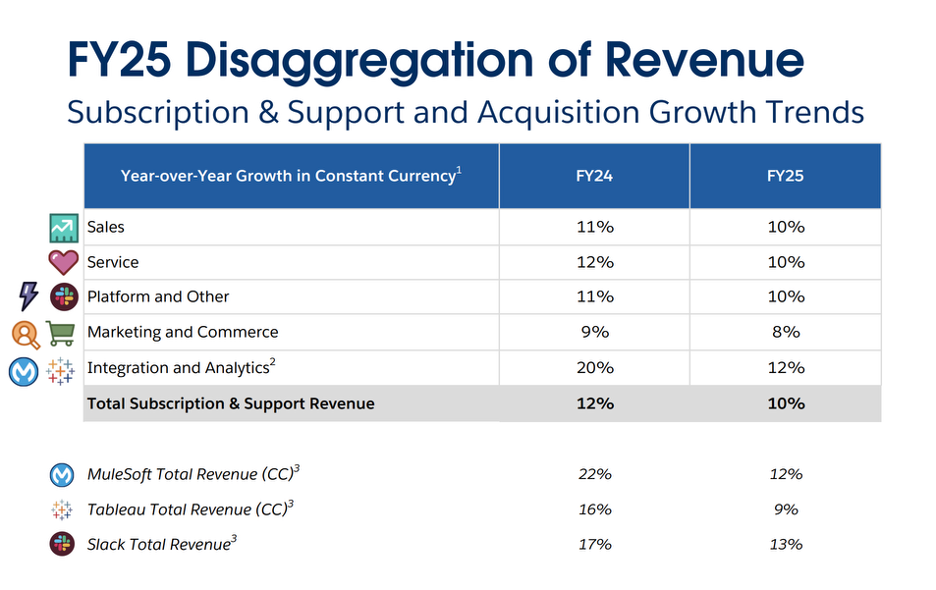

Salesforce has $41.5bn in total revenues with 2 reporting segments: 1) Subscriptions and Support and 2) Professional services and other.

94% of revenues are in the Subscription segment and 6% are in the professional services.

The professional services revenue is basically fees they charge to implement, advise, and train employees on their software.

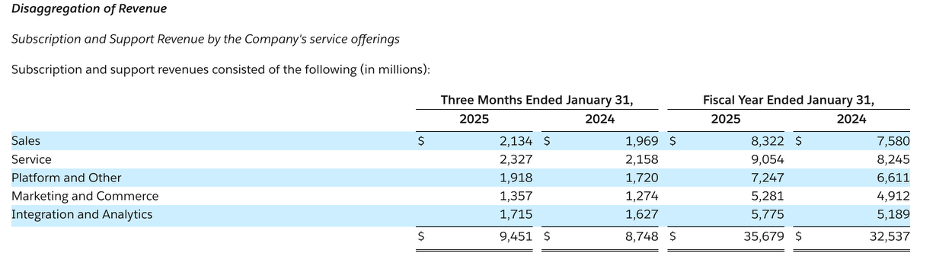

A more helpful distinction is the revenue disaggregation they provide on the earnings release.

They break their products up into 5 categories:

1) Sales

2) Services

3) Platform and Other

4) Marketing and Commerce

5) Integration and Analytics.

Let’s take them one by one.

1. Sales (~23% of Business)

This is the "classic" Salesforce. It is the digital rolodex and pipeline manager for sales reps.

• Sales Cloud – pipeline/opportunity management, account/contact management, forecasting, territory mgmt.

- Tracking a deal from "hello" to a signed contract.

• Sales engagement and productivity – sequences, activity capture, conversation intelligence (varies by SKU).

- Automating the "outreach" (emails/calls) so reps spend more time selling and less time typing.

• Revenue / CPQ (configure, price, quote) workflows – quoting, contracting, renewals

- Ensuring sales reps don’t send out wrong prices or impossible product bundles.

2. Service (~25% of Business)

The largest segment focuses on fixing their customers’ issues.

• Service Cloud: Case Management, Agent Desktop, Omnichannel support

- Routing a customer's complaint (email, phone, or chat) to the right human agent.

• Field Service: dispatching technicians, scheduling, work orders, parts

- Dispatching technicians to a customer's house to fix the internet or a broken appliance

• Contact Center / Digital engagement - chat, messaging, voice integrations, routing.

3. Platform & Other (~23% of Business)

• Salesforce Platform – custom objects, workflows/automation, security, admin tooling.

• Data Cloud that connects to disparate databases and harmonize all data so users can run analytics

- Data360 is the name of their marquee product and they work with data lakes like Snowflake and Datadog, but note that sales people don’t log into those databases. (Data360 revenue is not necessarily all housed here)

• Industry vertical offerings

• Agentforce (AI agents layer) – Salesforce describes this as an “agentic layer” on the platform for deploying autonomous AI agents across functions

• Slack, the corporate chat app that Salesforce is trying to turn to the center interaction piece for corporates

• AppExchange: Basically the "App Store" for businesses.

• Low-Code Tools: Drag-and-drop tools that let non-coders build business workflows.

4. Integration & Analytics (~16% of Business)

This segment is built on two massive acquisitions: MuleSoft and Tableau.

• MuleSoft - APIs / integration / connecting apps and data across systems.

- Acts as a translator for on-prem and disparate databases so they can talk to each other

• Tableau - BI, dashboards, analytics (business users).

- Turns data into charts and dashboards

• Informatica – enterprise data management and integration to connect, clean, and unify data across different systems so it is usable for analytics and AI.

5. Marketing & Commerce (~14% of Business)

This is about the "before" and "during" of a purchase.

• Marketing – segmentation, journeys, personalization (often associated with Marketing Cloud positioning).

- Sending those "You left this in your cart" emails and managing massive social media ad campaigns.

• Commerce – unifying storefront + order + customer experience; Salesforce describes Commerce as connecting marketing/sales/service/fulfillment on one platform.

- The actual "Buy Now" button on websites.

Now each of their segments are growing in the same ballpark.

Let us now talk about the competitive environment and where Salesforce stacks up.

Competitive Landscape.

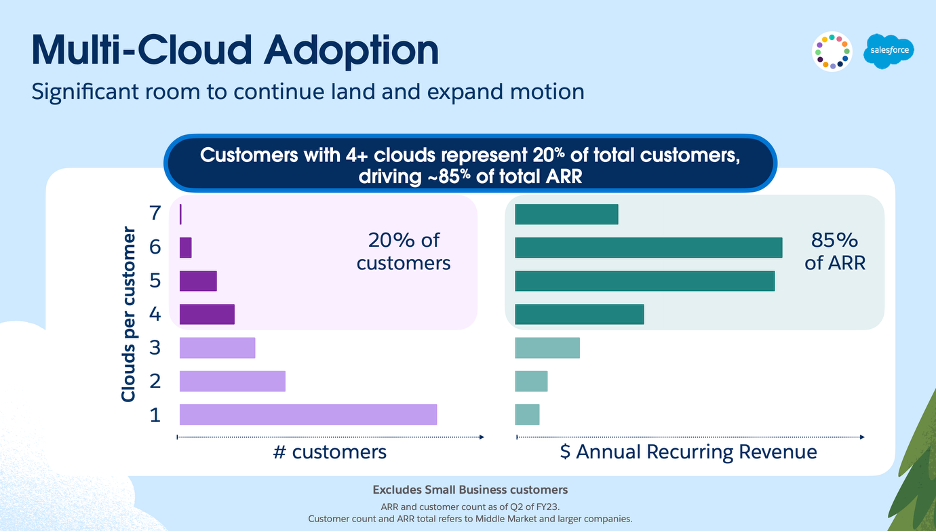

Over 90% of Fortune 500 customers use multiple Salesforce products, with 3 or more “clouds” being standard.

In their 2022 investor day, they noted that 20% of customers are on 4 or more clouds, and they drive over 85% of revenues.

Overall, they are the #1 CRM provider with an estimated 22% market share.

Other players like Microsoft’s Dynamics 365, Oracle, and SAP, HubSpot (more SMB focused), and Adobe (on the marketing side, not sales) all have a mid-single digit market share.

The rest (or majority of CRM) includes more specialized business’s like ZenDesk for specialized customer support and many vertical specific CRM’s like Veeva for life sciences and Toast for restaurants.

The category of CRM is a bit too broad to be the best distinction though. Breaking it down more granularly…

Among Salesforce’s products, Service Cloud is estimated to be the most dominant with ~45% market share.

Salesforce’s next biggest product is the Sales Cloud with ~40% market share.

In both segments Oracle and Microsoft are also key competitors, albeit with much lower market share.

HubSpot is also up there, but focuses more on SMBs. However, they are making a push upmarket.

ServiceNow is also increasing encroaching on the space. And in turn, Salesforce is trying to get more into ITSM (IT Service Management) to move more into the backend and attack what was traditionally a ServiceNow stronghold.

Marketing cloud is smaller with just 14%.

Adobe is a key competitor here and is bigger than Salesforce by most estimates.

Adobe wins with creatives and Salesforce wins with companies that are less design focused and lead with sales.

Big picture, Salesforce is an amalgamation of acquired software businesses—over 70 to be exact.

Anytime there is a successful software business that can plug into a corporation's workflow, they just acquire it.

They may enter a business through CRM, but they cross-sell many different product groups to get a company using more and more of their products.

In contrast, ServiceNow(and HubSpot) largely build products in-house and have a unified code base. This generally means a cleaner platform with less integration issues.

In fact, when ServiceNow buys a company, they often rewrite the code to make it native to their platform. ServiceNow started in the backend and now moving more to the front end with CRM and Sales tools—all the while Salesforce is going in the other direction.

With ServiceNow you pay a premium to be on their platform, whereas with Salesforce you have an “integration tax”.

Nevertheless, though, it is very hard to move off of Salesforce once you are on it.

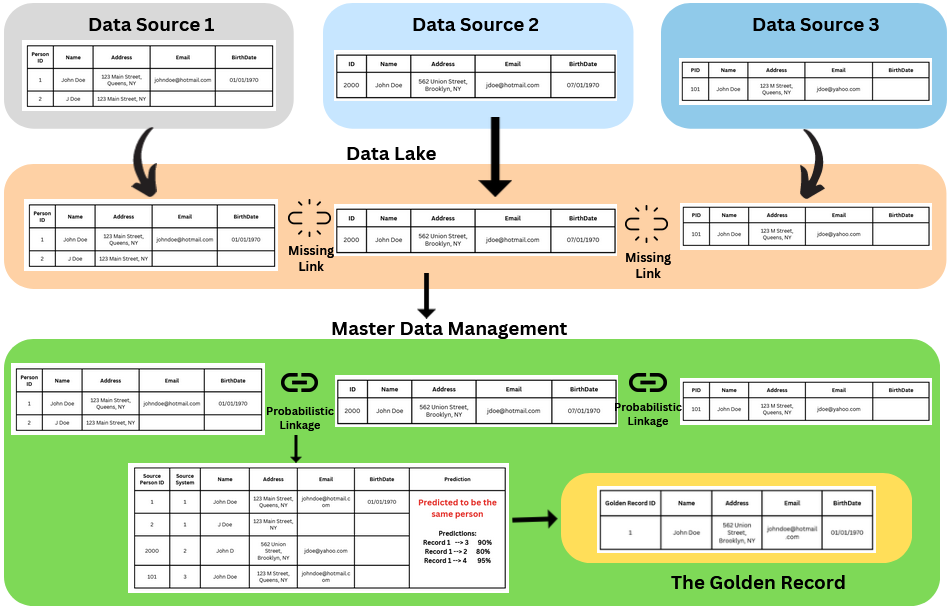

Salesforce’s advantage is that they are seen as the “golden record” of a customer’s data. This is also called the “single source of truth”. They house all of the most critical data there is on a customer.

• Emails, deals, customer complaints, records of which user clicked which ads, billing addresses, payment info, and everything else that can be recorded.

Point of clarification: the data itself is stored in a data lake like Snowflake, but it is unstructured and unconnected. You may have multiple entries for the same customer, but Salesforce is the one that stitches all of the data together. As they say, sales people don’t log into Snowflake, only data scientist do.

Snowflake is trying to move up to control the golden record with a product called Unistore, but they don’t control the interface or the habit. Sales people log into Salesforce and they control the actual buttons too—like refund, call, email that can allow them to take action.

Snowflake is a pile of data, whereas Salesforce is a map of that data. That “map” is the “golden record” or “single source of truth”.

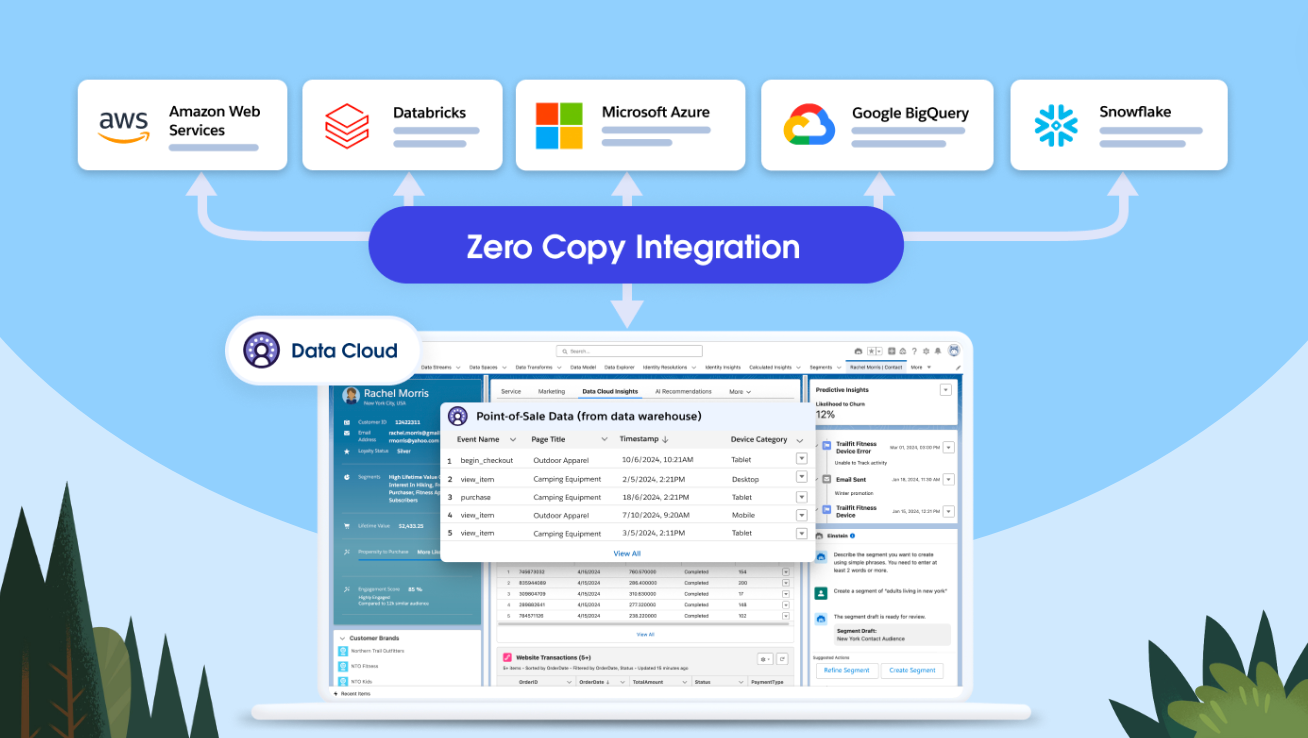

Salesforce has worked hard though to unify their platform and just did an acquisition of Informatica to help unify and cleanse their databases and make all the data “AI ready”.

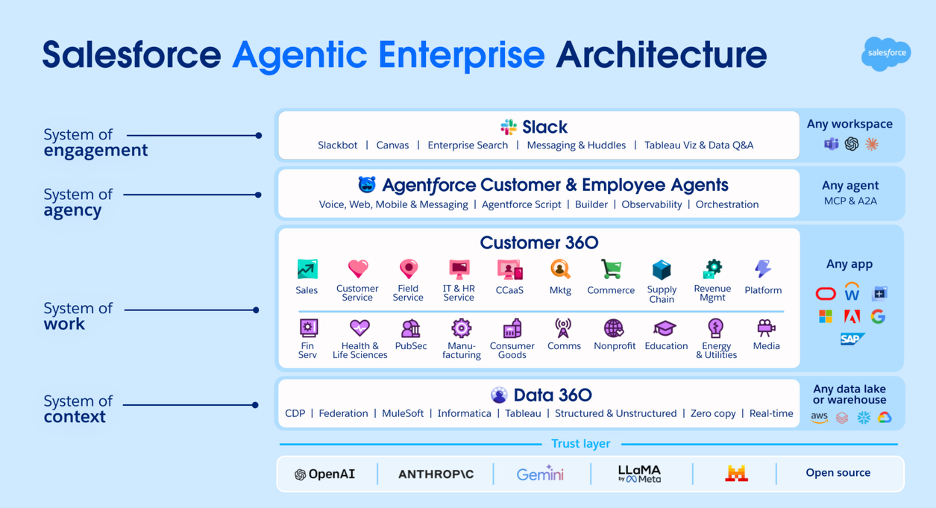

The new vision is the Data 360 platform that feeds into their different clouds: Sales, Service, Marketing, and Commerce.

Data 360 is a zero-copy data federation, which means it can work with multiple data sources and doesn’t need to actually export the data out. This is quicker and less expensive, since the data isn’t actually moving.

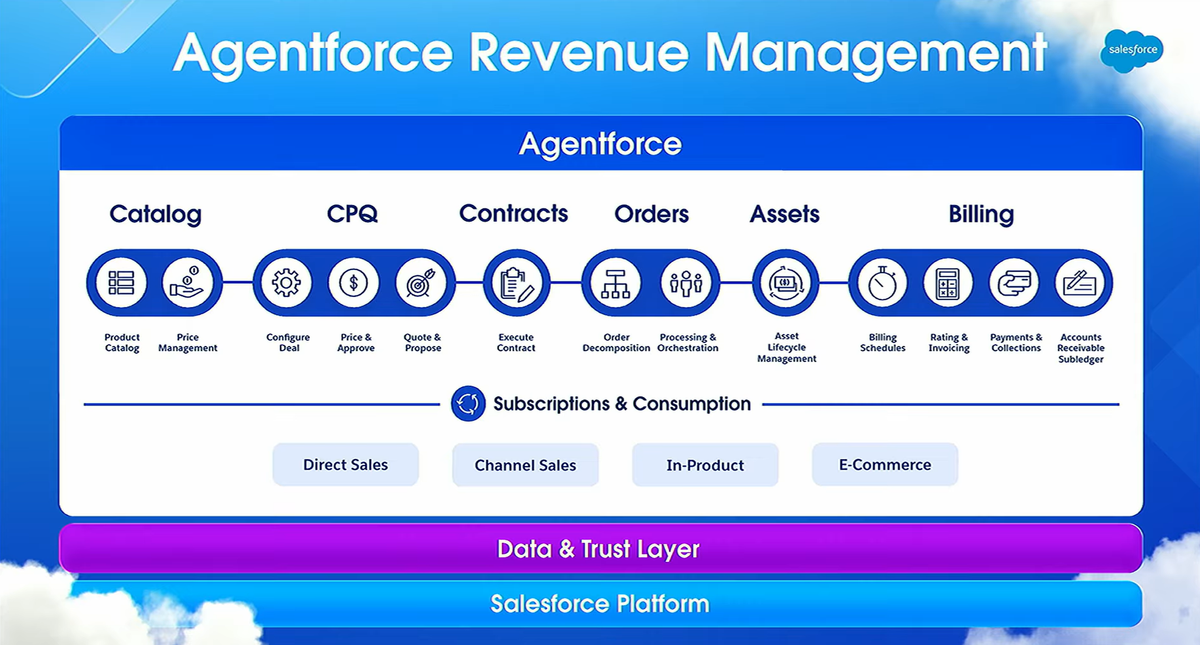

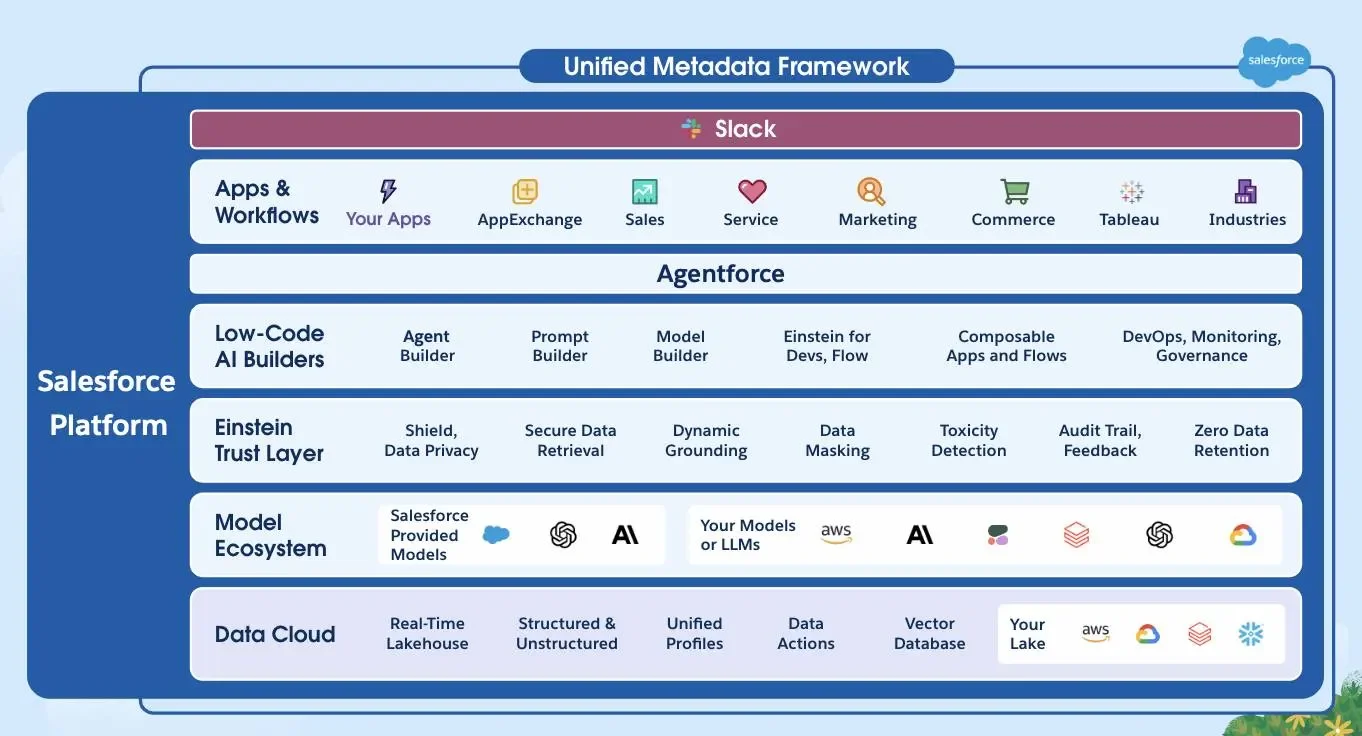

On top of this comes the Agent layer. This is where Salesforce is trying to differentiate themselves and make inroads against the competition.

Agentforce and an AI World.

First, we need to understand the problem with LLMs…

They lie…

or to put it nicer, “hallucinate”.

If you asked an LLM to gather you data, it essentially “guesses” at it.

For most businesses, this is understandably a deal breaker.

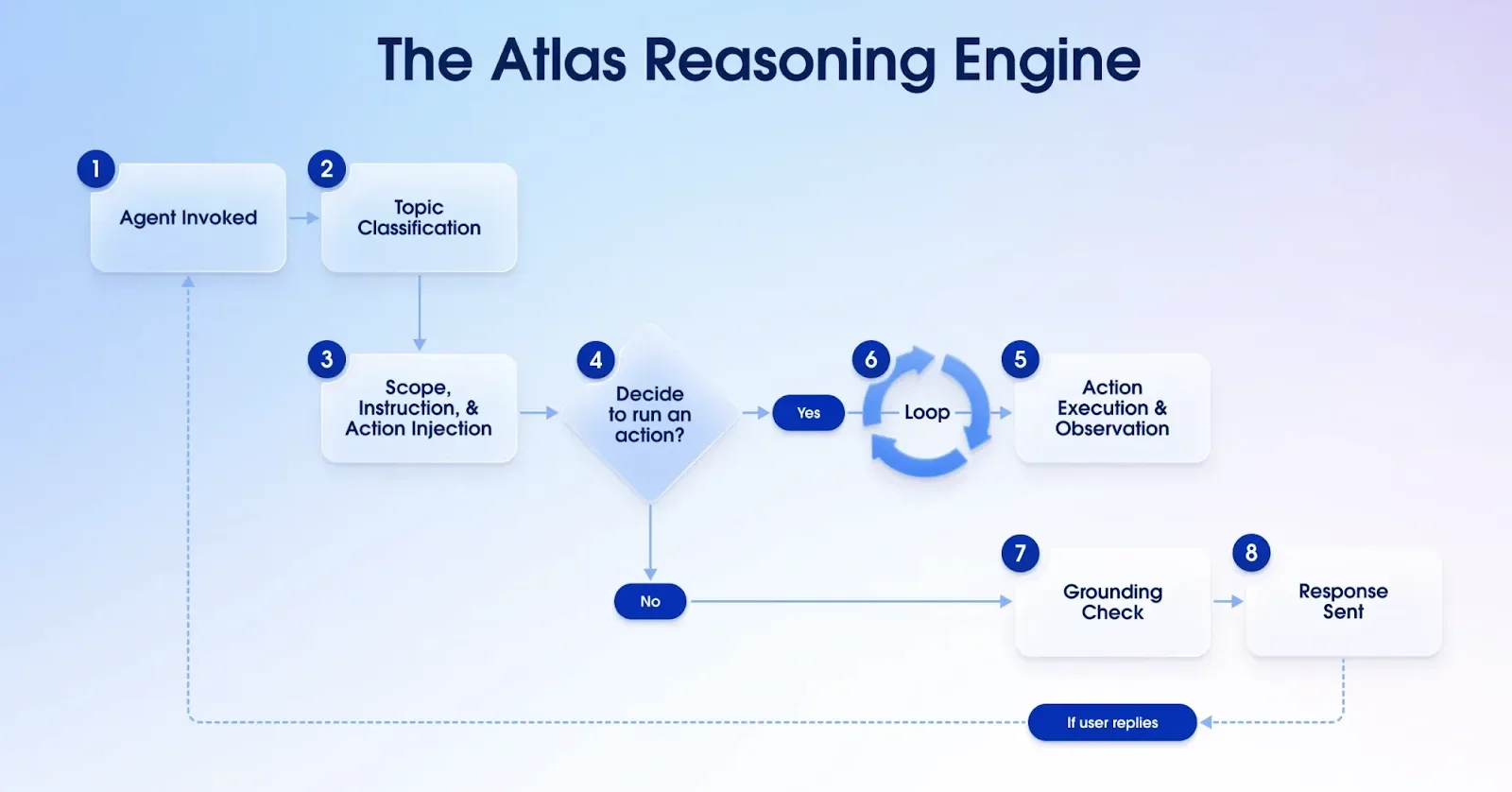

What Salesforce has rolled out to address this is the “Atlas Reasoning Model”.

They essentially plug into LLM models from OpenAI, Anthropic, and Google and then interpret requests and create business logic.

Business logic is a set of sequences that are deterministic.

So, for example, if a customer asks if they can get a refund on a product, the LLM can help decipher the request and then the Atlas Reasoning Model puts it into a set of sequencies.

Check the customer’s account to see if the product was actually purchased.

Check the return window, is it within 30 days?

Check if this item is allowed to be returned once opened.

Then issue the refund for $45.50.

These are all steps that need to be done deterministically, not probabilistically.

They call this grounding the model and it is a part of the “Trust layer” of the AI agent as it ensures accuracy.

Atlas creates the agent script with the logic for it to follow.

And it sits in-between a companies’ private data and the LLMs to mask sensitive data before sending it out. This ensures Zero Retention by the LLM of private data.

The key here to note is that Salesforce works with different AI Models, and instead is trying to compete on having better data that is easily accessible (Data 360) and stronger guardrails that improve accuracy, trust, and security.

Below we see how all of the pieces work together.

At the bottom is the data. Then their apps are on top.

The agents sit on top of the apps and the user uses a workspace like Slack to engage.

They came up with an acronym, AWU, or agentic work units to showcase how the use of AI is proliferating.

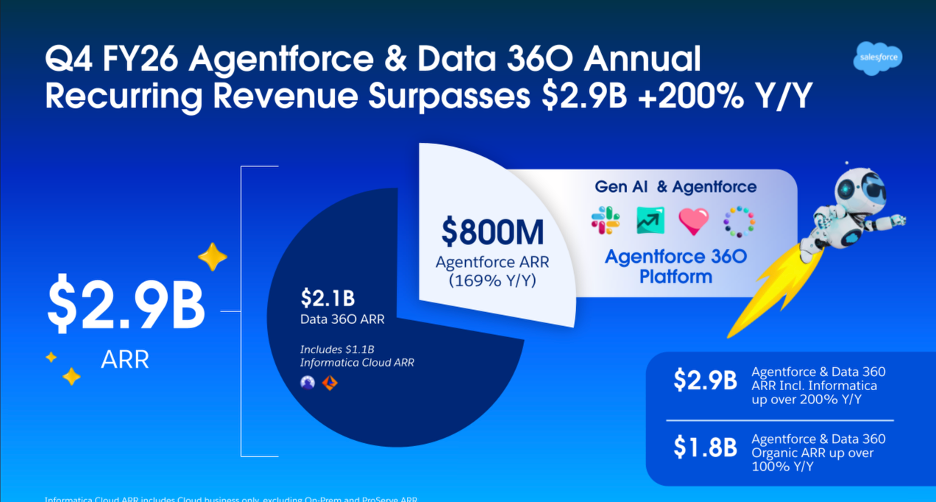

Agentforce and Data 360 together are growing +100% y/y organically. Agentforce alone has $800 million in ARR, making it one of their fastest growing products ever.

So far it seems like they have a decent AI, strategy….

So why is the stock down ~50%?

Risks.

The first risk is the “seats” risk facing all of SaaS.

The more productive AI gets, the fewer humans users there are, the fewer licenses they sell.

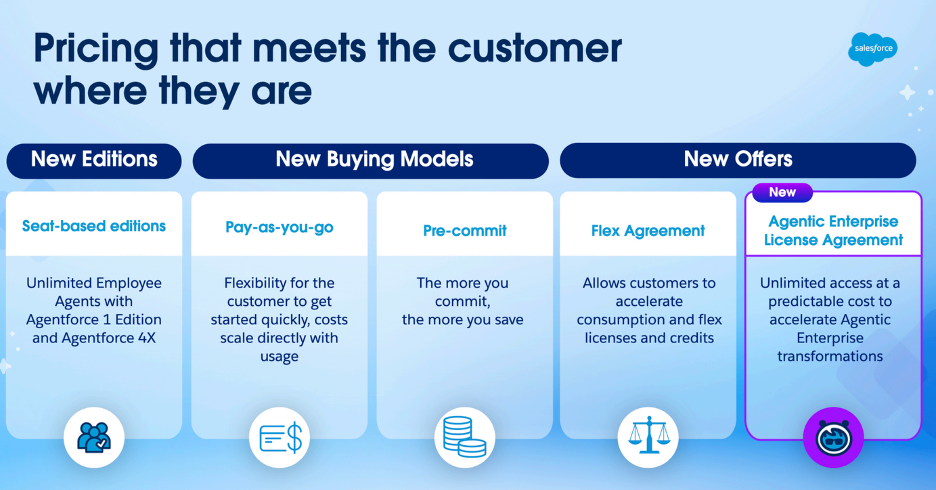

Salesforce notes they are addressing this with different pricing models, including a usage fee or a Enterprise wide licensing agreement.

Businesses like predictability in spend because they budget at the beginning of the year, so it seems like an agentic enterprise license with predictable costs will make sense.

They will price on a business level instead of a per seat level.

While there is still some risk in this pricing transformation, I think they will probably handle this transition fine.

The bigger risk is that AI agents take over workflow and cut Salesforce out.

This could mean that a new AI native start-up or the models themselves move further into a companies work flows to cut out Salesforce.

It also is a bit hard to see this taking place, as customers of Salesforce are so entrenched and it would be an absolute headache to rip them out, reintegrate with all of their systems, and even rewrite code.

This is especially unlikely so long as Salesforce continues to adopt new AI technologies, so a new comer doesn’t really offer anything great that they can’t do.

Now maybe if there is true Super Intelligent AI that can do everything and can circumvent all of the application layer, the data trust layer, and the governance, this could happen…

But that seems like that’ll be Sci-fi for a long time.

The real risk I see is simply competition…

Not from necessarily a new breed of AI competitors, but from the incumbents weaponizing AI to encroach on each other’s lanes.

This isn’t conjecture, it is already happening.

All of the large software platforms want to stand in between the user and all of their work functions.

With access to data and controlling the user’s UI (which can be Office 365/ Teams for Microsoft, Slack for Salesforce or the ServiceNow Platform) they are in the position to leverage AI to move into each other’s product verticals.

Salesforce, as an incumbent is in a good position, but so are the other large players.

However, it also is just as likely they all grow at the expense of smaller players and also the cost to maintain and implement IT tools

For every $1 spent on software, about $3 is spent on consultants and maintenance.

This $3 is more under pressure as the AI and platforms take on more of these functions.

Where new competitors are most worrisome is in winning new companies that don’t have any legacy ties to Salesforce. That is where a new platform or suite of products has the most potential to weigh on their growth.

The other risk is the AI models charge a premium for their tokens and that weighs on their margins… even in scenario it seems that they can pass off the cost to the customers.

So margins may fall, but not margin dollars.

With all of these risks, it ultimately comes down to what’s priced in.

Valuation.

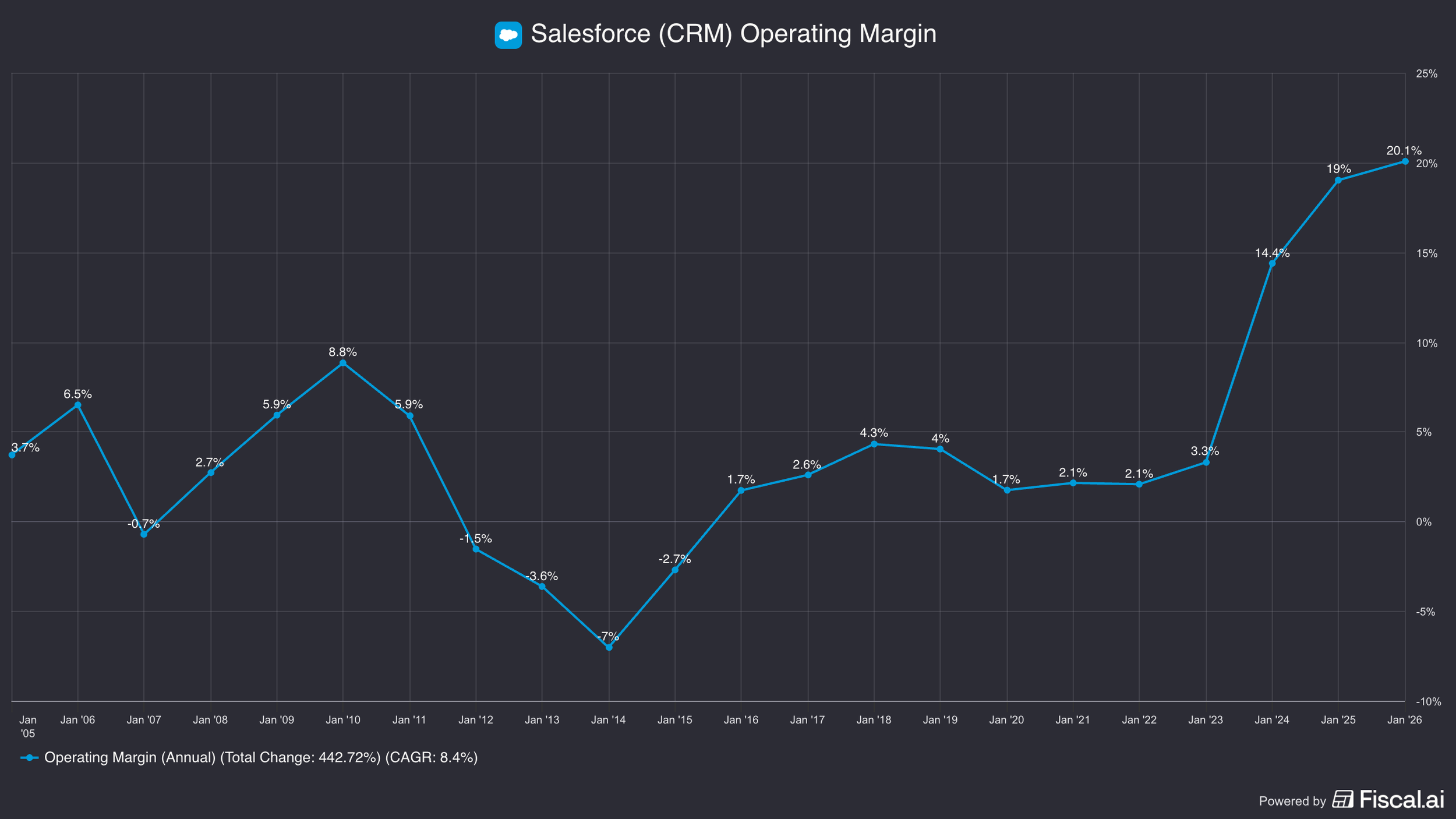

Salesforce has LTM revenues of $41.5 billion and operating margins of 20%.

It is worth pointing out that their margins have expanded from 2% in 2020 as they focused on efficiency, cut headcount, and raised prices (as they typically do).

Operating profits stand at $8.3 billion, up 15% y/y.

Free cash flow (after SBC) is $10.9 billion.

At a stock price of $200, that is a market cap of $186 billion.

That is a Free Cash Flow multiple of 17x.

That figure does include about $2.9 billion in unearned revenue, that technically isn’t a sustainable source of cash (as growth slows this shrinks). Investors will have different opinions on whether to back that out, but if you do, it is 23x FCF.

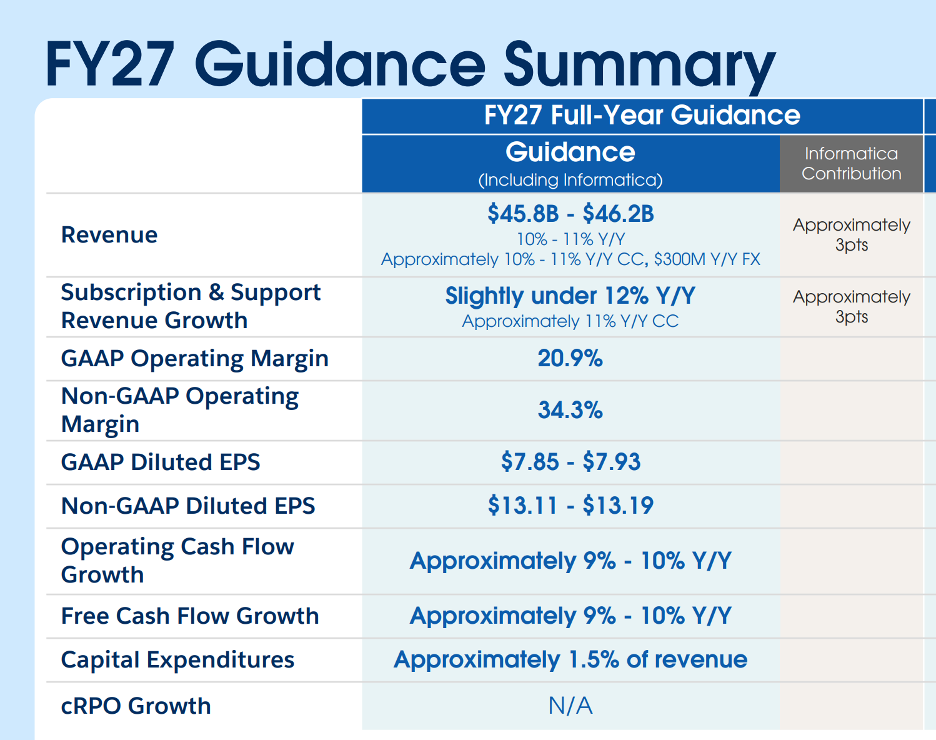

Last year’s revenue growth was 10% and they are guiding 2027 to about 10% as well…

But that includes a 3 point benefit from their last acquisition of Informatica.

If they can sustain a high single digit growth rate a low 20s to 25x cash flow multiple seems fair.

However, they put out big 2030 target of $63 billion in revenue.

This implies a growth rate of about 11%, suggesting revenue could inflect from their current organic rate of 7-8%.

If they can grow at 11% top line and benefit from a bit of operating leverage, they could perhaps grow cash flows closer to the mid-teens, which justifies a 25-30x multiple.

Another way to look at it is on $63 billion revenue, they could probably earn at least a 30% mature margin.

This is $15bn in profits after tax.

At 25x, that would be worth $375 billion. This is over 100% upside.

Plus they will bring in over $40 billion in cash flow over that period, which they intend to direct towards stock buybacks.

They announced a massive $50 billion stock authorization, which could buy back almost 28% of the company at today’s prices.

On the other hand, competition is intensifying and it isn’t impossible that they just grow less than they expect.

And in response, they start spending more money to keep up with the competition and maybe make a few very expensive acquisitions.

Then instead of a company that can sustainably grow revenues with growing cash flows that they return to the shareholders, they spent most of the money just maintaining their existing position.

It is up to an investor to decide what they believe.

For more on Salesforce, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.