Mercado Libre Stock Breakdown

Get smarter on investing, business, and personal finance in 5 minutes.

Stock Breakdown

While Amazon has been loudly dominating the U.S. and Europe in ecommerce…

There has been a quiet ecommerce player dominating South America.

Starting as a classified ads business, it was basically the eBay of Latin America.

Except unlike eBay, they created their own inhouse payments system (eBay bought PayPal instead) AND…

They moved to fixed prices to mimic Amazon in the mid 2000s.

While for years their growth was hampered by low ecommerce penetration…

Post Covid consumer began to flock to site alongside overall ecommerce penetration growing from ~5% to ~14% today.

And at the same time Mercado Libre decoupled their payment platform—Mercado Pago—from being an exclusive on-site payment option to being welcomed anywhere.

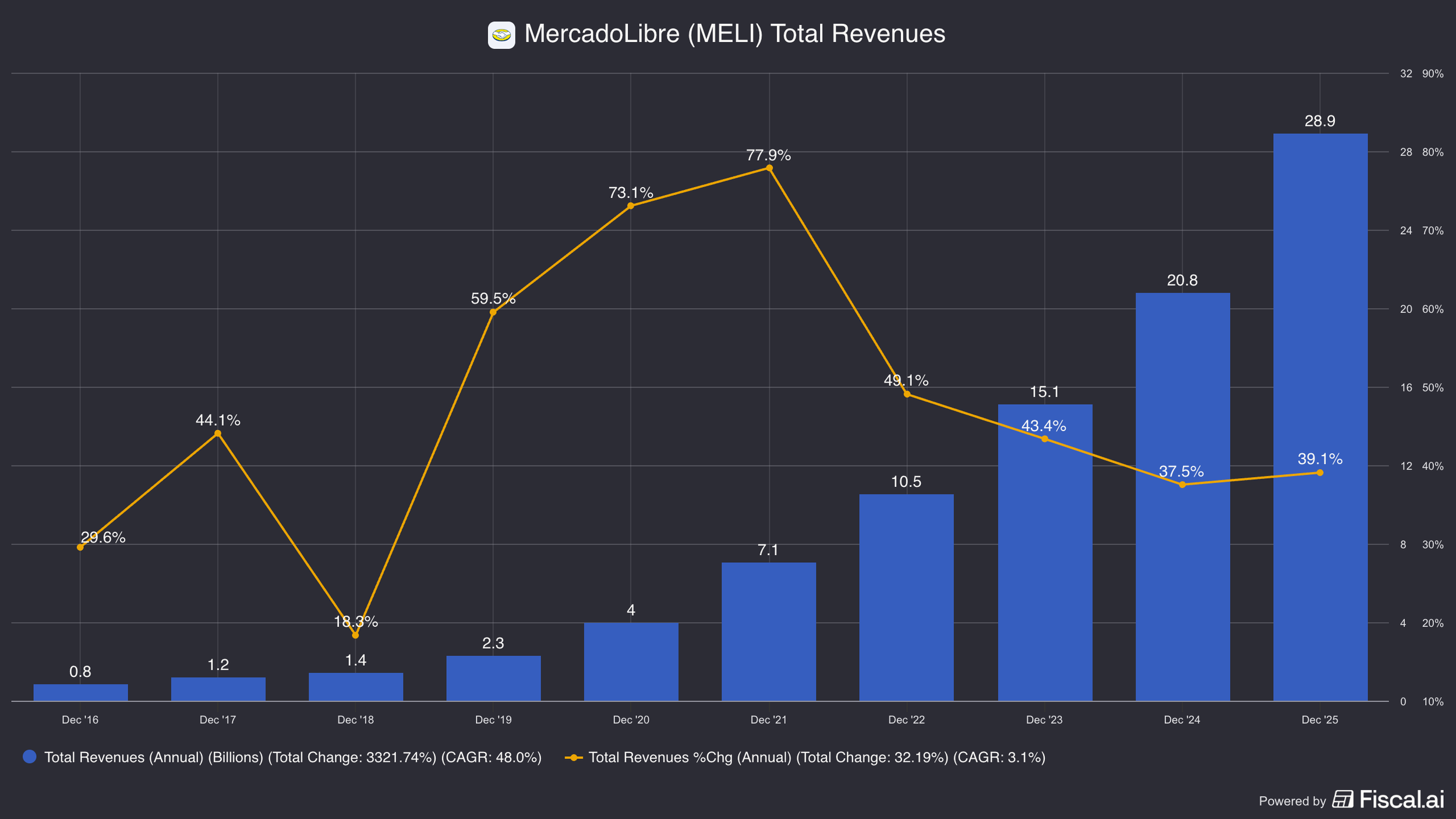

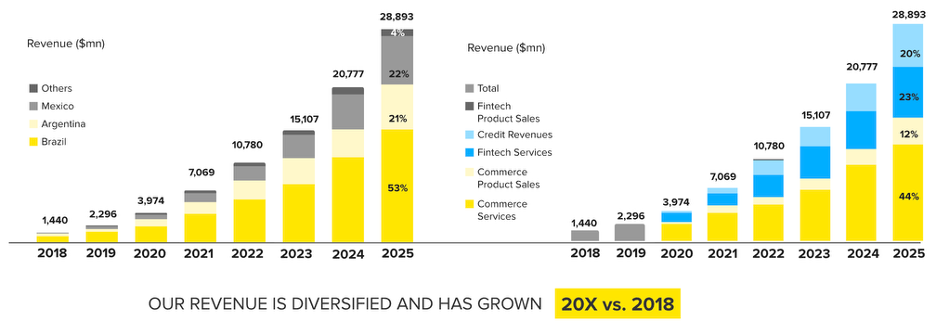

This resulted in a revenue growth accelerating massively, from 18% in 2018 to 60% a year later..

Since 2019 revenues and gross profits have more than 10x’ed!

And they are STILL growing +39% y/y on a $28 billion revenue base.

And the low ecommerce penetration rates present a long runway for growth

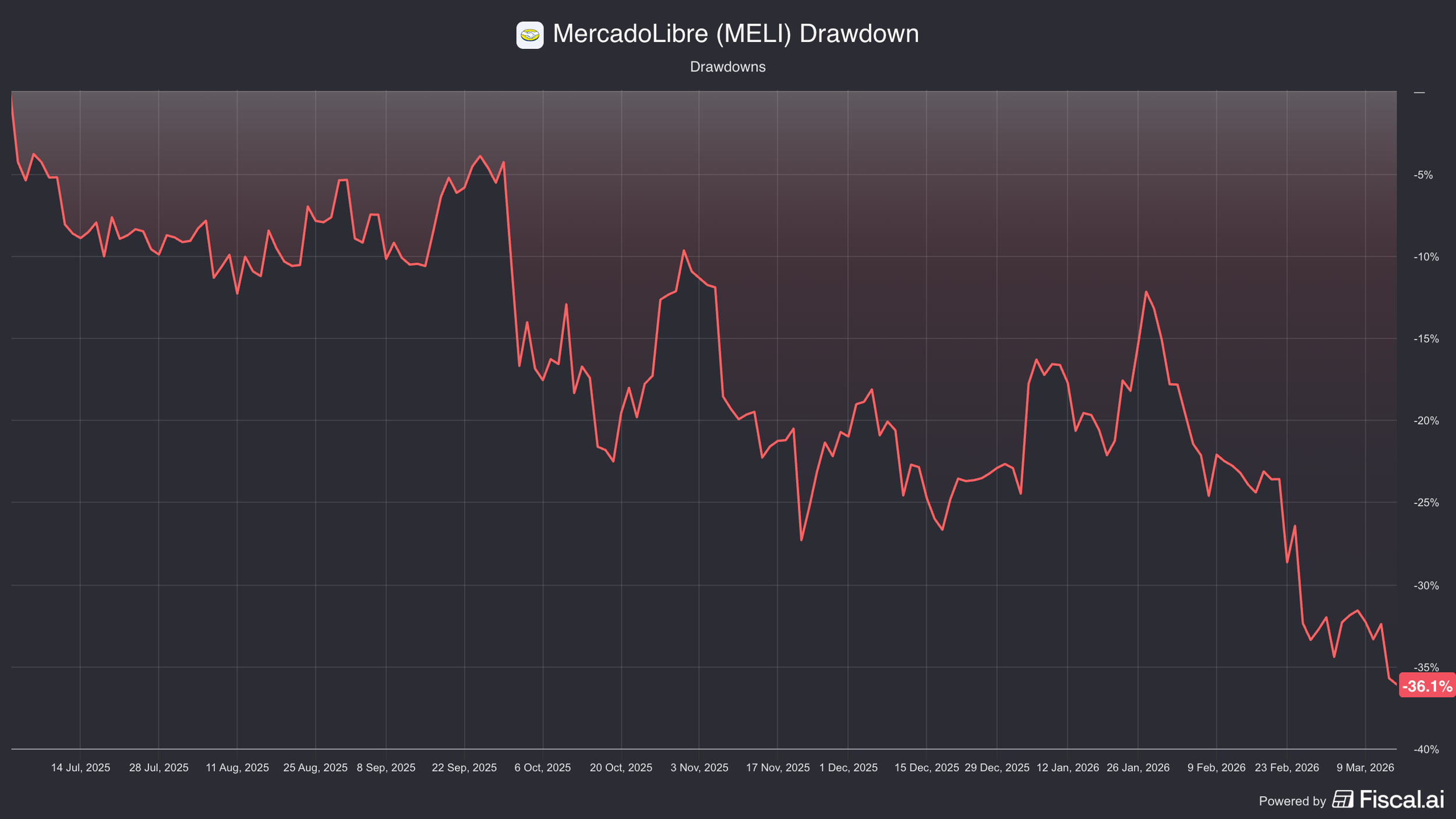

The stock has recently sold off 36% from it’s recent highs in June…

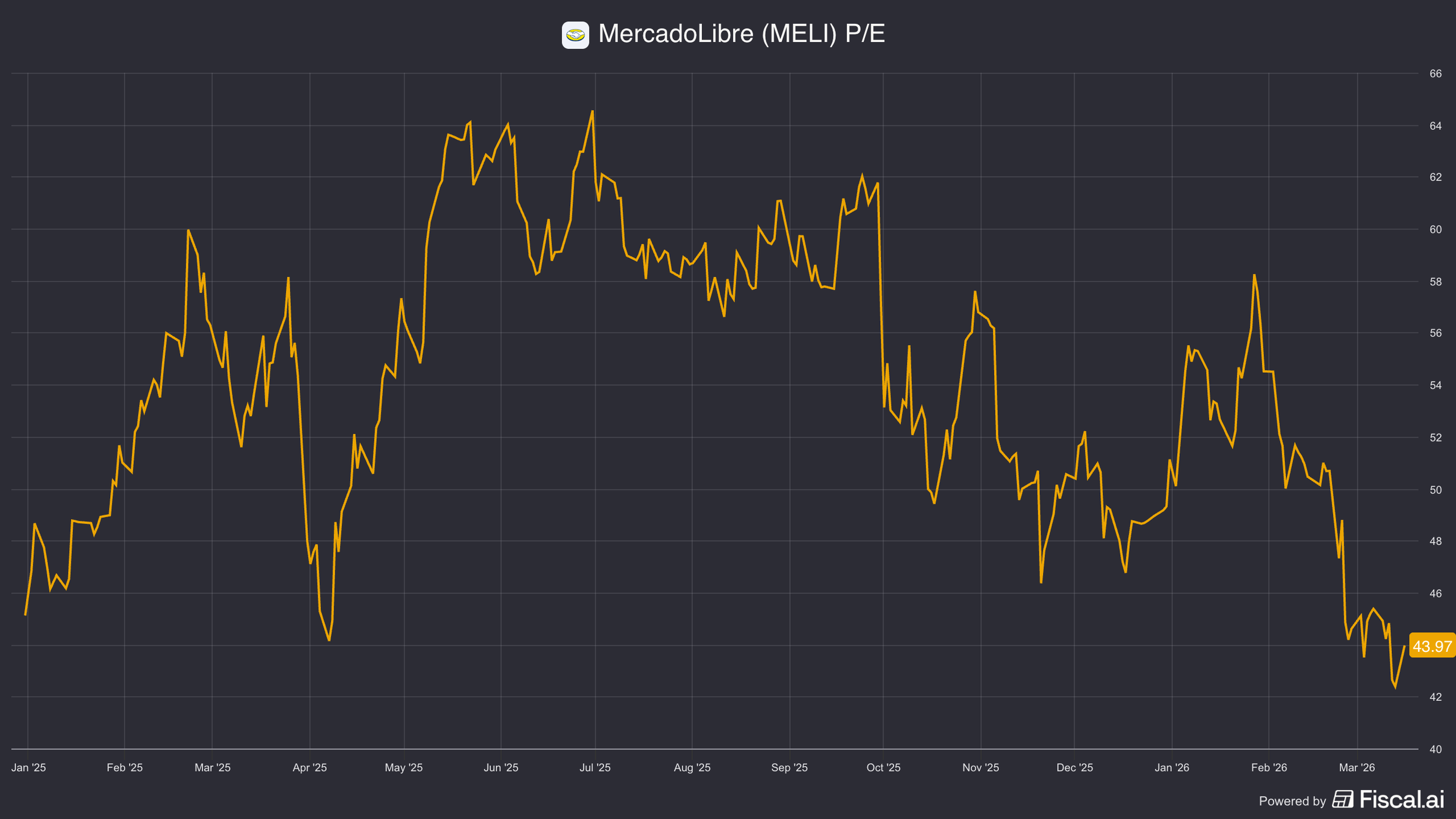

They still look optically expensive with $2.2bn of after tax profits,

At 44x trailing earnings.

But with just 3 more years of 30% growth, that multiple can drop below 20x.

And if they keep growing thereafter…

It could be an interesting opportunity for investors.

BUT…

Unlike Amazon’s dominance in the United States…

They have competition from Sea Limited who is trying to take share

And from Amazon themselves who are doubling their South American efforts.

How dominant is Mercado Libre and are they well positioned to continue to grow at such high rates?

We cover all of this and more in this week’s Five Minute Money!

Business.

Mercado Libre has revenues of $28.8 billion, growing 39%. In 4Q they grew even faster at 45% y/y.

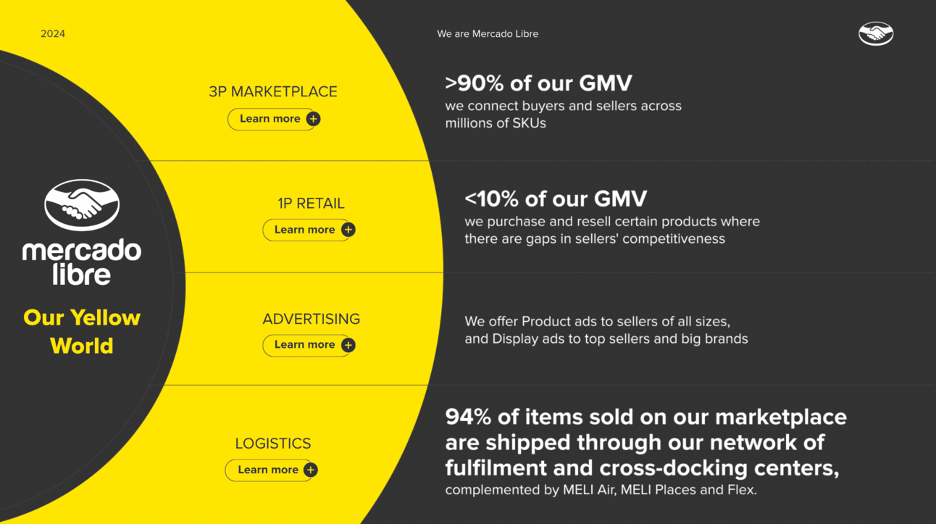

They operate through two segments: commerce and fintech.

Commerce.

Commerce includes their Mercado Libre ecommerce platform. It functions much like Amazon does.

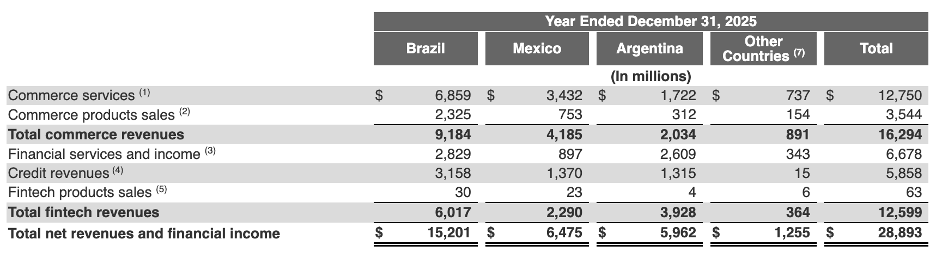

They operate in 18 countries, but their biggest ecommerce markets in order are Brazil, Mexico, and Argentina.

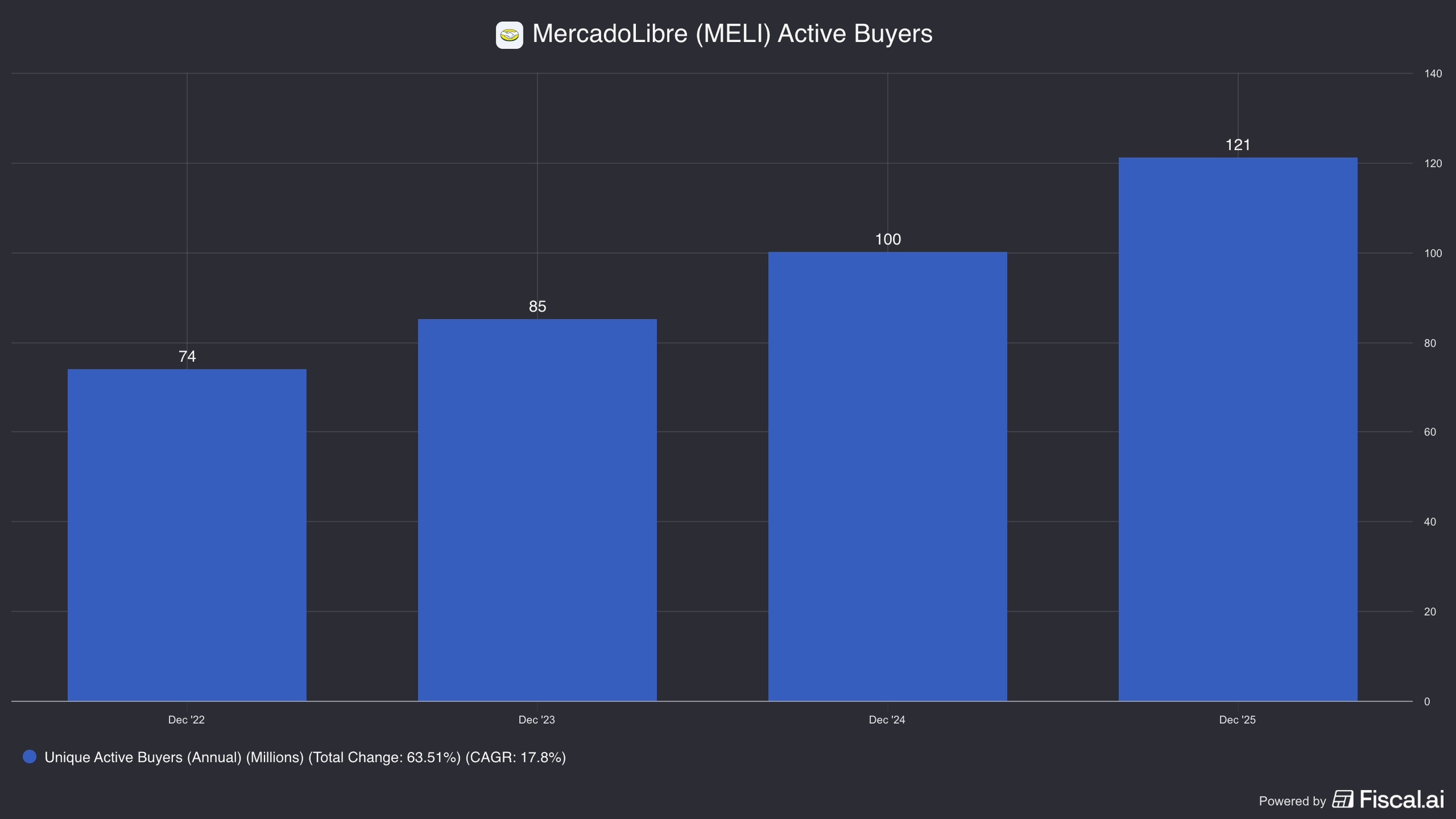

They currently have 121mn active buyers, growing 21% y/y.

In contrast to Amazon and Coupang though, >90% of their sales are through 3rd party merchants that sell on the platform, with the remaining being 1P sales—that means Mercado buys items from suppliers directly and resells them on their platform.

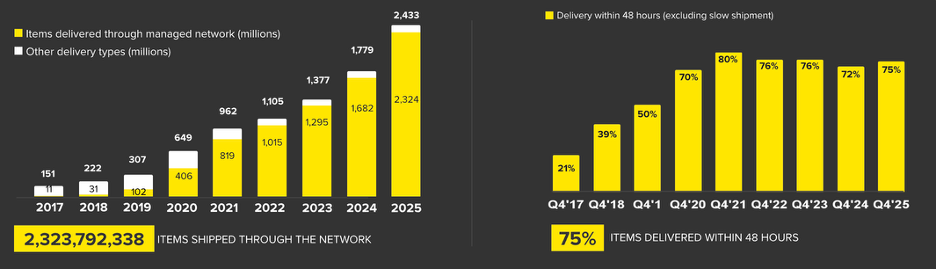

Their logistics arm, called Mercado Envios, is closely integrated with the marketplace.

75% of items sold are delivered in under 48 hours. Which is more impressive than it might sound given how massive Latin America is and how less developed the logistics network was prior to Mercado Libre.

In order to continue to gain volumes and grow their logistics network (as well as a competitive threat we will talk about later), they have reduced their free shipping threshold for the third time to just R$19 now ($3.65 per order).

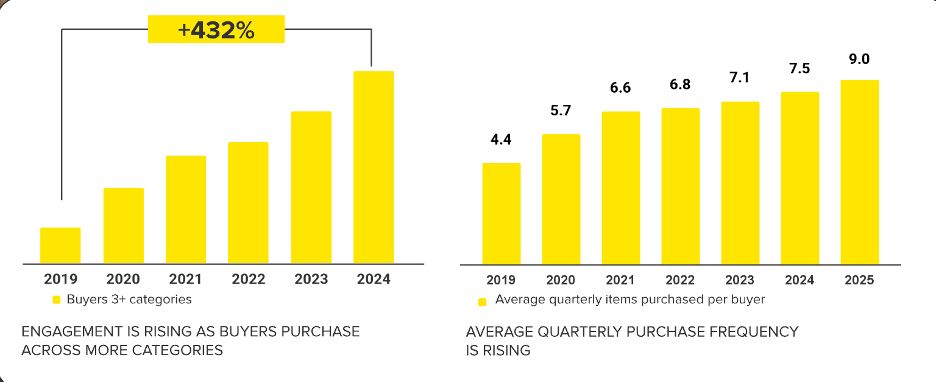

This has resulted in more buyers and growth in how many buyers purchase across 3 categories, as well as purchase frequency.

In Brazil, items sold grew 45% y/y, while unique buyers grew 25%, and GMV grew 35%.

All very important things to grow user loyalty to the platform.

This does mean that the average basket size (value of each order) did fall, but it is a trade off they are making in order to push more volumes into their logistics network, so they can spread costs across a wider number of packages.

As they noted in the 4Q25 shareholder letter: “Unit shipping costs in local currency fell 11% y/y in Brazil in Q4'25, and fell y/y in fulfillment in Brazil, Mexico, Chile and Colombia.”

Alongside the lower shipping threshold came the creation of a “slow shipping network” that can ship packages cheaper for the most cost sensitive customers. This competes with newer ecommerce players like Shopee, Temu, and Shein (more on this later).

They also are investing in their 1P business in order to improve assortment and price competitive of the platform.

Many other ecommerce players like Coupang and Amazon started with 1P, as it is important to keep 3rd party marketplace pricing in line, build out selection, and improve inventory in stock.

While 1P GMV is growing 80% y/y, they have said it won’t be more than 10% of total GMV.

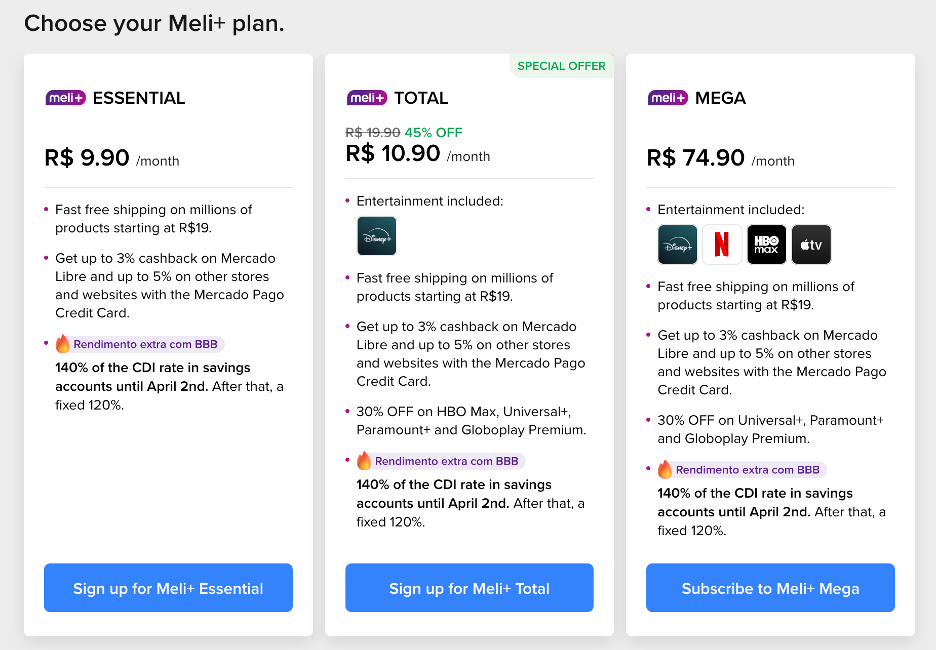

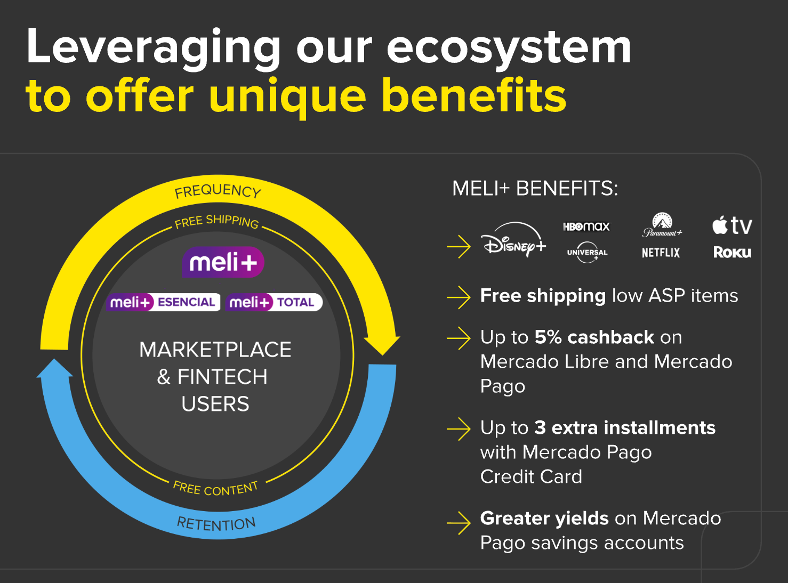

Similar to Amazon Prime, they have Meli+. However, they have 3 different plans.

Disney+ is included in the R$10.90 ($2.10/mo) plan or consumers can push to a more expensive plan (R$74.90 or $14.40 USD/mo) that gets them a suite of entertainment at price cheaper than buying each on a standalone basis.

The streaming business also works well with the product list advertising ecommerce business. Meli can use a users purchase data to help serve better ads on Disney+ for example.

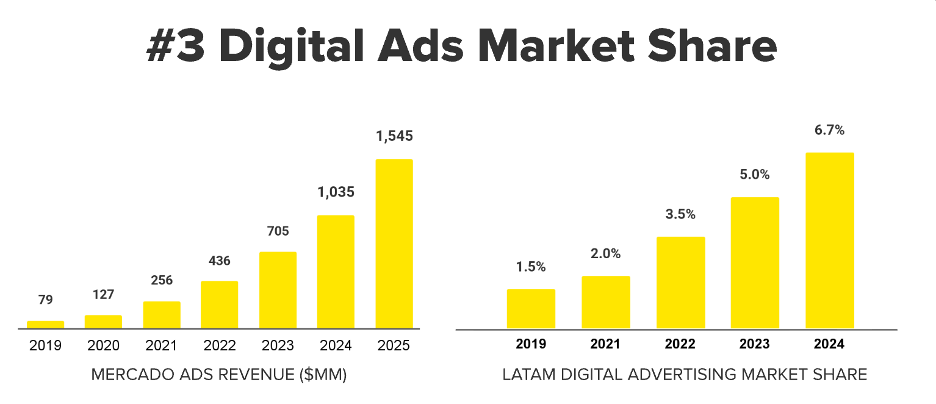

The biggest part of their advertising today though is simple sponsored search ads on the Mercado Libre marketplace. Advertising is now a >$1.5 billion business for them.

They split up commerce further into “product sales”, which is 1P and “services” which is everything else from the commission they charge sellers to logistics fees and advertising.

The average “take-rate”, which is how much a seller pays Meli, varies depending on the listing category and whether they advertise and use shipping, but it is estimated around 25%.

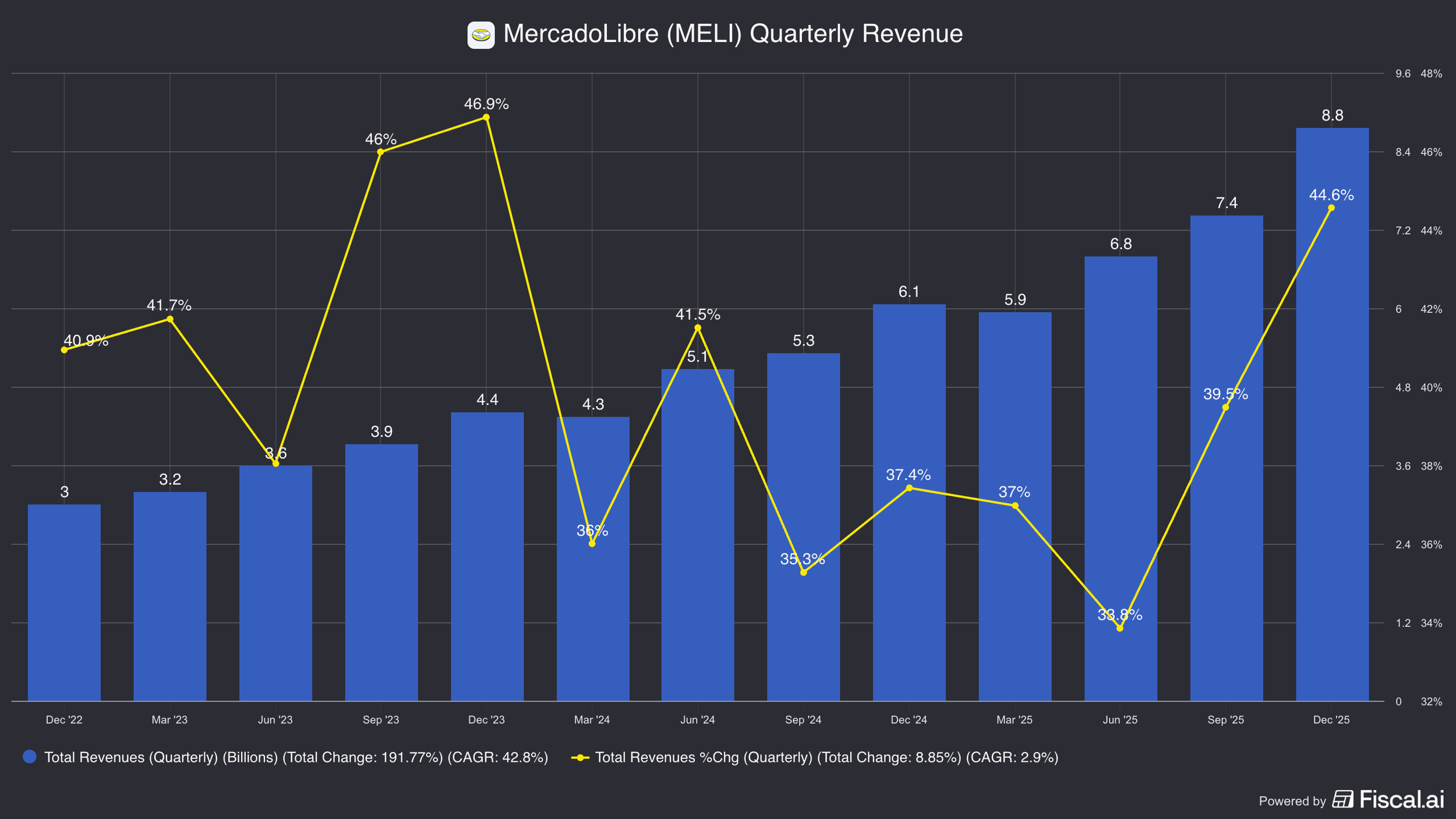

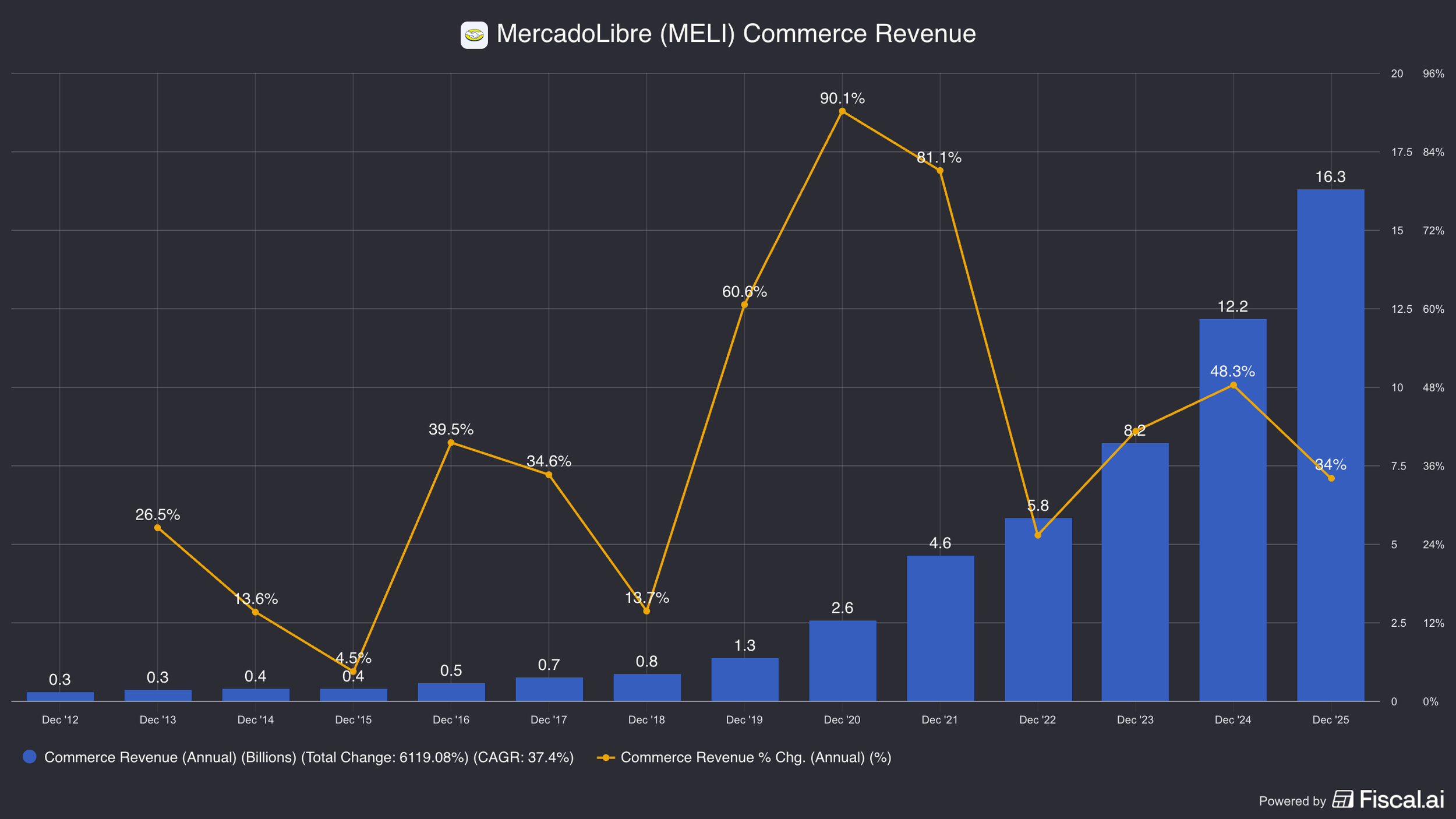

Commerce generated $16.3bn in revenues, growing 34% y/y

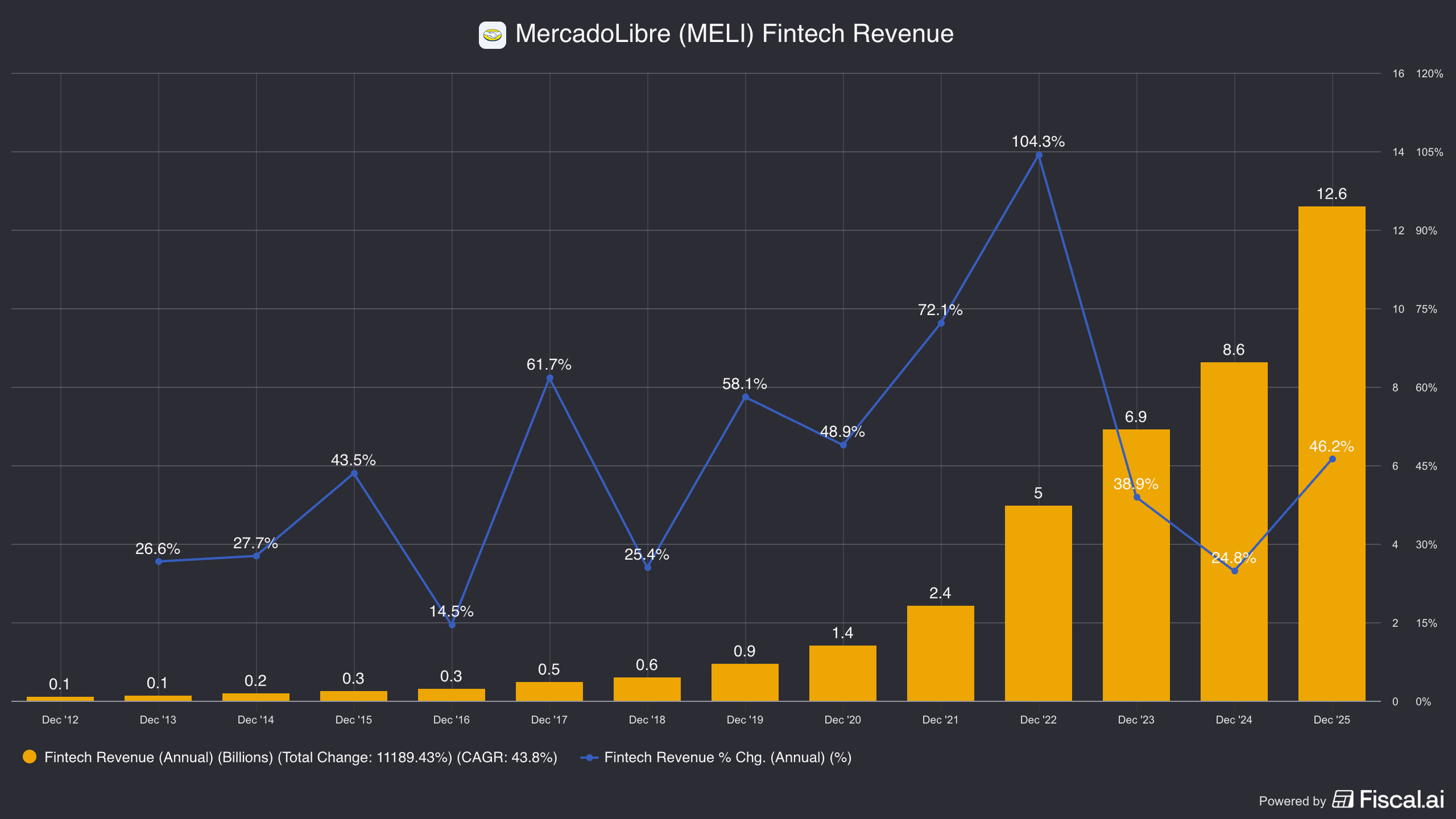

Fintech generated $12.6bn in revenues, growing 46% y/y/

Currently, commerce is 56% of total revenues with Fintech smaller at 44%.

Since Fintech is growing quicker, it is possible it overtakes commerce as the largest segment eventually.

However, the two work closer together.

Fintech.

Before talking about this business, it is important to understand the financial backdrop of LATAM.

Over 70% of the population is classified as unbanked or underbanked.

Banks tend to focus on the most affluent and credit card penetration is very low too.

Still today less than 20% of Mexican’s and 40% of Argentinian’s have a credit card.

This means that most people had no way to pay digitally.

This is where Mercado Pago stepped in. Originally it was a means to pay only on Mercado Libre, but they decided to decouple the payment means from the marketplace.

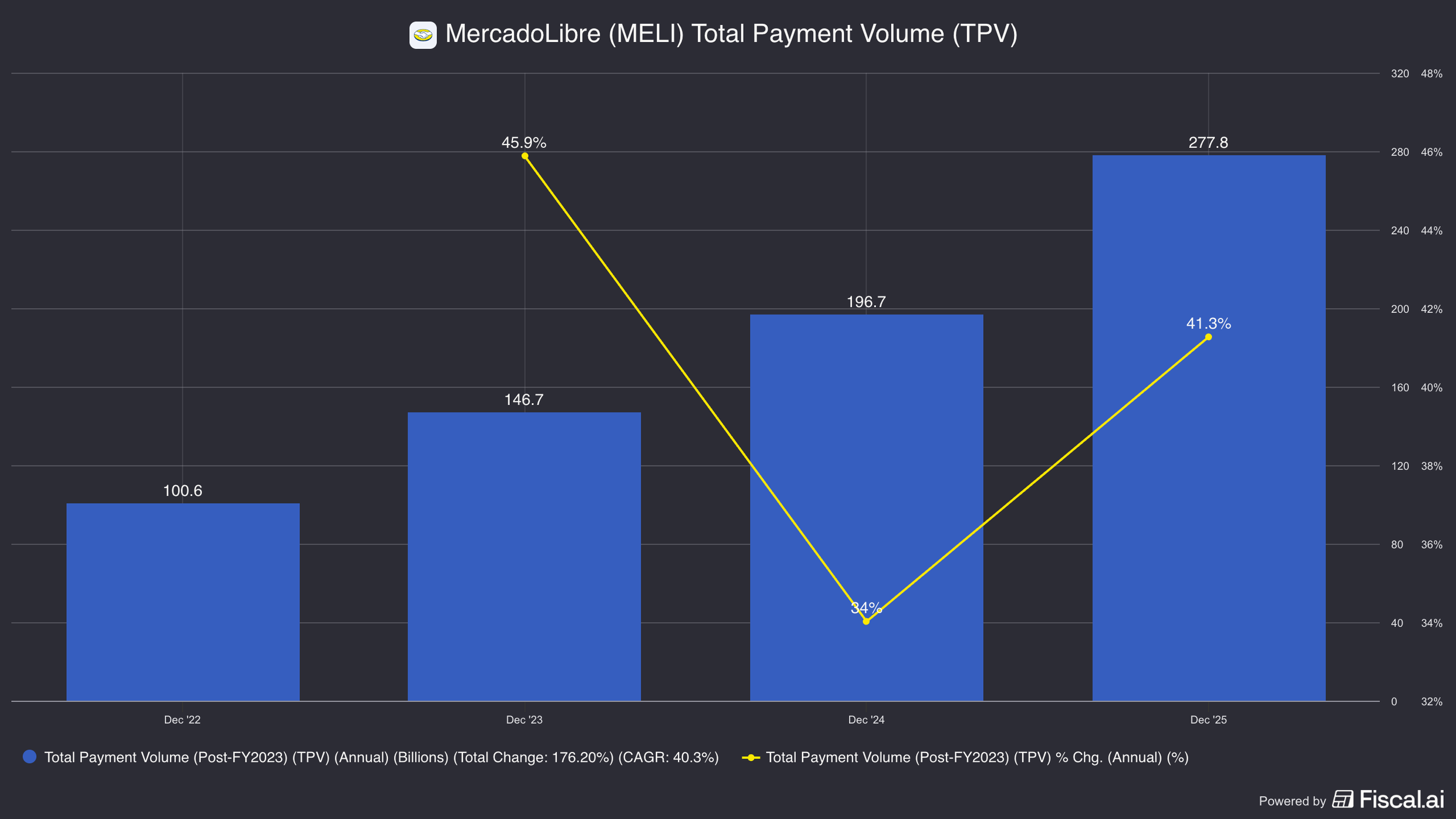

Total payment volume +41% y/y last Q

MAUs on their Mercado Pago Consumer app are 79 million, +28% y/y.

Here, consumers can use the app to pay for items, pay in installments without a personal loan, transfer money for free, pay bills, withdraw cash, make investments, send money abroad, and buy micro insurance policies for cellphones or buy basic life insurance.

(They do not offer auto loans or mortgages, which is a more competitive area.)

Users can also receive interest on the money they keep in their e-wallet, which is especially important given high inflation rates. These rates can easily exceed 15% depending on what currency you are storing money in (Argentina pays ~25% for context).

They also offer stable coins backed by US treasuries so users can “own US Dollars”, which are far more stable.

They attribute part of their growth because they offer such high rates on money stored in the app and not “treating deposits as a short-term profit pool”.

They also pioneered QR codes and payment links so even very small merchants like street vendors can accept payments without any hardware.

But they also rolled out Mobile POS (point of sale) and card reader devices.

They label all of this off-platform activity for merchants “Acquiring TPV” (Total payment volume).

And in 4Q alone, it was $56 billion, growing 33% y/y.

This Merchant Acquiring business is more competitive in Brazil, but in Mexico, their installed base of “active POS devices approaches all incumbents combined”.

Since they have data on consumers' purchases both from their Mercado Libre marketplace as well as their network of merchants and users that use the Mercado Pago app, they can “pre-approve” consumers for credit cards.

Now for anyone that knows banking history, this is typically a red flag.

But it is important to emphasize they have transaction history before they issue the card so they have some sense of what the user can afford or not.

Then they reflect this in the card limit, which isn’t large—an average for Mexico was reported around MX$8,000 or $480 USD.

With frequent use and paybacks, this can increase.

They also can offer credit cards at check out on Mercado Libre. So as a user is about to buy something, they allow them to put that on the credit card and then issue it at the same time.

Their credit models are about 1/3rd informed by this proprietary transaction data.

They have learned for instance that someone who buys supplements and workout clothes tends to be a better credit risk (read they are more likely to pay back).

These credit lines existing in the Meli ecosystem since 2019 and after some testing, they brought this ability to off-platform lending as well.

They do a similar thing on the merchant side where they know the merchants’ sales, so can offer them an appropriate amount of credit.

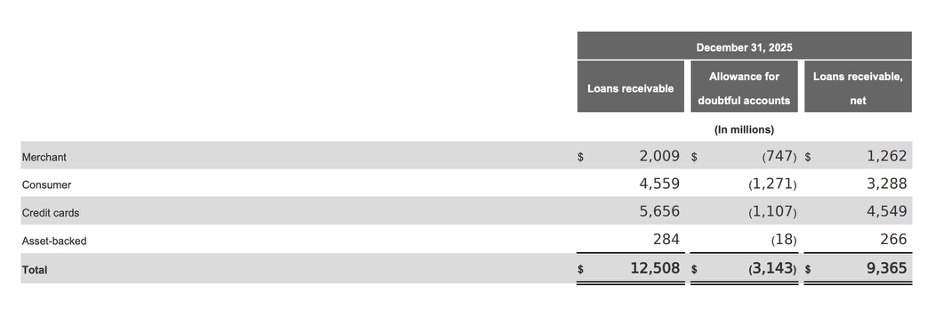

You can see their loan portfolio below, which now is ~$12.5 billion gross or $9.3 billion after expected losses.

Anyone with credit card or bank experience, might see that allowance for doubtful accounts at 25% as being very high… and it is.

This is because a lot of these consumers and merchants’ default at much higher rates than a more developed economy like the US where a bank might be around 1-2% or a credit card company with 7-10%.

The average loan duration is around 3-6 months with the highest usually at 12 months. The quick loan turnover is a good thing as it means there is less time for adverse macro events to adversely impact the portfolio (even if there is a recession, you usually don’t feel the financial pain immediately).

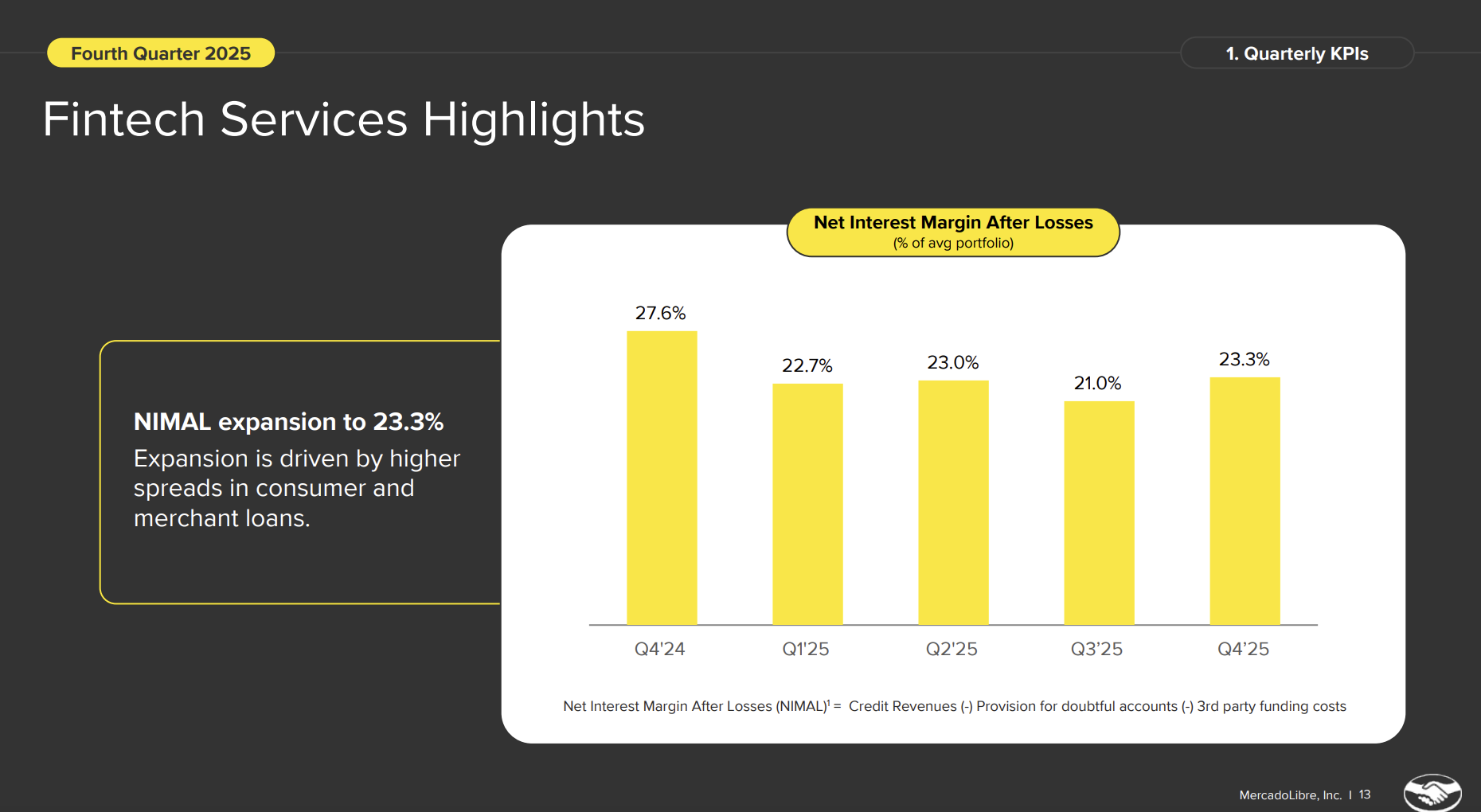

Their NIMAL or Net Interest Margin after Losses is basically what their interest income on the loans is, less the cost to fund them and less loan losses.

This figure was around 23% for them. For context, many banks have NIMs (net interest margins before losses) of around 3-4%.

This figure is very high because the going rates for credit commonly exceed 100% in these countries because of the high loss rates (and inflation).

There is margin pressure because of an accounting standard called CECL.

In short, they have to provision against the entire expected loss of the loan today, instead of just how much they expect to lose in a given quarter or year.

This means as they grow, the loan loss provisions are higher than their expected losses in a period. (Loan loss provision in an expense on the P&L).

The accounting treatment from CECL combined with a huge new issuance of credit cards, drove a 2.5% margin hit.

Mercado Libre doesn’t keep all of these loans on their balance sheet . Instead, they securitize a lot of them.

That just means they bundle the loans together and sell them to others.

Often though, they keep the “junior” portion of the securitization. This is done so lenders feel good about buying the securitizations from them because if the loans default beyond want Mercado Libre models them too, Mercado Libre takes the first loss before anyone else.

This means that they are eating their own cooking. If their credit risks models are wrong, then they could see large losses.

If they are right, then they make a pretty good credit-risk adjusted spread on them.

The two businesses work together to create a sort of ecosystem.

The Mercardo Libre marketplace acquires users and merchants and can use that transaction data to feed credit profiles.

At the same time, by tying payment to Mercado Pago’s various credit offerings, they have created a very low cost way to acquire new users.

Users who use Mercado Pago credit cards also get cash back on Mercardo Libre purchases, incentivizing more activity.

Meli+ also offers members enhanced benefits like better savings rates and more installment payments.

Let us talk next about competition.

Competition.

Mercado Libre was an early entrant in ecommerce in Latin America and commanded the market.

As the Meli lore goes, when Amazon launched in Mexico, which was one of its largest international launches ever, CEO Marcos Galperin saw the writing on the wall.

Prior to this they had been a capital light business and avoided all of the expensive and complicated tasks of taking over logistics.

He knew though that if they didn’t, Amazon could…

And that could be goodbye to most of their business.

Thus they started investing heavily in distribution centers, cross-docking facilities, and vans and planes.

This neutralized the Amazon threat, but Amazon still was able to capture meaningful market share in Mexico, particularly in the big cities.

They are also used across South America for higher end purchases, especially expensive electronics.

Amazon has a position in Brazil, but Mercado Libre is used much more often.

After addressing this threat, a new one popped up: Shopee.

Shopee is the ecommerce platform of Singapore-based Sea Limited.

They aggressively expanded across the global post Covid as ecommerce was booming and capital was freely available.

They launched with 0-5% seller fees in Brazil and heavily subsidized early sales.

Shopee also leveraged Free Fire, a mobile video game they owned, that had a very large presence in Brazil by offering in app free virtual items for users who downloaded the Shopee app.

While investors were highly skeptical they would ever be able to make a business profitable that sold extremely cheap items, usually with an average order under $10, in 2025 they announced they were EBITDA positive in Brazil.

Part of their success came from onboarding local sellers instead of relying on mass market, cheap goods shipped from China.

In fact, Sea management claims by volume they are the largest seller in Brazil today.

However, despite the lead by orders, their far lower average order prices means that their market share is a fraction of Meli’s by GMV (some estimates put Meli around 40% versus Shopee at 15%).

And while they built a foothold in Brazil, they have all but pulled out of the rest of South America and only serve cross-border trade there.

Cross-boarder trade is harder now though with new import tariffs and the removal of the de minimus exception that a lot of ecommerce companies were using to ship cheap goods.

Shopee could also see a headwind with a new Brazil tax system. In short, a lot of sellers are (alleged) to register as individuals on the platform (CPF) instead of as businesses (CNPJ) and they weren’t required to issue formal digital invoices, which made it easier to evade taxes. A new tax law and system is in it’s pilot phase and will pull the taxes out of every purchase (and make platforms like Shopee responsible for making sure it is implemented). This doesn’t impact Mercado Libre because they required CNPJ registration to sell on their platform.

So to summarize, consumers tend to use all three apps but for different things.

Shopee is used for cheap items and their app makes it fun to discover new things to buy and it’s gamified. Users don’t expect quality from them.

Amazon is used primarily for high end electronics, books, and some other higher end categories.

For the vast majority of people, Mercado Libre is their “staple” ecommerce platform. This is where they buy virtually everything else.

To address the Shopee threat though, they lowered their free delivery minimum to R$19. This resulted in 45% item sold growth and 35% GMV growth in Brazil.

To address Amazon, they keep investing more in logistics infrastructure.

Generally speaking, Brazil is their most competitive market with competition from Shopee and Amazon.

Amazon actually is partnering with Rappi (like a South American DoorDash) and Nubank (LATAM Fintech) which is a new vector of competitive threat vs historically.

While Meli has carved a large chunk of market share out, they do have to keep fighting for it and in order to grow.

Right now it is legacy players like Americanas and Magalu that are the first to lose share.

Amazon is still investing in Mexico, but is focused more on AWS and other more profitable ecommerce markets internationally.

Meli is still pouring billions into infrastructure in Mexico and has a big advantage by coupling retail with their Mercado Pago credit.

Argentina is Mercado Libre’s home market and they have dominance there in both ecommerce and payments.

Other countries like Chile, Peru, Columbia, are smaller today, but also don’t have much competition.

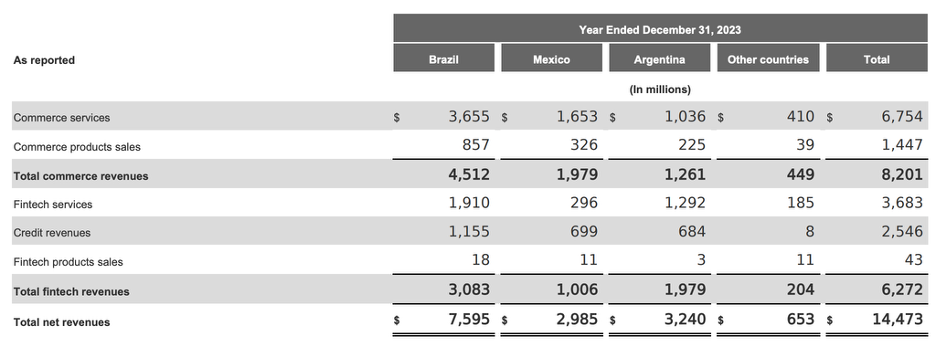

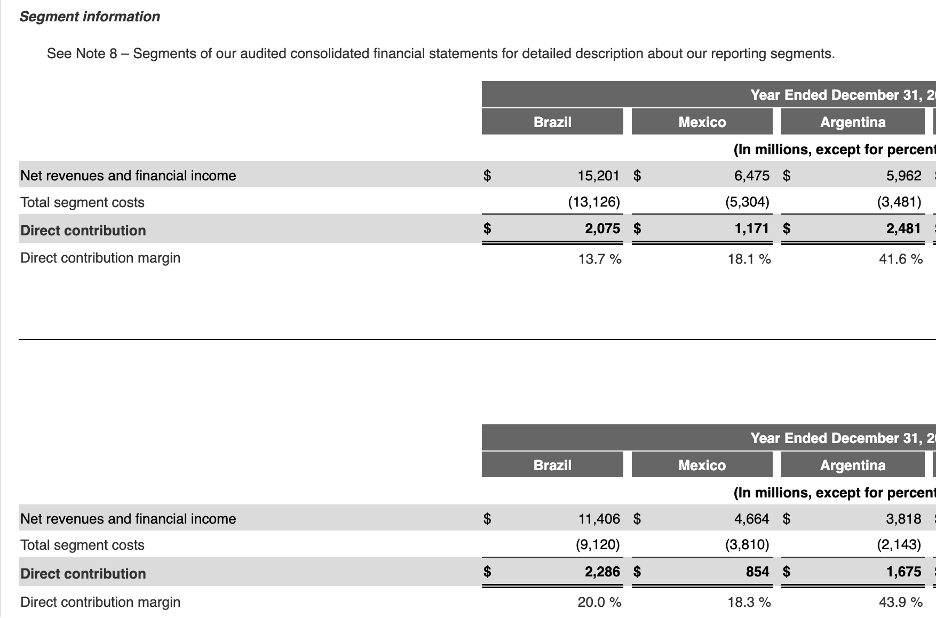

We can see below that Argentina is the most profitable market for them, despite revenues being only $6bn versus Brazil’s $15.2bn.

Part of this is by choice as they invest back into Brazil via free shipping and increasing their credit card issuances.

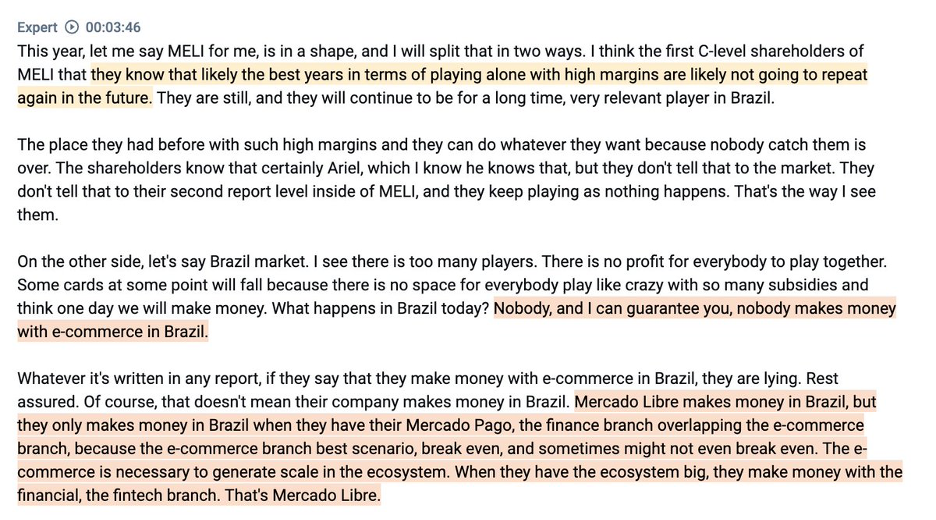

The more bearish read though is that they were forced to do this and competitive intensity will mean this is always a rough market. The former President of Brazil Shopee thought that no one in Brazil was making money on ecommerce and Mercado Libre might make money only with the financing arm.

He was at Shopee at the time they were spending money without much cost discipline.

Since then, Shopee has raised their take-rates to be close to what Mercado Libre charges.

And Mercado has already noted they have seen reduction in shipping costs per unit from the volume increases, as well as increased purchase frequency, all of which suggest it could improve their competitive positioning and profitability longer term.

The other leg of competition comes on the fintech side.

Nubank is one of Mercado Pago’s most formidable competitors with 131mn customers versus Mercado Pago’s 78 million MAUs (not exactly an apples-to-apples comparison)

Nubank also has a particularly strong hold on the Brazilian market with some estimates putting them at 60% of the countries adults.

This is the most competitive market for Mercado Pago, but it is worth mentioning that consumers can have more than one banking app, and it could be worth it with perks like cash back on Mercado Libre. (Some estimates put Mercado Pago around 40-50 million users in Brazil).

Mercado Pago dominants Argentina and Mexico is the latest breeding ground for competition. Nubank is smaller here with 13 million customers and Meli is aggressively attacking this market.

There are other fintechs in each smaller LATAM country and it is also a different set of competition on the merchant acquiring side, including Stone and PagSeguro in Brazil who are the largest.

That is all to say there is no forgone conclusion that Mercado Libre continues to win incremental market share, but they certainly are the most formidable competitor in ecommerce and have a unique value prop in fintech.

Growth and Valuation.

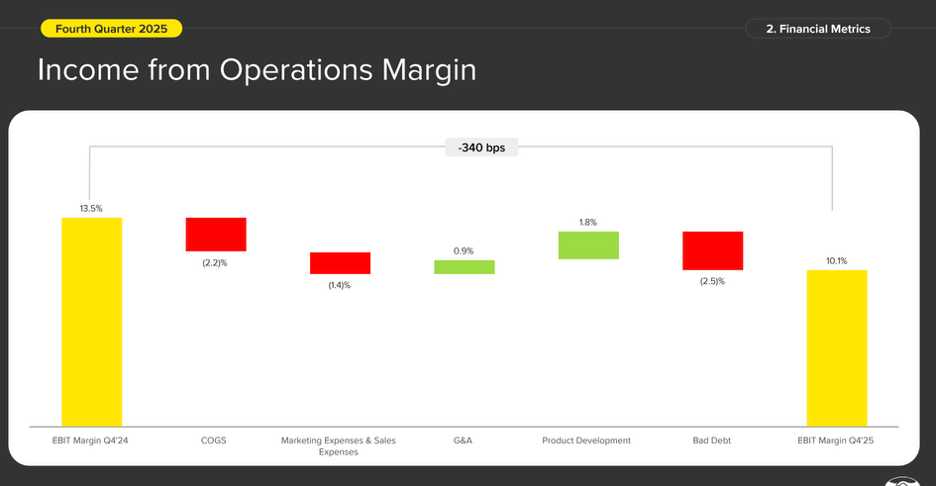

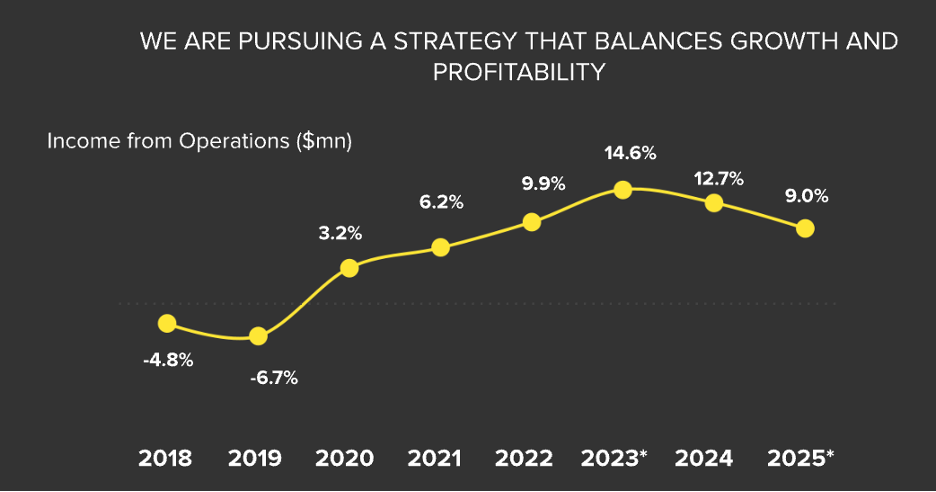

As they have invested, their margins had decreased.

They note that in 4Q these growth investments weighed on operating income by 5-6 points, which makes sense—that is where they were in 2023.

While they are investing for growth now which is holding back margin, they also have the opportunity for margins to expand even beyond the prior 15% from advertising (both on the marketplace and by supporting their TV streaming partners ad businesses), as well as improvements in their logistics operations and credit risk underwriting.

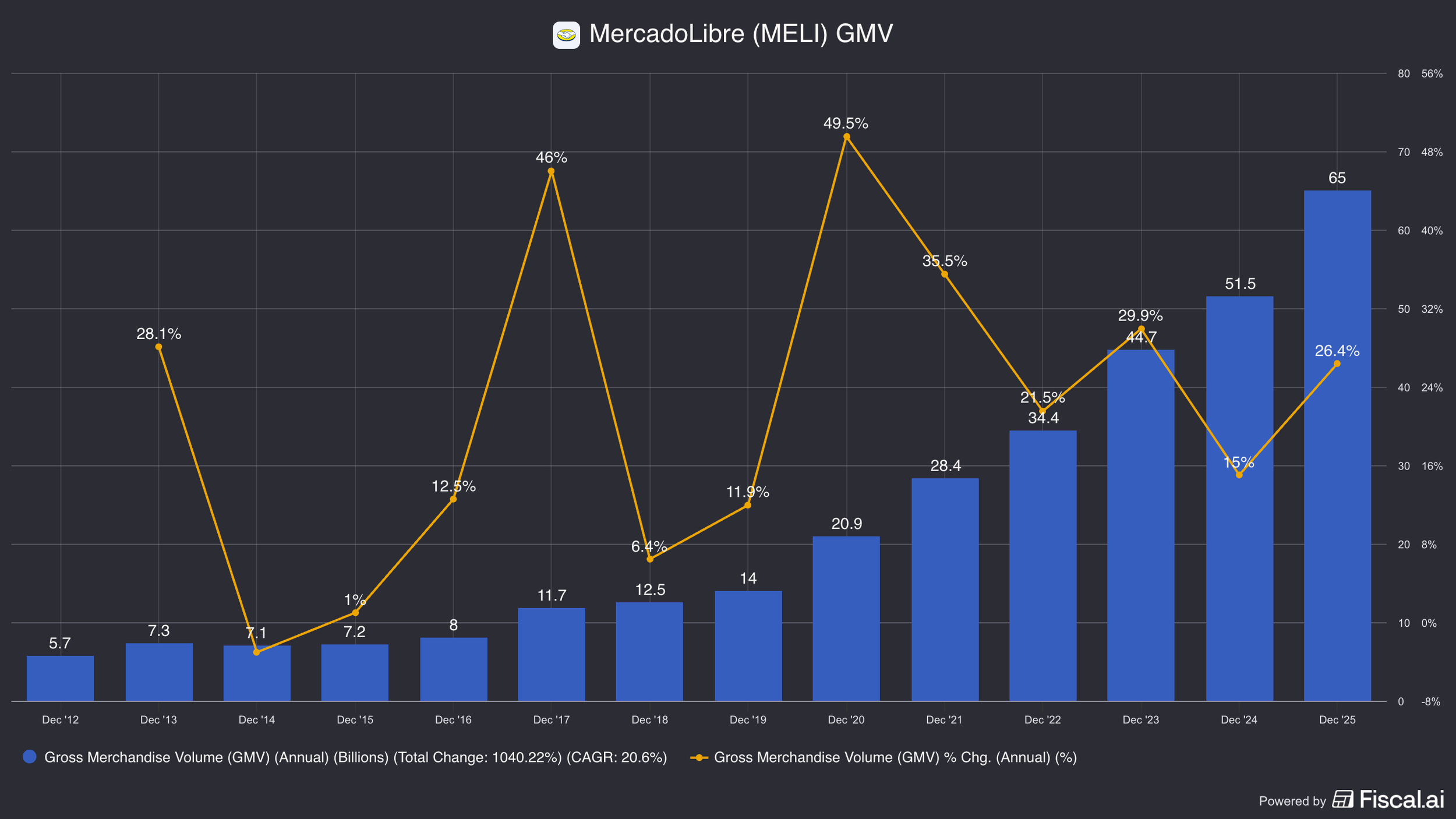

They have $65 billion of GMV in 2025 and currently ecommerce penetration is about 15%.

This is much lower than the United State’s 25% and many Asian countries above 30%.

Last quarter GMV grew +36% and was run-rating closer to $80 billion.

The ecommerce market is growing a mid to high teens rate.

If assume a 20% growth rate for 3 years, that is about $$112 billion in GMV.

An estimated margin range on GMV at maturity (no more investing for growth) would be 4-8%.

For context, in Amazon’s North America business—probably the most mature and highest quality ecommerce market in the world because of the limited competition and high average incomes—is around 6% EBIT as a % of GMV.

This is a rough estimate as they don’t report GMV, but it is directionally correct. With $68 billion in advertising globally, analyst expect the majority of their ~$32 billion is profits in North America come from advertising.

Mercado Libre is in a more competitive market and so their EBIT as a % of GMV is likely going to be lower at maturity. They do have the option though that advertising grows beyond GMV because of their off-marketplace ad business, but that is not likely to be too material to the valuation.

A 4-8% range gets us $4.5 to $9 billion in EBIT, with $3.2 to $6.4bn in NOPAT.

The fintech business is harder to model out because of the combined earnings streams from payment acquiring, on-network payment processing, as well as the various lending businesses and asset management business.

They have $12.6bn in fintech revenues and grew that 35% y/y.

Looking at some banking and payment comps, a 30-40% margin seems fair (Nubank is at 35% currently and Synchrony is a US-based, pure play credit card lender that is at 30%).

If they grow 20% for 3 more years, that gets us $22 billion in revenues, which at that margin range gets us $6.5 to $8.7 billion in pretax profit or $4.5 to $6 billion after tax.

Putting those two estimated ranges together, we get $7.7 to $12.4 billion in mature margin earnings.

At their current stock price of $1,670, their market cap is $85 billion.

This means in 3 years they could be trading at 7x to 11x mature margin earnings.

Remember though, these aren’t actual earnings estimates, they are what the company could be making if at that time they stopped investing and started harvesting for cash flow, which of course is unlikely, but is how you should value a business so you are valuing the full profitability of the existing assets.

Now it is worth emphasizing that a 20% growth rate for 3 years is not a forgone conclusion.

And this mature margin framework could be wrong if competitive intensity continues to be high—these may just be structurally less profitable markets.

The high end of our estimates could also be too optimistic. Amazon hasn’t even achieved 8% EBIT as a % of GMV in North America yet.

And their credit lending could prove to be somewhat cyclical with worse losses than expected.

There is also the risk of more financial regulation capping their profits.

Or a macro risk wrecking a country’s operations like what happened with Meli’s Venezuela operation and they had to basically pull out of the country.

However, if you are comfortable with the risks and Meli could achieve just the low end of these revenue estimates and investors had confidence in the low end of the mature margin structure, then they a fair multiple 3 years could be:

20x if growing mid to high single digits —81% upside or 20x/11x.

25x if growing low double digits—121% upside or 25x/11x.

Or 30x if growing 20%+ still—171% upside or 30x/11x.

Ultimately, it is up to an investor to decide what they are comfortable assuming.

For more on Mercado Libre, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.