Why Unrealized Stock Gains Act Like a 0% Loan

Get smarter on investing, business, and personal finance in 5 minutes.

Congratulations!

You bought a stock and it went up.

Let’s say you’ve held it for a period of time, and now you’re trying to figure out whether or not you should sell it.

Part of you thinks, “It’s a pretty good company, but it’s kind of expensive now.”

Then again, on the other hand, you don’t want to pay all the taxes.

If you do end up selling it, then you have to find something else to invest your money in.

There are all sorts of different things to think about when selling a stock, but I really want to focus on how taxes can factor into that decision.

This is a real example from my own experience.

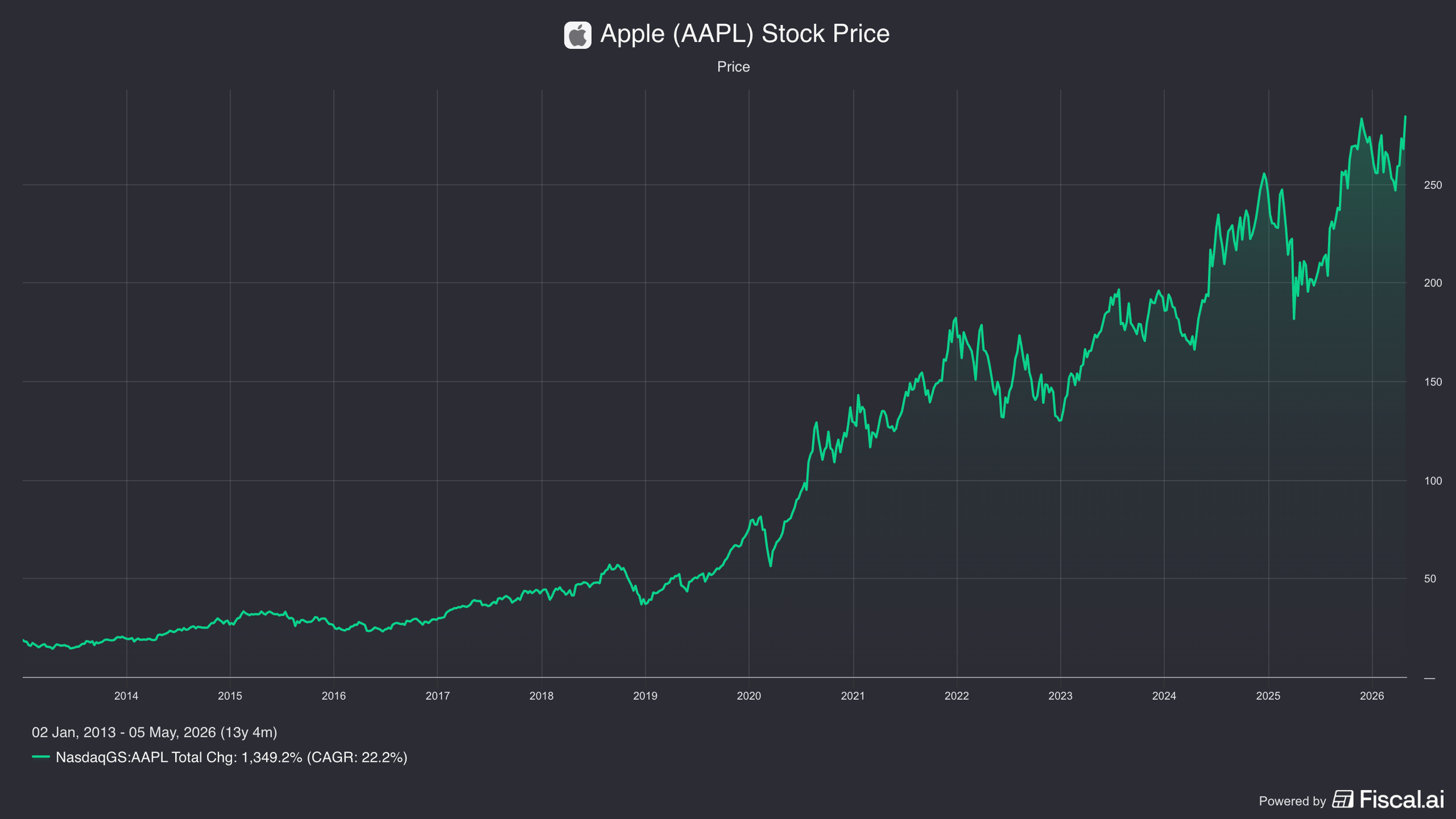

After I was done with trading and speculating, I found value investing and Buffett. That led me to make my first “real investment” in Apple stock.

It was one of the first investments I made after doing real research and analysis on a business, back in 2013-2014.

I paid a split-adjusted price of around $15 a share, give or take a few bucks.

I still held those shares more than a decade later.

That means I have a pretty large embedded gain in those shares.

Taking that split-adjusted price and the current Apple stock price of $275, that’s an embedded gain of about $260 per share.

So how does that factor into the decision of whether or not to sell the stock?

Uncallable Interest-Free Loan.

One way to think about this is that deferred taxes are essentially like an uncallable, interest-free loan from the government.

Let me explain.

We have this $260 embedded gain in Apple stock.

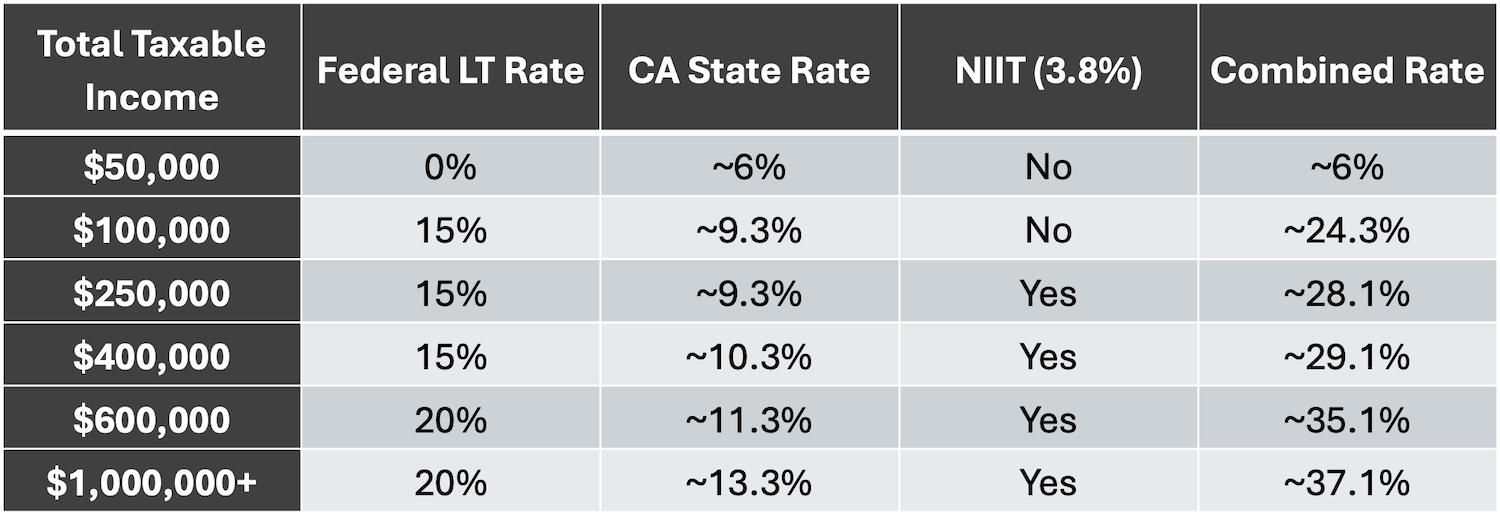

If I were to sell Apple stock today, I’d be paying taxes.

I’d be paying federal taxes, state taxes, and net investment income tax.

That’s three different taxes right there.

Depending on the country or state you live in, your taxes will be different.

But those taxes can add up.

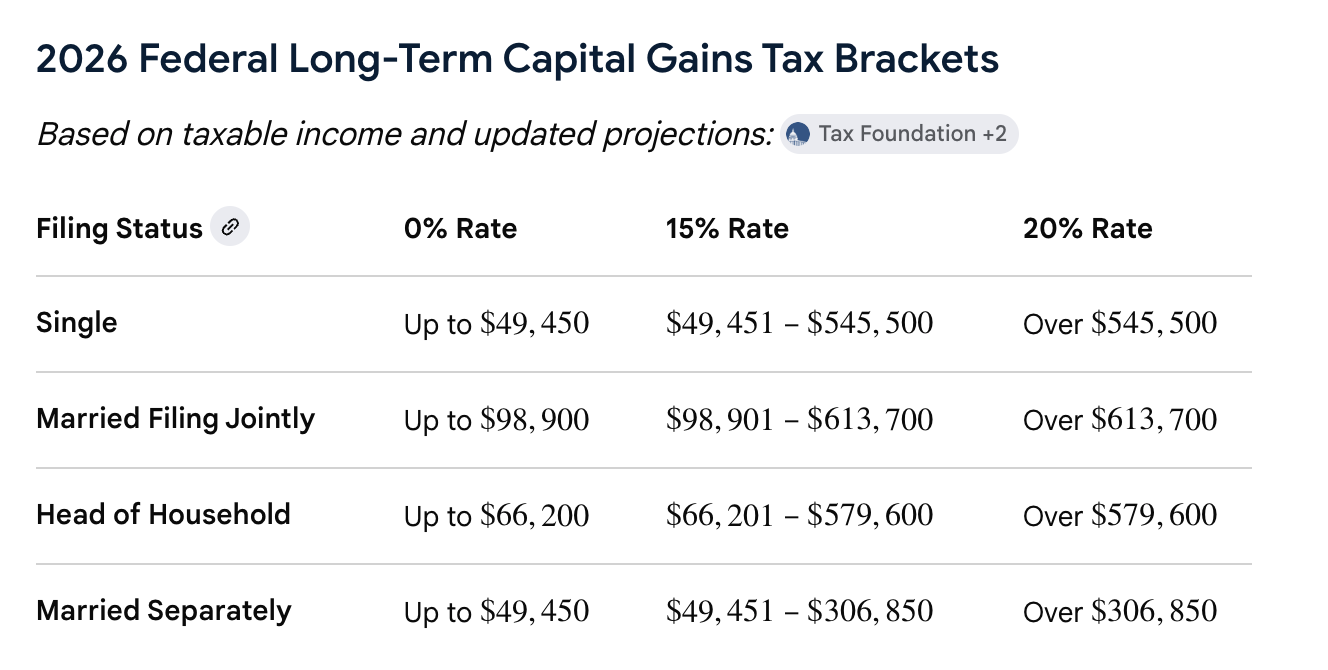

The federal tax bracket on long-term capital gains ranges from 0% to 20%.

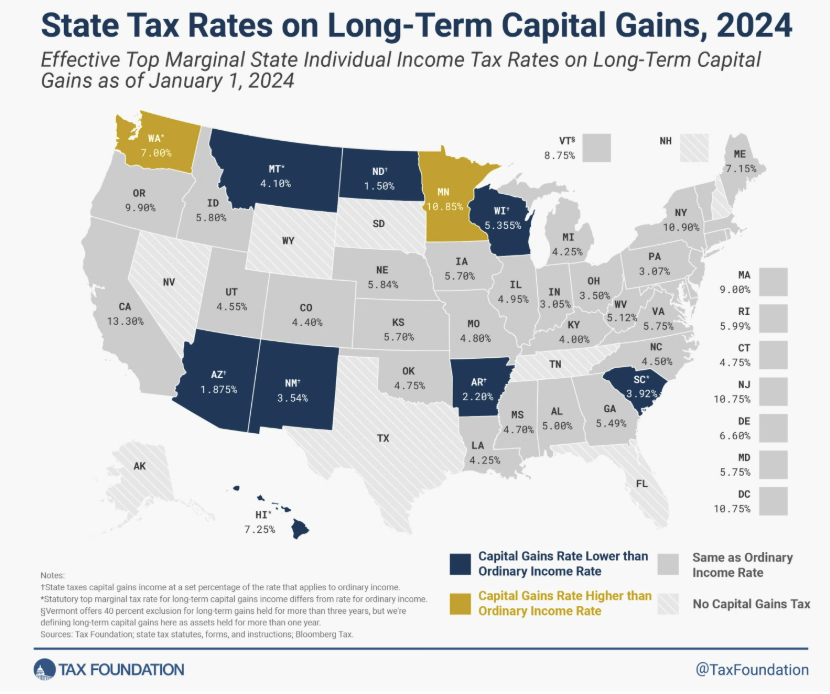

California state tax, where I’m based, ranges from around 1% to a little over 13%.

Then you also have the net investment income tax of about 3.8%.

Add all those up, and at the high end, you could be paying about 37% in taxes.

That’s a lot.

There’s also a difference between short-term and long-term capital gains.

For federal taxes, short-term capital gains are taxed basically the same as ordinary income.

That means the marginal tax rates are even higher.

For state taxes like California, they don’t distinguish between short-term and long-term gains.

No matter what, they tax you the same.

The math is basically this:

Apple stock is at $275 today.

Let’s say the cost basis is $15 per share.

That means your gain is $260.

Now take that 37% tax rate and multiply the $260 gain by the 37% tax rate. ($260 x 37% Tax)

That gives you your tax liability if you sell the stock today.

That comes out to about $100.

What this means is that if I sell one share of Apple today, my net proceeds are not actually $275 per share, they’re really closer to $175.

I get $275 from the sale, but then I pay the government $100 in taxes.

Because of that, we can think of my Apple investment as having an interest-free loan from the government.(Or some may prefer to think of the government as having an equity interest in your position, which is paid out upon sale, but that is a bit more complicated).

The government can’t call the loan as long as I continue holding the stock.

That money stays invested in Apple on my behalf.

That $100 I’ll eventually owe in taxes can continue compounding inside the investment.

It’s essentially an interest-free loan from the government.

The byproduct of that is I can have more money invested in Apple than I otherwise could.

Because of that, I can also accept a lower return from Apple than I would need if I sold it and bought another stock today.

Accepting a Lower Return.

Let’s say I want at least a 10% return on my investments.

If I think about the extra $100 per share effectively invested in Apple, maybe I only need around a 7% return from Apple to achieve the same result.

That could be equivalent to selling the stock, paying the taxes, and reinvesting elsewhere at a 10% return.

That’s because we effectively have leverage on the position.

The deferred tax acts like leverage.

That leverage allows us to earn the same effective return even with a lower return on the total investment.

It’s a really interesting way to frame the decision of whether or not to sell a stock.

When you have a large embedded gain, a significant portion of the money will go to taxes if you sell.

By keeping the investment, you effectively keep more money working for you.

When you have a large gain in a stock, think carefully before selling it.

Remember that paying taxes means you’ll have less money available to reinvest elsewhere.

Of course, if you do sell the stock, there are other considerations.

Maybe you have losses in another position that can offset some of the gains.

That changes the math as well.

You also might be in a lower tax bracket.

If your income is below certain thresholds, you may not owe federal taxes on smaller gains.

You also may live in a state that doesn’t charge capital gains tax.

Of course, if you do sell the stock, there are other considerations.

Maybe you have losses in another position that can offset some of the gains.

That changes the math as well.

You also might be in a lower tax bracket.

If your income is below certain thresholds, you may not owe federal taxes on smaller gains.

You also may live in a state that doesn’t charge capital gains tax.

There are definitely lots of other considerations, but anytime you think about selling a stock with a large embedded gain, remember that a good portion of that money disappears once you sell the position.

Because of that, you might be willing to accept a slightly lower return from the stock.

This is especially true when you’re talking about a great company like Apple.

Maybe Apple is trading around 30 times earnings today instead of the low-teens multiple it had when I originally bought it.

That’s a lot of multiple expansion.

But when you also factor in the large embedded gain, it’s almost like you’re owning the stock at a lower multiple in a way.

At the end of the day, taxes shouldn’t be the only reason you hold a stock.

In fact, taxes should never be the primary reason you make any investment decision.

But they absolutely should be part of the equation.

Because when you own a great business for a long period of time, that deferred tax liability becomes a hidden asset.

It allows more capital to stay invested and continue compounding for you over time.

So before you automatically sell a winner because the valuation looks a little expensive, take a step back and think about the after-tax math.

Ask yourself:

“Can this business continue compounding at a good enough rate to justify keeping that deferred tax advantage alive?”

Sometimes the answer will be no.

But other times, the best decision is simply to keep holding a great company and let time continue doing the heavy lifting.

For more on how taxes can affect your investing decision process, check out this video below.

Nothing in this newsletter is investment advice nor should be construed as such. Contributors to the newsletter may own securities discussed. Furthermore, accounts contributors advise on may also have positions in companies discussed. Please see our full disclaimers here.