PayPal Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

And while competitors may be outcompeting, payments are still a generally sticky business.

They still process an astounding $1.8 trillion in annual payments…

With 230 million monthly users.

Could PayPal stock be massively oversold?

Or are they the epitome of a value trap?

First, we will start with a breakdown of their business. Many are probably familiar with their PayPal checkout button, but did you know they process payments for Uber, Airbnb, and Spotify too?

There are a few different pieces of the business investors need to be aware of.

Let us get into it!

Business.

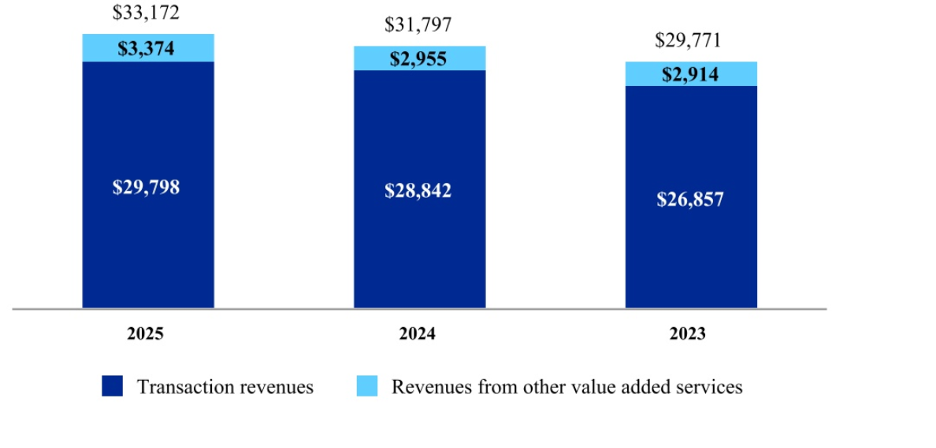

In total PayPal has revenues of $33.1 billion and splits it up between transaction revenue and “value added services”.

Value added services primarily includes interest and fees from their lending business and interest earned on customer deposits.

A more helpful breakdown though is if the look at PayPal’s core products. While, they don’t regularly break out revenues by products like this, we have some ad hoc disclosures to get a sense of how big each of these businesses is.

PayPal Branded Checkout.

This is when you use the PayPal logo check out button on a website (or their app for in-store use).

On their 2025 investor day they showed that this was about 30% of total payment value (TPV).

This is their most important profit driver, but growth here has been slow as they face a slew of competitors.

Their take-rate (revenue over TPV) is estimated to be around 2.5-2.9%.

Their profits in this business can vary a lot.

At it’s best it is a “closed loop” transaction where a buyer pays from funds on their PayPal wallet and they don’t have to pay interchange fees, which are the largest cost pool in a transaction.

Often though, transaction are funded by credit cards. Even then though they make around an estimated 0.8% to 1.2% per transaction (gross profits / TPV).

This business is 30% of their TPV, but an estimated 60-65% of profits.

PSP.

Their biggest business by TPV is Payment Service Processing or PSP.

This business is basically unbranded payment processing. A lot of this business comes from a 2013 acquisition of Braintree (which also owned Venmo).

This business is low margin and powers a lot of large enterprises including Uber, Spotify, and Airbnb.

They aren’t exclusive payment providers as enterprises have multiple providers—Adyen and Stripe are two big competitors here.

It is primarily digital only, which is also known as a more competitive payment space with worth economics than on-prem. The fact that they have a large portion of enterprise clients (who can negotiate rates down), further makes this a bad business.

Historically, they used this business as a loss leader to help better position their branded PayPal checkout business.

The strategy behind this is specious, which is also why it didn’t really work.

The idea was that they would offer a business payment processing at an extremely competitive rate, in hopes of making it up when users used the branded PayPal checkout button or paid with their PayPal wallets.

Below you see that PayPal (and Venmo) are pay options on Uber.

There was also some thinking that gathering the data on the user could be helpful.

This business was focused on gaining market share and had many unprofitable accounts.

In the last year, they pushed to focus on profitable accounts and renegotiated or shed loss-making clients.

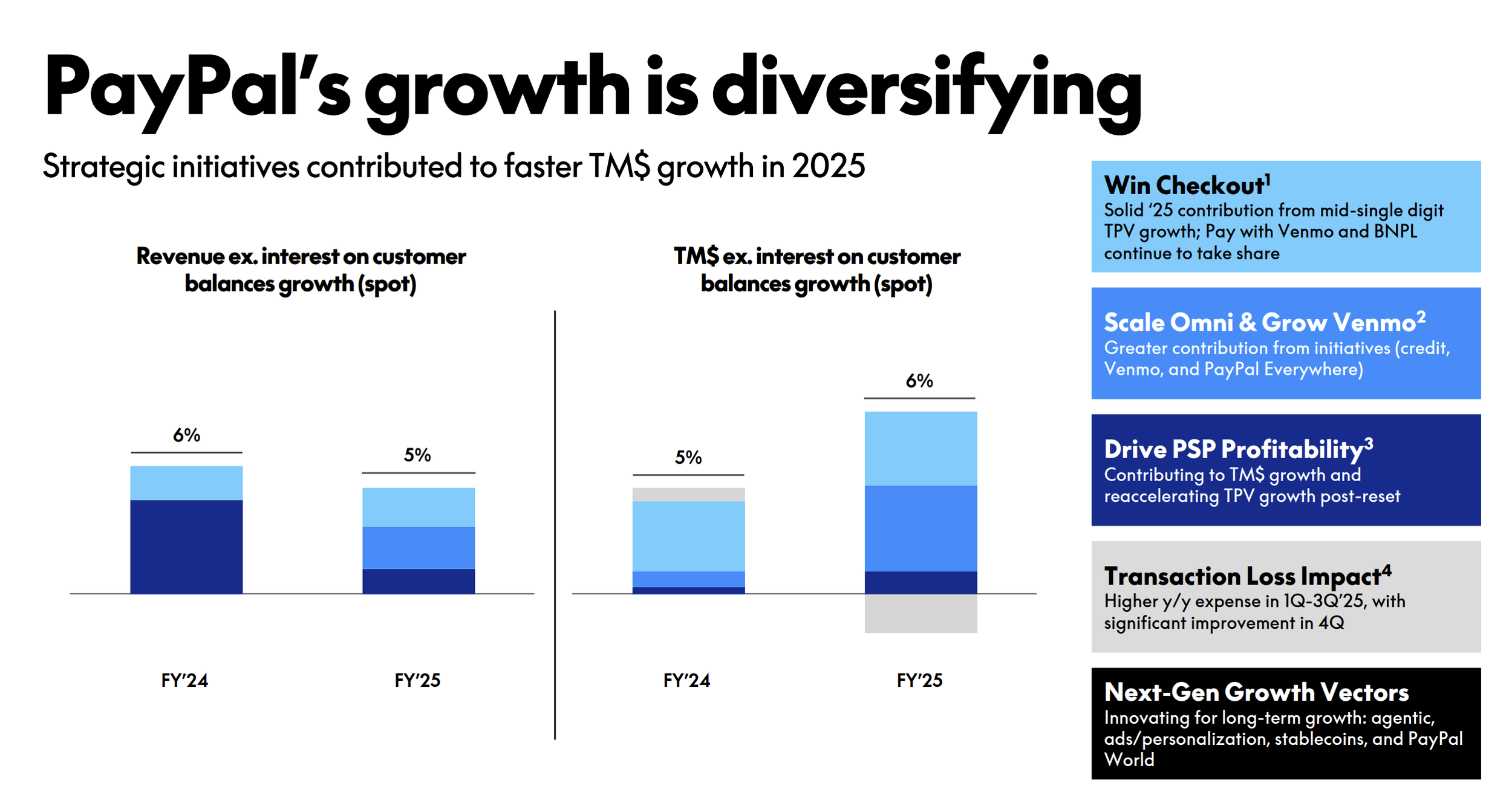

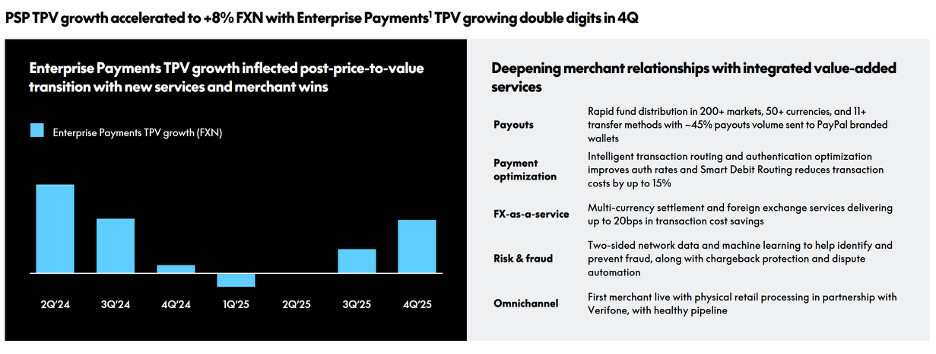

While they don’t disclose this segment separately, you can see the progress in the slide below.

Note how big the dark blue bar is for 2024 on the right side and how much smaller it is in 2025.

That is how much less revenues grew.

BUT, the dark blue bar on the left (transaction margin dollars, which is basically gross profits) is much bigger for 2025 vs 2024.

This backs up the focus on more profitable accounts.

They also had this slide in their 4Q earnings, which shows enterprise payments returning back to growth after a reset (enterprise is primarily served by the PSP business).

Venmo.

This is a very popular P2P (peer to peer) payment app that allows users to send money for free.

The probable is figuring out how to monetize it.

The main way they make money is from interest income on excess balances held in a user's wallet. The problem is that users don’t tend to hold much money there.

On the consumer side, they also offer instant balance transfers for a small fee and try to cross-sell other financial products to their users like debit and credit cards.

The most profitable push is to get users to pay with Venmo, where they can charge a ~2% fee to merchants.

PayPal did disclose they generated $1.7bn in revenues here that are growing 20%.

Lending Revenue.

They have a few different lending products from BNPL (buy now pay later) to credit cards, to merchant working capital loans.

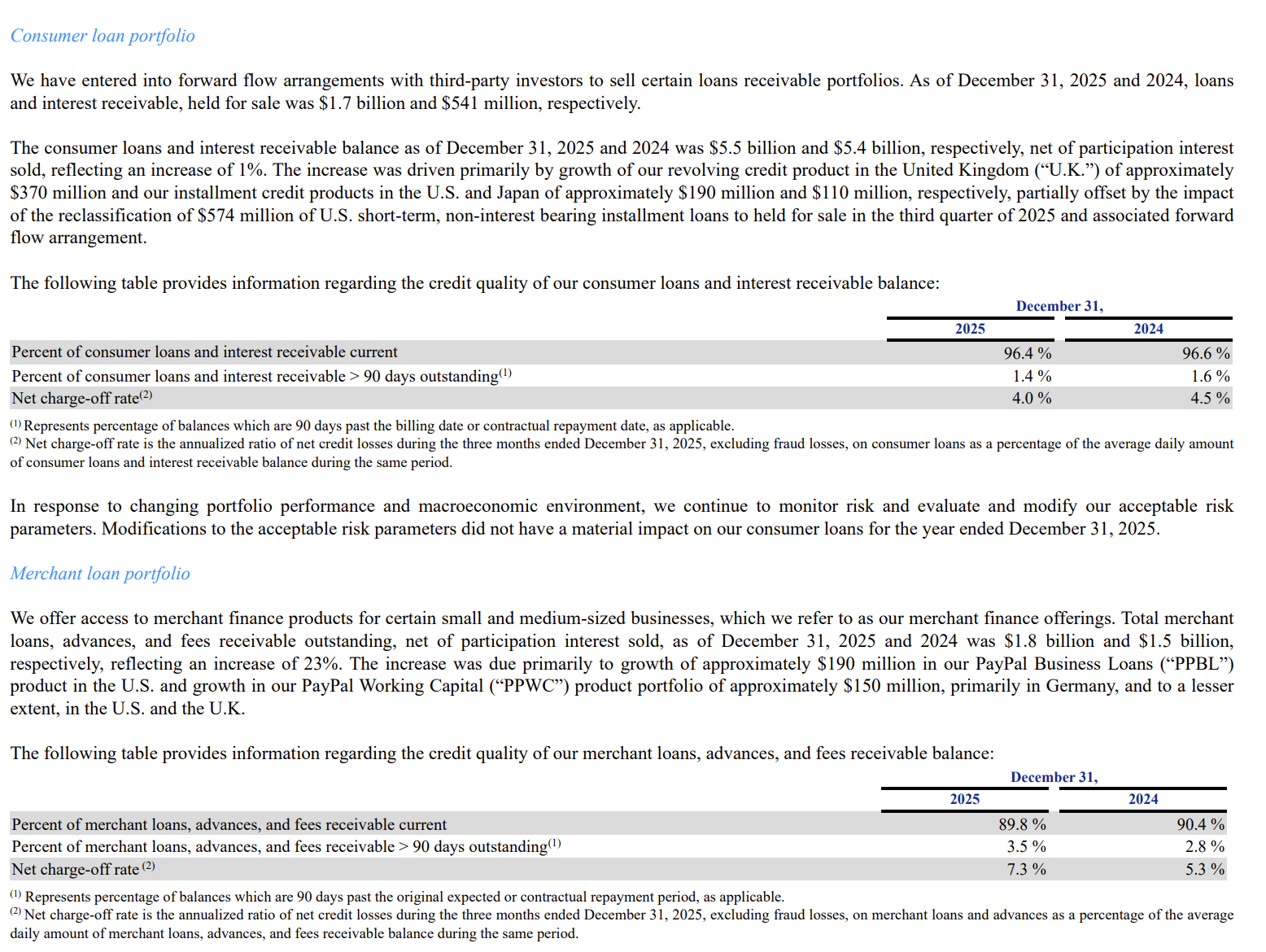

In total they have about a $5.5bn consumer loan portfolio and a $1.8 billion merchant loan portfolio.

They have had some issues with the loss rates being high—in 2023 the consumer portfolio was around 7% and the Merchant portfolio hit 19%.

These have both come down to about 5 and 7% since.

Poor underwriting is a key risk for any lending business and the problem is it doesn’t show up until there is economic stress. (Their loans are relatively low duration, which reduces the risk though).

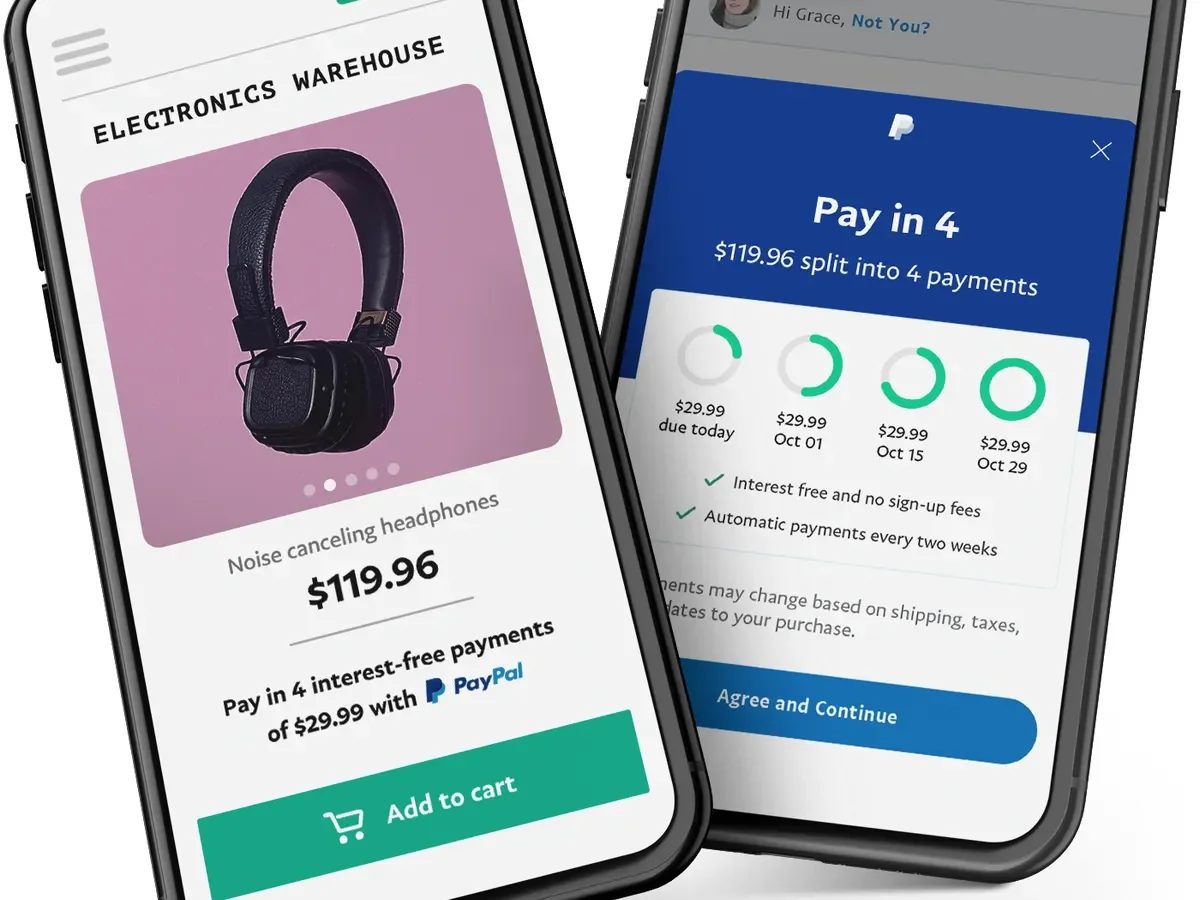

The big push in this business is BNPL.

BNPL allows users to buy products in small installments. It is a bit different than a traditional lending business because BNPL is usually advertised on the product page instead of just in checkout—this means it can actually help boost demand for an item.

There is competition here from Klarna and Affirm, but they grew TPV 20% here to $40 billion.

Company Financials.

In total they have $33.1 billion in revenues and $15.5 billion in gross profits for gross margins of 47%.

One of their largest costs is interchange fees to the networks/ issuing banks.

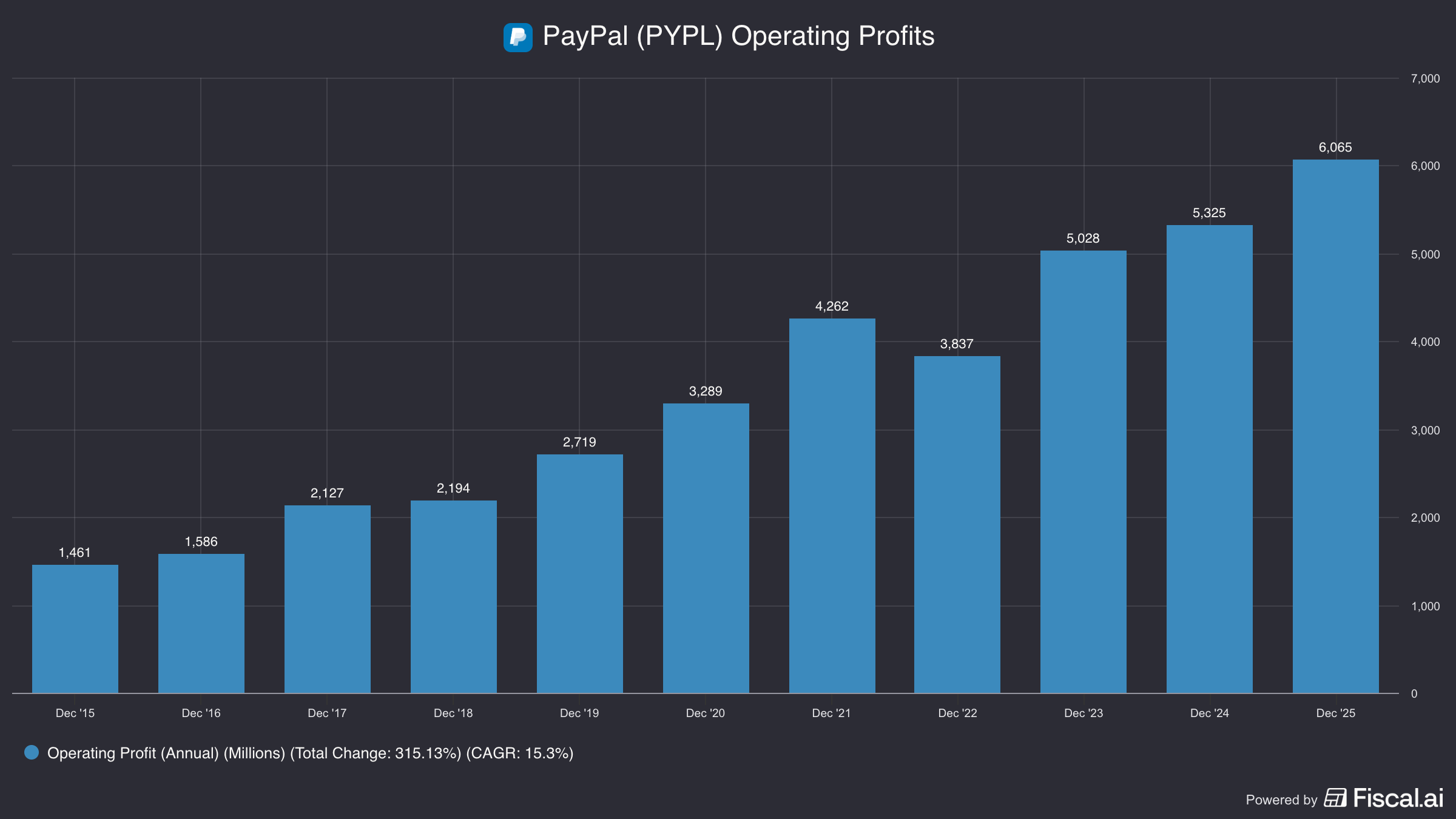

Operating profits are $6 billion for a margin of 18%.

You can see that operating profits have grown a lot since 2020 (almost doubled), but revenues are up only 54%.

While part of this can be explained on the focus of better quality business (mentioned above) combined with cost costs, but the biggest factor is interest rates.

They make interest income off deposits and interest rates jumped over that period.

Other Value-Added Services (where this revenue is captured) grew 120% since 2020. As interest rates fall though, they are at risk of losing this profit pool.

Business Issues.

The key issue facing PayPal is simple competition and a dated tech stack.

They were very early to get hundreds of millions of customers payment info preloaded, but now users have many fast check out payment options.

On top of that, competitors like Apple Pay are far quicker and easier to use.

Since Apple Pay has access to the NFC chip in the phone, plus can make the only big button on the phone default to Apple Pay when doubled clicked, they were able to create a far quicker payment experience.

When paying online, Google Chrome and Safari will try to grab your payment details and save them for later, so a key value prop of PayPal to consumers is negated.

Other competitors have checkout buttons now too like Shop Pay, Affirm or Klarna for BNPL, and a bunch of local competitors depending on the market.

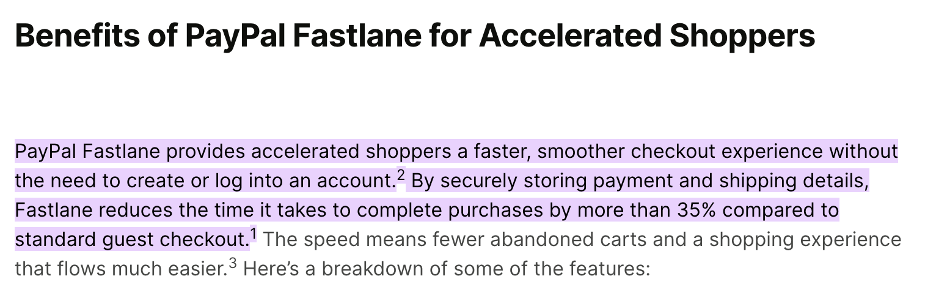

PayPal is responding by modernizing their checkout to eliminate the web page hop that asks for a manual password log in, which adds friction and results in lost sales when users forget it.

One of their key products here is Fastlane, which identifies a user by their email and sends them a one-time code or allows them to sign-in with biometrics.

This simple change has increased complete purchases by more than 35% compared with a standard checkout.

They are focused on increasing the number of users who have biometrics stored (FaceID or TouchID) from 33% to 50%.

They also are moving to install more up to date integrations across their SMB user base, so they can more quickly push updated products across. BNPL is something that is not easy for a normal SMB to add on.

This effort is called PayPal Complete Payments, or PPCP, and it is a unified platform that integrates to a SMBs backend and automatically can offer the latest updates, without them needing to manually update.

They also are trying to move their BNPL buttons on an individual item, so that it induces demand for the seller and it locks in the payment method before the competition in the checkout page.

All in all, these are initiatives that make sense and will likely see at least moderate success.

Will it be enough to save of the onslaught of competition?

No.

But given how much PayPal has sold off, the market is pricing them has a secular decliner.

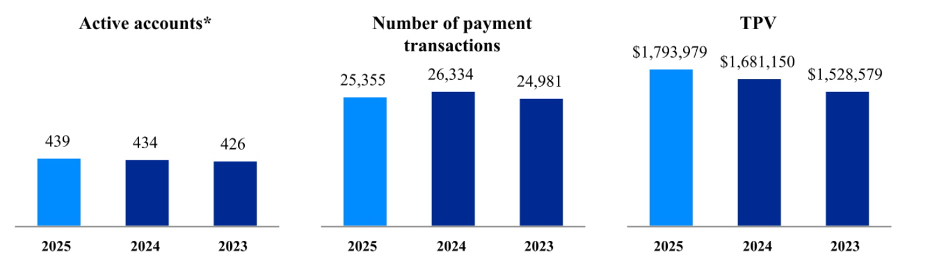

Even if they just maintain their existing business and can ek out a little bit of growth from their existing user base of 439 million who conduct $1.8 trillion in payment volume, it can outpace market expectations.

To unpack this argument though, we turn to our valuation.

Valuation.

On a free cash flow basis PayPal trades at 8x.

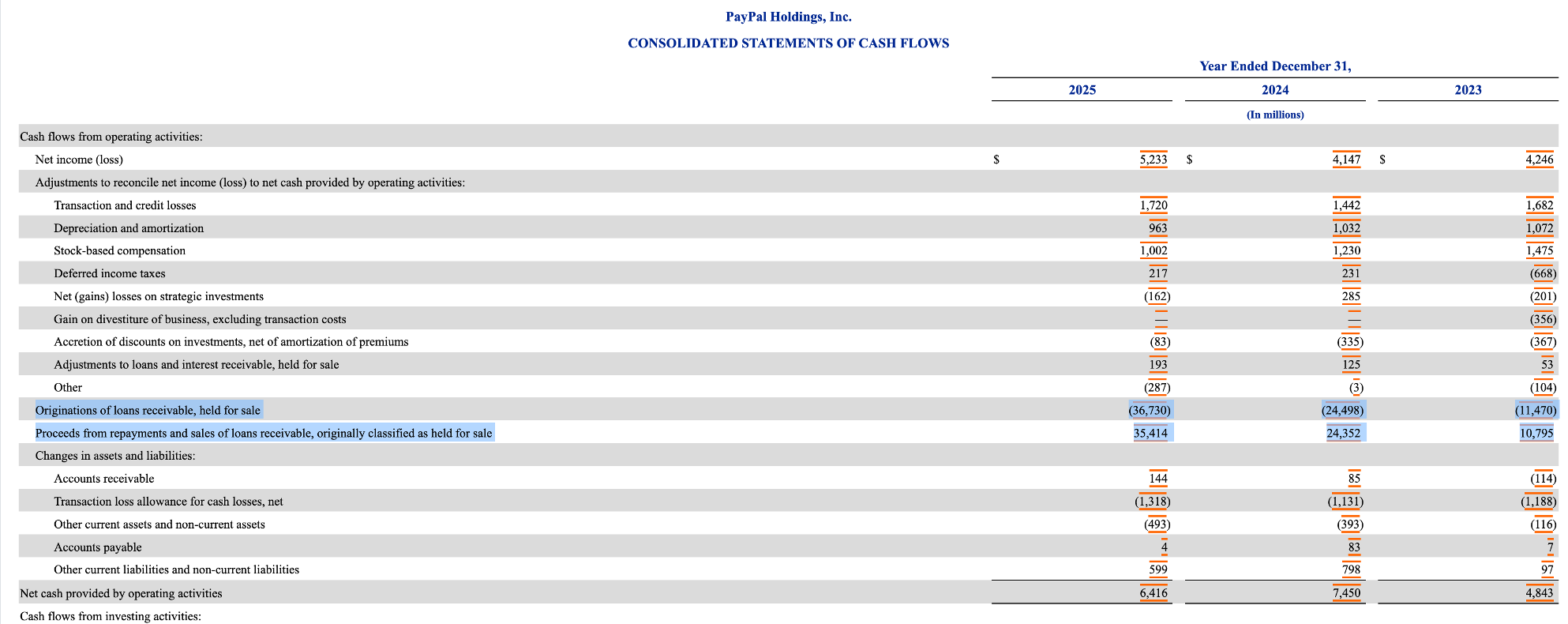

However, since they entered the lending business, an investor cannot easily rely on cash flows as a metric of business health.

This is because these two items (highlighted below) from originations and repayments flow through the cash flow statement.

However, these items do not create economic value (beyond the potential gain on sale or interest and fees collected).

To understand this distortion, let’s say they originate $35 billion in loans in a given period, but get repayments of $40 billion (assumes they originated more loans in the prior period). This will be recorded as a positive operating cash flow of $5 billion, but it simply represents getting paid back for money you gave out.

The economic value isn’t $5 billion, but that is what the cash flow statement suggests.

This is one reason why bank investors never talk about valuing banks on cash flow.

So at a stock price of $46 and a market cap of $42 billion, they trade at an earnings multiple of 8.5x.

Any time a company gets a multiple below 10x, you can generally assume the market thinks this business is in secular decline and earnings will contract.

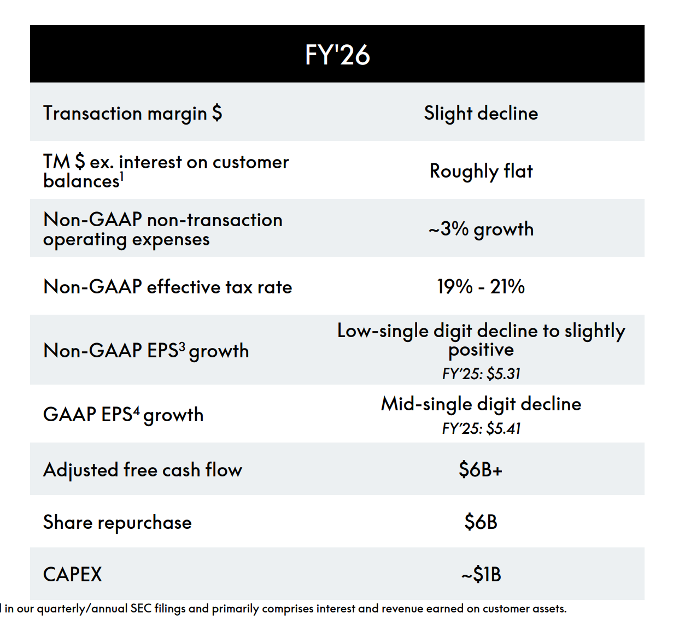

While they have still been growing, next year they have guided earnings to potentially contract low-single digits at the low-end of their guidance range.

However, the main reasons for this is because 1) interest rates are lower, 2) they sold a loan portfolio, which reduces earnings (but these are low quality earnings), and 3) they are increasing investments to improve their core products technology.

Even though branded checkout growth slowed to 1% in the last quarter, which is dangerously close to contracting, these new initiatives should improve this.

The key with PayPal is that they stop trying to come up with far flung ideas to return this business to growth and instead do the basic (and boring) things they can to optimize this as a mature business.

Even if PayPal never is a payments leader and there days of strong growth are behind them, it still could be a good investment provided that they are:

1) very responsible capital allocators and 2) the competition doesn’t further intensify.

Despite this being an old business, there still are plenty of users that habitually reach for the PayPal option and as long as they can provide them a good experience, there isn’t great reason they will switch.

Investors need to just assume that the company doesn’t fall apart and management doesn’t do anything silly—like talk about trying to be a SuperApp or an advertising powerhouse—and instead focuses on their core products.

After resetting the business, it is not implausible to think the can achieve low single digit revenue growth, which can translate to mid single digit operating income growth.

If they were able to do this consistently, then a fair value would likely be closer to 10-12x.

They are buying back a lot of stock, $6 billion last year, and have a 1.3% dividend yield. At the current market cap, that is about a 16% shareholder yield.

The downside risks are still there.

And they unceremoniously fired the last CEO, with a new one set to start next month.

The risk is they focus too much on trying to grow again and look for new businesses, which waste shareholder capital and they are unlikely to succeed in (they do not have the best reputation for execution).

With more balance sheet lending too, there is also a risk they are viewed more like a bank and get a “bank multiple” as they become more capital intensive.

In short, whether investors are interested in owning a business that is far from at it’s prime, but may stick around longer than the market expects, is ultimately going to come down to the time investor you are.

Warrant Buffet later in his career only focused on high quality businesses, but earlier in his career he would own anything he thought was trading under it’s fair value.

It’s up to you to decide what kind of investor you are and if the risks inherent in a potential melting ice cube are worth the perceived returns.

For more on PayPal, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.